Contemporary Accounting Theory Report: ACCT20074, Term 1

VerifiedAdded on 2022/12/20

|16

|4389

|76

Report

AI Summary

This report delves into contemporary accounting theory, focusing on conceptual frameworks and financial reporting practices. The report is divided into two main sections: Part A examines the conceptual framework, tracing its development in the USA, UK, Australia, and globally under the IASB. It also addresses the Australian accounting profession's concerns regarding the application of the IASB/IFRS framework and critically discusses academic perspectives on its quality and potential drawbacks. Part B explores integrated and sustainability reporting, including the GRI framework and Integrated Reporting under IIRC, with a focus on two companies: Blackmores Limited (Australian) and Anheuser-Bush InBev (South African). The report analyzes their financial statements, including the application of accounting standards, asset valuation, liability recognition, and disclosure practices. The analysis covers aspects such as the use of historical and fair value methods, treatment of trade receivables, fixed assets, intangible assets, liabilities, and lease accounting. The report concludes by summarizing the key findings and implications of the analysis.

Running head: Accounting Theory

Accounting Theory

Name of the Student

Name of the University

Author Note

Accounting Theory

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Accounting Theory

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................3

Part A: Conceptual Framework..................................................................................................3

Requirement (a):.....................................................................................................................3

Requirement (b):....................................................................................................................5

Requirement (c):.....................................................................................................................5

Requirement (d):....................................................................................................................6

Part B: Integrated/Sustainability Reporting...............................................................................8

Requirement (a):.....................................................................................................................8

Requirement (b):....................................................................................................................9

Requirement (c):...................................................................................................................10

Requirement (d):..................................................................................................................11

Requirement (e):...................................................................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

Accounting Theory

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................3

Part A: Conceptual Framework..................................................................................................3

Requirement (a):.....................................................................................................................3

Requirement (b):....................................................................................................................5

Requirement (c):.....................................................................................................................5

Requirement (d):....................................................................................................................6

Part B: Integrated/Sustainability Reporting...............................................................................8

Requirement (a):.....................................................................................................................8

Requirement (b):....................................................................................................................9

Requirement (c):...................................................................................................................10

Requirement (d):..................................................................................................................11

Requirement (e):...................................................................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

2

Accounting Theory

Executive Summary

The report is been based upon the contemporary accounting which also show details

of the sustainability report of the company and it also able to describe the conceptual

framework in the company. It show about the Australian company Blackmores limited and

the South African company Anheuser-Bush InBev. It show about the different accounting

framework and the sustainability reporting of the company.

Introduction

Contemporary accounting helps the company to perform different types of role in the

company (Adams 2017). This report show different aspects of the contemporary account and

also it able to show the different sustainability and conceptual framework of different

company. The report can be separated into two sections. The first section of the report is able

to show the different types of the conceptual framework in regards of the financial reporting.

The second section of the report show the company is able to show the different accounting

framework which the company is using and also it able to show the different sustainability

report of the company. It also able to show the GRI framework and also the Integrated

Reporting under IIRC (Adams 2015). The report is been based upon Blackmores limited

which is an Australian company and Anheuser-Bush InBev which is a South African

company.

Part A: Conceptual Framework

Requirement (a):

As per the decade it can be said that there is a very big background in regards of the

conceptual framework as many big nation are involve in the same such as Australia, UK and

many other organization which have adopted the conceptual framework in regards for the

preparation of the financial reporting of the company in accordance of the IASB (Atkins &

Accounting Theory

Executive Summary

The report is been based upon the contemporary accounting which also show details

of the sustainability report of the company and it also able to describe the conceptual

framework in the company. It show about the Australian company Blackmores limited and

the South African company Anheuser-Bush InBev. It show about the different accounting

framework and the sustainability reporting of the company.

Introduction

Contemporary accounting helps the company to perform different types of role in the

company (Adams 2017). This report show different aspects of the contemporary account and

also it able to show the different sustainability and conceptual framework of different

company. The report can be separated into two sections. The first section of the report is able

to show the different types of the conceptual framework in regards of the financial reporting.

