Accounting Thought: Current Developments, HCA Alternatives & IASB

VerifiedAdded on 2023/06/12

|15

|3514

|246

Essay

AI Summary

This essay provides a comprehensive analysis of current developments in accounting thought, focusing on alternatives to Historical Cost Accounting (HCA) such as Current Purchasing Power Accounting (CPPA), Current Cost Accounting (CCA), and Fair Value Accounting (FVA), along with their underlying assumptions and practical applications. It critically evaluates the viability of these alternatives and discusses the IASB conceptual framework, its objectives, and the primary users of general-purpose financial reporting. The essay also explores the implications of user identification on accounting measurement, considering fair values and historical cost accounting. Furthermore, it outlines the advantages of conceptual framework development, contrasts them with Hines' perspective on who benefits most, and discusses potential disadvantages, providing a thorough understanding of modern accounting practices and their theoretical underpinnings. Desklib offers this document as a valuable resource for students studying accounting.

Running head: CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Current Developments in Accounting Thought

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Current Developments in Accounting Thought

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Table of Contents

Answer to Question 1:.....................................................................................................................2

1.1 Normative theory:..................................................................................................................2

1.2 Historical cost accounting:....................................................................................................2

1.3 Alternatives to historical cost accounting and their assumptions:.........................................2

1.4 Feasibility of the normative alternatives to historical cost accounting:................................4

Answer to Question 2:.....................................................................................................................4

2.1 Conceptual framework of IASB and its objective:................................................................4

2.2 Primary users of general purpose financial reporting:...........................................................5

2.3 Implications to the users for measurement of accounting:....................................................6

Answer to Question 3:.....................................................................................................................8

3.1 Advantages to be derived from the conceptual framework development and pertinent

beneficiaries:................................................................................................................................8

3.2 Disadvantages of the conceptual framework after consideration of the work of Hines:.......9

3.3 Contrast between the view of Hines and the identified benefits of the conceptual

framework:.................................................................................................................................10

References:....................................................................................................................................12

Table of Contents

Answer to Question 1:.....................................................................................................................2

1.1 Normative theory:..................................................................................................................2

1.2 Historical cost accounting:....................................................................................................2

1.3 Alternatives to historical cost accounting and their assumptions:.........................................2

1.4 Feasibility of the normative alternatives to historical cost accounting:................................4

Answer to Question 2:.....................................................................................................................4

2.1 Conceptual framework of IASB and its objective:................................................................4

2.2 Primary users of general purpose financial reporting:...........................................................5

2.3 Implications to the users for measurement of accounting:....................................................6

Answer to Question 3:.....................................................................................................................8

3.1 Advantages to be derived from the conceptual framework development and pertinent

beneficiaries:................................................................................................................................8

3.2 Disadvantages of the conceptual framework after consideration of the work of Hines:.......9

3.3 Contrast between the view of Hines and the identified benefits of the conceptual

framework:.................................................................................................................................10

References:....................................................................................................................................12

2CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Answer to Question 1:

1.1 Normative theory:

In order to gauge income, the importance of normative theory is immense in the current

era. The reason lies behind the use of a formula in order to ascertain income based on value,

while cost is not taken into consideration. Hence, observation is not the sole factor for normative

theory; however, the reliance is on the accounting process to be formulated (Barth, 2015).

1.2 Historical cost accounting:

Historical cost accounting (HCA) is a part of the normative accounting theory, which

gauges the value in which the asset price on the statement of financial position relies on nominal

cost when it is acquired. The main benefit of this measure could be observed in terms of

unbiased estimation and independent verification. Due to this, the investors and other users are

provided with reliable information about the financial information of the organisations (Deegan,

2014). However, its benefit is minimised during recessionary period and as a result, there is

decline in the asset price.

