Accounting Theory and Current Issues: Tutorial Questions Analysis

VerifiedAdded on 2023/01/11

|10

|1839

|81

Homework Assignment

AI Summary

This document presents a comprehensive solution to tutorial questions from an Accounting Theory and Practice course (HI6025), covering key concepts in financial reporting. The solution explores the qualitative characteristics of financial information, specifically relevance and faithful representation, providing examples of each. It addresses depreciation calculations, including asset revaluation and profit/loss on sale, and provides journal entries. Furthermore, the document examines goodwill impairment, determining the impairment loss and related journal entries. Lease accounting is also covered, demonstrating the present value calculation of lease payments and journal entries for both the lessee and lessor. The assignment also discusses the social contract and organisational legitimacy in relation to corporate disclosure.

ACCOUNTING THEORY AND

PRACTICE

PRACTICE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

WEEK 1...........................................................................................................................................1

a) Example where the information is relevant but is not faithfully presented.............................1

b) Example where the information is not relevant but faithfully represented.............................2

c) Example where information is relevant and faithfully presented............................................2

WEEK 2...........................................................................................................................................2

a) Social Contract and its relation with organisational legitimacy..............................................2

b) Corporate disclosure policy for maintaining legitimacy.........................................................3

WEEK 3...........................................................................................................................................3

Required :.....................................................................................................................................3

WEEK..............................................................................................................................................5

Required:......................................................................................................................................5

WEEK 5...........................................................................................................................................5

Required:......................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

WEEK 1...........................................................................................................................................1

a) Example where the information is relevant but is not faithfully presented.............................1

b) Example where the information is not relevant but faithfully represented.............................2

c) Example where information is relevant and faithfully presented............................................2

WEEK 2...........................................................................................................................................2

a) Social Contract and its relation with organisational legitimacy..............................................2

b) Corporate disclosure policy for maintaining legitimacy.........................................................3

WEEK 3...........................................................................................................................................3

Required :.....................................................................................................................................3

WEEK..............................................................................................................................................5

Required:......................................................................................................................................5

WEEK 5...........................................................................................................................................5

Required:......................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUTION

Accounting refers to the process of recording the financial transactions related with the

business. Accounting process includes the process of recording journals, posting to ledger and

the preparation to financial statements. They are the brief summary of the accounting events and

transactions that are carried out during the year. The financial statements are to be prepared by

the organisation for giving information to the public. Therefore this requires the financial

statements to give true and fair representation of the financial position of the company. financial

statement are to be prepared in compliance with the reporting frameworks given by the

accounting authorities. The report is based on the qualitative characteristics of the financial

information. It will include the concepts of relevance and faithful representation of the financial

information provided by the statements. All the information are not relevant for the business

decision making. Study will also provide the solution about the depreciation, lease payments and

the impairment of goodwill. It will enhance the understanding about the accounting concepts.

WEEK 1

Faithful representation is fundamental qualitative characteristics of the financial

framework. Faithful representation and are relevance are categorized as qualitative

characteristics of the financial reporting framework. Enhancing the qualitative characteristic of

the financial reporting data and information will involve comparability, understandability,

timeliness and verifiability. This is focused over having relevant and reliable information

provided by the financial statements of the company (Kokina, Mancha and Pachamanova,

2017). Financial statements are essential for decision making of various users therefore it is

essential that it is free from any errors and material misstatements in the company. It should

represent actual and accurate position and performance of the business.

a) Example where the information is relevant but is not faithfully presented.

Fundamental quality in conceptual framework of the Financial Reporting is the faithful

representation. In simple terms the financial information represented by the company should

accurately reflect the position of company’s financial statement. For example company having

the debt of 800000 is relevant and presented in the business but is not faithfully presented as the

additional information regarding the debt is not provided in the notes of financial statements.

1

Accounting refers to the process of recording the financial transactions related with the

business. Accounting process includes the process of recording journals, posting to ledger and

the preparation to financial statements. They are the brief summary of the accounting events and

transactions that are carried out during the year. The financial statements are to be prepared by

the organisation for giving information to the public. Therefore this requires the financial

statements to give true and fair representation of the financial position of the company. financial

statement are to be prepared in compliance with the reporting frameworks given by the

accounting authorities. The report is based on the qualitative characteristics of the financial

information. It will include the concepts of relevance and faithful representation of the financial

information provided by the statements. All the information are not relevant for the business

decision making. Study will also provide the solution about the depreciation, lease payments and

the impairment of goodwill. It will enhance the understanding about the accounting concepts.

