Accounting Theory and Issues Report: Boral Limited Financial Analysis

VerifiedAdded on 2023/05/30

|12

|2406

|291

Report

AI Summary

This report delves into the conceptual framework of general purpose financial reporting (GPFR) and its application, using Boral Limited's 2018 financial report as a case study. The report explores the objectives of GPFR, including providing useful information for decision-making, predicting cash flows, and understanding economic resources and claims. It examines the elements of financial statements (assets, liabilities, equity, revenues, and expenses), along with recognition and measurement principles and assumptions. The report also analyzes the qualitative characteristics of financial information, differentiating between primary characteristics (relevance, reliability, and materiality) and secondary characteristics (comparability and consistency). The conclusion emphasizes Boral Limited's compliance with GPFR requirements, highlighting the reliability of the financial information for user decision-making and the consistent application of recognition criteria. The report provides a thorough overview of accounting theory and its practical application in financial reporting.

Running head: ACCOUNTING THEORY AND ISSUES

Accounting theory and issues

Name of the student

Name of the university

Student ID

Author note

Accounting theory and issues

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND ISSUES

Table of Contents

1.0 Introduction..........................................................................................................................2

2.0 Objectives of the general purpose financial reporting.........................................................2

2.1 Useful information for making decision..........................................................................3

2.2 Prediction of cash flows...................................................................................................3

2.3 Economic resources and changes in resources and claims..............................................3

3.0 Elements...............................................................................................................................3

3.1 Asset.................................................................................................................................4

3.2 Liabilities..........................................................................................................................4

3.3 Equity...............................................................................................................................4

3.4 Revenues..........................................................................................................................4

3.5 Expenses...........................................................................................................................5

4.0 Recognition and measurement.............................................................................................5

4.1 Assumptions.....................................................................................................................5

4.2 Principles..........................................................................................................................5

5.0 Qualitative characteristics....................................................................................................6

5.1 Primary.............................................................................................................................6

5.2 Secondary.........................................................................................................................7

6.0 Conclusion............................................................................................................................8

Reference..................................................................................................................................10

Table of Contents

1.0 Introduction..........................................................................................................................2

2.0 Objectives of the general purpose financial reporting.........................................................2

2.1 Useful information for making decision..........................................................................3

2.2 Prediction of cash flows...................................................................................................3

2.3 Economic resources and changes in resources and claims..............................................3

3.0 Elements...............................................................................................................................3

3.1 Asset.................................................................................................................................4

3.2 Liabilities..........................................................................................................................4

3.3 Equity...............................................................................................................................4

3.4 Revenues..........................................................................................................................4

3.5 Expenses...........................................................................................................................5

4.0 Recognition and measurement.............................................................................................5

4.1 Assumptions.....................................................................................................................5

4.2 Principles..........................................................................................................................5

5.0 Qualitative characteristics....................................................................................................6

5.1 Primary.............................................................................................................................6

5.2 Secondary.........................................................................................................................7

6.0 Conclusion............................................................................................................................8

Reference..................................................................................................................................10

2ACCOUNTING THEORY AND ISSUES

1.0 Introduction

Conceptual framework associated with general purpose financial reporting provides

IPSASB (International public sector accounting standards board) with various concepts for

strengthening the development of IPSASs (International Public Sector Accounting

Standards). It deals with various concepts required for presenting the general purpose

financial reporting (GPFR) in accordance with the accrual accounting basis. Various concepts

required to be considered includes objectivity, recognition criteria, qualitative characteristic,

elements, financial statements and constraints (A Review of the IASB’s Conceptual

Framework for Financial Reporting 2018).

Boral Limited, the ASX listed company is engaged in manufacturing and supplying

the construction materials all over Australia, Asia and United States. It delivers blocks,

asphalt, bricks, concretes, cementitious materials, retaining walls, pavers, plasterboards, roof

tiles, stones, window, masonry, roofing, fly ash and material technical. Apart from that is is

engaged in landfill, property and transport activities (Boral.com.au 2018).

