Comprehensive Accounting Report: Business Transactions, Assessment 1

VerifiedAdded on 2020/10/22

|11

|2320

|51

Report

AI Summary

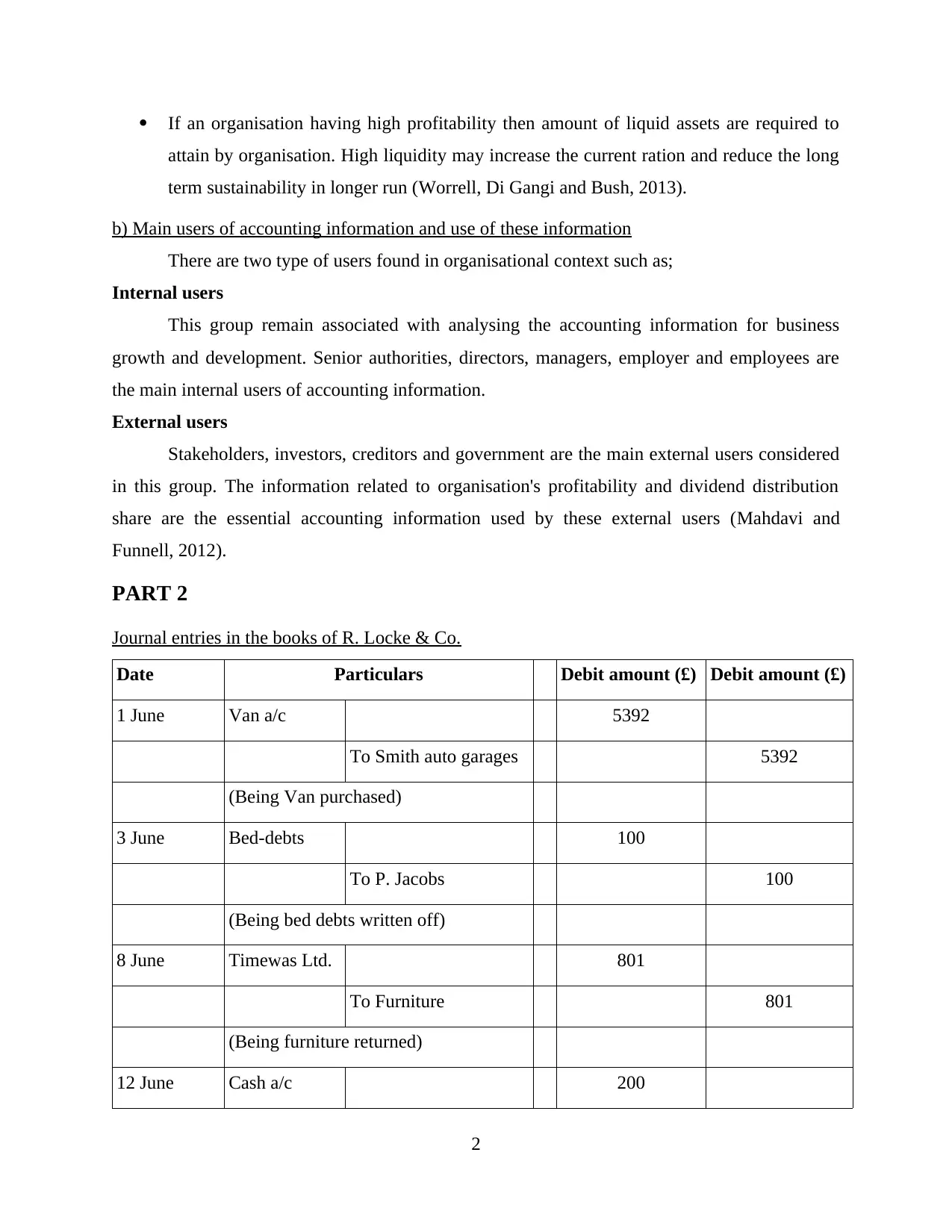

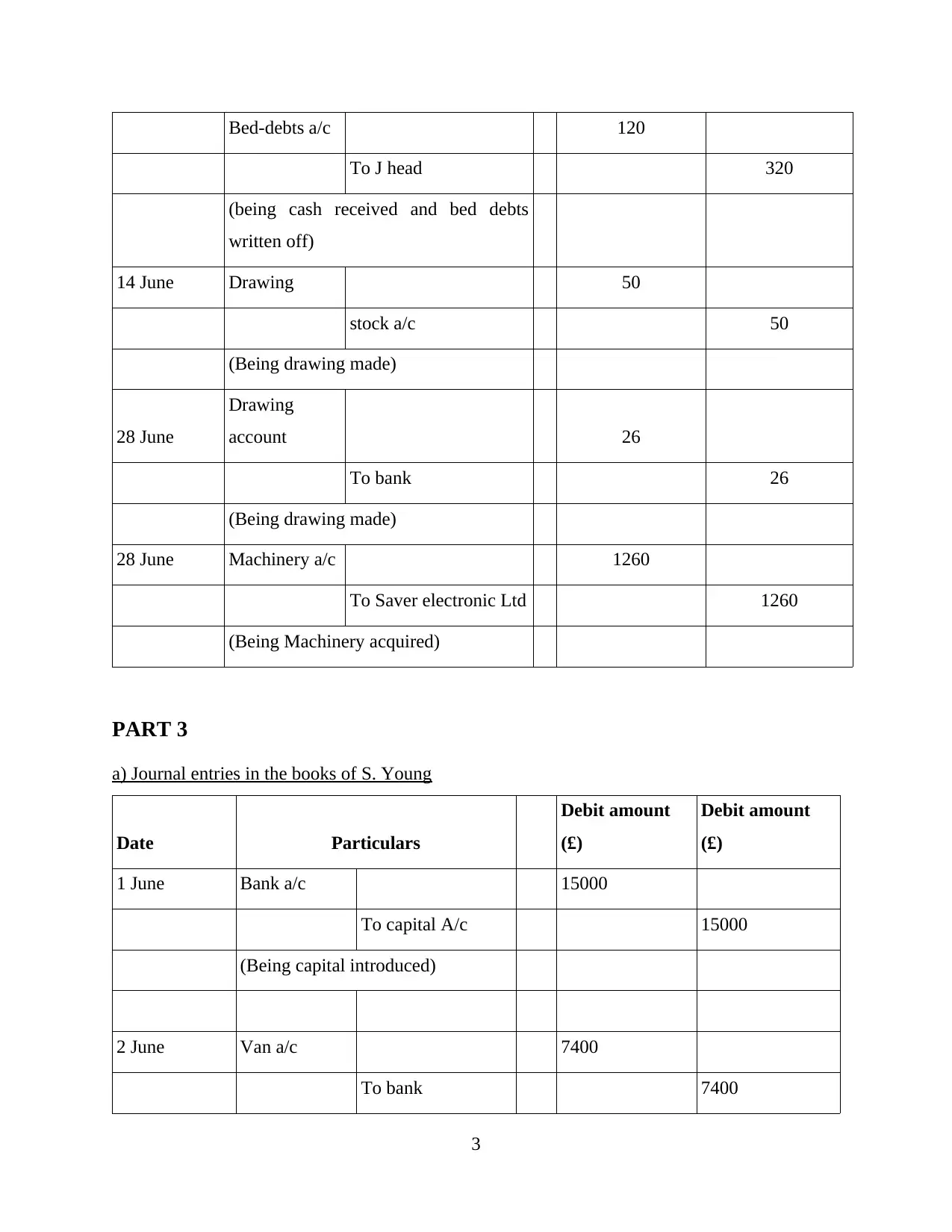