WEEK 1

Faithful representation is fundamental qualitative characteristics of the financial

framework. Faithful representation and are relevance are categorized as qualitative

characteristics of the financial reporting framework. Enhancing the qualitative characteristic of

the financial reporting data and information will involve comparability, understandability,

timeliness and verifiability. This is focused over having relevant and reliable information

provided by the financial statements of the company (Kokina, Mancha and Pachamanova,

2017). Financial statements are essential for decision making of various users therefore it is

essential that it is free from any errors and material misstatements in the company. It should

represent actual and accurate position and performance of the business.

a) Example where the information is relevant but is not faithfully presented.

Fundamental quality in conceptual framework of the Financial Reporting is the faithful

representation. In simple terms the financial information represented by the company should

accurately reflect the position of company’s financial statement. For example company having

the debt of 800000 is relevant and presented in the business but is not faithfully presented as the

additional information regarding the debt is not provided in the notes of financial statements.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Example where the information is not relevant but faithfully represented.

There are cases where the information is not relevant for the investors but is presented

faithfully by the company in the financial statements. Information is relevant that could influence

the decisions of the investors or user of the financial statements (Hoque, 2018). Relevance of the

information also depends over the materiality of the transaction or event. For example the

contingent liability that may arise in the year of 10000 is not relevant for the users of big

companies but is faithfully represented in the notes of financial statements for which the

provisions is made on balance sheet of company.

c) Example where information is relevant and faithfully presented.

All the information are not relevant but are required to be presented in the financial

statements likewise there are information that is both relevant and faithfully represented in the

financial statements of company. For example the Change in accounting policy is relevant for the

investors and also the effects are faithfully represented in the accounting figures in the financial

statements and also in qualitative terms explaining the effect.

WEEK 2

a) Social Contract and its relation with organisational legitimacy

Social contract refers to the process of how the company will be interacting with the

society. This is related to implicit and explicit expectation of the society about the business and

how it should be acting for having sustainable survival in future. It is not always a written

agreement but the expectations of the society. Relationship between business and society is

explained by social contract, the organisational legitimacy describe states where the organisation

is meeting the social contract. The process explains process through which organisation meets

terms of social contract. It has explained the process through which terms of the social contract

are maintained or gained. Social contract is hypothetical, actual or agreement between rulers and

ruled defining rights and the duties of the each.

Social contract states that the moral and obligations of the people depend on the contract

or agreement they have entered into. In the accounting organisations are required to give true and

fair view of the financial statement representing actual position and condition of company.

Organisational legitimacy is concerned with establishing congruency between social values that

are associated with the norms of behaviours accepted behaviour in the society they are operating

2

There are cases where the information is not relevant for the investors but is presented

faithfully by the company in the financial statements. Information is relevant that could influence

the decisions of the investors or user of the financial statements (Hoque, 2018). Relevance of the

information also depends over the materiality of the transaction or event. For example the

contingent liability that may arise in the year of 10000 is not relevant for the users of big

companies but is faithfully represented in the notes of financial statements for which the

provisions is made on balance sheet of company.

c) Example where information is relevant and faithfully presented.

All the information are not relevant but are required to be presented in the financial

statements likewise there are information that is both relevant and faithfully represented in the

financial statements of company. For example the Change in accounting policy is relevant for the

investors and also the effects are faithfully represented in the accounting figures in the financial

statements and also in qualitative terms explaining the effect.

WEEK 2

a) Social Contract and its relation with organisational legitimacy

Social contract refers to the process of how the company will be interacting with the

society. This is related to implicit and explicit expectation of the society about the business and

how it should be acting for having sustainable survival in future. It is not always a written

agreement but the expectations of the society. Relationship between business and society is

explained by social contract, the organisational legitimacy describe states where the organisation

is meeting the social contract. The process explains process through which organisation meets

terms of social contract. It has explained the process through which terms of the social contract

are maintained or gained. Social contract is hypothetical, actual or agreement between rulers and

ruled defining rights and the duties of the each.

