3101AFE Accounting Theory & Practice: Accounting Policy Changes

VerifiedAdded on 2023/06/04

|6

|894

|152

Homework Assignment

AI Summary

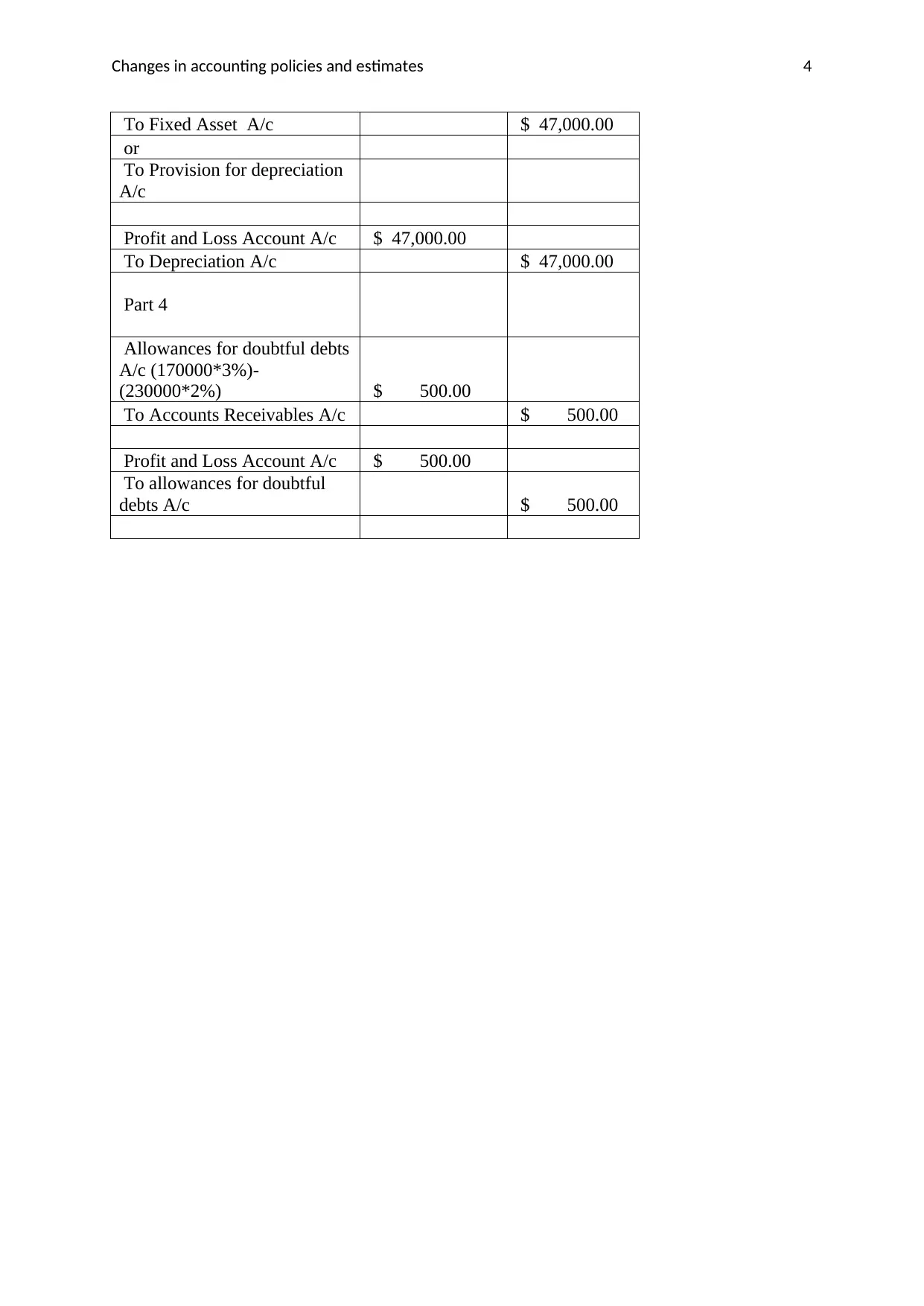

This assignment provides solutions to questions related to changes in accounting policies and estimates in financial accounting. It covers topics such as the treatment of omitted expenses from previous years, changes in the measurement methods of assets (e.g., from cost to revaluation method), and changes in depreciation methods. The assignment also addresses the accounting treatment of prior period items, such as losses due to unforeseen events like floods, and provides journal entries for various accounting adjustments, including warranty costs, annual leave, depreciation, and allowances for doubtful debts. References to AASB standards are included to support the solutions. Desklib offers a platform for students to access similar solved assignments and study resources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.