Accounting Theory and Contemporary Issues: Harvey Norman Analysis

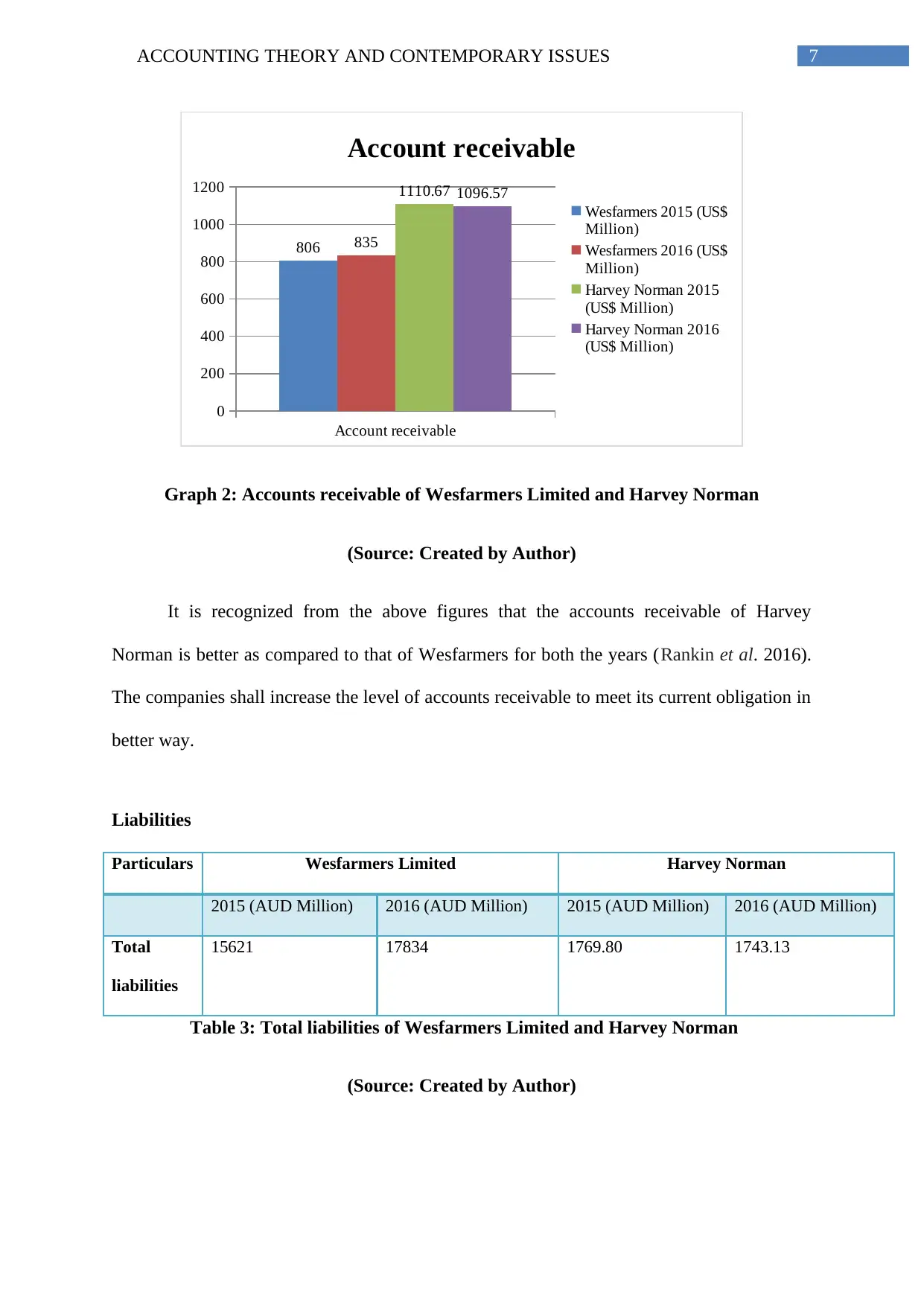

VerifiedAdded on 2020/03/07

|15

|2391

|236

Report

AI Summary

This report provides a comprehensive analysis of accounting theory and contemporary issues, focusing on the financial performance of Harvey Norman. The report begins with an executive summary outlining the key objectives and structure, followed by an introduction to Harvey Norman's business model. The core of the report involves an in-depth analysis of Harvey Norman's general purpose financial report (GPFR), remuneration report, inventory analysis, accounts receivable, liabilities, and income analysis. The report compares Harvey Norman's financial aspects with those of Wesfarmers, providing a comparative perspective. The analysis includes key financial metrics and their implications. The report also delves into the conceptual framework, particularly the concept of prudence, discussing its importance, benefits, and criticisms. The report identifies and discusses issues specific to Harvey Norman, such as shareholder concerns. The report concludes with recommendations for the company, based on the financial analysis, and a comprehensive list of references.

Running head: ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Accounting theory and contemporary issues

Name of the student

Name of the university

Author note

Accounting theory and contemporary issues

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Executive summary

The main objective of this report is to focus on the conceptual framework and prudence with

regard to accounting and financial statement. The report will focus on the analysis of the

general purpose financial report, remuneration report, inventory analysis, account receivable,

income analysis and liabilities of Harvey Norman. Further, the report will compare the

financial aspect of the company with that of Wesfarmers. Based on the outcomes, finally

some recommendation will be provided.

