Analysis of Accounting Theory and Governance: A Case Study Report

VerifiedAdded on 2020/03/16

|11

|3725

|32

Report

AI Summary

This report delves into accounting theory and governance, analyzing financial statements and executive remuneration through case studies. It examines the financial performance of Wesfarmers Limited, adhering to ASIC guidelines for investment analysis. The report explores key financial figures like profit after tax, earnings per share, and dividends, alongside management opinions. It assesses the company's financial health and potential as an investment. Additionally, the report investigates executive remuneration practices, particularly in the United States, evaluating the effectiveness of reforms and the role of taxation laws. The report concludes with recommendations based on the findings.

Accounting theory and governance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Summary of Case Studies..........................................................................................................3

Case Study 1...............................................................................................................................3

Analysis of Annual Report (Company Name: Wesfarmers)......................................................3

Examining figures in financial statements.............................................................................3

Important Financial Figures in Understanding the Financial Performance of the Company.4

Management Opinion in the Report about the Financial Figures...........................................5

Assessment of Financial Report in relation to Management Opinion....................................6

Analysis of the Wesfarmers as the potential investment........................................................7

Case Study B..............................................................................................................................8

Recent Changes for Addressing Executive Remuneration in the United States....................8

Effectiveness of reforms on the Shareholders Assumptions to Act.......................................8

Role of Taxation laws and Denying Contract Adoption for Addressing Executive

Remuneration.........................................................................................................................9

Conclusion................................................................................................................................10

Recommendations....................................................................................................................10

References................................................................................................................................11

2

Introduction................................................................................................................................3

Summary of Case Studies..........................................................................................................3

Case Study 1...............................................................................................................................3

Analysis of Annual Report (Company Name: Wesfarmers)......................................................3

Examining figures in financial statements.............................................................................3

Important Financial Figures in Understanding the Financial Performance of the Company.4

Management Opinion in the Report about the Financial Figures...........................................5

Assessment of Financial Report in relation to Management Opinion....................................6

Analysis of the Wesfarmers as the potential investment........................................................7

Case Study B..............................................................................................................................8

Recent Changes for Addressing Executive Remuneration in the United States....................8

Effectiveness of reforms on the Shareholders Assumptions to Act.......................................8

Role of Taxation laws and Denying Contract Adoption for Addressing Executive

Remuneration.........................................................................................................................9

Conclusion................................................................................................................................10

Recommendations....................................................................................................................10

References................................................................................................................................11

2

Introduction

Financial knowledge has been a must in order to take the review of the company

financial performance. As the investors it is not possible to review the whole business

performance and to take decisions to invest in the various choices of investment options. In

this regards Australia Securities and Investment Commission (ASIC) has provided 10 major

points that every investors need to undertake before making the decision to invest in any

company. All these points help investors to analyze the performance of the company and to

come with the proper choice. All these points are defined in detail and are really helpful for

the investors. In this report in order to explain all these points a case study 1 has been

undertaken and various questions to case study has been answered. For case study company

called Wesfarmers has been taken to explain the case study questions.

Executive remuneration is always the concern for the stakeholders as their pay

increase year to year even in the situation of financial crises. In order to explain the reform

undertaken to make changes on how the remuneration of the top management has to be

calculated, the case study 2 has been taken and various questions has been answered.

Summary of Case Studies

Case Study 1: This study provides the 10 major points that every investors must

review in context of any company chosen for investment purpose before making the

decision of investment. In this regard Wesfarmers has been selected to explain the

procedure.

Case Study 2: This study discusses the issues with the excessive executive

remuneration in the United States and reforms to make changes in the calculation of

the executive remuneration.

Case Study 1

Analysis of Annual Report (Company Name: Wesfarmers)

Examining figures in financial statements

The financial statements developed by an entity aims to reflects its financial

performance for supporting the decision-making of end-users. In this context, the ASIC

(Australian Securities Investment Commission) has provided suggestions to the non-

3

Financial knowledge has been a must in order to take the review of the company

financial performance. As the investors it is not possible to review the whole business

performance and to take decisions to invest in the various choices of investment options. In

this regards Australia Securities and Investment Commission (ASIC) has provided 10 major

points that every investors need to undertake before making the decision to invest in any

company. All these points help investors to analyze the performance of the company and to

come with the proper choice. All these points are defined in detail and are really helpful for

the investors. In this report in order to explain all these points a case study 1 has been

undertaken and various questions to case study has been answered. For case study company

called Wesfarmers has been taken to explain the case study questions.

Executive remuneration is always the concern for the stakeholders as their pay

increase year to year even in the situation of financial crises. In order to explain the reform

undertaken to make changes on how the remuneration of the top management has to be

calculated, the case study 2 has been taken and various questions has been answered.

