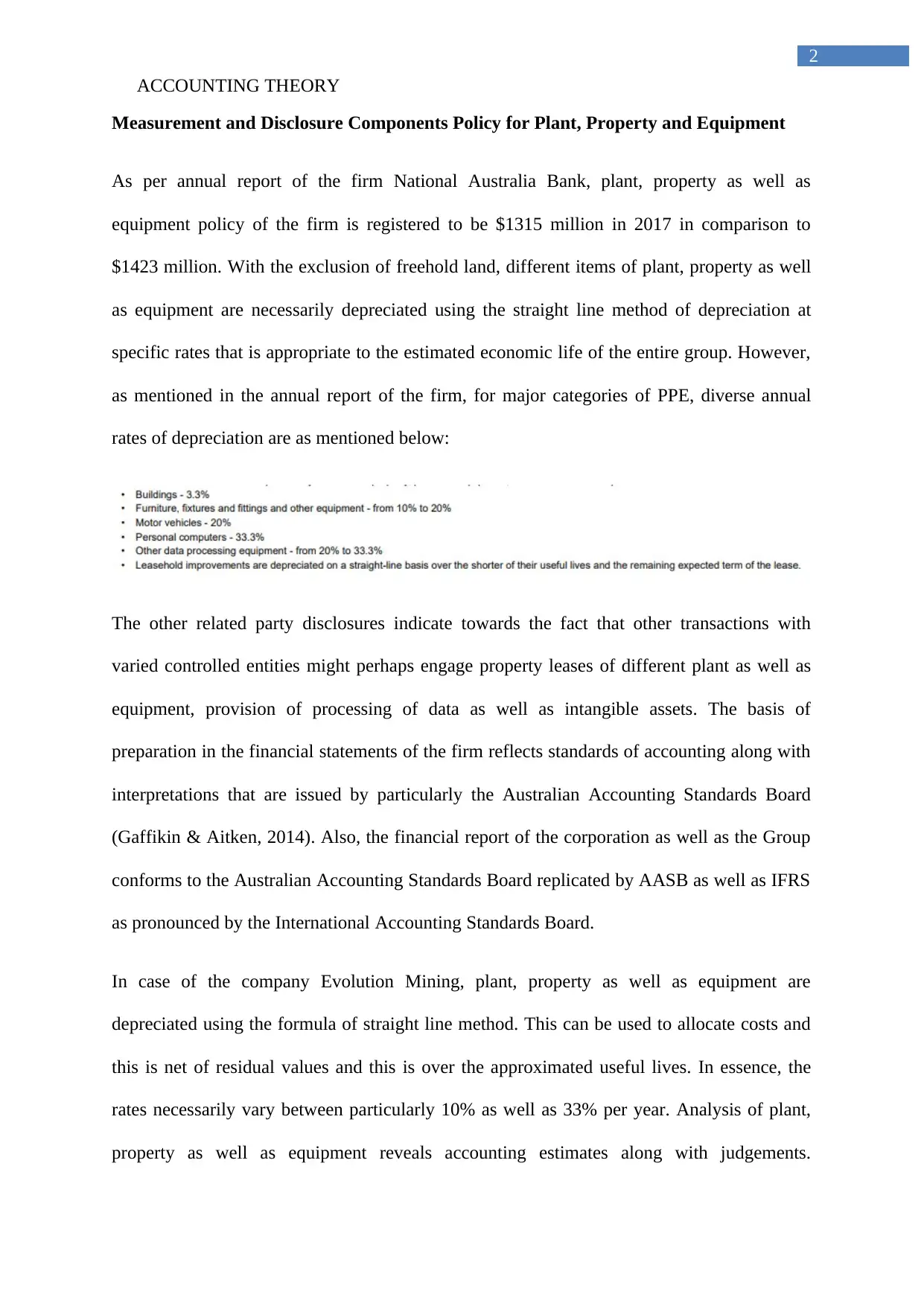

Accounting Theory Report: Analysis of Accounting Policies for PPE

VerifiedAdded on 2021/05/31

|5

|883

|99

Report

AI Summary

This report analyzes accounting theory concerning Plant, Property, and Equipment (PPE), drawing on the annual reports of National Australia Bank and Evolution Mining. It explores the accounting policies related to depreciation, including the straight-line method and varying depreciation rates. The report highlights the application of AASB 116 and IFRS standards, emphasizing the importance of accounting estimates and judgments in determining economic lives and residual values. It compares the accounting treatments of PPE, focusing on recognition, depreciation methods, and disclosures, providing a comprehensive overview of accounting practices for PPE within the context of financial reporting for for-profit entities. References to Gaffikin & Aitken (2014), Scott (2015), Sin et al. (2015), and Smith et al. (2015) are included to support the analysis.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.