2.0 Objectives of the GPFR

The financial statement of the company represents consolidated results of the

company. It is a for-profit company that is limited by the shares and domiciled and

incorporated in Australia and company’s shares are traded in ASX. It is observed from the

financial report of the company for the year ended 2018 that the GPFR is prepared as per the

requirement of Corporation Act 2001 and AASs (Australian Accounting Standards) adopted

by AASB (Australian Accounting Standards Board). Further, the CFS (Consolidated financial

1.0 Introduction

Conceptual framework associated with general purpose financial reporting provides

IPSASB (International public sector accounting standards board) with various concepts for

strengthening the development of IPSASs (International Public Sector Accounting

Standards). It deals with various concepts required for presenting the general purpose

financial reporting (GPFR) in accordance with the accrual accounting basis. Various concepts

required to be considered includes objectivity, recognition criteria, qualitative characteristic,

elements, financial statements and constraints (A Review of the IASB’s Conceptual

Framework for Financial Reporting 2018).

Boral Limited, the ASX listed company is engaged in manufacturing and supplying

the construction materials all over Australia, Asia and United States. It delivers blocks,

asphalt, bricks, concretes, cementitious materials, retaining walls, pavers, plasterboards, roof

tiles, stones, window, masonry, roofing, fly ash and material technical. Apart from that is is

engaged in landfill, property and transport activities (Boral.com.au 2018).

2.0 Objectives of the GPFR

The financial statement of the company represents consolidated results of the

company. It is a for-profit company that is limited by the shares and domiciled and

incorporated in Australia and company’s shares are traded in ASX. It is observed from the

financial report of the company for the year ended 2018 that the GPFR is prepared as per the

requirement of Corporation Act 2001 and AASs (Australian Accounting Standards) adopted

by AASB (Australian Accounting Standards Board). Further, the CFS (Consolidated financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND ISSUES

statements) of the company is complied with the IFRS (International financial reporting

standards) adopted by IASB (International Accounting Standards Board).

2.1 Useful information for making decision

Purpose of financial reporting by publicly held entities are to provide the useful

information of the entity to the users for enabling them to make appropriate decisions based

on the accounting data of the company.

2.2 Prediction of cash flows

Conceptual framework requires the financial statements to be presented in such a way

that the amount of cash flows can be predicted from it. From the cash flow statement of the

company for the year ended 2018 it can be found that the cash balance from each activities

like operating, investing and financing activities are clearly mentioned (De Villiers, Rinaldi

and Unerman 2014). Further, the cash balances at the beginning of the year as well as closing

of the year are mentioned clearly.

2.3 Economic resources and changes in resources and claims

As per the compliance of conceptual framework financial statement shall provide

clear information as regards to the available resources of the entity, sources through which

the resources are generated and the changes in the resources. It is noticed from the company’s

financial report that entity’s financial statement clearly stated the changes in resource levels

and its generation source (Garrett, Hoitash and Prawitt 2014).

3.0 Elements

As per the requirement of GPFRs the financial statements shall include various

elements like asset, liabilities, equity, revenues and expenses to provide proper information to

the users. The entity recognises any element in its financial statement when its value can be

statements) of the company is complied with the IFRS (International financial reporting

standards) adopted by IASB (International Accounting Standards Board).

2.1 Useful information for making decision

Purpose of financial reporting by publicly held entities are to provide the useful

information of the entity to the users for enabling them to make appropriate decisions based

on the accounting data of the company.

2.2 Prediction of cash flows

Conceptual framework requires the financial statements to be presented in such a way

that the amount of cash flows can be predicted from it. From the cash flow statement of the

company for the year ended 2018 it can be found that the cash balance from each activities

like operating, investing and financing activities are clearly mentioned (De Villiers, Rinaldi

and Unerman 2014). Further, the cash balances at the beginning of the year as well as closing

of the year are mentioned clearly.

2.3 Economic resources and changes in resources and claims

As per the compliance of conceptual framework financial statement shall provide

clear information as regards to the available resources of the entity, sources through which

the resources are generated and the changes in the resources. It is noticed from the company’s

financial report that entity’s financial statement clearly stated the changes in resource levels

and its generation source (Garrett, Hoitash and Prawitt 2014).

3.0 Elements

As per the requirement of GPFRs the financial statements shall include various

elements like asset, liabilities, equity, revenues and expenses to provide proper information to

the users. The entity recognises any element in its financial statement when its value can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND ISSUES

reliably measured and it is apparent that the future economic benefit will flow to the entity or

economic outflow will take place for fulfilling any obligation.