Summary of Case Studies

Case Study 1: This study provides the 10 major points that every investors must

review in context of any company chosen for investment purpose before making the

decision of investment. In this regard Wesfarmers has been selected to explain the

procedure.

Case Study 2: This study discusses the issues with the excessive executive

remuneration in the United States and reforms to make changes in the calculation of

the executive remuneration.

Case Study 1

Analysis of Annual Report (Company Name: Wesfarmers)

Examining figures in financial statements

The financial statements developed by an entity aims to reflects its financial

performance for supporting the decision-making of end-users. In this context, the ASIC

(Australian Securities Investment Commission) has provided suggestions to the non-

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

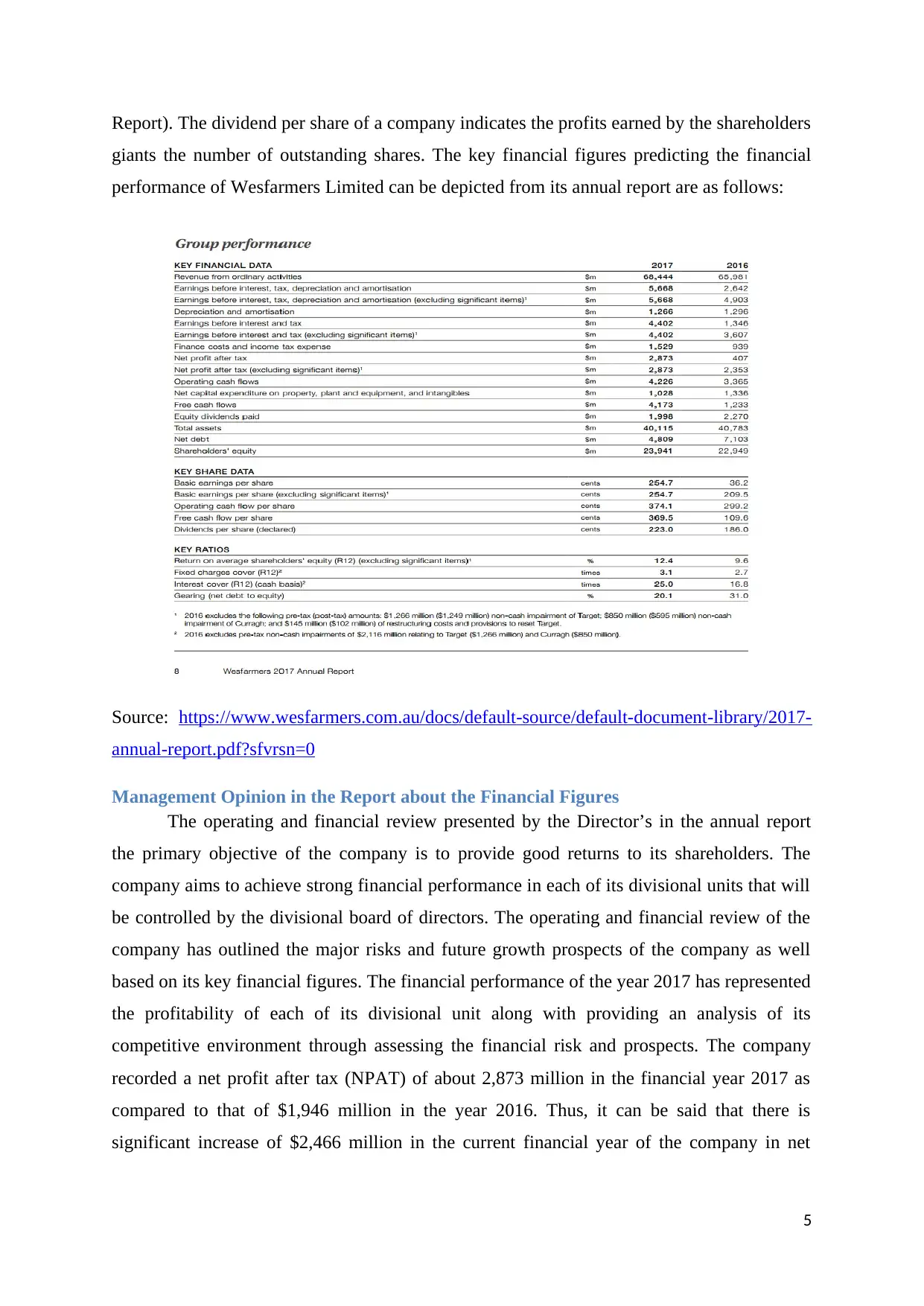

professional investors for evaluating the financial performance of a company through its

financial statements analysis. The suggestions are provided on ASIC for protecting the

interests of investors so that accurately interprets the financial information for making

informed decisions for investing (Australia, 2011). The financial performance of Wesfarmers

