Analysis of Accounting Theory and Contemporary Issues (ACC706 Report)

VerifiedAdded on 2023/05/28

|14

|2627

|321

Report

AI Summary

This report provides a detailed analysis of Orica Limited's financial reporting practices, focusing on its compliance with the Australian Accounting Standards Board (AASB) and the conceptual framework. The report examines a news article concerning a drop in Orica's share price and discusses the company's adherence to both fundamental and enhancing qualitative characteristics of financial reporting. It delves into the application of accounting theories, specifically positive agency theory and stakeholder normative theory, within the context of Orica Limited's operations. Furthermore, the report compares Orica's financial performance with that of its competitor, BHP Billiton, and evaluates the implications of its financial position on investment decisions. The analysis covers the preparation of general-purpose financial statements, highlighting the company's compliance with relevant standards and regulations. The report concludes with a summary of findings, emphasizing Orica Limited's adherence to accounting principles while acknowledging the company's financial performance challenges.

Running head: ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Accounting Theory and Contemporary Issues

Name of the Student

Name of the University

Author’s Note

Accounting Theory and Contemporary Issues

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Executive Summary

It is the responsibility of the companies to comply with the requirements of conceptual

framework for the preparation and presentation of their financial statements. At the same

time, the companies are needed to comply with the measurement requirements of the

conceptual framework. This report analyses various aspects of the compliance of Orica

Limited with the requirements of conceptual framework. In addition, this report also takes

into consideration the discussion of an issue related to the company. At the same time, this

report also tests the compliance of the company with both the fundamental and enhancing

qualitative characteristics of financial reporting. The report also involves in the analysis of

certain theories in respect to the company.

Executive Summary

It is the responsibility of the companies to comply with the requirements of conceptual

framework for the preparation and presentation of their financial statements. At the same

time, the companies are needed to comply with the measurement requirements of the

conceptual framework. This report analyses various aspects of the compliance of Orica

Limited with the requirements of conceptual framework. In addition, this report also takes

into consideration the discussion of an issue related to the company. At the same time, this

report also tests the compliance of the company with both the fundamental and enhancing

qualitative characteristics of financial reporting. The report also involves in the analysis of

certain theories in respect to the company.

2ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Table of Contents

Introduction................................................................................................................................3

Discussion of the Issue...............................................................................................................4

Analysis of the Annual Report...................................................................................................5

Compliance with the Conceptual Framework............................................................................5

Enhancing Qualitative Characteristics.......................................................................................7

Comparison of the Annual Report.............................................................................................8

Preparation of General Purpose Financial Statements...............................................................9

Application of Accounting Theories........................................................................................10

Investment Decision.................................................................................................................10

Conclusion or Summary...........................................................................................................11

References................................................................................................................................12

Table of Contents

Introduction................................................................................................................................3

Discussion of the Issue...............................................................................................................4

Analysis of the Annual Report...................................................................................................5

Compliance with the Conceptual Framework............................................................................5

Enhancing Qualitative Characteristics.......................................................................................7

Comparison of the Annual Report.............................................................................................8

Preparation of General Purpose Financial Statements...............................................................9

Application of Accounting Theories........................................................................................10

Investment Decision.................................................................................................................10

Conclusion or Summary...........................................................................................................11

References................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Introduction

The main aim of this report is the analysis and evaluation of a certain accounting issue

in one of the top 100 Australian Stock Exchange (ASX) listed companies. For this report,

Orica Limited is taken into consideration.

This report also takes into consideration the discussion about a news article about

Orica Limited that shows that drop of the share price of the company.

In this context, one major issue for the company is the compliance of the company

with various requirements of Australian Accounting Standard Board (AASB) and Conceptual

Framework. It is the prime responsibility of the business organisations under ASX to comply

with the standards and principles of accounting conceptual framework with the aim to

prepare and present the financial statements on the true and correct manner. Chances of

financial frauds and errors increase in case the companies do not comply with the standards

of AASB and conceptual framework (aasb.gov.au 2018).

Orica Limited is a multinational company based on Australia and is the world’s

largest provider of commercial explosives along with the blasting system for mines, oil, gas,

construction and others. The company has a workforce of around 11500 and it has customer

base more the hundred countries all over the world (orica.com 2018).

