Analysis of Accounting Theory and Corporate Governance Report

VerifiedAdded on 2023/04/26

|10

|2368

|412

Report

AI Summary

This report delves into the intricate relationship between accounting theory and corporate governance, offering a comprehensive analysis of corporate governance practices. The report begins with a comparative analysis of Wesfarmers Limited and Boral Limited, evaluating their corporate governance disclosures based on the ASX Corporate Governance Council's principles. It then provides a detailed discussion on the critical roles corporate governance plays in accounting and business practices. The report explores the rules-based and principles-based approaches to corporate governance, highlighting the significance of ASIC and CLERP 9 in the Australian context. Furthermore, it emphasizes the importance of independent directors, ethical standards, and integrated reporting in strengthening corporate governance mechanisms. The report concludes by underscoring the need for continuous improvement and adaptation in corporate governance to ensure long-term sustainability and stakeholder trust. This report provides valuable insights for students seeking to understand the complexities of corporate governance and its impact on accounting practices.

Running head: ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Author’s Note

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Table of Contents

Answer to Part A........................................................................................................................2

Requirement 1........................................................................................................................2

Requirement 2........................................................................................................................2

Requirement 3........................................................................................................................2

Answer to Part B........................................................................................................................3

References..................................................................................................................................8

Table of Contents

Answer to Part A........................................................................................................................2

Requirement 1........................................................................................................................2

Requirement 2........................................................................................................................2

Requirement 3........................................................................................................................2

Answer to Part B........................................................................................................................3

References..................................................................................................................................8