1.3 Alternatives to historical cost accounting and their assumptions:

The alternatives to HCA are numerous, three of which along with their assumptions are

enumerated as follows:

Current Purchasing Power Accounting (CPPA):

Depending on everyday consumer index, this method denotes updating and recording the

accounting-related items. During recession, there would be rise in price and thus, up-to-date

maintenance of accounts is needed in order to adjust monetary items. The assumptions stated in

Answer to Question 1:

1.1 Normative theory:

In order to gauge income, the importance of normative theory is immense in the current

era. The reason lies behind the use of a formula in order to ascertain income based on value,

while cost is not taken into consideration. Hence, observation is not the sole factor for normative

theory; however, the reliance is on the accounting process to be formulated (Barth, 2015).

1.2 Historical cost accounting:

Historical cost accounting (HCA) is a part of the normative accounting theory, which

gauges the value in which the asset price on the statement of financial position relies on nominal

cost when it is acquired. The main benefit of this measure could be observed in terms of

unbiased estimation and independent verification. Due to this, the investors and other users are

provided with reliable information about the financial information of the organisations (Deegan,

2014). However, its benefit is minimised during recessionary period and as a result, there is

decline in the asset price.

1.3 Alternatives to historical cost accounting and their assumptions:

The alternatives to HCA are numerous, three of which along with their assumptions are

enumerated as follows:

Current Purchasing Power Accounting (CPPA):

Depending on everyday consumer index, this method denotes updating and recording the

accounting-related items. During recession, there would be rise in price and thus, up-to-date

maintenance of accounts is needed in order to adjust monetary items. The assumptions stated in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

going concern as well as accrual basis concepts are used in this theory (Ellul et al., 2015). Due to

the supplementary preparation of CPPA statements, there is effective maintenance of the

historical accounts. However, only the differences in general purchasing power are considered in

this method and no attention is paid on the differences in the values of individual items.

For example, XYZ Limited bought machinery on 1st January 2016 at an amount of

$148,000. The economic life of the asset is four years and it follows the straight-line depreciation

method having no residual amount. The general price level indices have been 140 on 1st January

2016 and 150 on 1st January 2017. Thus, the depreciation to be charged would be $37,000

($148,000/4). However, the amount that would be reported in the income statement of the

organisation on 1st January 2017 would be $39,643 ($37,000 x 150/140).

Current cost accounting (CCA):

In this method, the change in individual item price is realised because of the change in

the general level of price. This method considers the method of preparing and evaluating

financial statements in a way that the relevant price change is considered adequately (Henderson

et al., 2015). It is assumed that the replacement cost is used to record fixed assets, while

inventories are shown at market values. The primary benefit of this system is the computation of

profit, as there is no change in historical profit. On the other hand, this method lacks to supply

information that is needed for the investors.

For instance, a ten-year life machinery could be bought for $80,000. It is assumed that the

machinery could be used for additional five years having no residual amount. Due to this, the

replacement cost of the machine would stand at $40,000 ($80,000 minus five-year depreciation

amount).

going concern as well as accrual basis concepts are used in this theory (Ellul et al., 2015). Due to

the supplementary preparation of CPPA statements, there is effective maintenance of the

historical accounts. However, only the differences in general purchasing power are considered in

this method and no attention is paid on the differences in the values of individual items.

For example, XYZ Limited bought machinery on 1st January 2016 at an amount of

$148,000. The economic life of the asset is four years and it follows the straight-line depreciation

method having no residual amount. The general price level indices have been 140 on 1st January

2016 and 150 on 1st January 2017. Thus, the depreciation to be charged would be $37,000

($148,000/4). However, the amount that would be reported in the income statement of the

organisation on 1st January 2017 would be $39,643 ($37,000 x 150/140).

Current cost accounting (CCA):

In this method, the change in individual item price is realised because of the change in

the general level of price. This method considers the method of preparing and evaluating

financial statements in a way that the relevant price change is considered adequately (Henderson

et al., 2015). It is assumed that the replacement cost is used to record fixed assets, while

inventories are shown at market values. The primary benefit of this system is the computation of

profit, as there is no change in historical profit. On the other hand, this method lacks to supply

information that is needed for the investors.