In the recent years, one major accounting issue is not to comply with the required

accounting standards and principles for financial reporting. This aspect creates chances for

financial frauds along with the collapse of the companies. In order to avoid this, the

companies must comply with relevant accounting standards. In addition, this report also

involves in the analysis of two specific theories in relation to the financial reporting of Orica

Limited. These theories are positive theory and the stakeholder theory in relation to the

company.

Introduction

The main aim of this report is the analysis and evaluation of a certain accounting issue

in one of the top 100 Australian Stock Exchange (ASX) listed companies. For this report,

Orica Limited is taken into consideration.

This report also takes into consideration the discussion about a news article about

Orica Limited that shows that drop of the share price of the company.

In this context, one major issue for the company is the compliance of the company

with various requirements of Australian Accounting Standard Board (AASB) and Conceptual

Framework. It is the prime responsibility of the business organisations under ASX to comply

with the standards and principles of accounting conceptual framework with the aim to

prepare and present the financial statements on the true and correct manner. Chances of

financial frauds and errors increase in case the companies do not comply with the standards

of AASB and conceptual framework (aasb.gov.au 2018).

Orica Limited is a multinational company based on Australia and is the world’s

largest provider of commercial explosives along with the blasting system for mines, oil, gas,

construction and others. The company has a workforce of around 11500 and it has customer

base more the hundred countries all over the world (orica.com 2018).

In the recent years, one major accounting issue is not to comply with the required

accounting standards and principles for financial reporting. This aspect creates chances for

financial frauds along with the collapse of the companies. In order to avoid this, the

companies must comply with relevant accounting standards. In addition, this report also

involves in the analysis of two specific theories in relation to the financial reporting of Orica

Limited. These theories are positive theory and the stakeholder theory in relation to the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Discussion of the Issue

(Source: afr.com 2018)

It can be seen from the above news that the share price of Orica Limited crashes close

to three months low due to the untimely acquisition of a brand new ammonium nitrate facility

in Western Australia, inadvertent maintenance and plans to the record close to $300 million

of impairments as well as provisions on the other business parts. However, after this, the

management of the company announced that the operation of the new plant would not be

started until 2018. Based on the above, it can be said that it is a major financial issue for the

company that is related to the financial performance as well as unplanned acquisition.

Discussion of the Issue

(Source: afr.com 2018)

It can be seen from the above news that the share price of Orica Limited crashes close

to three months low due to the untimely acquisition of a brand new ammonium nitrate facility

in Western Australia, inadvertent maintenance and plans to the record close to $300 million

of impairments as well as provisions on the other business parts. However, after this, the

management of the company announced that the operation of the new plant would not be

started until 2018. Based on the above, it can be said that it is a major financial issue for the

company that is related to the financial performance as well as unplanned acquisition.

5ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Analysis of the Annual Report

It needs to be mentioned that the annual report of Orica Limited is for publishing the

information of the company and its controlled entities for the year ended 30 September 2018

(orica.com 2018). It needs to be mentioned that the general purpose financial statements of

Orica Limited has been prepared as well as presented as per the standards of Australian

Accounting Standards and the Corporations Act 2001; at the same time, the company has

complied with the principles of International Financial Reporting Standards (IFRS) and

International Accounting Standard Board (IASB) (orica.com 2018). At the same time, it can

be observed from the 2018 Annual Report of Orica Limited that the company has followed

the principles of ASIC Corporations Instrument 2016/191 (orica.com 2018). Thus, it can be

observed that the company has complied with the required principles for accounting.