2ACCOUNTING THEORY AND CORPORATE GOVERNANCE

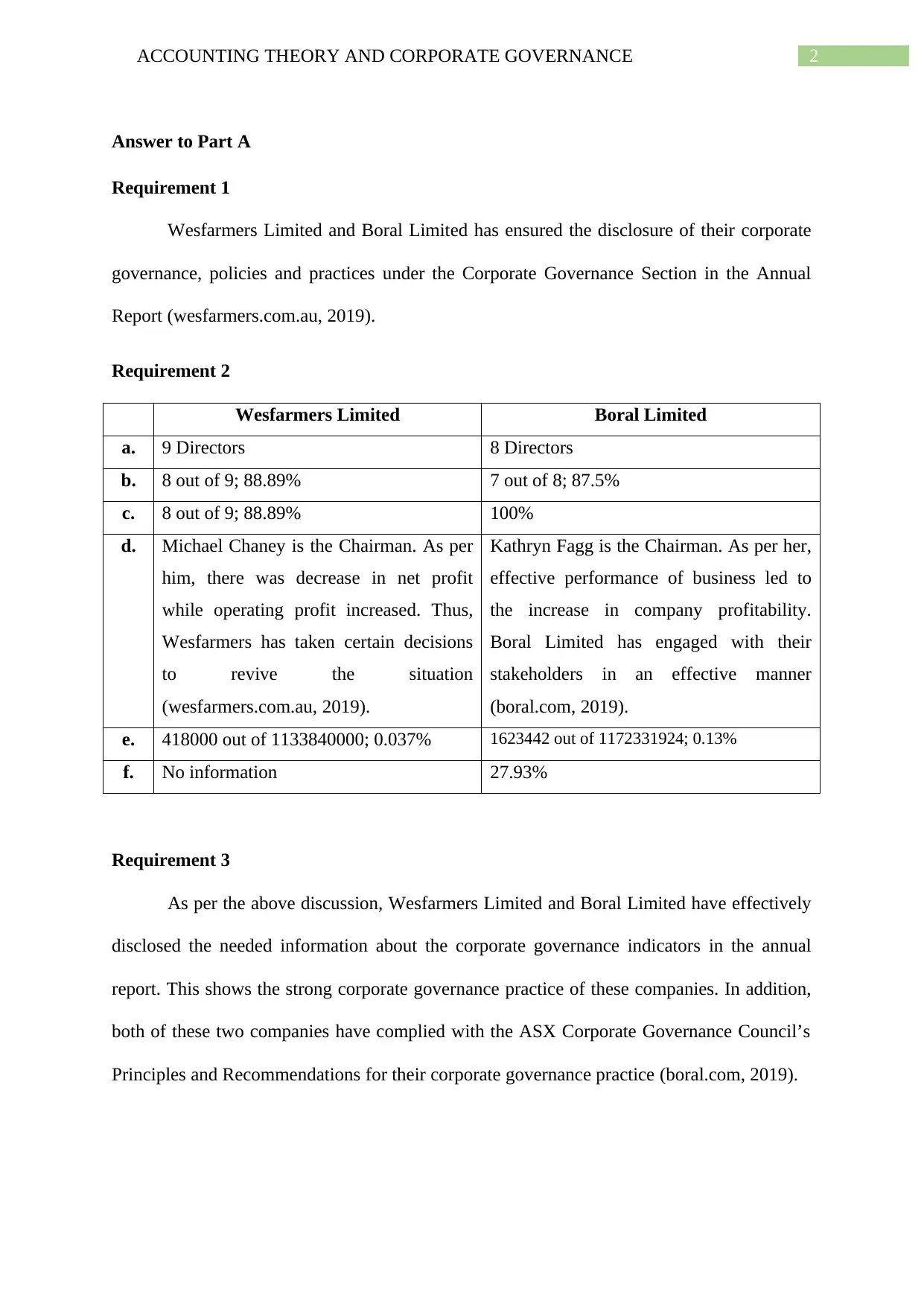

Answer to Part A

Requirement 1

Wesfarmers Limited and Boral Limited has ensured the disclosure of their corporate

governance, policies and practices under the Corporate Governance Section in the Annual

Report (wesfarmers.com.au, 2019).

Requirement 2

Wesfarmers Limited Boral Limited

a. 9 Directors 8 Directors

b. 8 out of 9; 88.89% 7 out of 8; 87.5%

c. 8 out of 9; 88.89% 100%

d. Michael Chaney is the Chairman. As per

him, there was decrease in net profit

while operating profit increased. Thus,

Wesfarmers has taken certain decisions

to revive the situation

(wesfarmers.com.au, 2019).

Kathryn Fagg is the Chairman. As per her,

effective performance of business led to

the increase in company profitability.

Boral Limited has engaged with their

stakeholders in an effective manner

(boral.com, 2019).

e. 418000 out of 1133840000; 0.037% 1623442 out of 1172331924; 0.13%

f. No information 27.93%

Requirement 3

As per the above discussion, Wesfarmers Limited and Boral Limited have effectively

disclosed the needed information about the corporate governance indicators in the annual

report. This shows the strong corporate governance practice of these companies. In addition,

both of these two companies have complied with the ASX Corporate Governance Council’s

Principles and Recommendations for their corporate governance practice (boral.com, 2019).

Answer to Part A

Requirement 1

Wesfarmers Limited and Boral Limited has ensured the disclosure of their corporate

governance, policies and practices under the Corporate Governance Section in the Annual

Report (wesfarmers.com.au, 2019).

Requirement 2

Wesfarmers Limited Boral Limited

a. 9 Directors 8 Directors

b. 8 out of 9; 88.89% 7 out of 8; 87.5%

c. 8 out of 9; 88.89% 100%

d. Michael Chaney is the Chairman. As per

him, there was decrease in net profit

while operating profit increased. Thus,

Wesfarmers has taken certain decisions

to revive the situation

(wesfarmers.com.au, 2019).

Kathryn Fagg is the Chairman. As per her,

effective performance of business led to

the increase in company profitability.

Boral Limited has engaged with their

stakeholders in an effective manner

(boral.com, 2019).

e. 418000 out of 1133840000; 0.037% 1623442 out of 1172331924; 0.13%

f. No information 27.93%

Requirement 3

As per the above discussion, Wesfarmers Limited and Boral Limited have effectively

disclosed the needed information about the corporate governance indicators in the annual

report. This shows the strong corporate governance practice of these companies. In addition,

both of these two companies have complied with the ASX Corporate Governance Council’s

Principles and Recommendations for their corporate governance practice (boral.com, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Answer to Part B

Introduction

In today’s business world, companies are giving major importance to the various

aspects of corporate governance due to the fact that the presence of an effective corporate

governance system ensures the governance of the business operations of the companies

(Cheffins, 2013). It implies that in the presence of the necessary adherence with the various

rules and regulations of corporate governance, business organizations become able in

effectively directing as well as controlling the crucial aspects of their business. For this

reason, it is needed for all the companies to ensure the presence of an effective corporate

governance system within their organizations as they can become beneficial from different

angles (ArAs, 2016). The intention of this report is to discuss about the roles that corporate

governance play in the accounting as well as other practices in the companies.