The second section of the report show the company is able to show the different accounting

framework which the company is using and also it able to show the different sustainability

report of the company. It also able to show the GRI framework and also the Integrated

Reporting under IIRC (Adams 2015). The report is been based upon Blackmores limited

which is an Australian company and Anheuser-Bush InBev which is a South African

company.

Part A: Conceptual Framework

Requirement (a):

As per the decade it can be said that there is a very big background in regards of the

conceptual framework as many big nation are involve in the same such as Australia, UK and

many other organization which have adopted the conceptual framework in regards for the

preparation of the financial reporting of the company in accordance of the IASB (Atkins &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Accounting Theory

Maroun 2015). Conceptual framework help the investors to get the confident in the financial

statement of the company as in late 1934 the economic slum which have come up in USA

have directly affect the individual investors as they were not able to invest in the company so

to overcome the problem the government came up with the use of the conceptual framework

so that it can able to clear the problem and also it will help them to gain the confidence of the

individual in the company financial reporting. The responsibility of the developing and

managing of the conceptual framework is been given to FASB so that proper framework can

be maintain by the authority (Bebbington, Unerman & O’Dwyer 2014).

The accounting in the Australia has also able to adopt the conceptual framework in

their financial reporting in regards of the AASB. The use of the conceptual framework in

Australia is due to the affect of the global competition as if all will be able to use the same

accounting framework in the reporting than it will able to help the user to compare the

financial statement of the company with the other company so that it can able to know the

performance of the company and able to know the better company so that it can able to invest

properly in the company (Brown & Dillard 2014).

As per the UK is been concern before the adoption of the conceptual framework in the

company it used to use the rules based accounting standard which does not have any relation

with the global accounting standard as it does not have any similarities with the global

accounting standard as it is only be applicable to the UK company (Cheng et al.,2014). So to

overcome the problem and able to make proper accounting standard, the UK government is

able to apply to the IASB and able to develop the conceptual framework in the financial

reporting of the company (Churet & Eccles 2014).

Their are many other nation except the one which are been mention above and the

reason they able to shift to IASB in order that it can able to match the global accounting

Accounting Theory

Maroun 2015). Conceptual framework help the investors to get the confident in the financial

statement of the company as in late 1934 the economic slum which have come up in USA

have directly affect the individual investors as they were not able to invest in the company so

to overcome the problem the government came up with the use of the conceptual framework

so that it can able to clear the problem and also it will help them to gain the confidence of the

individual in the company financial reporting. The responsibility of the developing and

managing of the conceptual framework is been given to FASB so that proper framework can

be maintain by the authority (Bebbington, Unerman & O’Dwyer 2014).

The accounting in the Australia has also able to adopt the conceptual framework in

their financial reporting in regards of the AASB. The use of the conceptual framework in

Australia is due to the affect of the global competition as if all will be able to use the same

accounting framework in the reporting than it will able to help the user to compare the

financial statement of the company with the other company so that it can able to know the

performance of the company and able to know the better company so that it can able to invest

properly in the company (Brown & Dillard 2014).

As per the UK is been concern before the adoption of the conceptual framework in the

company it used to use the rules based accounting standard which does not have any relation

with the global accounting standard as it does not have any similarities with the global

accounting standard as it is only be applicable to the UK company (Cheng et al.,2014). So to

overcome the problem and able to make proper accounting standard, the UK government is

able to apply to the IASB and able to develop the conceptual framework in the financial

reporting of the company (Churet & Eccles 2014).

Their are many other nation except the one which are been mention above and the

reason they able to shift to IASB in order that it can able to match the global accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Accounting Theory

standard and able to carry the accounting process similar to the global company. It help the

company to carry business easily as it able to hold all the global accounting standard in the

company and able to match up with the global reporting of the company (Clayton, Rogerson

& Rampedi 2015).