Executive summary

The main objective of this report is to focus on the conceptual framework and prudence with

regard to accounting and financial statement. The report will focus on the analysis of the

general purpose financial report, remuneration report, inventory analysis, account receivable,

income analysis and liabilities of Harvey Norman. Further, the report will compare the

financial aspect of the company with that of Wesfarmers. Based on the outcomes, finally

some recommendation will be provided.

2ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Table of Contents

Introduction................................................................................................................................3

Analysis of (GPFR) general purpose financial report................................................................3

Remuneration report and conceptual framework.......................................................................4

Inventory analysis......................................................................................................................5

Account receivable.....................................................................................................................6

Liabilities....................................................................................................................................7

Income analysis..........................................................................................................................8

Prudence in conceptual framework............................................................................................9

Importance of prudence............................................................................................................10

Benefits and criticism of prudence...........................................................................................10

Issues with the company..........................................................................................................11

Conclusion................................................................................................................................11

Recommendation......................................................................................................................11

Reference..................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Analysis of (GPFR) general purpose financial report................................................................3

Remuneration report and conceptual framework.......................................................................4

Inventory analysis......................................................................................................................5

Account receivable.....................................................................................................................6

Liabilities....................................................................................................................................7

Income analysis..........................................................................................................................8

Prudence in conceptual framework............................................................................................9

Importance of prudence............................................................................................................10

Benefits and criticism of prudence...........................................................................................10

Issues with the company..........................................................................................................11

Conclusion................................................................................................................................11

Recommendation......................................................................................................................11

Reference..................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Introduction

Harvey Norman is the big multi-national, Australian based retailer for furniture,

computers, consumer electrical and communication products. Their operating structure is

different from others with respect to the fact that each of the store department is operated by

the separate management entity. Therefore, the superstores are the combination of three to

four different management of business that are independently managed through contribution

of revenue to the Harvey Norman Holdings Ltd. through the sales portion and lease

payments. The stores of Harvey Norman are operated and owned by Sydney based and ASX

Listed parent company Harvey Norman Holdings Limited. The main objective of the

company is to get the recognition as the global leader in delivering the retail services in fast

moving sector of consumer goods, generate sufficient returns for the stakeholders, creating

the inspiring workplace and to be welcomed by the communities under which they operate

their business (Harveynormanholdings.com.au 2016).

Analysis of (GPFR) general purpose financial report

The company is the profit company that is limited by shares and incorporated as well

as operated in Australia. The shares of the company are traded publicly under the Australian

Securities Exchange (ASX) and trading under ASX with the code HVN. The financial

statement of the company is the general purpose financial report and is prepared as per the

requirements of the Corporation Act 2001, interpretation of the Australian Accounting

Standards and the compliance of other law. The financial report of the company further

omplied with the AAS (Australian Accounting Standard) as issued by the AASB and the

IFRS (International Financial Reporting Board) as released by the IASB (International

Accounting Standard Board). Further, the accounts are prepared based on the historical cost

approach except for the land, buildings, investment properties, listed shares those are held for

Introduction

Harvey Norman is the big multi-national, Australian based retailer for furniture,

computers, consumer electrical and communication products. Their operating structure is

different from others with respect to the fact that each of the store department is operated by

the separate management entity. Therefore, the superstores are the combination of three to

four different management of business that are independently managed through contribution

of revenue to the Harvey Norman Holdings Ltd. through the sales portion and lease

payments. The stores of Harvey Norman are operated and owned by Sydney based and ASX

Listed parent company Harvey Norman Holdings Limited. The main objective of the

company is to get the recognition as the global leader in delivering the retail services in fast

moving sector of consumer goods, generate sufficient returns for the stakeholders, creating

the inspiring workplace and to be welcomed by the communities under which they operate

their business (Harveynormanholdings.com.au 2016).

Analysis of (GPFR) general purpose financial report

The company is the profit company that is limited by shares and incorporated as well

as operated in Australia. The shares of the company are traded publicly under the Australian

Securities Exchange (ASX) and trading under ASX with the code HVN. The financial

statement of the company is the general purpose financial report and is prepared as per the

requirements of the Corporation Act 2001, interpretation of the Australian Accounting

Standards and the compliance of other law. The financial report of the company further

omplied with the AAS (Australian Accounting Standard) as issued by the AASB and the

IFRS (International Financial Reporting Board) as released by the IASB (International

Accounting Standard Board). Further, the accounts are prepared based on the historical cost

approach except for the land, buildings, investment properties, listed shares those are held for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CONTEMPORARY ISSUES

trading, investments those are available for sale and few derivative instruments which are

measured at the fair value approach.