Discussion

In order to ensure the success of the businesses, there must be the needed control and

directions in them which an effective corporate governance system delivers; and the

companies can suffer from corporate collapses in the absence of the same (Bottomley, 2016).

Thus, the principles of corporate governance demand certain commitments from the

companies. First, the probability of corporate collapses increases when the companies do not

have the adequate number of external directors in the Board. It is considered that the internal

directors of the companies often less objective and less independent when taking the business

decisions (Bottomley, 2016). Second, the companies are needed to avoid the twin role of

company CEO that is called the CEO Duality as the two different roles of the same individual

is not good for the company’s success. Third, the companies are needed to ensure the

employment of effective corporate governance in the remuneration of the executives in order

Answer to Part B

Introduction

In today’s business world, companies are giving major importance to the various

aspects of corporate governance due to the fact that the presence of an effective corporate

governance system ensures the governance of the business operations of the companies

(Cheffins, 2013). It implies that in the presence of the necessary adherence with the various

rules and regulations of corporate governance, business organizations become able in

effectively directing as well as controlling the crucial aspects of their business. For this

reason, it is needed for all the companies to ensure the presence of an effective corporate

governance system within their organizations as they can become beneficial from different

angles (ArAs, 2016). The intention of this report is to discuss about the roles that corporate

governance play in the accounting as well as other practices in the companies.

Discussion

In order to ensure the success of the businesses, there must be the needed control and

directions in them which an effective corporate governance system delivers; and the

companies can suffer from corporate collapses in the absence of the same (Bottomley, 2016).

Thus, the principles of corporate governance demand certain commitments from the

companies. First, the probability of corporate collapses increases when the companies do not

have the adequate number of external directors in the Board. It is considered that the internal

directors of the companies often less objective and less independent when taking the business

decisions (Bottomley, 2016). Second, the companies are needed to avoid the twin role of

company CEO that is called the CEO Duality as the two different roles of the same individual

is not good for the company’s success. Third, the companies are needed to ensure the

employment of effective corporate governance in the remuneration of the executives in order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CORPORATE GOVERNANCE

to ensure the distribution of the justified amount of remuneration to the directors as per their

performance (Bottomley, 2016). Thus, the business organizations can avoid corporate failure

by covering these aspects through corporate governance system.

For the implementation of an effective corporate governance system, the companies

are needed to select the appropriate approach while considering the necessary aspects of their

business. Two popular approaches of corporate governance are Rules-based approach and

Principles-based approach of corporate governance (Filatotchev & Nakajima, 2014). Rules-

based approach of corporate governance is developed on the concept that the presence of

certain laws and regulations put the obligation on the firms to ensure the necessary adherence

with the corporate governance principles and the firms must comply with these principles.

This ensures adhering to the minimum requirements of corporate governance by the firms.

However, the principles-based approach of corporate governance is developed on the concept

that the companies are needed to adhere to the different principles of corporate governance as

per their situation as same principles are never adequate for all the companies (Filatotchev &

Nakajima, 2014). This is a famous alternative solution of the rules-based approach of

corporate governance.

There is a strict obligation on the Australian companies to comply with the necessary

principles and standards of corporate governance; and these principles and standards can be

found in the Australian Securities and Investment Commission (ASIC) and CLERP 9. The

roles of these two in corporate governance are discussed below.

ASIC believes that the presence of effective corporate governance can positively

influence firms’ performance. For this, ASIC has taken into account the necessary aspects of

corporate governance with the aim to provide the companies with the required guidelines and

regulations that they must adhere to for ensuring organizations success (Bavoso, 2014). Thus,

to ensure the distribution of the justified amount of remuneration to the directors as per their

performance (Bottomley, 2016). Thus, the business organizations can avoid corporate failure

by covering these aspects through corporate governance system.

For the implementation of an effective corporate governance system, the companies

are needed to select the appropriate approach while considering the necessary aspects of their

business. Two popular approaches of corporate governance are Rules-based approach and

Principles-based approach of corporate governance (Filatotchev & Nakajima, 2014). Rules-

based approach of corporate governance is developed on the concept that the presence of

certain laws and regulations put the obligation on the firms to ensure the necessary adherence

with the corporate governance principles and the firms must comply with these principles.

This ensures adhering to the minimum requirements of corporate governance by the firms.

However, the principles-based approach of corporate governance is developed on the concept

that the companies are needed to adhere to the different principles of corporate governance as

per their situation as same principles are never adequate for all the companies (Filatotchev &

Nakajima, 2014). This is a famous alternative solution of the rules-based approach of

corporate governance.