Social contract states that the moral and obligations of the people depend on the contract

or agreement they have entered into. In the accounting organisations are required to give true and

fair view of the financial statement representing actual position and condition of company.

Organisational legitimacy is concerned with establishing congruency between social values that

are associated with the norms of behaviours accepted behaviour in the society they are operating

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

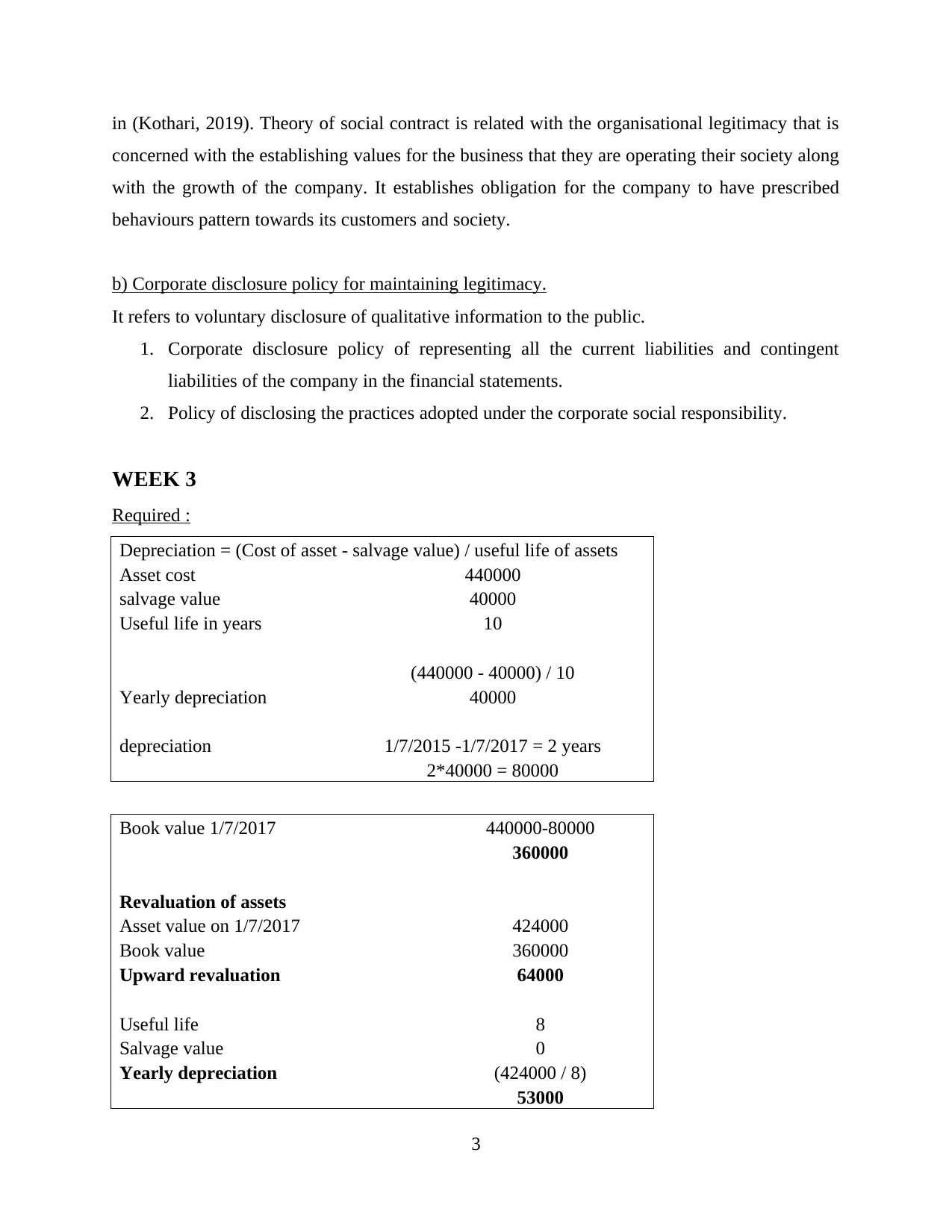

in (Kothari, 2019). Theory of social contract is related with the organisational legitimacy that is

concerned with the establishing values for the business that they are operating their society along

with the growth of the company. It establishes obligation for the company to have prescribed

behaviours pattern towards its customers and society.

b) Corporate disclosure policy for maintaining legitimacy.