Limited, Australian retail giant, can be based from the financial statements net figures of

income statement and balance sheet as per ASIC guidelines. The income statement analysis

has depicted that the company has recorded a net increase in its profit in the year 2017 as

compared to the financial year 2016. The underlying net profit has increased to 22.1 per cent

in the year 2017 and has reached to $2,873 million. The earnings per share have increased to

21.6 per cent and return on equity has reported an increase to about 12.4 per cent in the year

2017 as compared to the previous financial year. The increased profitability of the company

has resulted in raising the dividend per year from $1.86 per share to $2.23 per share in the

year 2017 (Wesfarmers 2017: Annual Report). The increased cash inflow of the company on

account of its improved return on capital has helped in to expand its business operations. As

reflected from the director’s report of the company, its improved financial performance has

resulted from its recent conglomerate structure. The company is presently emphasizing on its

strategy of providing improved return to shareholders through realizing larger returns form its

industrial businesses in Kmart and Bunnings.

Important Financial Figures in Understanding the Financial Performance of the

Company

As analyzed from the case study, the ASIC has regarded the financial figures

disclosed in the director’s report in order to gain an insight into the profit or loss realized by a

company. The directors of Wesfarmers have also discussed the financial performance of the

company in the annual report through the help of some key financial figures (Hussey and

Ong, 2005). The financial figures include profit after tax, earnings per share, return on equity

and dividend per share. The financial figure relating to profit after tax depicts to the investors

regarding the percentage of money earned on per dollar of revenue. The investors can gain

an insight into the net profit realized by a company after meeting its all tax related

expenditure. It enables the investors to analyze the profitability of a company without the

impact of operating leverage thus the investors can actually predict its real financial

condition. The earnings per share depict the amount of money earned by a company per every

outstanding share of stock. It helps the investors to predict the financial profits that a

company can provide to its shareholders. The return on equity provides a measure of the

profitability of a company in comparison to the net investment (Wesfarmers 2017: Annual

4

financial statements analysis. The suggestions are provided on ASIC for protecting the

interests of investors so that accurately interprets the financial information for making

informed decisions for investing (Australia, 2011). The financial performance of Wesfarmers

Limited, Australian retail giant, can be based from the financial statements net figures of

income statement and balance sheet as per ASIC guidelines. The income statement analysis

has depicted that the company has recorded a net increase in its profit in the year 2017 as

compared to the financial year 2016. The underlying net profit has increased to 22.1 per cent

in the year 2017 and has reached to $2,873 million. The earnings per share have increased to

21.6 per cent and return on equity has reported an increase to about 12.4 per cent in the year

2017 as compared to the previous financial year. The increased profitability of the company

has resulted in raising the dividend per year from $1.86 per share to $2.23 per share in the

year 2017 (Wesfarmers 2017: Annual Report). The increased cash inflow of the company on

account of its improved return on capital has helped in to expand its business operations. As

reflected from the director’s report of the company, its improved financial performance has

resulted from its recent conglomerate structure. The company is presently emphasizing on its

strategy of providing improved return to shareholders through realizing larger returns form its

industrial businesses in Kmart and Bunnings.

Important Financial Figures in Understanding the Financial Performance of the

Company

As analyzed from the case study, the ASIC has regarded the financial figures

disclosed in the director’s report in order to gain an insight into the profit or loss realized by a

company. The directors of Wesfarmers have also discussed the financial performance of the

company in the annual report through the help of some key financial figures (Hussey and

Ong, 2005). The financial figures include profit after tax, earnings per share, return on equity

and dividend per share. The financial figure relating to profit after tax depicts to the investors

regarding the percentage of money earned on per dollar of revenue. The investors can gain

an insight into the net profit realized by a company after meeting its all tax related

expenditure. It enables the investors to analyze the profitability of a company without the

impact of operating leverage thus the investors can actually predict its real financial

condition. The earnings per share depict the amount of money earned by a company per every

outstanding share of stock. It helps the investors to predict the financial profits that a

company can provide to its shareholders. The return on equity provides a measure of the

profitability of a company in comparison to the net investment (Wesfarmers 2017: Annual

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report). The dividend per share of a company indicates the profits earned by the shareholders

giants the number of outstanding shares. The key financial figures predicting the financial

performance of Wesfarmers Limited can be depicted from its annual report are as follows:

Source: https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Management Opinion in the Report about the Financial Figures