There is a strict obligation on the Australian companies to comply with the necessary

principles and standards of corporate governance; and these principles and standards can be

found in the Australian Securities and Investment Commission (ASIC) and CLERP 9. The

roles of these two in corporate governance are discussed below.

ASIC believes that the presence of effective corporate governance can positively

influence firms’ performance. For this, ASIC has taken into account the necessary aspects of

corporate governance with the aim to provide the companies with the required guidelines and

regulations that they must adhere to for ensuring organizations success (Bavoso, 2014). Thus,

5ACCOUNTING THEORY AND CORPORATE GOVERNANCE

the companies are needed to publish information about the responsibilities and obligations of

the directors of the companies and the information about the risk management mechanism

that is majorly useful information for different classes of stakeholders of the companies. In

order to know about the major corporate governance issues that the companies face, ASIC

has taken the initiative to engage with the firms’ stakeholders via meetings and others. For

this reason, ASIC has introduced the necessary regulations and principles of corporate

governance on different aspects like management of conflict, risk management, directors’

remuneration, stakeholder’s engagement and others (Bavoso, 2014).

Same as ASIC, CLERP 9 also plays an important role in the establishment of

effective corporate governance mechanism within the organizations by taking into

consideration certain advanced and additional issues of corporate governance. CLERP 9 is

essential for establishing a connection between corporate governance and financial reporting

of the firms (Faghani, Monem & Ng, 2015). There are certain new and essential requirements

of corporate governance in CLERP 9; they are continuous disclosure of the additional

information related to corporate governance, the changes in the financial reporting and audit

procedures of the firms, the facts of Management Discussion and Analysis, the required

obligation of licensing in the aspect of financial reporting, the required provisions for

fundraising, additional disclosure of directors’ remuneration and others. All these are the

necessary aspects of corporate governance (Faghani, Monem & Ng, 2015).

In order to strengthen the system of corporate governance within the organizations,

the companies are needed to ensure recruiting adequate number of independent directors who

do not have any prior connection with the companies (Ye, 2014). An independent director

can well be regarded as the company’s guide because of their prime role to ensure the

necessary development in the standards and trustworthiness of corporate governance system.

In addition, management of business risks is another major duty of the independent directors.

the companies are needed to publish information about the responsibilities and obligations of

the directors of the companies and the information about the risk management mechanism

that is majorly useful information for different classes of stakeholders of the companies. In

order to know about the major corporate governance issues that the companies face, ASIC

has taken the initiative to engage with the firms’ stakeholders via meetings and others. For

this reason, ASIC has introduced the necessary regulations and principles of corporate

governance on different aspects like management of conflict, risk management, directors’

remuneration, stakeholder’s engagement and others (Bavoso, 2014).

Same as ASIC, CLERP 9 also plays an important role in the establishment of

effective corporate governance mechanism within the organizations by taking into

consideration certain advanced and additional issues of corporate governance. CLERP 9 is

essential for establishing a connection between corporate governance and financial reporting

of the firms (Faghani, Monem & Ng, 2015). There are certain new and essential requirements

of corporate governance in CLERP 9; they are continuous disclosure of the additional

information related to corporate governance, the changes in the financial reporting and audit

procedures of the firms, the facts of Management Discussion and Analysis, the required

obligation of licensing in the aspect of financial reporting, the required provisions for

fundraising, additional disclosure of directors’ remuneration and others. All these are the

necessary aspects of corporate governance (Faghani, Monem & Ng, 2015).

In order to strengthen the system of corporate governance within the organizations,

the companies are needed to ensure recruiting adequate number of independent directors who

do not have any prior connection with the companies (Ye, 2014). An independent director

can well be regarded as the company’s guide because of their prime role to ensure the

necessary development in the standards and trustworthiness of corporate governance system.

In addition, management of business risks is another major duty of the independent directors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CORPORATE GOVERNANCE

It is needed for the independent directors to assess the situation of the companies with the aim

to ensure whether there is need for setting up additional committees or not. Hence, it can be

said in the presence of all these reasons that independent directors are the watchdogs of the

corporate governance that ensures the presence of robust corporate governance mechanism

(Ye, 2014).