It refers to voluntary disclosure of qualitative information to the public.

1. Corporate disclosure policy of representing all the current liabilities and contingent

liabilities of the company in the financial statements.

2. Policy of disclosing the practices adopted under the corporate social responsibility.

WEEK 3

Required :

Depreciation = (Cost of asset - salvage value) / useful life of assets

Asset cost 440000

salvage value 40000

Useful life in years 10

(440000 - 40000) / 10

Yearly depreciation 40000

depreciation 1/7/2015 -1/7/2017 = 2 years

2*40000 = 80000

Book value 1/7/2017 440000-80000

360000

Revaluation of assets

Asset value on 1/7/2017 424000

Book value 360000

Upward revaluation 64000

Useful life 8

Salvage value 0

Yearly depreciation (424000 / 8)

53000

3

concerned with the establishing values for the business that they are operating their society along

with the growth of the company. It establishes obligation for the company to have prescribed

behaviours pattern towards its customers and society.

b) Corporate disclosure policy for maintaining legitimacy.

It refers to voluntary disclosure of qualitative information to the public.

1. Corporate disclosure policy of representing all the current liabilities and contingent

liabilities of the company in the financial statements.

2. Policy of disclosing the practices adopted under the corporate social responsibility.

WEEK 3

Required :

Depreciation = (Cost of asset - salvage value) / useful life of assets

Asset cost 440000

salvage value 40000

Useful life in years 10

(440000 - 40000) / 10

Yearly depreciation 40000

depreciation 1/7/2015 -1/7/2017 = 2 years

2*40000 = 80000

Book value 1/7/2017 440000-80000

360000

Revaluation of assets

Asset value on 1/7/2017 424000

Book value 360000

Upward revaluation 64000

Useful life 8

Salvage value 0

Yearly depreciation (424000 / 8)