The operating and financial review presented by the Director’s in the annual report

the primary objective of the company is to provide good returns to its shareholders. The

company aims to achieve strong financial performance in each of its divisional units that will

be controlled by the divisional board of directors. The operating and financial review of the

company has outlined the major risks and future growth prospects of the company as well

based on its key financial figures. The financial performance of the year 2017 has represented

the profitability of each of its divisional unit along with providing an analysis of its

competitive environment through assessing the financial risk and prospects. The company

recorded a net profit after tax (NPAT) of about 2,873 million in the financial year 2017 as

compared to that of $1,946 million in the year 2016. Thus, it can be said that there is

significant increase of $2,466 million in the current financial year of the company in net

5

giants the number of outstanding shares. The key financial figures predicting the financial

performance of Wesfarmers Limited can be depicted from its annual report are as follows:

Source: https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Management Opinion in the Report about the Financial Figures

The operating and financial review presented by the Director’s in the annual report

the primary objective of the company is to provide good returns to its shareholders. The

company aims to achieve strong financial performance in each of its divisional units that will

be controlled by the divisional board of directors. The operating and financial review of the

company has outlined the major risks and future growth prospects of the company as well

based on its key financial figures. The financial performance of the year 2017 has represented

the profitability of each of its divisional unit along with providing an analysis of its

competitive environment through assessing the financial risk and prospects. The company

recorded a net profit after tax (NPAT) of about 2,873 million in the financial year 2017 as

compared to that of $1,946 million in the year 2016. Thus, it can be said that there is

significant increase of $2,466 million in the current financial year of the company in net

5

profit after tax. The cash flows have also increased from $861 million to $4,226 million in

the year 2017 (Wesfarmers 2017: Annual Report).

The increase in operational cash inflows indicates the higher earnings growth and

adequate managing and controlling of each inventory in all of its retail segments. There is

also a decrease in the capital expenditure of the company in the year 2017 to $218 million as

compared to $1,681 million in the year 2016. As per the director’s review, the decrease in the

capital expenditure is due to fewer openings of its retail stores and thus reduction in the

operational expenditure across its industrial divisions. The company also has realized

proceeds of about $947 million due to divestment of receivables from its Coles divisional

unit. The balance sheet of the company has also strengthened mainly due to reduction in the

net financial debt that includes interest rate swap assets to about $4,321 million in year 2017

as compared to $2,216 million in the year 2016. Also, there is a significant reduction in the

financial cost of the company to about 14.3 per cent from that of the previous year. The

management of the company has regarded the increase in its operating cash flows and return

on equity on account of its adequate conglomerate structure and its emphasis on improving

the cash generation and capital efficiency (Wesfarmers 2017: Annual Report).

Assessment of Financial Report in relation to Management Opinion

Management has elaborated the financial performance of the company through using

the graphs and charts. As per the ASIC reports it is essential to examine the management

viewpoint on the performance of the company and what actually has been reported in the

financial statements prepared. For instance, the management of the Wesfarmers has point that

the in the current year (2016-17) the profitability performance of the company has been

increased and they are paying good returns to their shareholder’s. There is high amount of

increase in the revenue of the company due to improvements made in retail and industrial

business. It has been told by the managing director that cash generation was quite strong that

reflects the company value to increase the return on capital invested in the business. Finance

director has elaborated the operating financial position of the different units in the

Wesfarmers and according to the report the net profit after tax has been $2873 million AUD

which itself a record for the company (Dagwell, Wines and Lambert, 2015). On

reinvestigating whole financial statements it has been found that there are no such

discrepancies in the management disclosures of the financial performance and that reported

under the audited financial statements. So it can be said that there is no change in the

financial performance as reported by the management personals and as described in the

6

the year 2017 (Wesfarmers 2017: Annual Report).

The increase in operational cash inflows indicates the higher earnings growth and

adequate managing and controlling of each inventory in all of its retail segments. There is

also a decrease in the capital expenditure of the company in the year 2017 to $218 million as

compared to $1,681 million in the year 2016. As per the director’s review, the decrease in the

capital expenditure is due to fewer openings of its retail stores and thus reduction in the

operational expenditure across its industrial divisions. The company also has realized

proceeds of about $947 million due to divestment of receivables from its Coles divisional

unit. The balance sheet of the company has also strengthened mainly due to reduction in the

net financial debt that includes interest rate swap assets to about $4,321 million in year 2017

as compared to $2,216 million in the year 2016. Also, there is a significant reduction in the

financial cost of the company to about 14.3 per cent from that of the previous year. The

management of the company has regarded the increase in its operating cash flows and return

on equity on account of its adequate conglomerate structure and its emphasis on improving

the cash generation and capital efficiency (Wesfarmers 2017: Annual Report).