Compliance with the Conceptual Framework

There are five elements of AASB conceptual framework; they are assets, liabilities,

equity, expenses and income. In case of the measurement requirements, AASB conceptual

framework has put certain obligation on the ASX listed companies. As per the conceptual

framework, companies should not adopt only one measurement basis for measuring the

elements like assets, liabilities and others and the reason is that it fails to provide the relevant

financial information to the users. There are four measurement mechanism for the companies

as per AASB conceptual framework; they are Historical cost, current value, Fair Value and

Value in use. The following discussion shows whether Orica Limited has complied with the

measurement requirements of AASB or not:

Analysis of the Annual Report

It needs to be mentioned that the annual report of Orica Limited is for publishing the

information of the company and its controlled entities for the year ended 30 September 2018

(orica.com 2018). It needs to be mentioned that the general purpose financial statements of

Orica Limited has been prepared as well as presented as per the standards of Australian

Accounting Standards and the Corporations Act 2001; at the same time, the company has

complied with the principles of International Financial Reporting Standards (IFRS) and

International Accounting Standard Board (IASB) (orica.com 2018). At the same time, it can

be observed from the 2018 Annual Report of Orica Limited that the company has followed

the principles of ASIC Corporations Instrument 2016/191 (orica.com 2018). Thus, it can be

observed that the company has complied with the required principles for accounting.

Compliance with the Conceptual Framework

There are five elements of AASB conceptual framework; they are assets, liabilities,

equity, expenses and income. In case of the measurement requirements, AASB conceptual

framework has put certain obligation on the ASX listed companies. As per the conceptual

framework, companies should not adopt only one measurement basis for measuring the

elements like assets, liabilities and others and the reason is that it fails to provide the relevant

financial information to the users. There are four measurement mechanism for the companies

as per AASB conceptual framework; they are Historical cost, current value, Fair Value and

Value in use. The following discussion shows whether Orica Limited has complied with the

measurement requirements of AASB or not:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CONTEMPORARY ISSUES

(Source: orica.com 2018)

It can be seen from the above image that Orica Limited has adopted the mechanism of

both historical cost and fair value for the measurement of their assets and liabilities. Further

evidence can be obtained from below:

(Source: orica.com 2018)

It can be observed from the above images from the annual report of Orica Limited

that the company has used both the fair value and historical cost method for the measurement

of different elements of conceptual framework such as assets, liabilities, income and others.

(Source: orica.com 2018)

It can be seen from the above image that Orica Limited has adopted the mechanism of

both historical cost and fair value for the measurement of their assets and liabilities. Further

evidence can be obtained from below:

(Source: orica.com 2018)

It can be observed from the above images from the annual report of Orica Limited

that the company has used both the fair value and historical cost method for the measurement

of different elements of conceptual framework such as assets, liabilities, income and others.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Hence, it can be seen from the above discussion that Orica Limited has made compliance

with all the requirements of AASB and conceptual framework.

According to the AASB conceptual framework, financial reports of the companies

must have the fundamental as well as enhancing qualitative characteristics; and the following

discussion shows the compliance of Orica Limited with these characteristics.

Fundamental Qualitative Characteristics

Relevance: Orica Limited provides relevant financial information to the users of the financial

statements for decision-making purposes that include both the confirmatory and predictive

value. The users of the financial statements can predict the financial outcome along with the

analysis of previous judgments (Callen, Khan and Lu 2013).

Faithful Representation: Orica Limited provides both the natural description as well as

numerical description of their different financial elements like assets, liabilities and others

with the aim to make the information complete. Neutral and free from errors.

Enhancing Qualitative Characteristics

Comparability: Orica Limited presents the financial information of their business in such a

manner so that the users can compare them with another company or with the different

timeline of the same company.

Verifiability: The users of the financial statements can verify the used method of accounting

in the financial statements with the help of accounting knowledge and independent

observation (Gebhardt, Mora and Wagenhofer 2014).

Timeliness: Orica Limited provides the necessary information to the users at timely basis

through various financial statements for their decision-making process.

Hence, it can be seen from the above discussion that Orica Limited has made compliance

with all the requirements of AASB and conceptual framework.

According to the AASB conceptual framework, financial reports of the companies

must have the fundamental as well as enhancing qualitative characteristics; and the following

discussion shows the compliance of Orica Limited with these characteristics.

Fundamental Qualitative Characteristics

Relevance: Orica Limited provides relevant financial information to the users of the financial

statements for decision-making purposes that include both the confirmatory and predictive

value. The users of the financial statements can predict the financial outcome along with the

analysis of previous judgments (Callen, Khan and Lu 2013).