53000

3

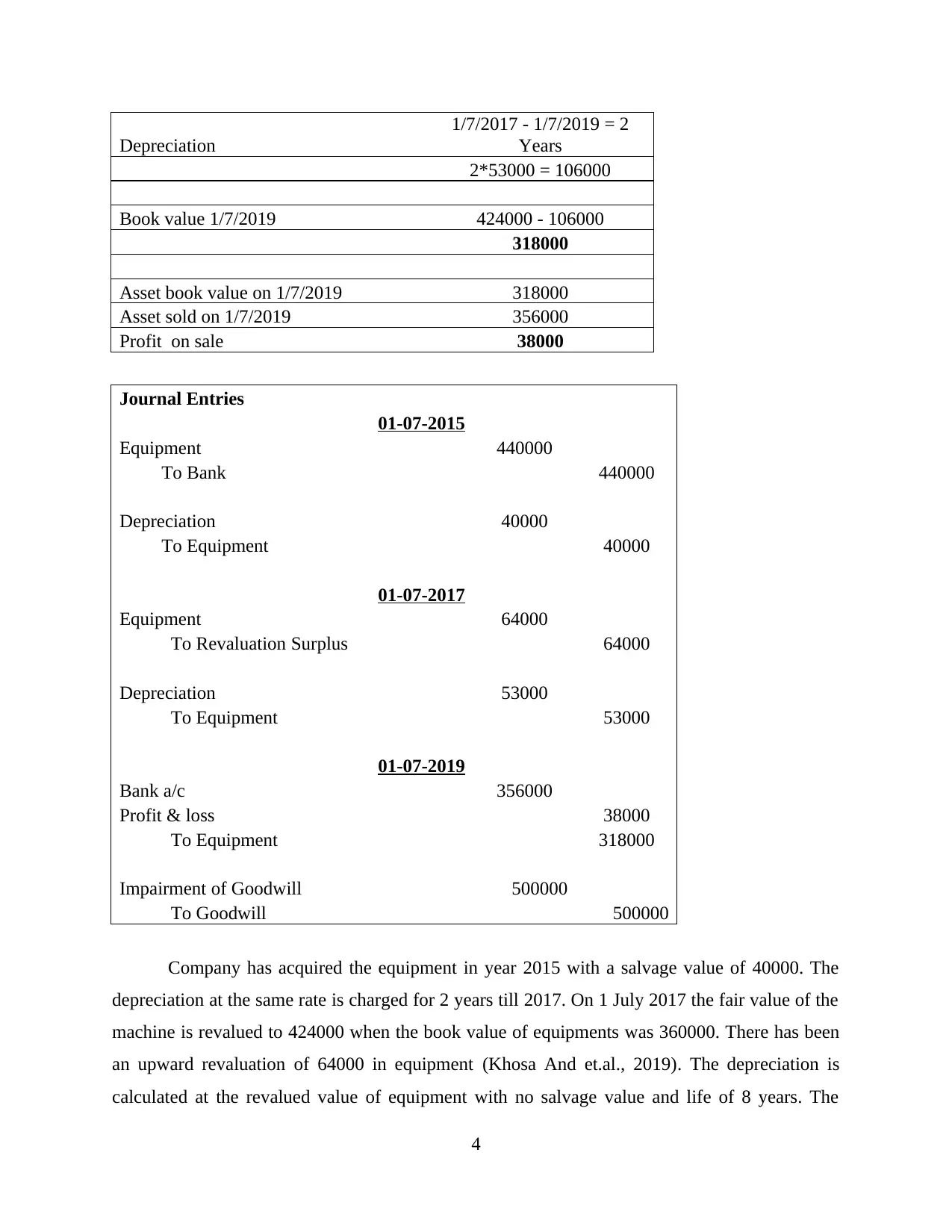

Depreciation

1/7/2017 - 1/7/2019 = 2

Years

2*53000 = 106000

Book value 1/7/2019 424000 - 106000

318000

Asset book value on 1/7/2019 318000

Asset sold on 1/7/2019 356000

Profit on sale 38000

Journal Entries

01-07-2015

Equipment 440000

To Bank 440000

Depreciation 40000

To Equipment 40000

01-07-2017

Equipment 64000

To Revaluation Surplus 64000

Depreciation 53000

To Equipment 53000

01-07-2019

Bank a/c 356000

Profit & loss 38000

To Equipment 318000

Impairment of Goodwill 500000

To Goodwill 500000

Company has acquired the equipment in year 2015 with a salvage value of 40000. The

depreciation at the same rate is charged for 2 years till 2017. On 1 July 2017 the fair value of the

machine is revalued to 424000 when the book value of equipments was 360000. There has been

an upward revaluation of 64000 in equipment (Khosa And et.al., 2019). The depreciation is

calculated at the revalued value of equipment with no salvage value and life of 8 years. The

4

1/7/2017 - 1/7/2019 = 2

Years

2*53000 = 106000

Book value 1/7/2019 424000 - 106000

318000

Asset book value on 1/7/2019 318000

Asset sold on 1/7/2019 356000

Profit on sale 38000

Journal Entries

01-07-2015

Equipment 440000

To Bank 440000

Depreciation 40000

To Equipment 40000

01-07-2017

Equipment 64000

To Revaluation Surplus 64000

Depreciation 53000

To Equipment 53000

01-07-2019

Bank a/c 356000

Profit & loss 38000

To Equipment 318000

Impairment of Goodwill 500000

To Goodwill 500000

Company has acquired the equipment in year 2015 with a salvage value of 40000. The

depreciation at the same rate is charged for 2 years till 2017. On 1 July 2017 the fair value of the

machine is revalued to 424000 when the book value of equipments was 360000. There has been

an upward revaluation of 64000 in equipment (Khosa And et.al., 2019). The depreciation is

calculated at the revalued value of equipment with no salvage value and life of 8 years. The

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

depreciation for 2017 & 2018 is charges at 53000. Equipment is sold for 356000 on July 1, 2019

when the carrying value was 318000. This means the company had earned a profit of 38000 on

the sale of equipments.