Assessment of Financial Report in relation to Management Opinion

Management has elaborated the financial performance of the company through using

the graphs and charts. As per the ASIC reports it is essential to examine the management

viewpoint on the performance of the company and what actually has been reported in the

financial statements prepared. For instance, the management of the Wesfarmers has point that

the in the current year (2016-17) the profitability performance of the company has been

increased and they are paying good returns to their shareholder’s. There is high amount of

increase in the revenue of the company due to improvements made in retail and industrial

business. It has been told by the managing director that cash generation was quite strong that

reflects the company value to increase the return on capital invested in the business. Finance

director has elaborated the operating financial position of the different units in the

Wesfarmers and according to the report the net profit after tax has been $2873 million AUD

which itself a record for the company (Dagwell, Wines and Lambert, 2015). On

reinvestigating whole financial statements it has been found that there are no such

discrepancies in the management disclosures of the financial performance and that reported

under the audited financial statements. So it can be said that there is no change in the

financial performance as reported by the management personals and as described in the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statements of the company. There is major reason behind similarity of management

disclosure and what has been disclosed by the audited reports of the company (Wesfarmers

2017: Annual Report). The reason is such that annual reports are prepared after financial

statements have been audited and verified by the top management. Top management people

provide their statements on the financial performance of the company after reviewing the

audited reports of the financial statements so that true and fair picture of the financial

statements can be presented in front of the users of the annual report (Henderson, 2015).

Analysis of the Wesfarmers as the potential investment

In order to analyze the company for its potential investment it is necessary to make

the detailed interpretation of the financial performance so that investors can use such

information to make the judgment regarding their investment in the company. Wesfarmers

has varied potential that can attract the investors (Horngren, 2012). Wesfarmers works in

different category of business such as retail segment, industry segment, home improvement

segment and many others that made a different from other to make the investment. Company

has diverse business operations and high growth balance sheet. The retail segment of the

company has foreseen major improvement in recent years and it has been monitored by

various changed made. Continuous improvements in merchandising and service; increase in

customer satisfaction through regular change in interaction at the stores and online purchase;

and investment proposals are some of the major highlights in the change of retail segment of

the Wesfarmers (Bazley, Hancock and Robinson, 2014).

The whole group cash generation power has increased out rightly that has provided

the management to manage the capital structure and to make the position of the balance sheet

strong. Wesfarmers continuously take opportunities to create and to improve the

shareholder’s wealth through proactively management of the portfolio and reviewing the

strategies regularly so that business resources are put in high end growth segments of the

company.

Coles the major segment of the business has faced high competition and pressure of

increase sales margin. In this action, the plan is to focus on the budgeted plans and to further

enhance the quality of the fresh offer and to improve the merchandising and availability,

through driving the operational efficiencies in order to the support investments in the various

services and values. There is expectation and budget driven approach to increase the

7

disclosure and what has been disclosed by the audited reports of the company (Wesfarmers

2017: Annual Report). The reason is such that annual reports are prepared after financial

statements have been audited and verified by the top management. Top management people

provide their statements on the financial performance of the company after reviewing the

audited reports of the financial statements so that true and fair picture of the financial

statements can be presented in front of the users of the annual report (Henderson, 2015).

Analysis of the Wesfarmers as the potential investment

In order to analyze the company for its potential investment it is necessary to make

the detailed interpretation of the financial performance so that investors can use such

information to make the judgment regarding their investment in the company. Wesfarmers

has varied potential that can attract the investors (Horngren, 2012). Wesfarmers works in

different category of business such as retail segment, industry segment, home improvement

segment and many others that made a different from other to make the investment. Company

has diverse business operations and high growth balance sheet. The retail segment of the

company has foreseen major improvement in recent years and it has been monitored by

various changed made. Continuous improvements in merchandising and service; increase in

customer satisfaction through regular change in interaction at the stores and online purchase;

and investment proposals are some of the major highlights in the change of retail segment of

the Wesfarmers (Bazley, Hancock and Robinson, 2014).

The whole group cash generation power has increased out rightly that has provided

the management to manage the capital structure and to make the position of the balance sheet

strong. Wesfarmers continuously take opportunities to create and to improve the

shareholder’s wealth through proactively management of the portfolio and reviewing the

strategies regularly so that business resources are put in high end growth segments of the

company.

Coles the major segment of the business has faced high competition and pressure of

increase sales margin. In this action, the plan is to focus on the budgeted plans and to further

enhance the quality of the fresh offer and to improve the merchandising and availability,

through driving the operational efficiencies in order to the support investments in the various

services and values. There is expectation and budget driven approach to increase the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of the Home Improvement segment of the business (Wesfarmers 2017: Annual

Report).