For instance, a ten-year life machinery could be bought for $80,000. It is assumed that the

machinery could be used for additional five years having no residual amount. Due to this, the

replacement cost of the machine would stand at $40,000 ($80,000 minus five-year depreciation

amount).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

Fair Value Accounting (FVA):

This method provides rational and balanced estimation of the potential market asset,

service or product price. In addition, it takes into account the objective factors such as demand

and supply, production, acquisition, cost of distribution, replacement and subjective factors like

cost, capital return, risk characteristics and individually perceived utility. However, there would

be minimisation in the assets’ book values.

1.4 Feasibility of the normative alternatives to historical cost accounting:

The above analysis clearly makes it evident that despite the availability of several

alternatives to HCA, none of the methods are free from errors that could be used for measuring

business performance. For CPPA, the variations are observed in general price level and adequate

stress is not given to the specific price level. Due to this, the financial statements do not depict

the present values related to the organisational resources (Huber, 2017). In case of CCA, it

becomes possible to ascertain tax liabilities and hence, it could not provide detailed evaluation of

the true business costs. On the other hand, the investors often could not identify the use of FVA

from the financial statements of the organisations. Due to this, the satisfaction level of the

investors tends to decline, as the loss of value in net income could lead to loss for the investors.

Therefore, none of the three alternatives are feasible in eliminating the drawbacks inherent in

HCA.

Answer to Question 2:

2.1 Conceptual framework of IASB and its objective:

The primary purpose of the IASB conceptual framework is to formulate the standards of

accounting in order to assure consistency between them, while improving the credibility related

Fair Value Accounting (FVA):

This method provides rational and balanced estimation of the potential market asset,

service or product price. In addition, it takes into account the objective factors such as demand

and supply, production, acquisition, cost of distribution, replacement and subjective factors like

cost, capital return, risk characteristics and individually perceived utility. However, there would

be minimisation in the assets’ book values.

1.4 Feasibility of the normative alternatives to historical cost accounting:

The above analysis clearly makes it evident that despite the availability of several

alternatives to HCA, none of the methods are free from errors that could be used for measuring

business performance. For CPPA, the variations are observed in general price level and adequate

stress is not given to the specific price level. Due to this, the financial statements do not depict

the present values related to the organisational resources (Huber, 2017). In case of CCA, it

becomes possible to ascertain tax liabilities and hence, it could not provide detailed evaluation of

the true business costs. On the other hand, the investors often could not identify the use of FVA

from the financial statements of the organisations. Due to this, the satisfaction level of the

investors tends to decline, as the loss of value in net income could lead to loss for the investors.

Therefore, none of the three alternatives are feasible in eliminating the drawbacks inherent in

HCA.

Answer to Question 2:

2.1 Conceptual framework of IASB and its objective:

The primary purpose of the IASB conceptual framework is to formulate the standards of

accounting in order to assure consistency between them, while improving the credibility related

5CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

to accounting information. The objective of this framework is to supply beneficial financial

information to the potential and current lenders, investors and other users so that resource

decisions could be undertaken (Li, 2015).

2.2 Primary users of general purpose financial reporting:

The primary users of the general purpose financial reporting constitute of the following:

Suppliers and creditors:

The creditors and suppliers would like to seek information that would allow them to

determine that the amounts paid to them are made timely.

Lenders:

The lenders of a business entity might want to accumulate information regarding the loan

payment schedules as they are due. With the help of such information, they could arrive at a

decision whether to provide further loans to the organisation in future (Laux, 2016).

Investors:

With the help of investors, a firm could risk capital in the form of funds. Moreover, these

users are concerned about the inherent risk and return to be expected from the investments made.

Customers:

The customers would like to know about the continuation of the business operations,

especially, if they depend greatly on the goods and services of the organisation.

Employees:

to accounting information. The objective of this framework is to supply beneficial financial

information to the potential and current lenders, investors and other users so that resource

decisions could be undertaken (Li, 2015).

2.2 Primary users of general purpose financial reporting:

The primary users of the general purpose financial reporting constitute of the following:

Suppliers and creditors:

The creditors and suppliers would like to seek information that would allow them to

determine that the amounts paid to them are made timely.

Lenders:

The lenders of a business entity might want to accumulate information regarding the loan

payment schedules as they are due. With the help of such information, they could arrive at a

decision whether to provide further loans to the organisation in future (Laux, 2016).