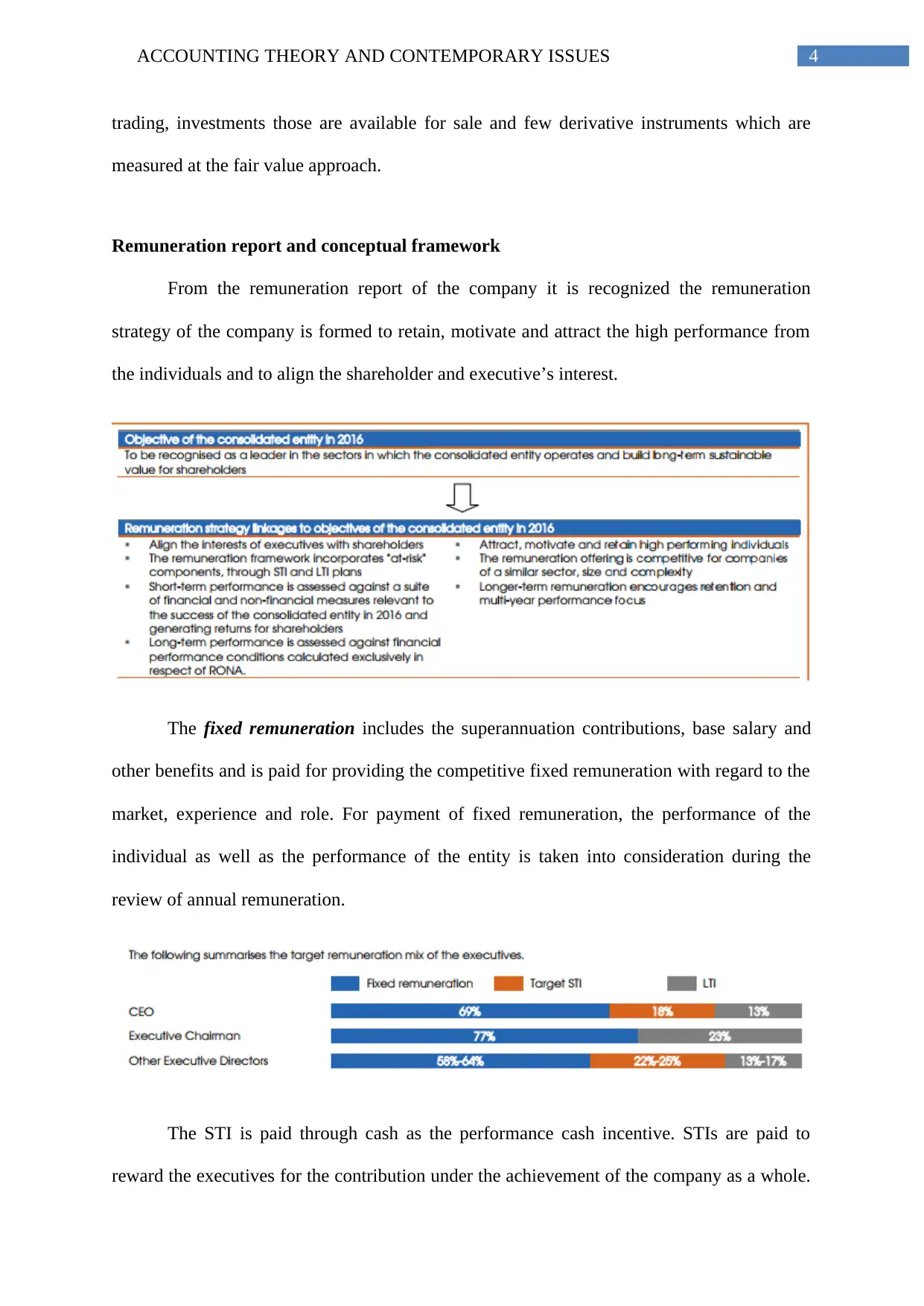

Remuneration report and conceptual framework

From the remuneration report of the company it is recognized the remuneration

strategy of the company is formed to retain, motivate and attract the high performance from

the individuals and to align the shareholder and executive’s interest.

The fixed remuneration includes the superannuation contributions, base salary and

other benefits and is paid for providing the competitive fixed remuneration with regard to the

market, experience and role. For payment of fixed remuneration, the performance of the

individual as well as the performance of the entity is taken into consideration during the

review of annual remuneration.

The STI is paid through cash as the performance cash incentive. STIs are paid to

reward the executives for the contribution under the achievement of the company as a whole.

trading, investments those are available for sale and few derivative instruments which are

measured at the fair value approach.

Remuneration report and conceptual framework

From the remuneration report of the company it is recognized the remuneration

strategy of the company is formed to retain, motivate and attract the high performance from

the individuals and to align the shareholder and executive’s interest.

The fixed remuneration includes the superannuation contributions, base salary and

other benefits and is paid for providing the competitive fixed remuneration with regard to the

market, experience and role. For payment of fixed remuneration, the performance of the

individual as well as the performance of the entity is taken into consideration during the

review of annual remuneration.

The STI is paid through cash as the performance cash incentive. STIs are paid to

reward the executives for the contribution under the achievement of the company as a whole.

5ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Out of the total STI, 50% is subject to the financial condition which is 50% satisfied at the

14% RONA, 100% satisfied at the 15% RONA and further 50% is subject to the non-

financial conditional performance. Finally, the LTI are paid for performance rights with

regard to the right to acquire 1 ordinary share of the company at zero exercise prices. Further,

the remuneration strategies are presented to the shareholders in the AGM for their approval.