Requirement (b):

As per the financial reposting is been concern and also the conceptual framework

there is many question which are been there by the Australia accounting profession. The first

question or concern which the profession has is related to the fair value of accounting as it is

been a rise in regards of the financial reporting with the new conceptual framework. This will

directly have an adverse affect upon the financial statement of the company and also will able

to affect then value of intangible asset and financial instruments (De Villiers, Rinaldi &

Unerman 2014). In spite of these it can also be said that it also affect the valuation method of

the asset and liability and also it will affect the disclosure of the same. As per the changes

which have come in the financial statement in regards of the adoption of the IASB it will

directly affect the interest of the stakeholder and they may have to meet up with the economic

ramifications in regards of the change which are been made by the company (Dumay et al.,

2016).

The changes of the account framework will also affect the non-profit organization

which is carrying their business in Australia (Flower 2015). As per the research it is been

found that the most company have already applied the accounting standard in their reporting

framework. As it is been necessary for the formulation of doctrine of each sector, so it will

directly affect the non-profit organization this will affect the conceptual framework of the

company (Frias‐Aceituno, Rodríguez‐Ariza & Garcia‐Sánchez 2014).

Accounting Theory

standard and able to carry the accounting process similar to the global company. It help the

company to carry business easily as it able to hold all the global accounting standard in the

company and able to match up with the global reporting of the company (Clayton, Rogerson

& Rampedi 2015).

Requirement (b):

As per the financial reposting is been concern and also the conceptual framework

there is many question which are been there by the Australia accounting profession. The first

question or concern which the profession has is related to the fair value of accounting as it is

been a rise in regards of the financial reporting with the new conceptual framework. This will

directly have an adverse affect upon the financial statement of the company and also will able

to affect then value of intangible asset and financial instruments (De Villiers, Rinaldi &

Unerman 2014). In spite of these it can also be said that it also affect the valuation method of

the asset and liability and also it will affect the disclosure of the same. As per the changes

which have come in the financial statement in regards of the adoption of the IASB it will

directly affect the interest of the stakeholder and they may have to meet up with the economic

ramifications in regards of the change which are been made by the company (Dumay et al.,

2016).

The changes of the account framework will also affect the non-profit organization

which is carrying their business in Australia (Flower 2015). As per the research it is been

found that the most company have already applied the accounting standard in their reporting

framework. As it is been necessary for the formulation of doctrine of each sector, so it will

directly affect the non-profit organization this will affect the conceptual framework of the

company (Frias‐Aceituno, Rodríguez‐Ariza & Garcia‐Sánchez 2014).

5

Accounting Theory

Requirement (c):

The significant advantage which can be said in regards of the conceptual framework

is that it able to provide sufficient accounting standard and principle which will help the

company to do better reporting in the financial statement of the company. There are some

contexts which contain or show some drawbacks in regards of the theory of the conceptual

framework (Higgins, Stubbs & Love 2014). The adoption of the conceptual is not possible for

each organization as it require a lot of money and time which is not possible for each type of

the organization. The accounting in regards of the conceptual framework is not easy as it is

not a flexible so if the company has adopted the same in their accounting process than it will

be very hard for the company to come up with new ideas and concepts in regards of the new

accounting framework in the company

The conceptual framework is also been affected with the old guidelines as it able to

conflict with the rules which are already there in the guidelines so it will so if both have the

same types of the rules than it will not able follow the rule. It can be state that the conceptual

framework is not able to take all the information which are been obtained by the same. So it

can be said that there is a bit different in conceptual framework and also the AASB so it

should take both the aspects into consideration (Integratedreporting.org. 2019).

Requirement (d):

1. After the interpretation of the annual report Blackmores limited in 2018, it can be said

that the company is able to have four types of the statement which help the company

to show all the financial information of the company. The statement which are been

prepared are consolidation statement of comprehensive income, consolidated cash

flow statement, consolidated statement of the financial position and also the statement

in regards of the changes in equity. It can also be seen that the company is able to

match all the requirement as per the conceptual framework as they have given all the

Accounting Theory

Requirement (c):