Investors:

With the help of investors, a firm could risk capital in the form of funds. Moreover, these

users are concerned about the inherent risk and return to be expected from the investments made.

Customers:

The customers would like to know about the continuation of the business operations,

especially, if they depend greatly on the goods and services of the organisation.

Employees:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

The employees would want to know about the level of profit and the stability of the

organisation, in which they work (Luke, 2016). If the position is strong, it would ensure their job

security and thus, such information could be used for making salary hikes and conditions of

employment.

Government:

The government and the agencies associated with it want to gain an insight regarding the

allocation of resources along with the business operations of the corporate firms.

General public:

A corporate entity could directly influence these users in various ways, especially the

method that helps in benefitting the overall community.

2.3 Implications to the users for measurement of accounting:

Direct implications are inherent related to the identification of the particular users on the

creation of future standards of accounting and review of the existing accounting standards for

presenting the financial statements effectively. Fair value as well as historical cost is taken into

account in fair value accounting, since fair value depicts the actual asset values enhancing the

transparency of the financial system (Magnan, Menini & Parbonetti, 2015). Five bases of

measurement are inherent and there are variations in needs of the users, which are elucidated as

follows:

Historical cost:

The value could be gauged with the help of historical cost, in which the asset price on the

statement of financial position relies on nominal cost at the time it is acquired. This measure is

The employees would want to know about the level of profit and the stability of the

organisation, in which they work (Luke, 2016). If the position is strong, it would ensure their job

security and thus, such information could be used for making salary hikes and conditions of

employment.

Government:

The government and the agencies associated with it want to gain an insight regarding the

allocation of resources along with the business operations of the corporate firms.

General public:

A corporate entity could directly influence these users in various ways, especially the

method that helps in benefitting the overall community.

2.3 Implications to the users for measurement of accounting:

Direct implications are inherent related to the identification of the particular users on the

creation of future standards of accounting and review of the existing accounting standards for

presenting the financial statements effectively. Fair value as well as historical cost is taken into

account in fair value accounting, since fair value depicts the actual asset values enhancing the

transparency of the financial system (Magnan, Menini & Parbonetti, 2015). Five bases of

measurement are inherent and there are variations in needs of the users, which are elucidated as

follows:

Historical cost:

The value could be gauged with the help of historical cost, in which the asset price on the

statement of financial position relies on nominal cost at the time it is acquired. This measure is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

useful, since it does not encourage biasness and it could be verified independently. Thus, the

overall reliability of the investors and the other users could be ensured as well. However, trust

issue still lies among the users due to the fact that this method does not consider the impact of

recession on the asset, which might reduce its overall value.

Fair value:

FVA provides balanced and unbiased estimation of the market price related to product,

asset or service. It takes into account the objective factors such as demand and supply,

production, acquisition, cost of distribution, replacement and subjective factors like cost, capital

return, risk characteristics and individually perceived utility. However, there would be

minimisation in the assets’ book values.

Current cost:

With the help of this method, the variation in individual item price could be recognised

because of the general price level variation (Newberry, 2015). In addition, it prepares and

assesses the financial statements in a way that the relevant price change is considered adequately.

Realisable value:

This is the value of the asset that could be realised when the asset is sold less acceptable

estimation of eventual selling cost or disposal of asset (Penman, 2016). In case of realisable

value, it becomes necessary to post the transactions fetching lower profits while minimising the

chance of profit overstatement. This might restrict the investors to find an actual insight of the

financial condition of the business entities.

Value-in-use:

useful, since it does not encourage biasness and it could be verified independently. Thus, the

overall reliability of the investors and the other users could be ensured as well. However, trust

issue still lies among the users due to the fact that this method does not consider the impact of

recession on the asset, which might reduce its overall value.

Fair value:

FVA provides balanced and unbiased estimation of the market price related to product,

asset or service. It takes into account the objective factors such as demand and supply,

production, acquisition, cost of distribution, replacement and subjective factors like cost, capital

return, risk characteristics and individually perceived utility. However, there would be

minimisation in the assets’ book values.