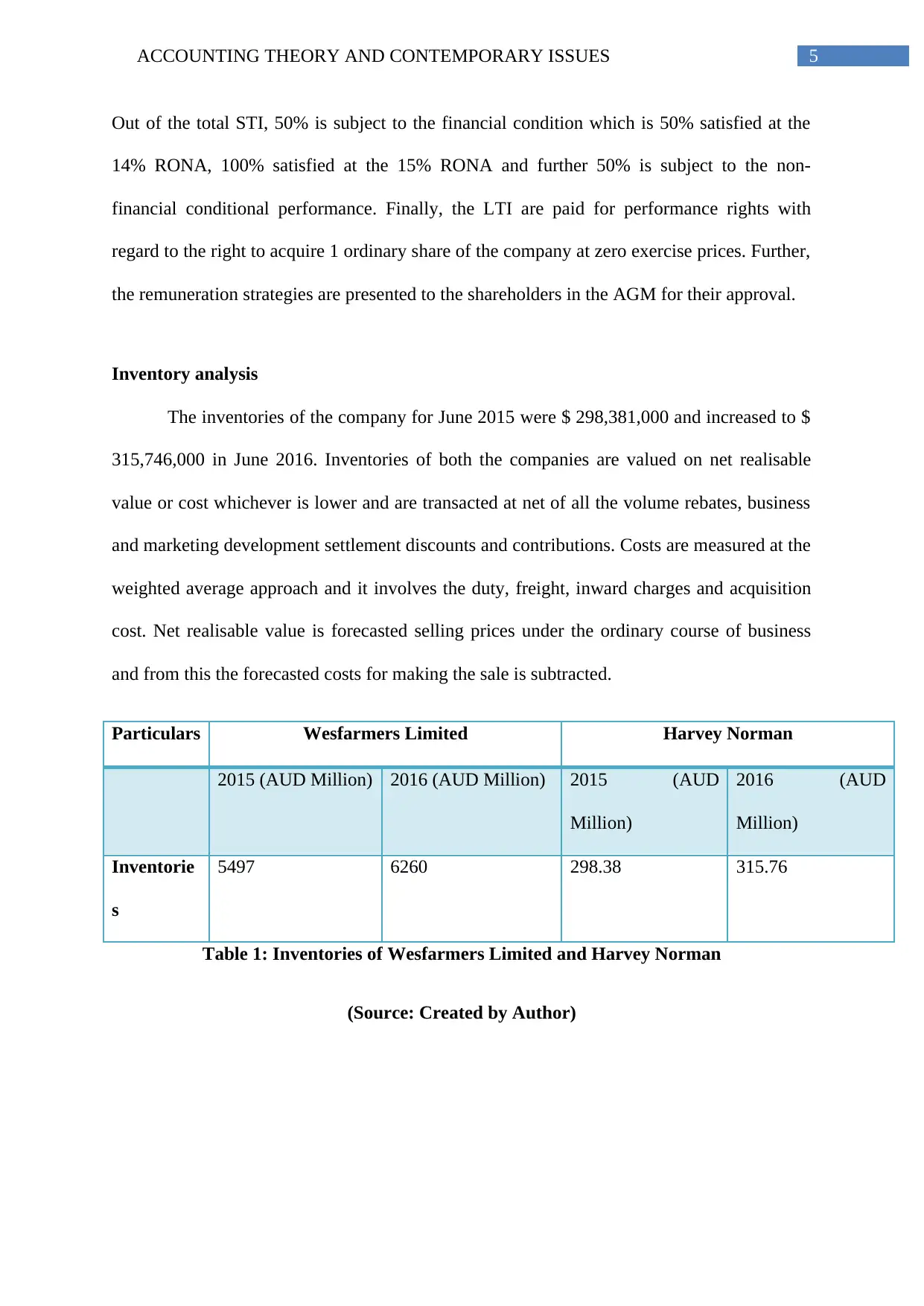

Inventory analysis

The inventories of the company for June 2015 were $ 298,381,000 and increased to $

315,746,000 in June 2016. Inventories of both the companies are valued on net realisable

value or cost whichever is lower and are transacted at net of all the volume rebates, business

and marketing development settlement discounts and contributions. Costs are measured at the

weighted average approach and it involves the duty, freight, inward charges and acquisition

cost. Net realisable value is forecasted selling prices under the ordinary course of business

and from this the forecasted costs for making the sale is subtracted.

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD

Million)

2016 (AUD

Million)

Inventorie

s

5497 6260 298.38 315.76

Table 1: Inventories of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

Out of the total STI, 50% is subject to the financial condition which is 50% satisfied at the

14% RONA, 100% satisfied at the 15% RONA and further 50% is subject to the non-

financial conditional performance. Finally, the LTI are paid for performance rights with

regard to the right to acquire 1 ordinary share of the company at zero exercise prices. Further,

the remuneration strategies are presented to the shareholders in the AGM for their approval.

Inventory analysis

The inventories of the company for June 2015 were $ 298,381,000 and increased to $

315,746,000 in June 2016. Inventories of both the companies are valued on net realisable

value or cost whichever is lower and are transacted at net of all the volume rebates, business

and marketing development settlement discounts and contributions. Costs are measured at the

weighted average approach and it involves the duty, freight, inward charges and acquisition

cost. Net realisable value is forecasted selling prices under the ordinary course of business

and from this the forecasted costs for making the sale is subtracted.

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD

Million)

2016 (AUD

Million)

Inventorie

s

5497 6260 298.38 315.76

Table 1: Inventories of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Inventories

0

1000

2000

3000

4000

5000

6000

7000

5497

6260

298.381 315.746

Inventories

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 1: Inventories of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized that the inventories of Harvey Norman is significantly low as

compared to that of Wesfarmers for both 2015 and 2016.