The significant advantage which can be said in regards of the conceptual framework

is that it able to provide sufficient accounting standard and principle which will help the

company to do better reporting in the financial statement of the company. There are some

contexts which contain or show some drawbacks in regards of the theory of the conceptual

framework (Higgins, Stubbs & Love 2014). The adoption of the conceptual is not possible for

each organization as it require a lot of money and time which is not possible for each type of

the organization. The accounting in regards of the conceptual framework is not easy as it is

not a flexible so if the company has adopted the same in their accounting process than it will

be very hard for the company to come up with new ideas and concepts in regards of the new

accounting framework in the company

The conceptual framework is also been affected with the old guidelines as it able to

conflict with the rules which are already there in the guidelines so it will so if both have the

same types of the rules than it will not able follow the rule. It can be state that the conceptual

framework is not able to take all the information which are been obtained by the same. So it

can be said that there is a bit different in conceptual framework and also the AASB so it

should take both the aspects into consideration (Integratedreporting.org. 2019).

Requirement (d):

1. After the interpretation of the annual report Blackmores limited in 2018, it can be said

that the company is able to have four types of the statement which help the company

to show all the financial information of the company. The statement which are been

prepared are consolidation statement of comprehensive income, consolidated cash

flow statement, consolidated statement of the financial position and also the statement

in regards of the changes in equity. It can also be seen that the company is able to

match all the requirement as per the conceptual framework as they have given all the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Accounting Theory

details of the accounting process in the disclosure as per the IFRS and the AASB in

regards of the financial statement of the company (Kerr, Rouse & De Villiers 2015).

The financial statement is able to elements such as asset, income, expense and

liabilities.

2. It can be seen from the annual report of the company that they have used historical

and fair value method of accounting in regards of the recognition of the revenue of the

company so that it can able to make proper accounting information to the financial

user so that it can able to have more amount of the information and able to judge the

financial statement and able to take proper amount of the decision in the company

(Serafeim 2015).

It can be seen that they are able to record proper amount of the trade receivable in the

company as the company is able to allow the credit limit from 30 – 60 so it is good

amount of credit so it will help them to get more amount of the return from the debtor

of the company. The fixed asset are been stated after deducting the depreciation

amount and the company have given proper amount of disclosure in the annual report

of the company. The intangible asset is been valued as per the accounting standard

and also proper amount of the disclosure is been given by them in the financial

statement of the company.

As per the liabilities is been concern in the company they able to use the

amortised cost method in regards of the liability and able to carry the trade payable

value also in the annual report of the company (Sierra‐García, Zorio‐Grima & García‐

Benau 2015). As per the annual report of the company is been concern it can be seen

that is able to different in the lease of the company as it have different the financial

lease and the operating lease so it will be helpful for the company financial user to

know the details of the lease and able to take the same in regards of the financial

Accounting Theory

details of the accounting process in the disclosure as per the IFRS and the AASB in

regards of the financial statement of the company (Kerr, Rouse & De Villiers 2015).

The financial statement is able to elements such as asset, income, expense and

liabilities.

2. It can be seen from the annual report of the company that they have used historical

and fair value method of accounting in regards of the recognition of the revenue of the

company so that it can able to make proper accounting information to the financial

user so that it can able to have more amount of the information and able to judge the

financial statement and able to take proper amount of the decision in the company

(Serafeim 2015).

It can be seen that they are able to record proper amount of the trade receivable in the

company as the company is able to allow the credit limit from 30 – 60 so it is good

amount of credit so it will help them to get more amount of the return from the debtor

of the company. The fixed asset are been stated after deducting the depreciation

amount and the company have given proper amount of disclosure in the annual report

of the company. The intangible asset is been valued as per the accounting standard

and also proper amount of the disclosure is been given by them in the financial

statement of the company.

As per the liabilities is been concern in the company they able to use the

amortised cost method in regards of the liability and able to carry the trade payable

value also in the annual report of the company (Sierra‐García, Zorio‐Grima & García‐

Benau 2015). As per the annual report of the company is been concern it can be seen

that is able to different in the lease of the company as it have different the financial

lease and the operating lease so it will be helpful for the company financial user to

know the details of the lease and able to take the same in regards of the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Accounting Theory

position of the company. The company is also able to make proper amount of the

disclosure in regards of the liabilities and also it able to make proper amount of the

provision in regards of the obligation which are there in the past event of the

company.