Faithful Representation: Orica Limited provides both the natural description as well as

numerical description of their different financial elements like assets, liabilities and others

with the aim to make the information complete. Neutral and free from errors.

Enhancing Qualitative Characteristics

Comparability: Orica Limited presents the financial information of their business in such a

manner so that the users can compare them with another company or with the different

timeline of the same company.

Verifiability: The users of the financial statements can verify the used method of accounting

in the financial statements with the help of accounting knowledge and independent

observation (Gebhardt, Mora and Wagenhofer 2014).

Timeliness: Orica Limited provides the necessary information to the users at timely basis

through various financial statements for their decision-making process.

8ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Understandability: With the assistance of the notes to the financial statements, the users can

understand the financial statements of Orica Limited.

Comparison of the Annual Report

One of the major competitors of Orica Limited is BHP Billiton as both of them

operate in the mining industry of Australia. Following discussion compares the financial

performance of Orica Limited with BHP Billiton:

(Source: orica.com 2018 and bhp.com 2018)

The above images of the income statements of Orica Limited and BHP Billion shows

that Orica Limited registered net loss for the year 2018 where BHP Billiton registered huge

profit for the same period.

Understandability: With the assistance of the notes to the financial statements, the users can

understand the financial statements of Orica Limited.

Comparison of the Annual Report

One of the major competitors of Orica Limited is BHP Billiton as both of them

operate in the mining industry of Australia. Following discussion compares the financial

performance of Orica Limited with BHP Billiton:

(Source: orica.com 2018 and bhp.com 2018)

The above images of the income statements of Orica Limited and BHP Billion shows

that Orica Limited registered net loss for the year 2018 where BHP Billiton registered huge

profit for the same period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CONTEMPORARY ISSUES