Current cost:

With the help of this method, the variation in individual item price could be recognised

because of the general price level variation (Newberry, 2015). In addition, it prepares and

assesses the financial statements in a way that the relevant price change is considered adequately.

Realisable value:

This is the value of the asset that could be realised when the asset is sold less acceptable

estimation of eventual selling cost or disposal of asset (Penman, 2016). In case of realisable

value, it becomes necessary to post the transactions fetching lower profits while minimising the

chance of profit overstatement. This might restrict the investors to find an actual insight of the

financial condition of the business entities.

Value-in-use:

8CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

The net worth could be termed as the value-in-use related to an asset that is calculated by

projecting the future value pertaining to the disposable amount; in case, there is impairment of

assets. The objective is that assets should not be evaluated at beyond their recoverable values

(Ryan et al., 2014). Hence, this value fails to take into account the price at which the asset is

acquired and thus, it depends on the existing market value. As a result, the investors could

undertake significant decisions.

Answer to Question 3:

3.1 Advantages to be derived from the conceptual framework development and pertinent

beneficiaries:

The conceptual framework for financial reporting helps in dealing with the financial

reporting concerns like the objectives and uses of the financial statements along with the benefits

of accounting information to the users. Moreover, it allows identifying the various elements of

the financial reports, methods of measurement and recognition of these elements in preparing

financial statements (Schaltegger & Zvezdov, 2015). There are various benefits that the

conceptual framework provides to the users, which are enumerated as follows:

The conceptual framework states that the standard-setters could develop a particular

framework in order to prepare financial statements in such a way that the accounting

practices and guidelines depend on common ideology.

With the help of the conceptual framework, the users and developers of the financial

reports could be guided about the unusual transactions (Smith & Smith, 2014).

The net worth could be termed as the value-in-use related to an asset that is calculated by

projecting the future value pertaining to the disposable amount; in case, there is impairment of

assets. The objective is that assets should not be evaluated at beyond their recoverable values

(Ryan et al., 2014). Hence, this value fails to take into account the price at which the asset is

acquired and thus, it depends on the existing market value. As a result, the investors could

undertake significant decisions.

Answer to Question 3:

3.1 Advantages to be derived from the conceptual framework development and pertinent

beneficiaries:

The conceptual framework for financial reporting helps in dealing with the financial

reporting concerns like the objectives and uses of the financial statements along with the benefits

of accounting information to the users. Moreover, it allows identifying the various elements of

the financial reports, methods of measurement and recognition of these elements in preparing

financial statements (Schaltegger & Zvezdov, 2015). There are various benefits that the

conceptual framework provides to the users, which are enumerated as follows:

The conceptual framework states that the standard-setters could develop a particular

framework in order to prepare financial statements in such a way that the accounting

practices and guidelines depend on common ideology.

With the help of the conceptual framework, the users and developers of the financial

reports could be guided about the unusual transactions (Smith & Smith, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

It ensures that random and haphazard decisions are not taken in order to sort out the

accounting issues. Due to this, there is restriction on the users for utilising the

inconsistent accounting approach in similar instances.

If there is no conceptual framework, the firms might be engaged in creative

representation of the financial reports, which might not disclose the true and fair view of

the state of the business affairs.

3.2 Disadvantages of the conceptual framework after consideration of the work of Hines:

According to Hines, the conceptual framework is formed for providing information to the

accounting profession and the accountants are able to achieve adequate level of success in their

profession. The validation of this statement could be made that the conceptual framework has

enabled the accounting professionals in having a body of knowledge about accounting (Hines,

1989). Along with this, it could be observed that the framework enables in providing flexibility

to the preparers and users of accounting information.

Despite these advantages, various disadvantages are present in the conceptual framework

pertaining to financial reporting. The fundamental weakness of this specific framework is the

difficulty in the set-up process. Moreover, plenty of time is needed for the set-up process, while

it is costly as well. As a result, it would not be possible for the developing countries to formulate

the conceptual framework (Taplin, Yuan & Brown, 2014). Moreover, rigidity is observed to be

inherent in this particular reporting framework. Furthermore, some features are present in the

conceptual framework that does not provide considerable accounting guidance. Despite the fact

that this framework is encouraging, it is inflexible too and thus, new ideas could not be

incorporated. Another disadvantage is the conflict between the previous standards and the

conceptual framework. The past standards have very common features with those of the

It ensures that random and haphazard decisions are not taken in order to sort out the

accounting issues. Due to this, there is restriction on the users for utilising the

inconsistent accounting approach in similar instances.