3.1 Asset

When it is likely that future economic benefits related to the particular asset will be

inflow for the entity it recognizes the asset it its balance sheet. It is recognised from the

company’s balance sheet for the year ended 30th June 2018 that the asset of the company is

segregated into current assets as well as non-current assets. While the current assets include

cash, inventories, receivables and financial assets, non-current assets include PP&E,

intangible assets, receivables, investors and financial assets (Kogan, Sudit and Vasarhelyi

2018).

3.2 Liabilities

When it is likely that the future economic outflow related to fulfilment of an

obligation will take place for the entity it recognizes obligation as liability in its balance

sheet. It is recognised from the company’s balance sheet for the year ended 30th June 2018

that the liabilities of the company is segregated into current liabilities and non-current non-

current. Current liabilities include trade creditors, financial liabilities, borrowing and loans,

current tax liabilities and provisions whereas the non-current assets long term trade creditors,

financial liabilities, borrowing and loans, liabilities for employee benefits, deferred tax

liabilities and provisions (Morioka and De Carvalho 2016).

3.3 Equity

Equity section of the balance sheet for the company includes issued capital, retained

earnings and reserves. Further, details regarding each item like opening balance and closing

balances are disclosed through notes to the accounts.

reliably measured and it is apparent that the future economic benefit will flow to the entity or

economic outflow will take place for fulfilling any obligation.

3.1 Asset

When it is likely that future economic benefits related to the particular asset will be

inflow for the entity it recognizes the asset it its balance sheet. It is recognised from the

company’s balance sheet for the year ended 30th June 2018 that the asset of the company is

segregated into current assets as well as non-current assets. While the current assets include

cash, inventories, receivables and financial assets, non-current assets include PP&E,

intangible assets, receivables, investors and financial assets (Kogan, Sudit and Vasarhelyi

2018).

3.2 Liabilities

When it is likely that the future economic outflow related to fulfilment of an

obligation will take place for the entity it recognizes obligation as liability in its balance

sheet. It is recognised from the company’s balance sheet for the year ended 30th June 2018

that the liabilities of the company is segregated into current liabilities and non-current non-

current. Current liabilities include trade creditors, financial liabilities, borrowing and loans,

current tax liabilities and provisions whereas the non-current assets long term trade creditors,

financial liabilities, borrowing and loans, liabilities for employee benefits, deferred tax

liabilities and provisions (Morioka and De Carvalho 2016).

3.3 Equity

Equity section of the balance sheet for the company includes issued capital, retained

earnings and reserves. Further, details regarding each item like opening balance and closing

balances are disclosed through notes to the accounts.

5ACCOUNTING THEORY AND ISSUES

3.4 Revenues

Revenues from sales are recognised when the goods are delivered to the customers

and that is the point of time when the goods are accepted by the customer and the rewards

and risks related to the goods are transferred to the customer. Further, the revenue is

recognised if the amount can be reliably measured and it is likely that the consideration will

be recovered and no continuing management is involved with goods (Boral.com.au 2018).

3.5 Expenses

Expenses are recognised by the company when economic resources are expensed by it

for generating economic benefits. Further, the expenses shall be related to increase in

liabilities or decrease in assets that can be reliably measured.

4.0 Recognition and measurement

Recognition and measurement is another key factor to determine whether the

information provided through financial statement of the company are properly recognised or

measured as per the requirement of GPFRs.

4.1 Assumptions

Financial statements preparation requires the management to make estimates,

assumptions and judgements regarding future events. Assumptions made by the company

regarding revenues, receivables, intangible assets, PPE, provisions and tax expenses are

properly disclosed through the notes. Further, it is recognised from the financial statement

that the Director’s of the company regularly review the dividend policy and capital structure

of the company and do so for assessing the company’s going concern status (Boral.com.au

2018). Further, the company in compliance with the requirement of GPFRs publish their

financial statements on annual basis and 6 months basis.

3.4 Revenues

Revenues from sales are recognised when the goods are delivered to the customers

and that is the point of time when the goods are accepted by the customer and the rewards

and risks related to the goods are transferred to the customer. Further, the revenue is

recognised if the amount can be reliably measured and it is likely that the consideration will

be recovered and no continuing management is involved with goods (Boral.com.au 2018).

3.5 Expenses

Expenses are recognised by the company when economic resources are expensed by it

for generating economic benefits. Further, the expenses shall be related to increase in

liabilities or decrease in assets that can be reliably measured.

4.0 Recognition and measurement

Recognition and measurement is another key factor to determine whether the

information provided through financial statement of the company are properly recognised or

measured as per the requirement of GPFRs.