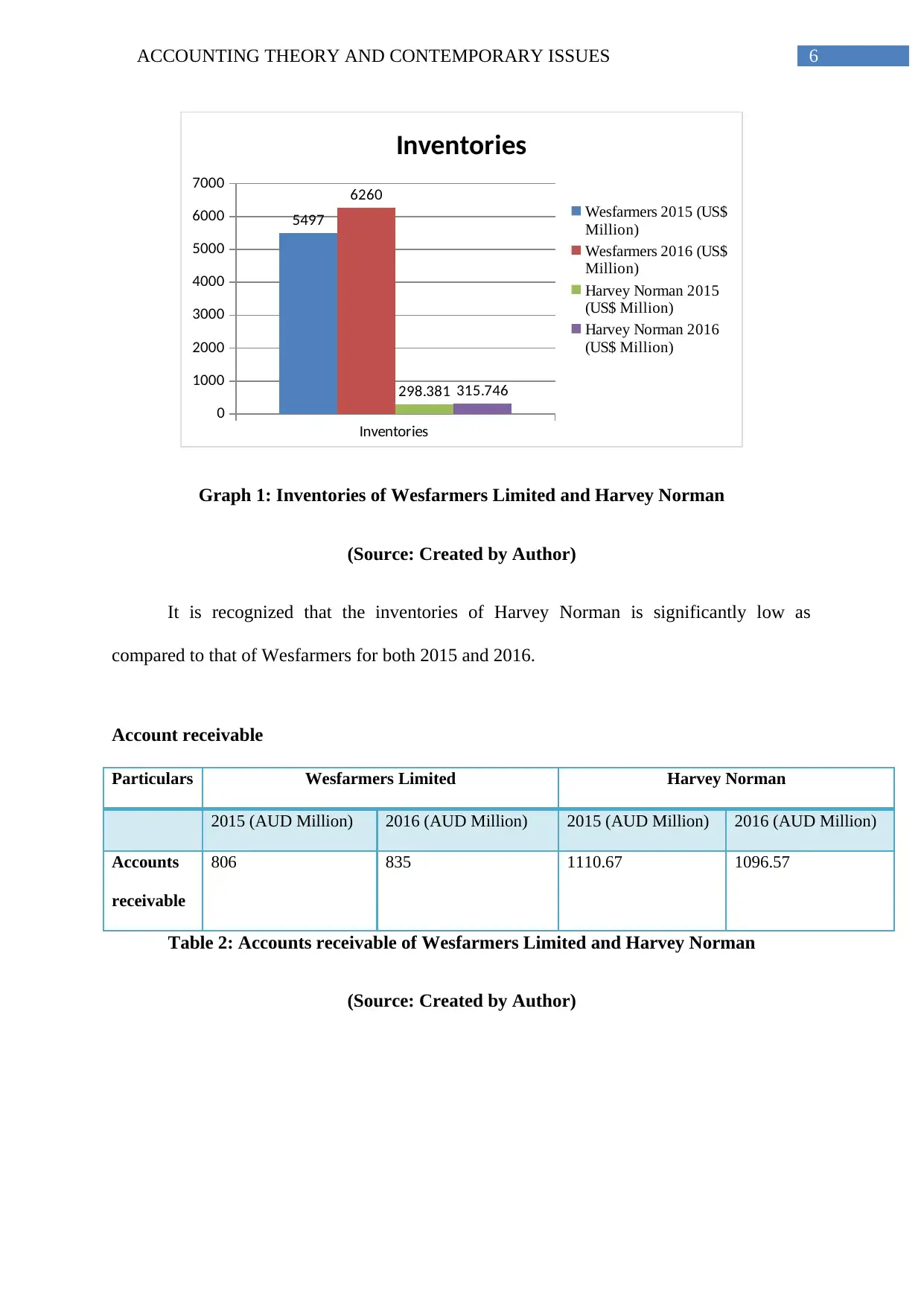

Account receivable

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

Accounts

receivable

806 835 1110.67 1096.57

Table 2: Accounts receivable of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

Inventories

0

1000

2000

3000

4000

5000

6000

7000

5497

6260

298.381 315.746

Inventories

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 1: Inventories of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized that the inventories of Harvey Norman is significantly low as

compared to that of Wesfarmers for both 2015 and 2016.

Account receivable

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

Accounts

receivable

806 835 1110.67 1096.57

Table 2: Accounts receivable of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Account receivable

0

200

400

600

800

1000

1200

806 835

1110.67 1096.57

Account receivable

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 2: Accounts receivable of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the accounts receivable of Harvey

Norman is better as compared to that of Wesfarmers for both the years (Rankin et al. 2016).

The companies shall increase the level of accounts receivable to meet its current obligation in

better way.

Liabilities

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

Total

liabilities

15621 17834 1769.80 1743.13

Table 3: Total liabilities of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

Account receivable

0

200

400

600

800

1000

1200

806 835

1110.67 1096.57

Account receivable

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 2: Accounts receivable of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the accounts receivable of Harvey

Norman is better as compared to that of Wesfarmers for both the years (Rankin et al. 2016).

The companies shall increase the level of accounts receivable to meet its current obligation in

better way.

Liabilities

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

Total

liabilities

15621 17834 1769.80 1743.13

Table 3: Total liabilities of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

8ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Total liabilities

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

15621

17834

1769.8 1743.13

Total liabilities

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 3: Total liabilities of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the total liabilities position of Harvey

Norman is better as compared to that of Wesfarmers for both the years. The companies

reduce the level of total liabilities to improve their liquidity position (Picker et al. 2016).