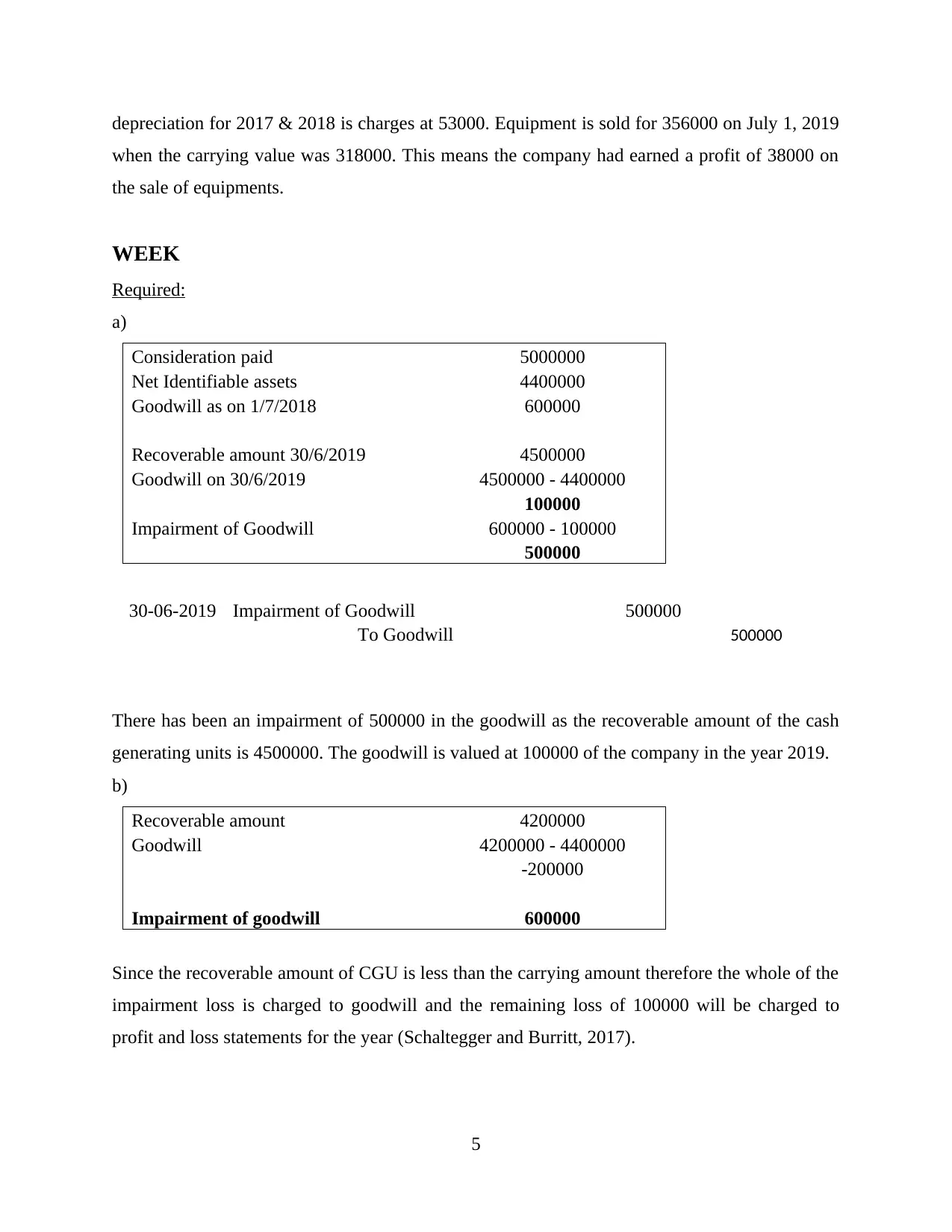

WEEK

Required:

a)

Consideration paid 5000000

Net Identifiable assets 4400000

Goodwill as on 1/7/2018 600000

Recoverable amount 30/6/2019 4500000

Goodwill on 30/6/2019 4500000 - 4400000

100000

Impairment of Goodwill 600000 - 100000

500000

30-06-2019 Impairment of Goodwill 500000

To Goodwill 500000

There has been an impairment of 500000 in the goodwill as the recoverable amount of the cash

generating units is 4500000. The goodwill is valued at 100000 of the company in the year 2019.

b)

Recoverable amount 4200000

Goodwill 4200000 - 4400000

-200000

Impairment of goodwill 600000

Since the recoverable amount of CGU is less than the carrying amount therefore the whole of the

impairment loss is charged to goodwill and the remaining loss of 100000 will be charged to

profit and loss statements for the year (Schaltegger and Burritt, 2017).