4.1 Assumptions

Financial statements preparation requires the management to make estimates,

assumptions and judgements regarding future events. Assumptions made by the company

regarding revenues, receivables, intangible assets, PPE, provisions and tax expenses are

properly disclosed through the notes. Further, it is recognised from the financial statement

that the Director’s of the company regularly review the dividend policy and capital structure

of the company and do so for assessing the company’s going concern status (Boral.com.au

2018). Further, the company in compliance with the requirement of GPFRs publish their

financial statements on annual basis and 6 months basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND ISSUES

4.2 Principles

Financial statements of the company are prepared on the foundation of historical cost

except for the revaluation of few financial instruments. Cost is depended on the fair values of

consideration that is given for exchanging the assets. Amounts are reported in Australian

dollars, unless it is note otherwise. Further, the financial statements are prepared taking into

consideration the matching principle (Zhang and Andrew 2014). For instance, income is

reported on systematic basis over periods required for matching with related costs under

which it required to be compensated. Further, details regarding all the items are properly

disclosed through notes to the accounts.

5.0 Qualitative characteristics

Qualitative characteristics for the information provided through financial statements

of the company recognizes the types of information those seems to be most important for the

users of the financial statements while making decisions on the basis of the information

provided.

5.1 Primary

Primary requirement of financial statement’s preparation as per GPFRs is the

information shall be relevant and reliable so that the users can make their valuable decisions.

Relevance – Financial information presented in the financial statement of the

company shall be presented in such manner that the information will be relevant to the

users while making any decisions. From the financial report of Boral Limited for the

year closed on 30th June 2018 it is noticed that financial data are presented and

segregated in proper manner so that the users find it relevant (Zhang and Andrew

2014). Further, the information is presented within the time frame to which it relates.

It enables the users to make comparative assessment with the previous period’s

4.2 Principles

Financial statements of the company are prepared on the foundation of historical cost

except for the revaluation of few financial instruments. Cost is depended on the fair values of

consideration that is given for exchanging the assets. Amounts are reported in Australian

dollars, unless it is note otherwise. Further, the financial statements are prepared taking into

consideration the matching principle (Zhang and Andrew 2014). For instance, income is

reported on systematic basis over periods required for matching with related costs under

which it required to be compensated. Further, details regarding all the items are properly

disclosed through notes to the accounts.

5.0 Qualitative characteristics

Qualitative characteristics for the information provided through financial statements

of the company recognizes the types of information those seems to be most important for the

users of the financial statements while making decisions on the basis of the information

provided.

5.1 Primary

Primary requirement of financial statement’s preparation as per GPFRs is the

information shall be relevant and reliable so that the users can make their valuable decisions.

Relevance – Financial information presented in the financial statement of the

company shall be presented in such manner that the information will be relevant to the

users while making any decisions. From the financial report of Boral Limited for the

year closed on 30th June 2018 it is noticed that financial data are presented and

segregated in proper manner so that the users find it relevant (Zhang and Andrew

2014). Further, the information is presented within the time frame to which it relates.

It enables the users to make comparative assessment with the previous period’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND ISSUES

performance. Further, the reports of the company are published annually as well as

semi-annually.

Reliability - Financial information presented in the financial statement of the

company shall be reliable to the users while making any decisions otherwise they will

end up with wrong decisions. The information presented by Boral Limited in their

annual report are seems to be reliable as the amount for each item can be verified

through the notes disclosed with the financial statements (Simnett and Huggins 2015).

Further, as per the CEO and CFO of the company the financial records are maintained

properly and are complied with proper accounting standards and provides true and fair

view of the entity’s financial performance and position.

Materiality – information are material if the omission or misstatement have impact on

the user’s decision making process. It is recognised from the finnacial report of the

company for the year ended 30th June 2018 that material items are properly disclosed

under the notes to financial statements (Cheng et al. 2014). Further, as per the review

of auditors no material misstatement were found in the financial statements presented

by the company.

5.2 Secondary

Secondary requirement of financial statement’s preparation as per GPFRs is the

information shall be comparable and consistent so that the users can make their valuable

decisions.

performance. Further, the reports of the company are published annually as well as

semi-annually.