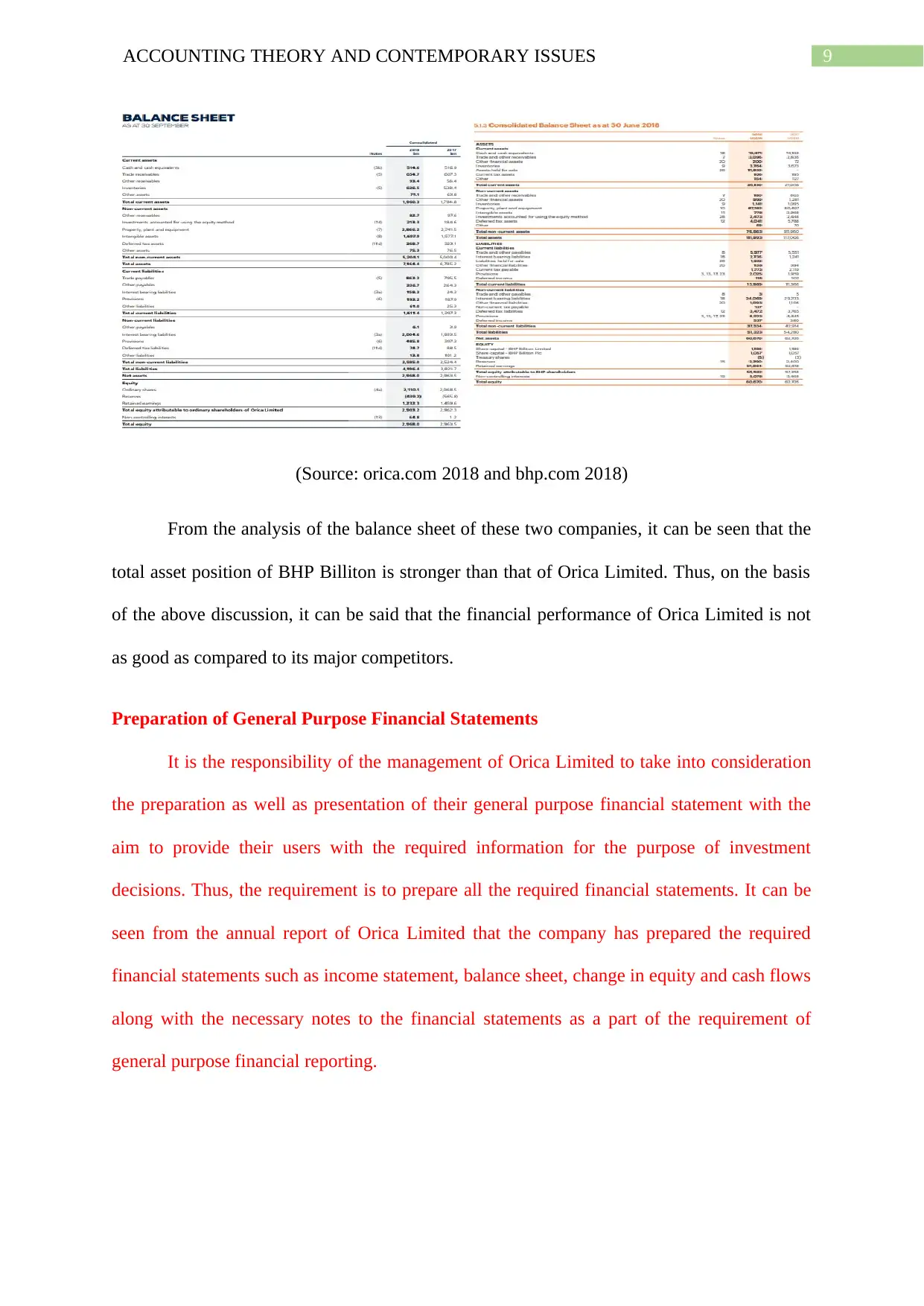

(Source: orica.com 2018 and bhp.com 2018)

From the analysis of the balance sheet of these two companies, it can be seen that the

total asset position of BHP Billiton is stronger than that of Orica Limited. Thus, on the basis

of the above discussion, it can be said that the financial performance of Orica Limited is not

as good as compared to its major competitors.

Preparation of General Purpose Financial Statements

It is the responsibility of the management of Orica Limited to take into consideration

the preparation as well as presentation of their general purpose financial statement with the

aim to provide their users with the required information for the purpose of investment

decisions. Thus, the requirement is to prepare all the required financial statements. It can be

seen from the annual report of Orica Limited that the company has prepared the required

financial statements such as income statement, balance sheet, change in equity and cash flows

along with the necessary notes to the financial statements as a part of the requirement of

general purpose financial reporting.

(Source: orica.com 2018 and bhp.com 2018)

From the analysis of the balance sheet of these two companies, it can be seen that the

total asset position of BHP Billiton is stronger than that of Orica Limited. Thus, on the basis

of the above discussion, it can be said that the financial performance of Orica Limited is not

as good as compared to its major competitors.

Preparation of General Purpose Financial Statements

It is the responsibility of the management of Orica Limited to take into consideration

the preparation as well as presentation of their general purpose financial statement with the

aim to provide their users with the required information for the purpose of investment

decisions. Thus, the requirement is to prepare all the required financial statements. It can be

seen from the annual report of Orica Limited that the company has prepared the required

financial statements such as income statement, balance sheet, change in equity and cash flows

along with the necessary notes to the financial statements as a part of the requirement of

general purpose financial reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Application of Accounting Theories

Positive Theory of Agency Theory: According to the concept of this theory, business

organization is an agency and it provides a relationship for a complex set of contracts and for

this reason, there is the generation of agency cost due to different interests and contracts

(Bosse and Phillips 2016). The application of this theory can be seen in the operation of Orica

Limited. As per this theory, Orica Limited is the principal and the management of Orica

Limited can be considered as the agent of the company. As per the agency theory, the agents

make decision on behalf of the principals. It can be seen in case of Orica Limited that the

managements of the company makes the required decisions and performs the tasks on behalf

of the principle that is the company (Dawar 2014).