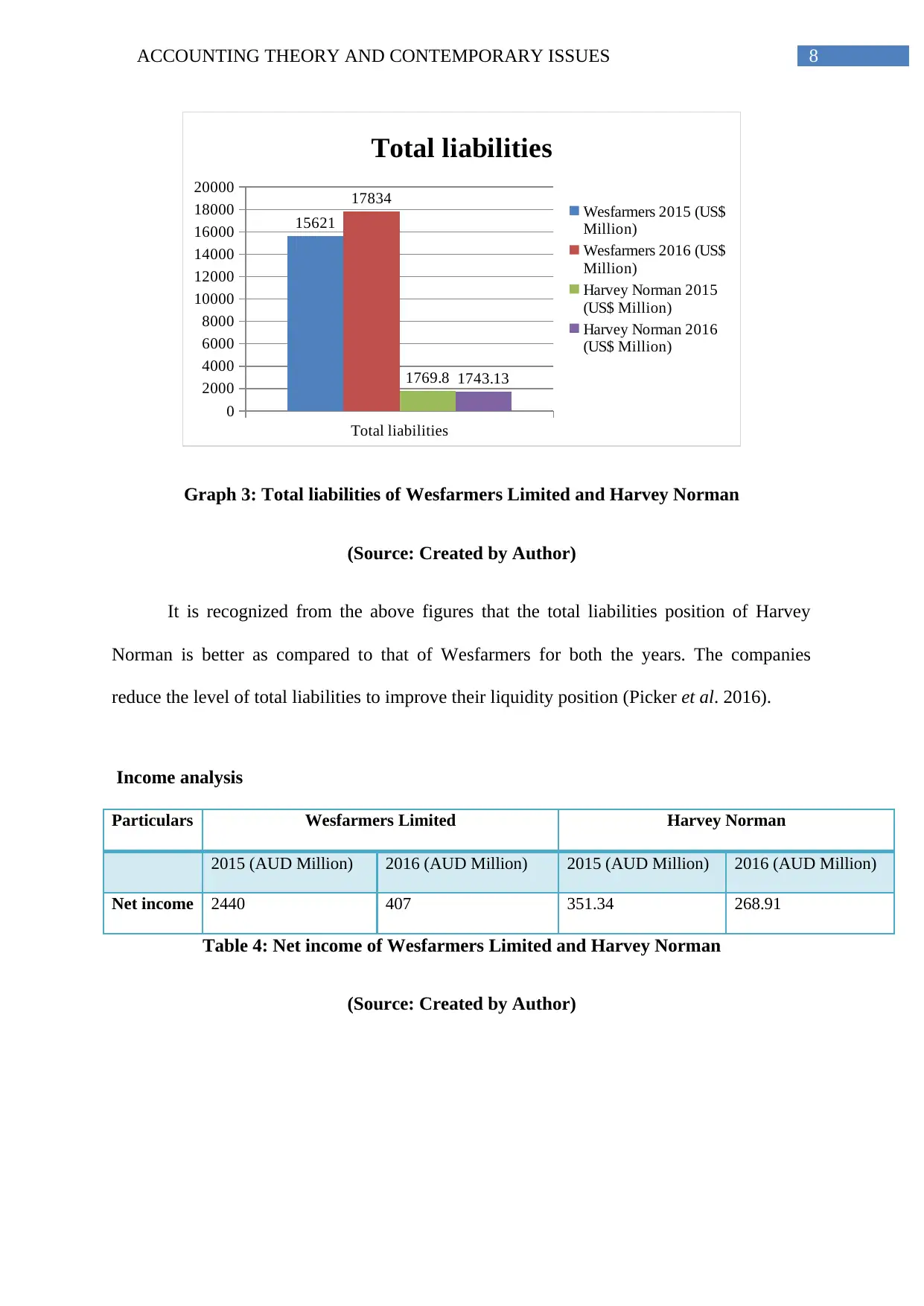

Income analysis

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

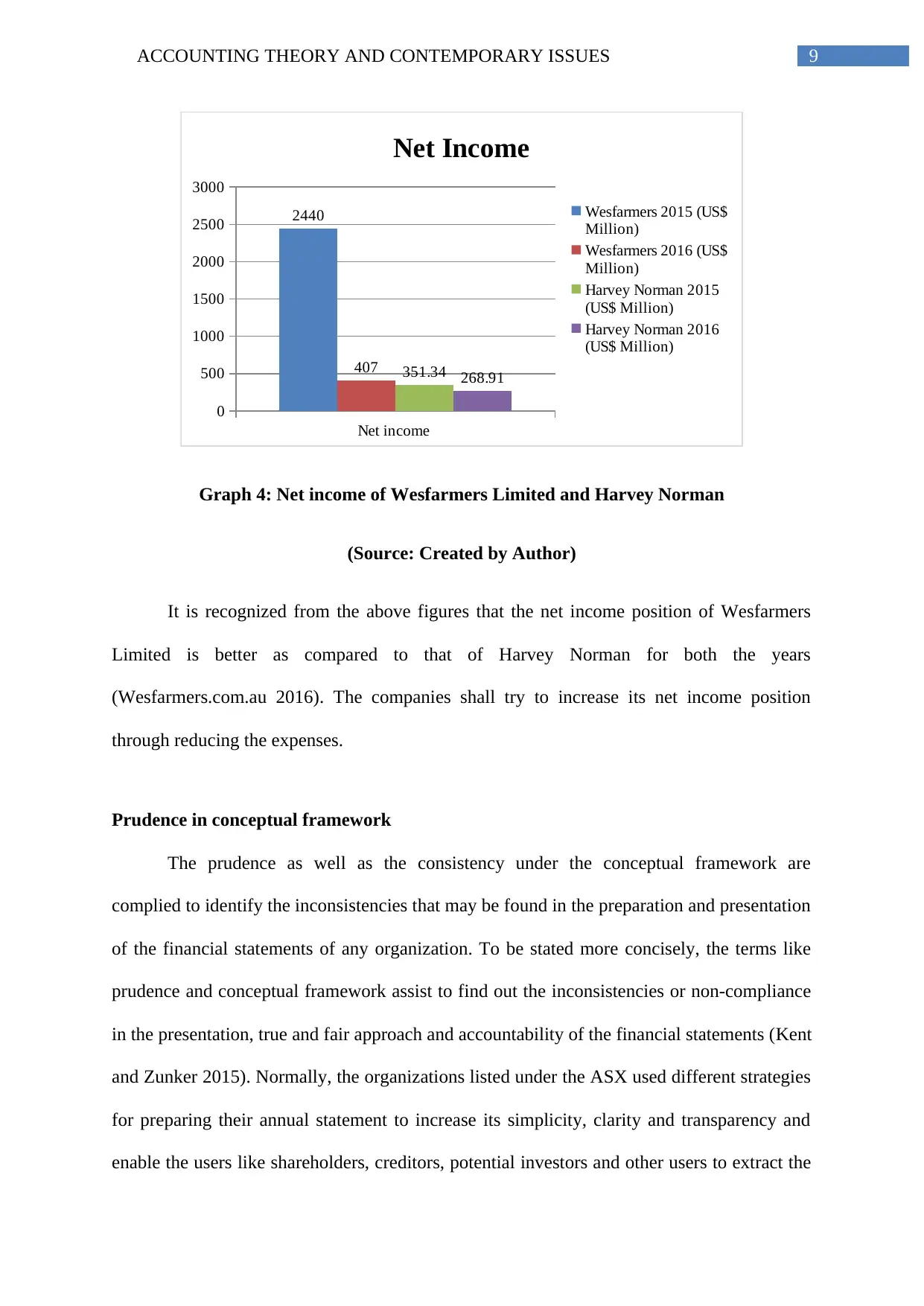

Net income 2440 407 351.34 268.91

Table 4: Net income of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

Total liabilities

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

15621

17834

1769.8 1743.13

Total liabilities

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 3: Total liabilities of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the total liabilities position of Harvey

Norman is better as compared to that of Wesfarmers for both the years. The companies

reduce the level of total liabilities to improve their liquidity position (Picker et al. 2016).

Income analysis

Particulars Wesfarmers Limited Harvey Norman

2015 (AUD Million) 2016 (AUD Million) 2015 (AUD Million) 2016 (AUD Million)

Net income 2440 407 351.34 268.91

Table 4: Net income of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Net income

0

500

1000

1500

2000

2500

3000

2440

407 351.34 268.91

Net Income

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 4: Net income of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the net income position of Wesfarmers

Limited is better as compared to that of Harvey Norman for both the years

(Wesfarmers.com.au 2016). The companies shall try to increase its net income position

through reducing the expenses.

Prudence in conceptual framework

The prudence as well as the consistency under the conceptual framework are

complied to identify the inconsistencies that may be found in the preparation and presentation

of the financial statements of any organization. To be stated more concisely, the terms like

prudence and conceptual framework assist to find out the inconsistencies or non-compliance

in the presentation, true and fair approach and accountability of the financial statements (Kent