The inclusion of the necessary ethical standards in the corporate governance

mechanism is needed for the overall improvements of the businesses. There can be the

development of wariness among the company directors in the application of corporate

governance mechanism and for this reason, all the business decisions need to be taken by

considering ethics and prosperity. One important aspect is that the senior managements of the

companies are not able to use illegal means for achieving the organizational goals and

objectives in the presence of effective ethical standards in corporate governance. For this, the

combination of ethical standards and corporate governance is needed for ensuring long-term

sustainability of the businesses (Boatright, 2017). Moreover, required transparency,

accountability and responsibility can be brought into the businesses by adhering with the

required ethical standards in corporate governance. Illegal draining of funds and corruption

can be demolished from the businesses with the help of ethical corporate governance

practices.

Like ethics, the merger between the corporate governance practices with integrated

reporting is needed for the companies to establish a sense of trust and faith with the key

stakeholders of the business organizations. In addition, it connects the key stakeholders with

the senior management teams of the firms. Integrated thinking is the basis of integrated

reporting and it helps in improving the internal processes of the firms to cater to the needs of

the key stakeholders (Eccles & Serafeim, 2015). At the same time, the corporate governance

practices of the firms can be enhanced in the presence of interacted reporting as it implants

It is needed for the independent directors to assess the situation of the companies with the aim

to ensure whether there is need for setting up additional committees or not. Hence, it can be

said in the presence of all these reasons that independent directors are the watchdogs of the

corporate governance that ensures the presence of robust corporate governance mechanism

(Ye, 2014).

The inclusion of the necessary ethical standards in the corporate governance

mechanism is needed for the overall improvements of the businesses. There can be the

development of wariness among the company directors in the application of corporate

governance mechanism and for this reason, all the business decisions need to be taken by

considering ethics and prosperity. One important aspect is that the senior managements of the

companies are not able to use illegal means for achieving the organizational goals and

objectives in the presence of effective ethical standards in corporate governance. For this, the

combination of ethical standards and corporate governance is needed for ensuring long-term

sustainability of the businesses (Boatright, 2017). Moreover, required transparency,

accountability and responsibility can be brought into the businesses by adhering with the

required ethical standards in corporate governance. Illegal draining of funds and corruption

can be demolished from the businesses with the help of ethical corporate governance

practices.

Like ethics, the merger between the corporate governance practices with integrated

reporting is needed for the companies to establish a sense of trust and faith with the key

stakeholders of the business organizations. In addition, it connects the key stakeholders with

the senior management teams of the firms. Integrated thinking is the basis of integrated

reporting and it helps in improving the internal processes of the firms to cater to the needs of

the key stakeholders (Eccles & Serafeim, 2015). At the same time, the corporate governance

practices of the firms can be enhanced in the presence of interacted reporting as it implants

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CORPORATE GOVERNANCE

both the financial as well as non-financial information of the business organizations. This

whole aspect contributes towards the better resource allocation, better decisions and better

actions for the companies in order to set up long-term sustainable value. Moreover, the

companies become able in identifying the business opportunities as well as business risks in

the presence of integrated reporting in corporate governance (Eccles & Serafeim, 2015).

Like Australia, there are many other countries all over the world that are adopting the

necessary corporate governance mechanism for ensuring the overall success of their

businesses. Every country considers their issues related to corporate governance while

adopting their corporate governance system. For example, the interest of the shareholders is

the major aspect that the countries like United Kingdom and United States consider in the

corporate governance mechanism, but other countries of Europe and Japan consider the

interest of all the key stakeholders like the suppliers, employees, customers and others for the

development of their corporate governance mechanism. However, for the government of

every country, one common aim behind the establishment of corporate governance

mechanism is to gain the trust and confidence of all classes of stakeholders of the companies

(Young & Thyil, 2014).

Conclusion

It can be seen from the above discussion that the presence of effective corporate

governance system reduces the possibility of corporate failures by ensuring the presence of

adequate number of external directors, independent directors and others. It also shows the

importance of ASIC and CLERP 9 for setting up of the effective corporate governance

system. It also shows that the companies are needed to ensure the merger of ethical

requirements and integrated reporting with corporate governance framework with the aim to

improve the overall efficiency of the companies.

both the financial as well as non-financial information of the business organizations. This

whole aspect contributes towards the better resource allocation, better decisions and better

actions for the companies in order to set up long-term sustainable value. Moreover, the

companies become able in identifying the business opportunities as well as business risks in

the presence of integrated reporting in corporate governance (Eccles & Serafeim, 2015).