Stakeholders Normative Theory: According to the concepts of stakeholder theory, all the

stakeholders have intrinsic moral value or worth. Stakeholders are the persona or groups

having legitimate interest in the activities of the business organizations. In addition, the

companies need to consider the interests of all the stakeholders as intrinsic value and thus, the

need to address the interest of all the stakeholders (Hasnas 2013). It needs to be mentioned

that Orica Limited has applied this concept of stakeholder normative theory in their business

operations by addressing the needs of their stakeholders. For example, existing investors and

potential investors are the major stakeholders of Orica Limited; and they are interested in

investing in the company for getting high return. For this reason, Orica Limited has addressed

their interest by providing them with all the required financial information about the financial

performance and position for the purpose of their investment decision-making (Harrison, J.S.

and Wicks 2013).

Investment Decision

At the time of investment, the investors considers the financial performance of the

companies and whether the companies have any accounting issues or not (Levy 2015). It can

Application of Accounting Theories

Positive Theory of Agency Theory: According to the concept of this theory, business

organization is an agency and it provides a relationship for a complex set of contracts and for

this reason, there is the generation of agency cost due to different interests and contracts

(Bosse and Phillips 2016). The application of this theory can be seen in the operation of Orica

Limited. As per this theory, Orica Limited is the principal and the management of Orica

Limited can be considered as the agent of the company. As per the agency theory, the agents

make decision on behalf of the principals. It can be seen in case of Orica Limited that the

managements of the company makes the required decisions and performs the tasks on behalf

of the principle that is the company (Dawar 2014).

Stakeholders Normative Theory: According to the concepts of stakeholder theory, all the

stakeholders have intrinsic moral value or worth. Stakeholders are the persona or groups

having legitimate interest in the activities of the business organizations. In addition, the

companies need to consider the interests of all the stakeholders as intrinsic value and thus, the

need to address the interest of all the stakeholders (Hasnas 2013). It needs to be mentioned

that Orica Limited has applied this concept of stakeholder normative theory in their business

operations by addressing the needs of their stakeholders. For example, existing investors and

potential investors are the major stakeholders of Orica Limited; and they are interested in

investing in the company for getting high return. For this reason, Orica Limited has addressed

their interest by providing them with all the required financial information about the financial

performance and position for the purpose of their investment decision-making (Harrison, J.S.

and Wicks 2013).

Investment Decision

At the time of investment, the investors considers the financial performance of the

companies and whether the companies have any accounting issues or not (Levy 2015). It can

11ACCOUNTING THEORY AND CONTEMPORARY ISSUES

be seen from the analysis of the annual report of Orica Limited that the company had made

all the required compliance with the needed standards, regulations and principles of AASB,

Corporations Act 2001 and Conceptual Framework. In addition, financial statements of Orica

Limited includes both the fundamental as well as enhancing qualitative characteristics.

However, it needs to consider that the company has registered net loss in the current financial

year. At the same time, Orica Limited has not performed in better manner as compared to

their competitors like BHP Billiton. Thus, in spite of the absence of accounting issues,

financial performance of the company is a concern for the investors. For this reason, the

investors should not invest in the company (Xu 2015).

Conclusion or Summary

As per the above discussion, Orica Limited has followed all the accounting principles

and standards of conceptual framework along with complying with the fundamental and

enhancing qualitative characteristics of financial reporting. However, the financial

performance of the company in the current year is not effective due to the presence of net

loss. In addition, Orica Limited has applied the concepts of agency theory and stakeholder

theory in their business.

be seen from the analysis of the annual report of Orica Limited that the company had made

all the required compliance with the needed standards, regulations and principles of AASB,

Corporations Act 2001 and Conceptual Framework. In addition, financial statements of Orica

Limited includes both the fundamental as well as enhancing qualitative characteristics.

However, it needs to consider that the company has registered net loss in the current financial

year. At the same time, Orica Limited has not performed in better manner as compared to

their competitors like BHP Billiton. Thus, in spite of the absence of accounting issues,

financial performance of the company is a concern for the investors. For this reason, the

investors should not invest in the company (Xu 2015).

Conclusion or Summary

As per the above discussion, Orica Limited has followed all the accounting principles

and standards of conceptual framework along with complying with the fundamental and

enhancing qualitative characteristics of financial reporting. However, the financial

performance of the company in the current year is not effective due to the presence of net

loss. In addition, Orica Limited has applied the concepts of agency theory and stakeholder

theory in their business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.