and Zunker 2015). Normally, the organizations listed under the ASX used different strategies

for preparing their annual statement to increase its simplicity, clarity and transparency and

enable the users like shareholders, creditors, potential investors and other users to extract the

Net income

0

500

1000

1500

2000

2500

3000

2440

407 351.34 268.91

Net Income

Wesfarmers 2015 (US$

Million)

Wesfarmers 2016 (US$

Million)

Harvey Norman 2015

(US$ Million)

Harvey Norman 2016

(US$ Million)

Graph 4: Net income of Wesfarmers Limited and Harvey Norman

(Source: Created by Author)

It is recognized from the above figures that the net income position of Wesfarmers

Limited is better as compared to that of Harvey Norman for both the years

(Wesfarmers.com.au 2016). The companies shall try to increase its net income position

through reducing the expenses.

Prudence in conceptual framework

The prudence as well as the consistency under the conceptual framework are

complied to identify the inconsistencies that may be found in the preparation and presentation

of the financial statements of any organization. To be stated more concisely, the terms like

prudence and conceptual framework assist to find out the inconsistencies or non-compliance

in the presentation, true and fair approach and accountability of the financial statements (Kent

and Zunker 2015). Normally, the organizations listed under the ASX used different strategies

for preparing their annual statement to increase its simplicity, clarity and transparency and

enable the users like shareholders, creditors, potential investors and other users to extract the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND CONTEMPORARY ISSUES

information easily as per their requirement. On the other hand, non-compliance explains that

the organization while preparing their annual statement has not followed the conceptual

framework of IFRS, IASB or AASB or did not followed the true and fair view approaches.