Reliability - Financial information presented in the financial statement of the

company shall be reliable to the users while making any decisions otherwise they will

end up with wrong decisions. The information presented by Boral Limited in their

annual report are seems to be reliable as the amount for each item can be verified

through the notes disclosed with the financial statements (Simnett and Huggins 2015).

Further, as per the CEO and CFO of the company the financial records are maintained

properly and are complied with proper accounting standards and provides true and fair

view of the entity’s financial performance and position.

Materiality – information are material if the omission or misstatement have impact on

the user’s decision making process. It is recognised from the finnacial report of the

company for the year ended 30th June 2018 that material items are properly disclosed

under the notes to financial statements (Cheng et al. 2014). Further, as per the review

of auditors no material misstatement were found in the financial statements presented

by the company.

5.2 Secondary

Secondary requirement of financial statement’s preparation as per GPFRs is the

information shall be comparable and consistent so that the users can make their valuable

decisions.

8ACCOUNTING THEORY AND ISSUES

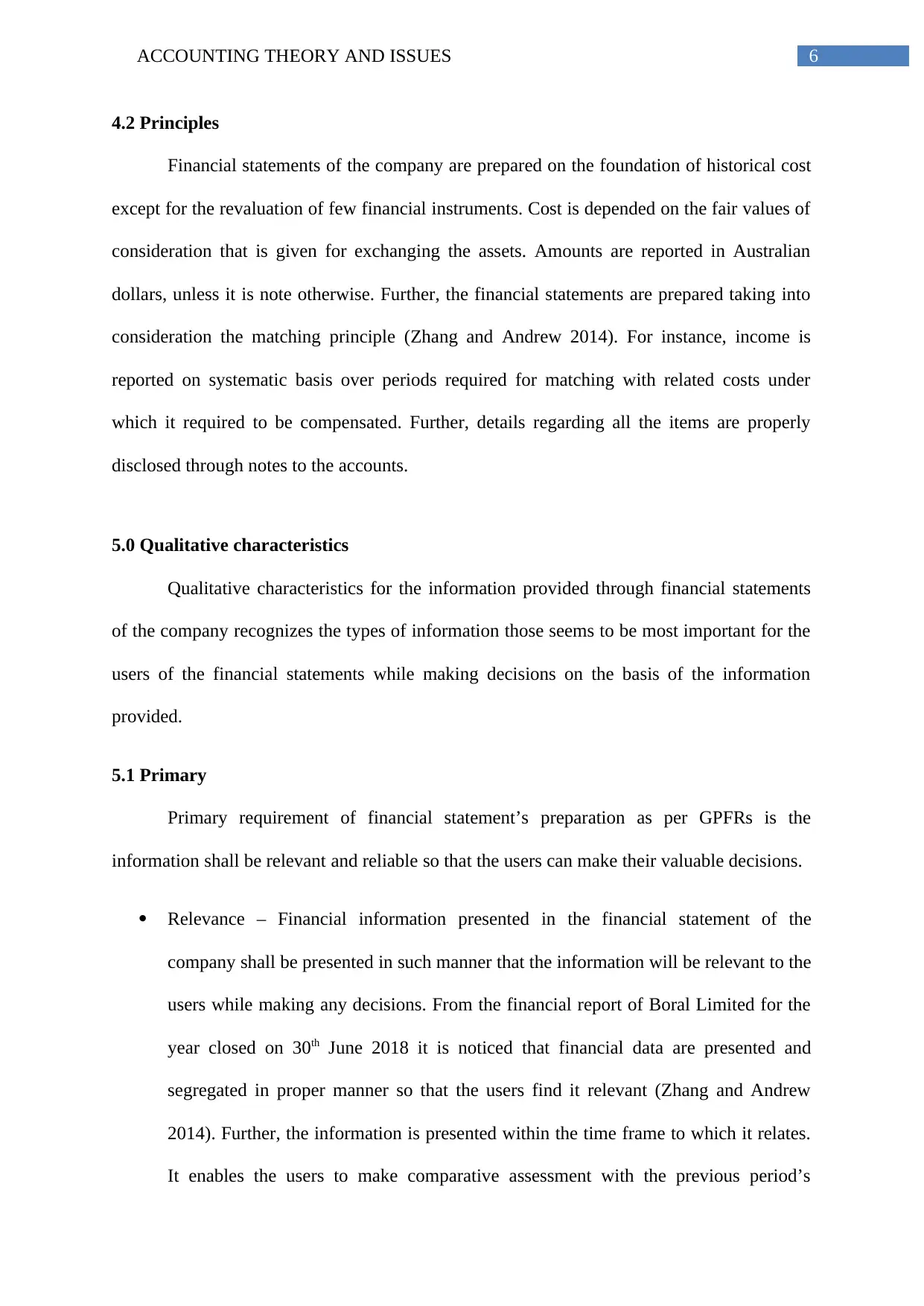

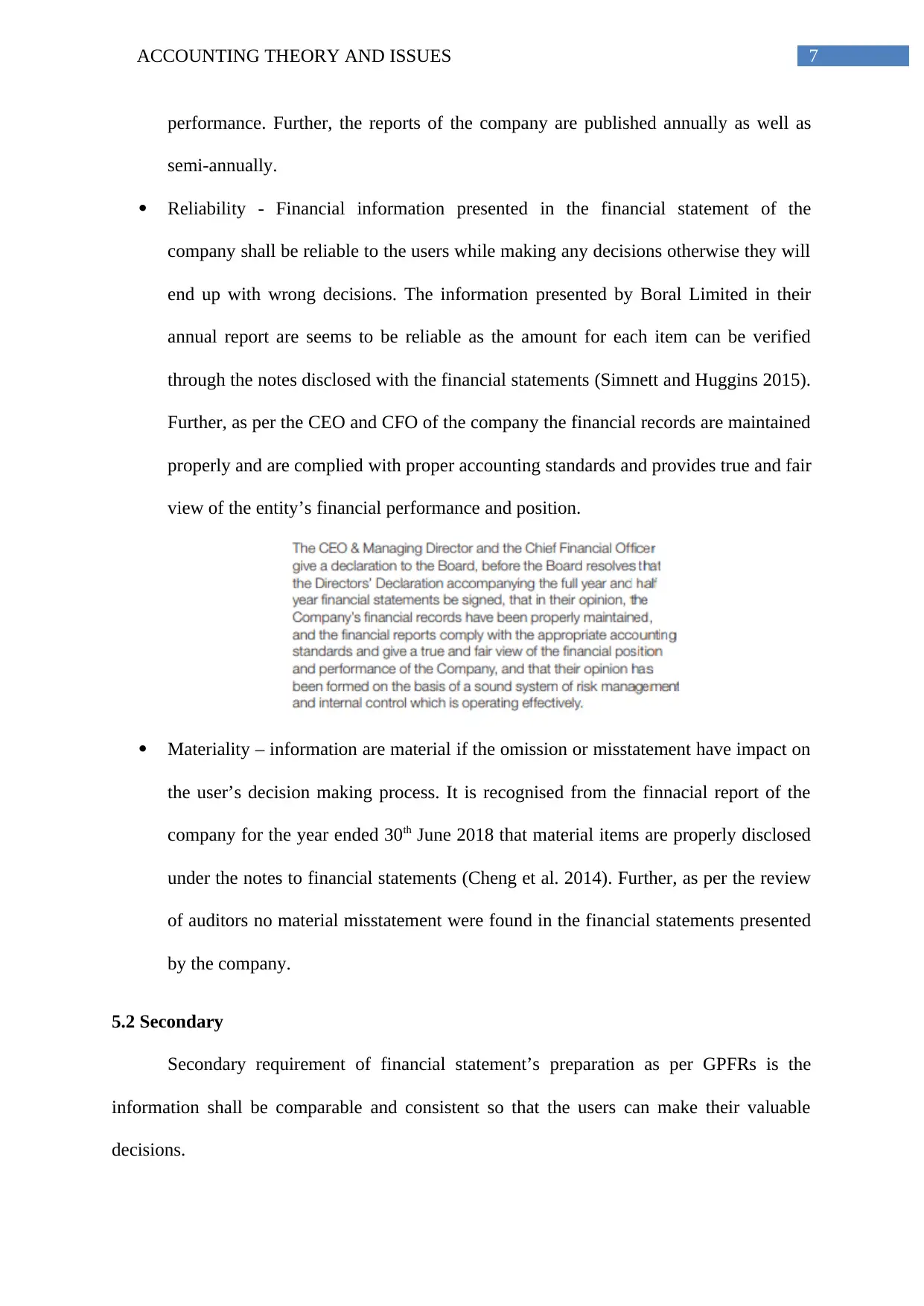

Comparability – It the qualitative character that enables the users of financial

statement to identify and understand the differences and similarities among the items

provided in financial statements (Boral.com.au 2018). It is recognised from the annual

report of the entity for the year closed on 30th June 2018 that the company presented

the data through tables and graphs that will enable the users to make proper

comparisons.