3. As per the proper disclosure is been made by the company it can be said that the

company is able to make proper amount of the disclosure in the financial statement of

the company and also it help the financial user to take proper amount of the decision

in regards of the financial statement (Simnett & Huggins 2015). The company is able

to have proper adoption of the accounting standard so that it can able to have a proper

amount of the presentation in the company and also help the financial user to know

more about the financial position of the company. The balance sheet of the company

is able to give the financial information for two years so it help the user to easily

compare their performance and able to know how the company is able to perform in

the market. As all the information are there in the financial report so it help the user to

get all the information at one place and also help them to know the performance of the

company in regards of the liquidity and other aspects. So as from the above

discussion it can be said that Blackmores limited is able to provide all the qualitative

information in the company financial reporting so that it will help the investor and

other users to know more about the company and able to take necessary decision for

the same as whether they should invest in the company or not.

Part B: Integrated/Sustainability Reporting

Requirement (a):

The main goal which the sustainability report has is the development of the social and

environmental factor as it also was stated in the reporting of IIRC. There is some amount of

Accounting Theory

position of the company. The company is also able to make proper amount of the

disclosure in regards of the liabilities and also it able to make proper amount of the

provision in regards of the obligation which are there in the past event of the

company.

3. As per the proper disclosure is been made by the company it can be said that the

company is able to make proper amount of the disclosure in the financial statement of

the company and also it help the financial user to take proper amount of the decision

in regards of the financial statement (Simnett & Huggins 2015). The company is able

to have proper adoption of the accounting standard so that it can able to have a proper

amount of the presentation in the company and also help the financial user to know

more about the financial position of the company. The balance sheet of the company

is able to give the financial information for two years so it help the user to easily

compare their performance and able to know how the company is able to perform in

the market. As all the information are there in the financial report so it help the user to

get all the information at one place and also help them to know the performance of the

company in regards of the liquidity and other aspects. So as from the above

discussion it can be said that Blackmores limited is able to provide all the qualitative

information in the company financial reporting so that it will help the investor and

other users to know more about the company and able to take necessary decision for

the same as whether they should invest in the company or not.

Part B: Integrated/Sustainability Reporting

Requirement (a):

The main goal which the sustainability report has is the development of the social and

environmental factor as it also was stated in the reporting of IIRC. There is some amount of

8

Accounting Theory

difference in both reporting framework (Stacchezzini, Melloni & Lai 2016). As per the GRI

sustainability reporting is been concern it can be said that it help the company to minimize

the negative impact which the company business activity is making in regards of the society,

environment and community. In the integrated reporting system it does not only takes the

financial information but it also takes the non-financial information of the company so that it

able to show the future of the shareholder and help them to know whether the plan and

objective which the company is having in the future will help the shareholder or not. So it

can be said that the both reporting help the company to show different aspects of the

organization and so it help them to know all the information which are there in the company

whether it is financial or non-financial information (Stent & Dowler 2015).

The discussion show the difference which is there in between the sustainability

reporting and integrated reporting. So this can be said that the sustainability reporting help

the company to show all the information of the policy which are been made in regards of the

social, environmental and community. This process is also been carried in the integrated

reporting framework in a different way. This reporting framework shows the long term value

by presenting the financial and non-financial information of the company so that the

stakeholder will able to know their future in the company (Stubbs & Higgins 2014). The six

capital method is been adopted in the integrated reporting so that it can able to show both

financial and non-financial performance of the company. So the basic difference which is

there in both reporting is shown above of the discussion.

Requirement (b):

The number of the benefits and drawbacks which are there in the sustainability

reporting is been shown by Conventional accounting. It can be said that in the traditional

accounting system help in providing the risk and opportunity consideration of both financial

and non-financial information. The sustainability helps the stakeholder to know all the future

Accounting Theory

difference in both reporting framework (Stacchezzini, Melloni & Lai 2016). As per the GRI

sustainability reporting is been concern it can be said that it help the company to minimize

the negative impact which the company business activity is making in regards of the society,

environment and community. In the integrated reporting system it does not only takes the

financial information but it also takes the non-financial information of the company so that it

able to show the future of the shareholder and help them to know whether the plan and

objective which the company is having in the future will help the shareholder or not. So it

can be said that the both reporting help the company to show different aspects of the

organization and so it help them to know all the information which are there in the company

whether it is financial or non-financial information (Stent & Dowler 2015).