Overall analysis of the part performance of the company shows that company has

done exceptional well in year 2017 as compare to other previous year and it makes a valid

choice for the investors to make investment in such growing company. The growth of the

company is marked with many potential and valid proofs such as increase in dividend payout,

high cash generation capacity, solid capital structure and plan to improve the further business

segment. This made the Wesfarmers a strong competitor for the other companies in same

segment and also for companies that are in competition as a potential investment for the

investors (Wesfarmers 2017: Annual Report).

Case Study B

Recent Changes for Addressing Executive Remuneration in the United States

The given article ‘Reining in Executive Pay’ has addressed the need for developing

implementing laws and regulations for addressing the excessive remuneration of the

executives. In this context, the article has particularly examined the excessive pay provided to

the executives in the United States. The executives are realizing higher pay in the United

States as indicated from the fact that there is increase of about 42 per cent executive

remuneration in the year 2008 despite of the collapse of the financial sector of the country.

There is significant growth in the executive pay over the consecutive years and thus there is

higher need for developing financial reforms in relation to monitoring of pay of executives.

In this context, the U.S government ha introduced a legislation knows as shareholder ‘say on

pay’ to be followed by all the publicly traded U.S companies (Executive Compensation and

Incentives, 2006). As per the legislation, the shareholders have a right to decide over the

matters relating to executive remuneration that should be followed by the Board of Directors.

In addition to this, the law has also stated that shareholders as per the SEC regulations can

appoint their own directors candidates through ballots if the company’s present directors does

not approve their decisions. Also, it is necessary for the U.S. companies to maintain the

independency of the board of directors in appointing and developing the remuneration

committee. The Board of Directors must also ensure that the corporations disclose all the

relevant information regarding the executive pay and its relation o financial performance. The

reforms introduced by the government in relation to monitor and control the excessive pay

provided to the executive’s aims at preventing the increased rewards to executives. This is

necessary because the increased rewards provided to executives can drive the misconduct in

manager’s behaviour by manipulating the financial information for achieving higher pays

when it is linked to the company’s financial performance.

8

Report).

Overall analysis of the part performance of the company shows that company has

done exceptional well in year 2017 as compare to other previous year and it makes a valid

choice for the investors to make investment in such growing company. The growth of the

company is marked with many potential and valid proofs such as increase in dividend payout,

high cash generation capacity, solid capital structure and plan to improve the further business

segment. This made the Wesfarmers a strong competitor for the other companies in same

segment and also for companies that are in competition as a potential investment for the

investors (Wesfarmers 2017: Annual Report).

Case Study B

Recent Changes for Addressing Executive Remuneration in the United States

The given article ‘Reining in Executive Pay’ has addressed the need for developing

implementing laws and regulations for addressing the excessive remuneration of the

executives. In this context, the article has particularly examined the excessive pay provided to

the executives in the United States. The executives are realizing higher pay in the United

States as indicated from the fact that there is increase of about 42 per cent executive

remuneration in the year 2008 despite of the collapse of the financial sector of the country.

There is significant growth in the executive pay over the consecutive years and thus there is

higher need for developing financial reforms in relation to monitoring of pay of executives.

In this context, the U.S government ha introduced a legislation knows as shareholder ‘say on

pay’ to be followed by all the publicly traded U.S companies (Executive Compensation and

Incentives, 2006). As per the legislation, the shareholders have a right to decide over the

matters relating to executive remuneration that should be followed by the Board of Directors.

In addition to this, the law has also stated that shareholders as per the SEC regulations can

appoint their own directors candidates through ballots if the company’s present directors does

not approve their decisions. Also, it is necessary for the U.S. companies to maintain the

independency of the board of directors in appointing and developing the remuneration

committee. The Board of Directors must also ensure that the corporations disclose all the

relevant information regarding the executive pay and its relation o financial performance. The

reforms introduced by the government in relation to monitor and control the excessive pay

provided to the executive’s aims at preventing the increased rewards to executives. This is

necessary because the increased rewards provided to executives can drive the misconduct in

manager’s behaviour by manipulating the financial information for achieving higher pays

when it is linked to the company’s financial performance.

8

Effectiveness of reforms on the Shareholders Assumptions to Act

The article has discussed the reforms introduced by the U.S. for monitoring the pay

structure of executives in order to ensure that executives does not receive higher rewards that

drive them to conduct unethical practices for achieving higher benefits. The reforms

introduced by the U.S. government known as shareholder ‘say on pay’ has stated that all the

public-listed companies in the country will decide the remuneration of the executives based

on the shareholders opinions. Thus, as such it can be said that the effectiveness of the reforms

is based on the assumptions that the shareholders will act ethically and right in deciding over

the matters of executive remuneration (McDonnell, 2008). However, there are some barriers

to effective shareholder control over the executive remuneration. The major obstacle faced by

the Board of the company in this regard is developing an effective strategy for creating an

effective communication channel for disseminating the information to the shareholders.