Importance of prudence

The financial statements of any organization are of biggest concern which is beyond

of just the true and fair approach and the contemporary issues of Accountability. Reliability

and prudence with regard to the financial statement accounting reporting has long record

(Zhang and Andrew 2014). Various arguments are there with regard to the significant

accounting standards, AASB and IFRS that must take into consideration the term prudence

and shall state its importance under the conceptual framework. Including the carefulness

while applying the judgements on the financial statements are required with regard to

probability and uncertainty in the circumstances, for example, the liabilities and the expenses

are not undervalued and the incomes and assets are not overvalued (Scott 2012.). Thus, the

concept of prudence is the big concern for the presentation of financial statement as per the

true and fair approach. Moreover, it offers wide initiative with regard to the operational as

well as the financial position of the company that is to be taken into consideration.

Benefits and criticism of prudence

The major advantage of prudence is the preparation of the financial statements on the

basis of going concern. It assists the accountant to forecast the future problems that may take

place in the business. Further, it assists the accountants to prepare the plan for the future and

allow them time to solve the financial problems. The prudence also assists in influencing the

financial statement to be useful for the investors (Schaltegger and Burritt 2013). On the other

hand, the criticism that is received against the prudence is that it failed to take into account

the fact that the economic value and book value of the asset are different. Further, the

information easily as per their requirement. On the other hand, non-compliance explains that

the organization while preparing their annual statement has not followed the conceptual

framework of IFRS, IASB or AASB or did not followed the true and fair view approaches.

Importance of prudence

The financial statements of any organization are of biggest concern which is beyond

of just the true and fair approach and the contemporary issues of Accountability. Reliability

and prudence with regard to the financial statement accounting reporting has long record

(Zhang and Andrew 2014). Various arguments are there with regard to the significant

accounting standards, AASB and IFRS that must take into consideration the term prudence

and shall state its importance under the conceptual framework. Including the carefulness

while applying the judgements on the financial statements are required with regard to

probability and uncertainty in the circumstances, for example, the liabilities and the expenses

are not undervalued and the incomes and assets are not overvalued (Scott 2012.). Thus, the

concept of prudence is the big concern for the presentation of financial statement as per the

true and fair approach. Moreover, it offers wide initiative with regard to the operational as

well as the financial position of the company that is to be taken into consideration.

Benefits and criticism of prudence

The major advantage of prudence is the preparation of the financial statements on the

basis of going concern. It assists the accountant to forecast the future problems that may take

place in the business. Further, it assists the accountants to prepare the plan for the future and

allow them time to solve the financial problems. The prudence also assists in influencing the

financial statement to be useful for the investors (Schaltegger and Burritt 2013). On the other

hand, the criticism that is received against the prudence is that it failed to take into account

the fact that the economic value and book value of the asset are different. Further, the

11ACCOUNTING THEORY AND CONTEMPORARY ISSUES

contracting demand for the accounting of prudence is received with regard to the problem

that most of the part that is to be applied does not exist actually.

Issues with the company

One of the major issues of the company is the revolt of the shareholder for more than

$ 943 million for loans to the franchisees along with the proxy advisor that recommended the

fund managers to vote against the reception of the financial accounts. The main issue

regarding the matter was detail regarding the loan was not provided. The lack of transparency

in the account was a serious issue. It was also found that during FY16 the franchisees retailer

doubled the sales growth that was amounted to $ 5.33 billion with increase of 7.6% as

compared to 3.7% increase for the previous year. Though the company was happy regarding

this tremendous growth, as per ASIC the company is not transparent to their shareholders.

Conclusion

From above analysis it is found that both the companies are following the AASB

framework and IFRS interpretation while preparing their financial statements. However, the

inventories of Harvey Norman is significantly low as compared to that of Wesfarmers for

both 2015 and 2016 and that the accounts receivable of Harvey Norman is better as compared

to that of Wesfarmers for both the years. Further, the total liabilities position of Harvey

Norman is better as compared to that of Wesfarmers for both the years and net income

position of Wesfarmers Limited is better as compared to that of Harvey Norman for both the

years.

Recommendation

As it is found from the financial report of the company that the inventories of the

company are significantly low, the company shall accumulate some fund to purchase

contracting demand for the accounting of prudence is received with regard to the problem

that most of the part that is to be applied does not exist actually.

Issues with the company

One of the major issues of the company is the revolt of the shareholder for more than

$ 943 million for loans to the franchisees along with the proxy advisor that recommended the

fund managers to vote against the reception of the financial accounts. The main issue

regarding the matter was detail regarding the loan was not provided. The lack of transparency

in the account was a serious issue. It was also found that during FY16 the franchisees retailer

doubled the sales growth that was amounted to $ 5.33 billion with increase of 7.6% as

compared to 3.7% increase for the previous year. Though the company was happy regarding

this tremendous growth, as per ASIC the company is not transparent to their shareholders.

Conclusion

From above analysis it is found that both the companies are following the AASB

framework and IFRS interpretation while preparing their financial statements. However, the

inventories of Harvey Norman is significantly low as compared to that of Wesfarmers for

both 2015 and 2016 and that the accounts receivable of Harvey Norman is better as compared

to that of Wesfarmers for both the years. Further, the total liabilities position of Harvey

Norman is better as compared to that of Wesfarmers for both the years and net income

position of Wesfarmers Limited is better as compared to that of Harvey Norman for both the

years.

Recommendation

As it is found from the financial report of the company that the inventories of the

company are significantly low, the company shall accumulate some fund to purchase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

![Report: Contemporary Issues in Accounting - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzz%2F9509ff46c136422d929242036a52e1cb.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.