The discussion show the difference which is there in between the sustainability

reporting and integrated reporting. So this can be said that the sustainability reporting help

the company to show all the information of the policy which are been made in regards of the

social, environmental and community. This process is also been carried in the integrated

reporting framework in a different way. This reporting framework shows the long term value

by presenting the financial and non-financial information of the company so that the

stakeholder will able to know their future in the company (Stubbs & Higgins 2014). The six

capital method is been adopted in the integrated reporting so that it can able to show both

financial and non-financial performance of the company. So the basic difference which is

there in both reporting is shown above of the discussion.

Requirement (b):

The number of the benefits and drawbacks which are there in the sustainability

reporting is been shown by Conventional accounting. It can be said that in the traditional

accounting system help in providing the risk and opportunity consideration of both financial

and non-financial information. The sustainability helps the stakeholder to know all the future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Accounting Theory

strategies of the company and how it will help their interest to grow in the organization. As

the sustainability show the internal performances of the company so it can able to mislead the

external stakeholder in regards of the traditional accounting method.

The conventional accounting system helps the company to know the drawbacks and

benefits which are there in integrated reporting framework. The traditional accounting can be

beneficial also as it help the stakeholder to know the transparency and clarity of the issue and

performance in the organization. It will help them by providing the details of the profit which

the company is earning as it will show both the financial and non-financial information of the

company. The data which is been collected by the accountant of the traditional accounting

system as they able to face issues while interpreting the performance of the company in

regards of the financial and non-financial information of the company.

Requirement (c):

The concept of the sustainability reporting and integrated reporting can be describe

with some types of theory.

Integrated reporting:

To know more about the integrated reporting concept it has to know the application of

the stakeholder theory and agency theory. As per the stakeholder theory is been concern it say

that the company should take consideration all the stakeholder and not only the shareholder

while making any decision in the company as it will also affect each class of stakeholder of

the company whereas the agency theory suggest that the company is only working on behalf

of the shareholder and their only motive should be wealth maximization so that the

shareholder will able to get more amount of the return. As per both the theory the reason why

the company should include the integrated reporting so that it will able fulfils the requirement

Accounting Theory

strategies of the company and how it will help their interest to grow in the organization. As

the sustainability show the internal performances of the company so it can able to mislead the

external stakeholder in regards of the traditional accounting method.

The conventional accounting system helps the company to know the drawbacks and

benefits which are there in integrated reporting framework. The traditional accounting can be

beneficial also as it help the stakeholder to know the transparency and clarity of the issue and

performance in the organization. It will help them by providing the details of the profit which

the company is earning as it will show both the financial and non-financial information of the

company. The data which is been collected by the accountant of the traditional accounting

system as they able to face issues while interpreting the performance of the company in

regards of the financial and non-financial information of the company.

Requirement (c):

The concept of the sustainability reporting and integrated reporting can be describe

with some types of theory.

Integrated reporting:

To know more about the integrated reporting concept it has to know the application of

the stakeholder theory and agency theory. As per the stakeholder theory is been concern it say

that the company should take consideration all the stakeholder and not only the shareholder

while making any decision in the company as it will also affect each class of stakeholder of

the company whereas the agency theory suggest that the company is only working on behalf

of the shareholder and their only motive should be wealth maximization so that the

shareholder will able to get more amount of the return. As per both the theory the reason why

the company should include the integrated reporting so that it will able fulfils the requirement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Accounting Theory

of the shareholder and also the stakeholder of the company for gaining in the sustainability

performance of the organization.

Sustainability reporting:

In regards of the sustainability reporting is concern it able to use two types of theories.