5

when the carrying value was 318000. This means the company had earned a profit of 38000 on

the sale of equipments.

WEEK

Required:

a)

Consideration paid 5000000

Net Identifiable assets 4400000

Goodwill as on 1/7/2018 600000

Recoverable amount 30/6/2019 4500000

Goodwill on 30/6/2019 4500000 - 4400000

100000

Impairment of Goodwill 600000 - 100000

500000

30-06-2019 Impairment of Goodwill 500000

To Goodwill 500000

There has been an impairment of 500000 in the goodwill as the recoverable amount of the cash

generating units is 4500000. The goodwill is valued at 100000 of the company in the year 2019.

b)

Recoverable amount 4200000

Goodwill 4200000 - 4400000

-200000

Impairment of goodwill 600000

Since the recoverable amount of CGU is less than the carrying amount therefore the whole of the

impairment loss is charged to goodwill and the remaining loss of 100000 will be charged to

profit and loss statements for the year (Schaltegger and Burritt, 2017).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

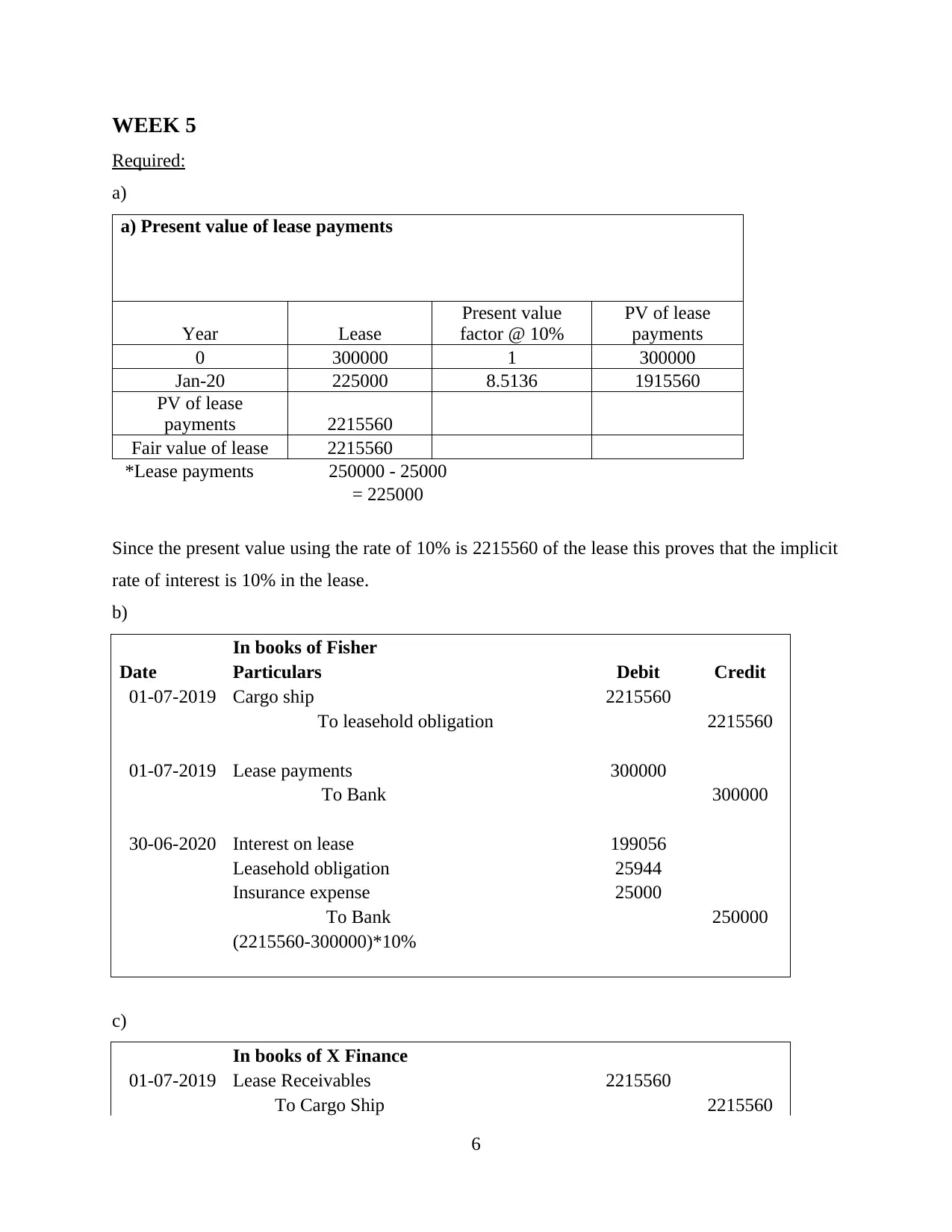

WEEK 5

Required:

a)

a) Present value of lease payments

Year Lease

Present value

factor @ 10%

PV of lease

payments

0 300000 1 300000

Jan-20 225000 8.5136 1915560

PV of lease

payments 2215560

Fair value of lease 2215560

*Lease payments 250000 - 25000

= 225000

Since the present value using the rate of 10% is 2215560 of the lease this proves that the implicit

rate of interest is 10% in the lease.

b)

In books of Fisher

Date Particulars Debit Credit

01-07-2019 Cargo ship 2215560

To leasehold obligation 2215560

01-07-2019 Lease payments 300000

To Bank 300000

30-06-2020 Interest on lease 199056

Leasehold obligation 25944

Insurance expense 25000

To Bank 250000

(2215560-300000)*10%

c)

In books of X Finance

01-07-2019 Lease Receivables 2215560

To Cargo Ship 2215560

6

Required:

a)

a) Present value of lease payments

Year Lease

Present value

factor @ 10%

PV of lease

payments

0 300000 1 300000

Jan-20 225000 8.5136 1915560

PV of lease

payments 2215560

Fair value of lease 2215560

*Lease payments 250000 - 25000

= 225000

Since the present value using the rate of 10% is 2215560 of the lease this proves that the implicit

rate of interest is 10% in the lease.

b)

In books of Fisher

Date Particulars Debit Credit

01-07-2019 Cargo ship 2215560

To leasehold obligation 2215560

01-07-2019 Lease payments 300000

To Bank 300000

30-06-2020 Interest on lease 199056

Leasehold obligation 25944

Insurance expense 25000

To Bank 250000

(2215560-300000)*10%

c)

In books of X Finance

01-07-2019 Lease Receivables 2215560

To Cargo Ship 2215560

6

30-06-2019 Bank 300000

To Lease rental income 300000

30-06-2020 Bank 250000

To Lease Receivables 199056

To Finance income 25944

To Insurance 25000

CONCLUSION

From the above report it could be concluded that the relevance and faithful presentation are

the qualitative characteristics of the financial statements. The accounting standards provides

about the reporting frameworks to be complied with for preparation of the financial statements.

The financial statements of company should give true and fair presentation of the financial

condition that is free from material misstatements.

7

To Lease rental income 300000

30-06-2020 Bank 250000

To Lease Receivables 199056

To Finance income 25944

To Insurance 25000

CONCLUSION

From the above report it could be concluded that the relevance and faithful presentation are

the qualitative characteristics of the financial statements. The accounting standards provides

about the reporting frameworks to be complied with for preparation of the financial statements.

The financial statements of company should give true and fair presentation of the financial

condition that is free from material misstatements.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Khosa, A. And et.al., 2019. Current issues in PhD supervision of accounting and finance

students: Evidence from Australia and New Zealand. The British Accounting

Review.p.100874.

Kothari, S.P., 2019. Accounting Information in Corporate Governance: Implications for Standard

Setting. The Accounting Review.94(2). pp.357-361.

Kokina, J., Mancha, R. and Pachamanova, D., 2017. Blockchain: Emergent industry adoption

and implications for accounting. Journal of Emerging Technologies in

Accounting.14(2).pp.91-100.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

8

Books and Journals

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Khosa, A. And et.al., 2019. Current issues in PhD supervision of accounting and finance

students: Evidence from Australia and New Zealand. The British Accounting

Review.p.100874.

Kothari, S.P., 2019. Accounting Information in Corporate Governance: Implications for Standard

Setting. The Accounting Review.94(2). pp.357-361.

Kokina, J., Mancha, R. and Pachamanova, D., 2017. Blockchain: Emergent industry adoption

and implications for accounting. Journal of Emerging Technologies in

Accounting.14(2).pp.91-100.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.