Thus, as such business entities need to induce changes in its business environment to promote

effective communication of all the information related to executive remuneration policies to

the shareholders. Also, it can be argued by the contract theory that corporations have

contractual obligations with the shareholders and therefore they should act in favour of the

shareholders to provide them larger returns (Finance Committee, 2016). Thus, the

corporations can influence the decision-making power of shareholders in relation to executive

pay through promising them larger retunes. Thus, as such shareholders have profit interest in

the corporations and therefore the power provided to them for monitoring the executive pay

cannot be stated to be right and just. The independency of the shareholders in deciding over

the matters of executive remuneration is question of debate as stated in the present article.

Therefore, as discussed in the given article there is need for introduction of more better

regulations in the U.S. that provides authority to all the stakeholders of a busies corporation

not only to shareholders for deciding and monitoring the executive remuneration.

Role of Taxation laws and Denying Contract Adoption for Addressing Executive

Remuneration

The article has stated that shareholders decision in relation to executive remuneration

cannot be regarded to be accurate as it is based on assumptions that they will act ethical and

fair in deciding the executive pay. Thus, the article has stated that the reforms introduced

should provide authority to all the stakeholders including consumers, workers and all the

communities that are impacted by corporate operations. This is because the corporation’s

activities’ can put all its stakeholders to risk and therefore the responsibility of the executive

pay decisions should not be provided only to shareholders but to all the stakeholders. In this

context, the tax dollars paid by the general public should not help in subsidizing the executive

pay in excess. This can result in a significant reduction of millions form the income taxes that

corporations pay as excessive executive remuneration. In addition to this, there is need for

developing a federal contract with the companies that provides remuneration to their

executive 100 times more than that of their labour wages (Treanor, 2016). The contract would

help in reducing the economic inequality as the contract would require that business

companies in the U.S. should maintain a fair proportion of the remuneration between its

executive and workers and should provide the ratio between the CEO compensation and the

workers in their annual report as well. The introduction of such measures will help in

9

The article has discussed the reforms introduced by the U.S. for monitoring the pay

structure of executives in order to ensure that executives does not receive higher rewards that

drive them to conduct unethical practices for achieving higher benefits. The reforms

introduced by the U.S. government known as shareholder ‘say on pay’ has stated that all the

public-listed companies in the country will decide the remuneration of the executives based

on the shareholders opinions. Thus, as such it can be said that the effectiveness of the reforms

is based on the assumptions that the shareholders will act ethically and right in deciding over

the matters of executive remuneration (McDonnell, 2008). However, there are some barriers

to effective shareholder control over the executive remuneration. The major obstacle faced by

the Board of the company in this regard is developing an effective strategy for creating an

effective communication channel for disseminating the information to the shareholders.

Thus, as such business entities need to induce changes in its business environment to promote

effective communication of all the information related to executive remuneration policies to

the shareholders. Also, it can be argued by the contract theory that corporations have

contractual obligations with the shareholders and therefore they should act in favour of the

shareholders to provide them larger returns (Finance Committee, 2016). Thus, the

corporations can influence the decision-making power of shareholders in relation to executive

pay through promising them larger retunes. Thus, as such shareholders have profit interest in

the corporations and therefore the power provided to them for monitoring the executive pay

cannot be stated to be right and just. The independency of the shareholders in deciding over

the matters of executive remuneration is question of debate as stated in the present article.

Therefore, as discussed in the given article there is need for introduction of more better

regulations in the U.S. that provides authority to all the stakeholders of a busies corporation

not only to shareholders for deciding and monitoring the executive remuneration.

Role of Taxation laws and Denying Contract Adoption for Addressing Executive

Remuneration

The article has stated that shareholders decision in relation to executive remuneration

cannot be regarded to be accurate as it is based on assumptions that they will act ethical and

fair in deciding the executive pay. Thus, the article has stated that the reforms introduced

should provide authority to all the stakeholders including consumers, workers and all the

communities that are impacted by corporate operations. This is because the corporation’s

activities’ can put all its stakeholders to risk and therefore the responsibility of the executive

pay decisions should not be provided only to shareholders but to all the stakeholders. In this

context, the tax dollars paid by the general public should not help in subsidizing the executive

pay in excess. This can result in a significant reduction of millions form the income taxes that

corporations pay as excessive executive remuneration. In addition to this, there is need for

developing a federal contract with the companies that provides remuneration to their

executive 100 times more than that of their labour wages (Treanor, 2016). The contract would

help in reducing the economic inequality as the contract would require that business

companies in the U.S. should maintain a fair proportion of the remuneration between its

executive and workers and should provide the ratio between the CEO compensation and the

workers in their annual report as well. The introduction of such measures will help in

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

developing the strong corporate governance practices for curbing the excessive executive

remuneration (McDonnell, 2008).