The theories which are applied are legitimacy theory and stakeholder theory. As per the

legitimacy theory is been concern it state that the company should disclosed all its activities

in regards of environmental and social performance and should compulsory maintain societal

sustainability. So the above theories is been discuss so it can be sure that the company is able

to show both the financial information as well as non-financial information so that the

stakeholder will be able to know the survival of the organization in the community. This all

the points should be taken into consideration while implementing the reporting in the

organization.

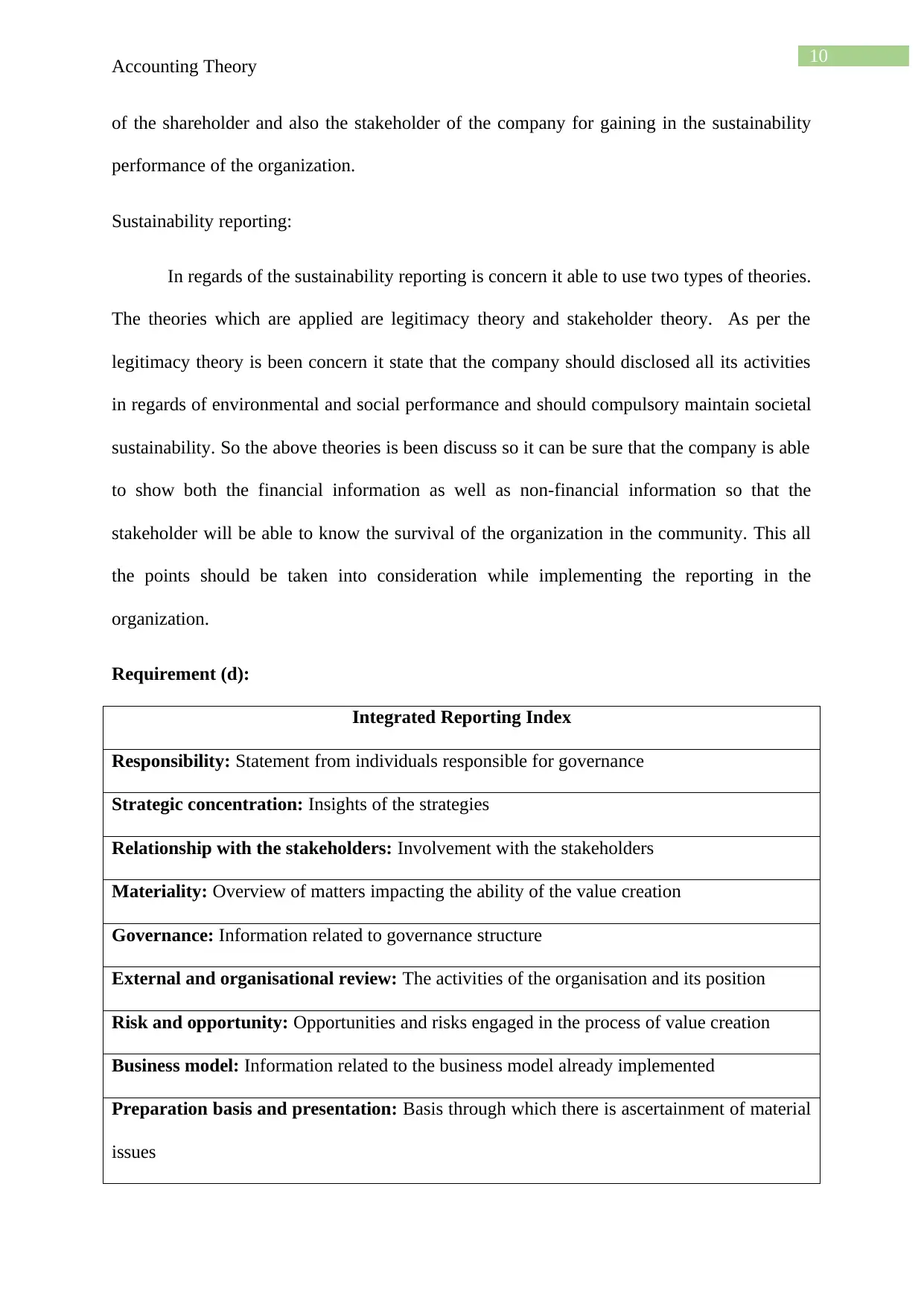

Requirement (d):