Like Australia, there are many other countries all over the world that are adopting the

necessary corporate governance mechanism for ensuring the overall success of their

businesses. Every country considers their issues related to corporate governance while

adopting their corporate governance system. For example, the interest of the shareholders is

the major aspect that the countries like United Kingdom and United States consider in the

corporate governance mechanism, but other countries of Europe and Japan consider the

interest of all the key stakeholders like the suppliers, employees, customers and others for the

development of their corporate governance mechanism. However, for the government of

every country, one common aim behind the establishment of corporate governance

mechanism is to gain the trust and confidence of all classes of stakeholders of the companies

(Young & Thyil, 2014).

Conclusion

It can be seen from the above discussion that the presence of effective corporate

governance system reduces the possibility of corporate failures by ensuring the presence of

adequate number of external directors, independent directors and others. It also shows the

importance of ASIC and CLERP 9 for setting up of the effective corporate governance

system. It also shows that the companies are needed to ensure the merger of ethical

requirements and integrated reporting with corporate governance framework with the aim to

improve the overall efficiency of the companies.

8ACCOUNTING THEORY AND CORPORATE GOVERNANCE

References

ArAs, G. (2016). A handbook of corporate governance and social responsibility. Routledge.

Bavoso, V. (2014). Explaining financial scandals: corporate governance, structured finance

and the enlightened sovereign control paradigm. Cambridge Scholars Publishing.

Boatright, J. R. (2017). Ethics and corporate governance: Justifying the role of

shareholder. The Blackwell Guide to Business Ethics, 38-60.

Boral.com., (2019). Annual Report 2018. Retrieved 7 February 2019, from

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-

Report-2018.pdf

Bottomley, S. (2016). The constitutional corporation: Rethinking corporate governance.

Routledge.

Cheffins, B. R. (2013). The history of corporate governance. The Oxford handbook of

corporate governance, 46-64.

Eccles, R. G., & Serafeim, G. (2015). Corporate and integrated reporting. Corporate

Stewardship: Achieving Sustainable Effectiveness, 156.

Faghani, M., Monem, R., & Ng, C. (2015). Say on pay regulation and chief executive officer

pay: Evidence from Australia. Corporate Ownership and Control, 12(3), 28-39.

Filatotchev, I., & Nakajima, C. (2014). Corporate governance, responsible managerial

behavior, and corporate social responsibility: Organizational efficiency versus

organizational legitimacy?. Academy of Management Perspectives, 28(3), 289-306.

Wesfarmers.com.au. (2019). Annual Report 2018. Retrieved 31 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4

References

ArAs, G. (2016). A handbook of corporate governance and social responsibility. Routledge.

Bavoso, V. (2014). Explaining financial scandals: corporate governance, structured finance

and the enlightened sovereign control paradigm. Cambridge Scholars Publishing.

Boatright, J. R. (2017). Ethics and corporate governance: Justifying the role of

shareholder. The Blackwell Guide to Business Ethics, 38-60.

Boral.com., (2019). Annual Report 2018. Retrieved 7 February 2019, from

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-

Report-2018.pdf

Bottomley, S. (2016). The constitutional corporation: Rethinking corporate governance.

Routledge.

Cheffins, B. R. (2013). The history of corporate governance. The Oxford handbook of

corporate governance, 46-64.

Eccles, R. G., & Serafeim, G. (2015). Corporate and integrated reporting. Corporate

Stewardship: Achieving Sustainable Effectiveness, 156.

Faghani, M., Monem, R., & Ng, C. (2015). Say on pay regulation and chief executive officer

pay: Evidence from Australia. Corporate Ownership and Control, 12(3), 28-39.

Filatotchev, I., & Nakajima, C. (2014). Corporate governance, responsible managerial

behavior, and corporate social responsibility: Organizational efficiency versus

organizational legitimacy?. Academy of Management Perspectives, 28(3), 289-306.

Wesfarmers.com.au. (2019). Annual Report 2018. Retrieved 31 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-

report.pdf?sfvrsn=4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Ye, K. (2014). Independent director cash compensation and earnings management. Journal of

Accounting and Public Policy, 33(4), 391-400.

Young, S., & Thyil, V. (2014). Corporate social responsibility and corporate governance:

Role of context in international settings. Journal of Business Ethics, 122(1), 1-24.

Ye, K. (2014). Independent director cash compensation and earnings management. Journal of

Accounting and Public Policy, 33(4), 391-400.

Young, S., & Thyil, V. (2014). Corporate social responsibility and corporate governance:

Role of context in international settings. Journal of Business Ethics, 122(1), 1-24.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.