Conclusion

It can be inferred from the overall analysis of the report that ASIC plays a major role

in protecting the investors interest through providing them suggestions to analyse the annual

report disclosures of various corporations. Also, the executive remuneration should not be

linked to the financial performance of a company as this can result in occurrence of

fraudulent financial activities in a business entity.

Recommendations

On the basis of the case study analysis, it is recommended to the investors that they

should consider the suggestions provided by the ASIC while analysing the annual report of

their selected company. This will help in securing the interests of amateur investors do not

possess adequate knowledge about the annual disclosures of a company. In addition to this, as

analysed from the second case study there is need for developing strong regulations that

provides more power to the stakeholders in deciding over the matters of executives

remuneration.

10

remuneration (McDonnell, 2008).

Conclusion

It can be inferred from the overall analysis of the report that ASIC plays a major role

in protecting the investors interest through providing them suggestions to analyse the annual

report disclosures of various corporations. Also, the executive remuneration should not be

linked to the financial performance of a company as this can result in occurrence of

fraudulent financial activities in a business entity.

Recommendations

On the basis of the case study analysis, it is recommended to the investors that they

should consider the suggestions provided by the ASIC while analysing the annual report of

their selected company. This will help in securing the interests of amateur investors do not

possess adequate knowledge about the annual disclosures of a company. In addition to this, as

analysed from the second case study there is need for developing strong regulations that

provides more power to the stakeholders in deciding over the matters of executives

remuneration.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Australia. 2011. Australian Corporations & Securities Legislation 2011: Corporations Act

2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Dagwell, R., Wines, G. and Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

Executive Compensation and Incentives. 2006. Retrieved 10 October, 2017 from

http://www.lse.ac.uk/fmg/researchProgrammes/corporateFinance/corporateGovernanc

e/pdf/executiveCompensationAndIncentives.pdf

Finance Committee. 2016. Recommendations and Decisions of the International Civil Service

Commission to the General Assembly (including Changes in Salary Scales and

Allowances). Retrieved 10 October, 2017 from http://www.fao.org/3/a-mq160e.pdf

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Hussey, R. and Ong, A. 2005. International Financial Reporting Standards Desk Reference:

Overview, Guide, and Dictionary. John Wiley & Sons.

McDonnell, B. 2008. Two Goals for Executive Compensation Reform. Retrieved 10 October,

2017 from http://scholarship.law.umn.edu/cgi/viewcontent.cgi?

article=1168&context=faculty_articles

Treanor, J. 2016. Pay ratios could be made public as part of executive salary reform.

Retrieved 10 October, 2017 from

https://www.theguardian.com/business/2016/jul/25/pay-ratios-could-be-made-public-

as-part-of-executive-salary-reform

Wesfarmers 2017 Annual Report. Retrieved 10 October, 2017 from

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

11

Australia. 2011. Australian Corporations & Securities Legislation 2011: Corporations Act

2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Dagwell, R., Wines, G. and Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

Executive Compensation and Incentives. 2006. Retrieved 10 October, 2017 from

http://www.lse.ac.uk/fmg/researchProgrammes/corporateFinance/corporateGovernanc

e/pdf/executiveCompensationAndIncentives.pdf

Finance Committee. 2016. Recommendations and Decisions of the International Civil Service

Commission to the General Assembly (including Changes in Salary Scales and

Allowances). Retrieved 10 October, 2017 from http://www.fao.org/3/a-mq160e.pdf

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Hussey, R. and Ong, A. 2005. International Financial Reporting Standards Desk Reference:

Overview, Guide, and Dictionary. John Wiley & Sons.

McDonnell, B. 2008. Two Goals for Executive Compensation Reform. Retrieved 10 October,

2017 from http://scholarship.law.umn.edu/cgi/viewcontent.cgi?

article=1168&context=faculty_articles

Treanor, J. 2016. Pay ratios could be made public as part of executive salary reform.

Retrieved 10 October, 2017 from

https://www.theguardian.com/business/2016/jul/25/pay-ratios-could-be-made-public-

as-part-of-executive-salary-reform

Wesfarmers 2017 Annual Report. Retrieved 10 October, 2017 from

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

11

1 out of 11

Related Documents

![Report: Contemporary Issues in Accounting - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzz%2F9509ff46c136422d929242036a52e1cb.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.