Integrated Reporting Index

Responsibility: Statement from individuals responsible for governance

Strategic concentration: Insights of the strategies

Relationship with the stakeholders: Involvement with the stakeholders

Materiality: Overview of matters impacting the ability of the value creation

Governance: Information related to governance structure

External and organisational review: The activities of the organisation and its position

Risk and opportunity: Opportunities and risks engaged in the process of value creation

Business model: Information related to the business model already implemented

Preparation basis and presentation: Basis through which there is ascertainment of material

issues

Accounting Theory

of the shareholder and also the stakeholder of the company for gaining in the sustainability

performance of the organization.

Sustainability reporting:

In regards of the sustainability reporting is concern it able to use two types of theories.

The theories which are applied are legitimacy theory and stakeholder theory. As per the

legitimacy theory is been concern it state that the company should disclosed all its activities

in regards of environmental and social performance and should compulsory maintain societal

sustainability. So the above theories is been discuss so it can be sure that the company is able

to show both the financial information as well as non-financial information so that the

stakeholder will be able to know the survival of the organization in the community. This all

the points should be taken into consideration while implementing the reporting in the

organization.

Requirement (d):

Integrated Reporting Index

Responsibility: Statement from individuals responsible for governance

Strategic concentration: Insights of the strategies

Relationship with the stakeholders: Involvement with the stakeholders

Materiality: Overview of matters impacting the ability of the value creation

Governance: Information related to governance structure

External and organisational review: The activities of the organisation and its position

Risk and opportunity: Opportunities and risks engaged in the process of value creation

Business model: Information related to the business model already implemented

Preparation basis and presentation: Basis through which there is ascertainment of material

issues

11

Accounting Theory

Performance: Information related to the fulfilment of strategic goals

Information disclosure of Blackmores limited:

As per the sustainability report of the company is been concern it can be said that they

have able to do the disclosure as per IIRC. The report also able to show the responsibility

which the individuals responsible for governance. The company is also able to show all the

strategies which are they have used in the strategy section of the report. It also able to

disclose all the material issue and other business model which show all the relationship and

resources of the company.

Requirement (e):

As per the website is been concern it can able to conclude that the company is

involved in the preparation of the integrated report which covers the sustainability social

reporting as well. The report cover all the aspects as the corporate social responsibility and

the sustainability initiatives of the company.

The report show that the company is able to show all the amount of the details which

are been required to be disclose in regards of the sustainability reporting. The report is able to

give all the non-financial information to the stakeholder. So it can be said that the company

is able to give more information as it have published the financial information and non-

financial information separately so that the user will able to understand all the details

properly.

As per the both company is been concern it can be said that they both have follow all

the norms and regulation while making the integrated reporting. The company Blackmores

limited is able to give more sufficient information of the non-financial which is not been able

to be provided by the Anheuser-Bush InBev.

Accounting Theory

Performance: Information related to the fulfilment of strategic goals

Information disclosure of Blackmores limited:

As per the sustainability report of the company is been concern it can be said that they

have able to do the disclosure as per IIRC. The report also able to show the responsibility

which the individuals responsible for governance. The company is also able to show all the

strategies which are they have used in the strategy section of the report. It also able to

disclose all the material issue and other business model which show all the relationship and

resources of the company.

Requirement (e):

As per the website is been concern it can able to conclude that the company is

involved in the preparation of the integrated report which covers the sustainability social

reporting as well. The report cover all the aspects as the corporate social responsibility and

the sustainability initiatives of the company.

The report show that the company is able to show all the amount of the details which

are been required to be disclose in regards of the sustainability reporting. The report is able to

give all the non-financial information to the stakeholder. So it can be said that the company

is able to give more information as it have published the financial information and non-

financial information separately so that the user will able to understand all the details

properly.

As per the both company is been concern it can be said that they both have follow all

the norms and regulation while making the integrated reporting. The company Blackmores

limited is able to give more sufficient information of the non-financial which is not been able

to be provided by the Anheuser-Bush InBev.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.