If there is no conceptual framework, the firms might be engaged in creative

representation of the financial reports, which might not disclose the true and fair view of

the state of the business affairs.

3.2 Disadvantages of the conceptual framework after consideration of the work of Hines:

According to Hines, the conceptual framework is formed for providing information to the

accounting profession and the accountants are able to achieve adequate level of success in their

profession. The validation of this statement could be made that the conceptual framework has

enabled the accounting professionals in having a body of knowledge about accounting (Hines,

1989). Along with this, it could be observed that the framework enables in providing flexibility

to the preparers and users of accounting information.

Despite these advantages, various disadvantages are present in the conceptual framework

pertaining to financial reporting. The fundamental weakness of this specific framework is the

difficulty in the set-up process. Moreover, plenty of time is needed for the set-up process, while

it is costly as well. As a result, it would not be possible for the developing countries to formulate

the conceptual framework (Taplin, Yuan & Brown, 2014). Moreover, rigidity is observed to be

inherent in this particular reporting framework. Furthermore, some features are present in the

conceptual framework that does not provide considerable accounting guidance. Despite the fact

that this framework is encouraging, it is inflexible too and thus, new ideas could not be

incorporated. Another disadvantage is the conflict between the previous standards and the

conceptual framework. The past standards have very common features with those of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

conceptual framework (Watts & Zuo, 2016). Thus, it provides benefits to few users; however, all

the parties are not benefitted from the same.

3.3 Contrast between the view of Hines and the identified benefits of the conceptual

framework:

There are certain points of differences between the opinion of Hines and the benefits

provided on the part of the conceptual framework, which are elucidated as follows:

Points of differences Opinion of Hines Arguments in favour of the

conceptual framework

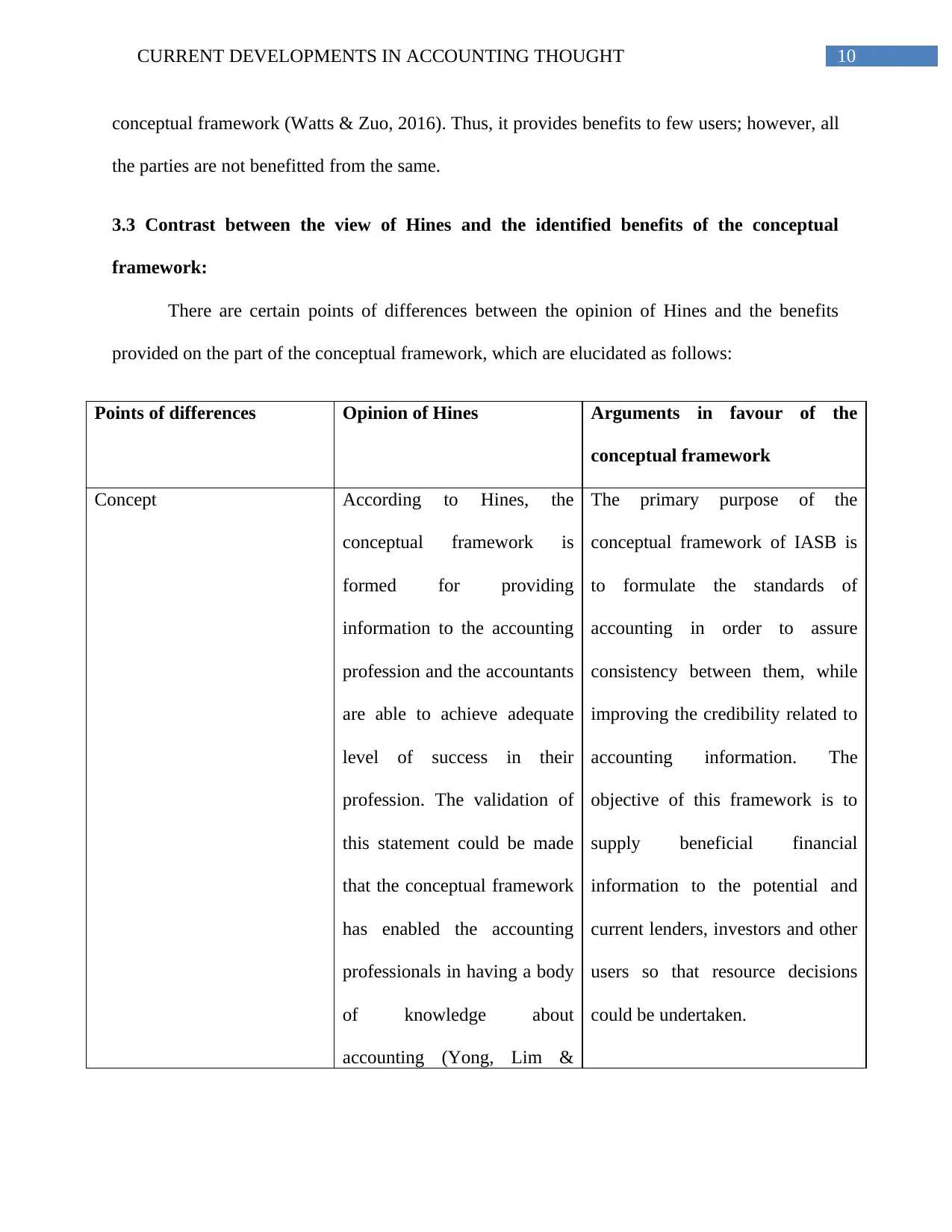

Concept According to Hines, the

conceptual framework is

formed for providing

information to the accounting

profession and the accountants

are able to achieve adequate

level of success in their

profession. The validation of

this statement could be made

that the conceptual framework

has enabled the accounting

professionals in having a body

of knowledge about

accounting (Yong, Lim &

The primary purpose of the

conceptual framework of IASB is

to formulate the standards of

accounting in order to assure

consistency between them, while

improving the credibility related to

accounting information. The

objective of this framework is to

supply beneficial financial

information to the potential and

current lenders, investors and other

users so that resource decisions

could be undertaken.

conceptual framework (Watts & Zuo, 2016). Thus, it provides benefits to few users; however, all

the parties are not benefitted from the same.

3.3 Contrast between the view of Hines and the identified benefits of the conceptual

framework:

There are certain points of differences between the opinion of Hines and the benefits

provided on the part of the conceptual framework, which are elucidated as follows:

Points of differences Opinion of Hines Arguments in favour of the

conceptual framework

Concept According to Hines, the

conceptual framework is

formed for providing

information to the accounting

profession and the accountants

are able to achieve adequate

level of success in their

profession. The validation of

this statement could be made

that the conceptual framework

has enabled the accounting

professionals in having a body

of knowledge about

accounting (Yong, Lim &

The primary purpose of the

conceptual framework of IASB is

to formulate the standards of

accounting in order to assure

consistency between them, while

improving the credibility related to

accounting information. The

objective of this framework is to

supply beneficial financial

information to the potential and

current lenders, investors and other

users so that resource decisions

could be undertaken.

11CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHT

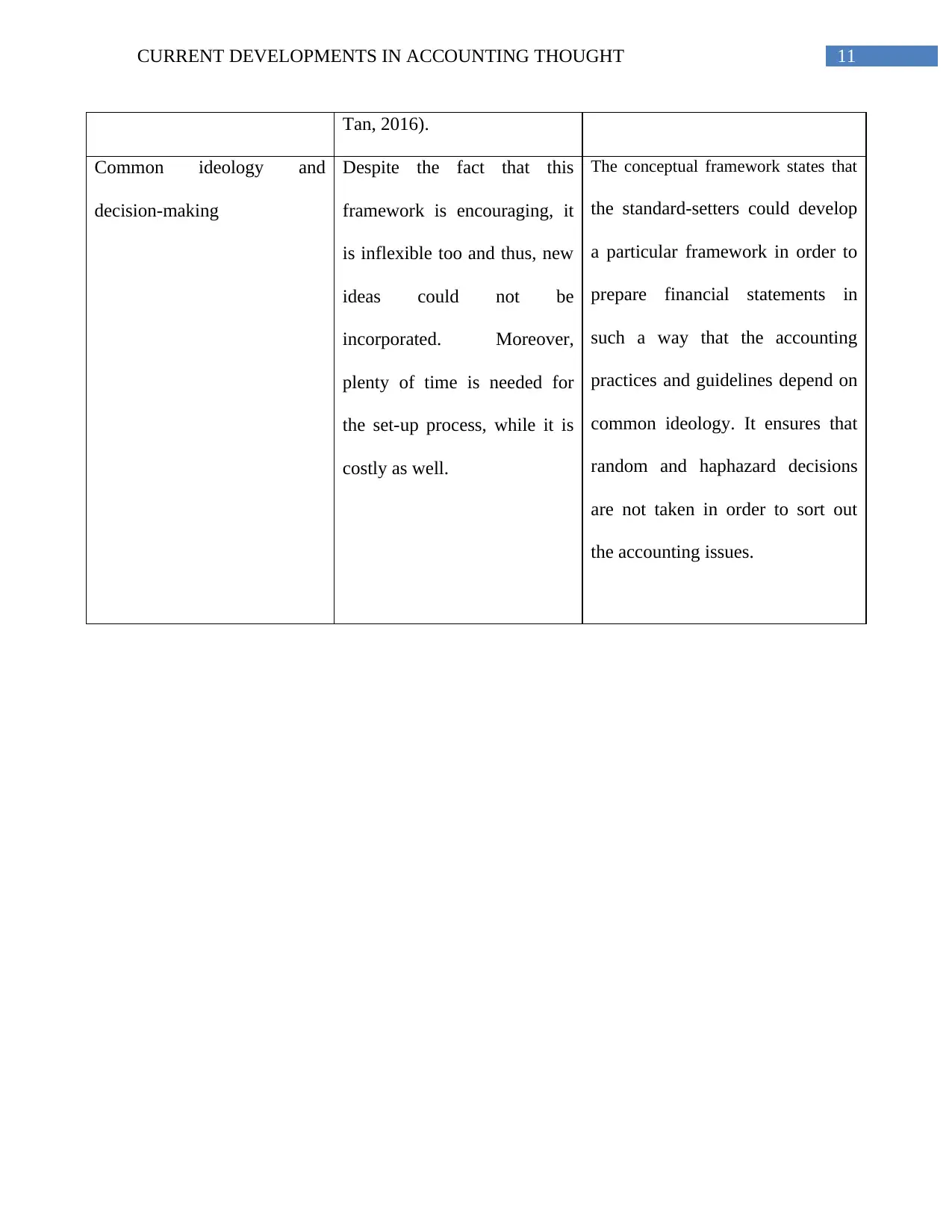

Tan, 2016).

Common ideology and

decision-making

Despite the fact that this

framework is encouraging, it

is inflexible too and thus, new

ideas could not be

incorporated. Moreover,

plenty of time is needed for

the set-up process, while it is

costly as well.

The conceptual framework states that

the standard-setters could develop

a particular framework in order to

prepare financial statements in

such a way that the accounting

practices and guidelines depend on

common ideology. It ensures that

random and haphazard decisions

are not taken in order to sort out

the accounting issues.

Tan, 2016).

Common ideology and

decision-making

Despite the fact that this

framework is encouraging, it

is inflexible too and thus, new

ideas could not be

incorporated. Moreover,

plenty of time is needed for

the set-up process, while it is

costly as well.

The conceptual framework states that

the standard-setters could develop

a particular framework in order to

prepare financial statements in

such a way that the accounting

practices and guidelines depend on

common ideology. It ensures that

random and haphazard decisions

are not taken in order to sort out

the accounting issues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.