Consistency – As per the requirement of GPFRs the accounting approach and

accounting standards used by the company shall be used consistently to provide the

information more transparently (Cajaiba-Santana 2014). It is recognised from the

financial report of the entity for the year ended 30th June 2018 that the accounting

standards and recognition approaches used by the company are used on consistent

basis.

Comparability – It the qualitative character that enables the users of financial

statement to identify and understand the differences and similarities among the items

provided in financial statements (Boral.com.au 2018). It is recognised from the annual

report of the entity for the year closed on 30th June 2018 that the company presented

the data through tables and graphs that will enable the users to make proper

comparisons.

Consistency – As per the requirement of GPFRs the accounting approach and

accounting standards used by the company shall be used consistently to provide the

information more transparently (Cajaiba-Santana 2014). It is recognised from the

financial report of the entity for the year ended 30th June 2018 that the accounting

standards and recognition approaches used by the company are used on consistent

basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND ISSUES

6.0 Conclusion

From above discussion it is found that Boral Limited is complying with all the

requirement of the objectives under GPFRs. Users of the financial reports of the company can

use the information reliably to make proper decisions. Further, all the recognition criteria for

liabilities, assets, equities, revenues and expenses are met and followed consistently by the

company.

6.0 Conclusion

From above discussion it is found that Boral Limited is complying with all the

requirement of the objectives under GPFRs. Users of the financial reports of the company can

use the information reliably to make proper decisions. Further, all the recognition criteria for

liabilities, assets, equities, revenues and expenses are met and followed consistently by the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND ISSUES

Reference

A Review of the IASB’s Conceptual Framework for Financial Reporting., 2018. [ebook]

Australian Accounting Standard Board. Available at:

http://www.aasb.gov.au/admin/file/content105/c9/ITC29_07-13.pdf [Accessed 12 December.

2018].

Boral.com.au. 2018. Boral Australia: Build something great™. [online] Available at:

https://www.boral.com.au/ [Accessed 6 Dec. 2018].

Cajaiba-Santana, G., 2014. Social innovation: Moving the field forward. A conceptual

framework. Technological Forecasting and Social Change, 82, pp.42-51.

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and

an agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

pp.1042-1067.

Garrett, J., Hoitash, R. and Prawitt, D.F., 2014. Trust and financial reporting quality. Journal

of Accounting Research, 52(5), pp.1087-1125.

Kogan, A., Sudit, E.F. and Vasarhelyi, M.A., 2018. Continuous online auditing: A program

of research. In Continuous Auditing: Theory and Application (pp. 125-148). Emerald

Publishing Limited.

Reference

A Review of the IASB’s Conceptual Framework for Financial Reporting., 2018. [ebook]

Australian Accounting Standard Board. Available at:

http://www.aasb.gov.au/admin/file/content105/c9/ITC29_07-13.pdf [Accessed 12 December.

2018].

Boral.com.au. 2018. Boral Australia: Build something great™. [online] Available at:

https://www.boral.com.au/ [Accessed 6 Dec. 2018].

Cajaiba-Santana, G., 2014. Social innovation: Moving the field forward. A conceptual

framework. Technological Forecasting and Social Change, 82, pp.42-51.

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and

an agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

pp.1042-1067.

Garrett, J., Hoitash, R. and Prawitt, D.F., 2014. Trust and financial reporting quality. Journal

of Accounting Research, 52(5), pp.1087-1125.

Kogan, A., Sudit, E.F. and Vasarhelyi, M.A., 2018. Continuous online auditing: A program

of research. In Continuous Auditing: Theory and Application (pp. 125-148). Emerald

Publishing Limited.

11ACCOUNTING THEORY AND ISSUES

Morioka, S.N. and De Carvalho, M.M., 2016. A systematic literature review towards a

conceptual framework for integrating sustainability performance into business. Journal of

Cleaner Production, 136, pp.134-146.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

Morioka, S.N. and De Carvalho, M.M., 2016. A systematic literature review towards a

conceptual framework for integrating sustainability performance into business. Journal of

Cleaner Production, 136, pp.134-146.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.