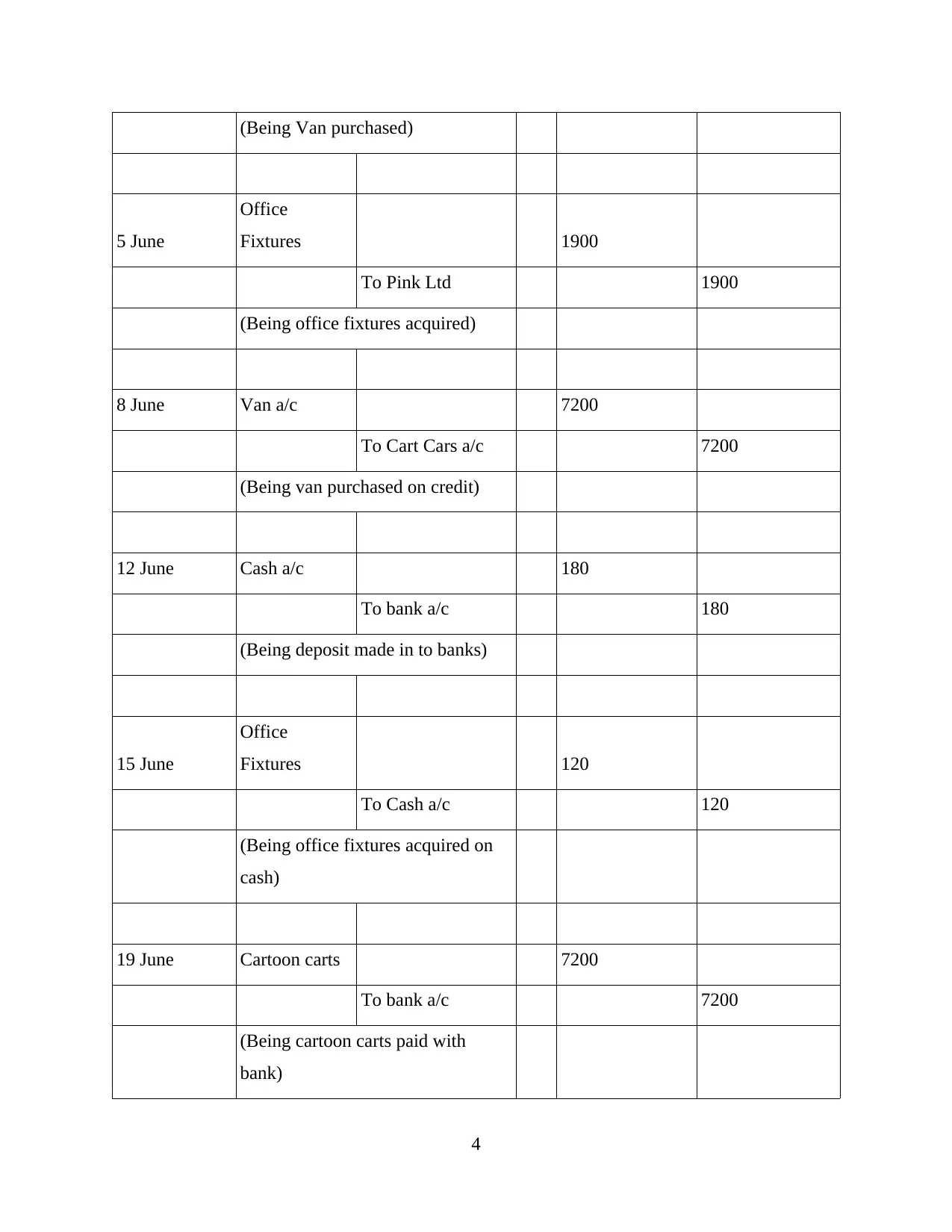

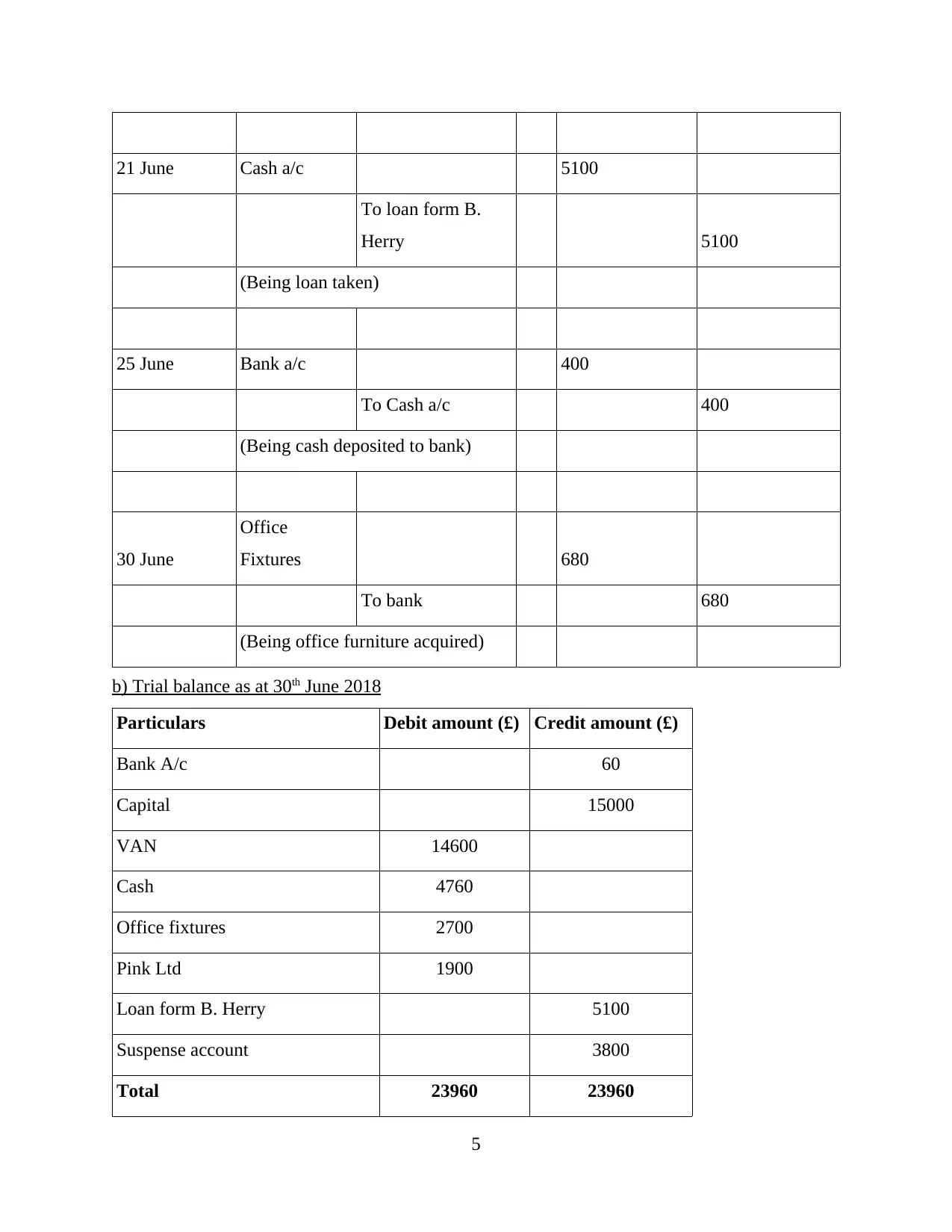

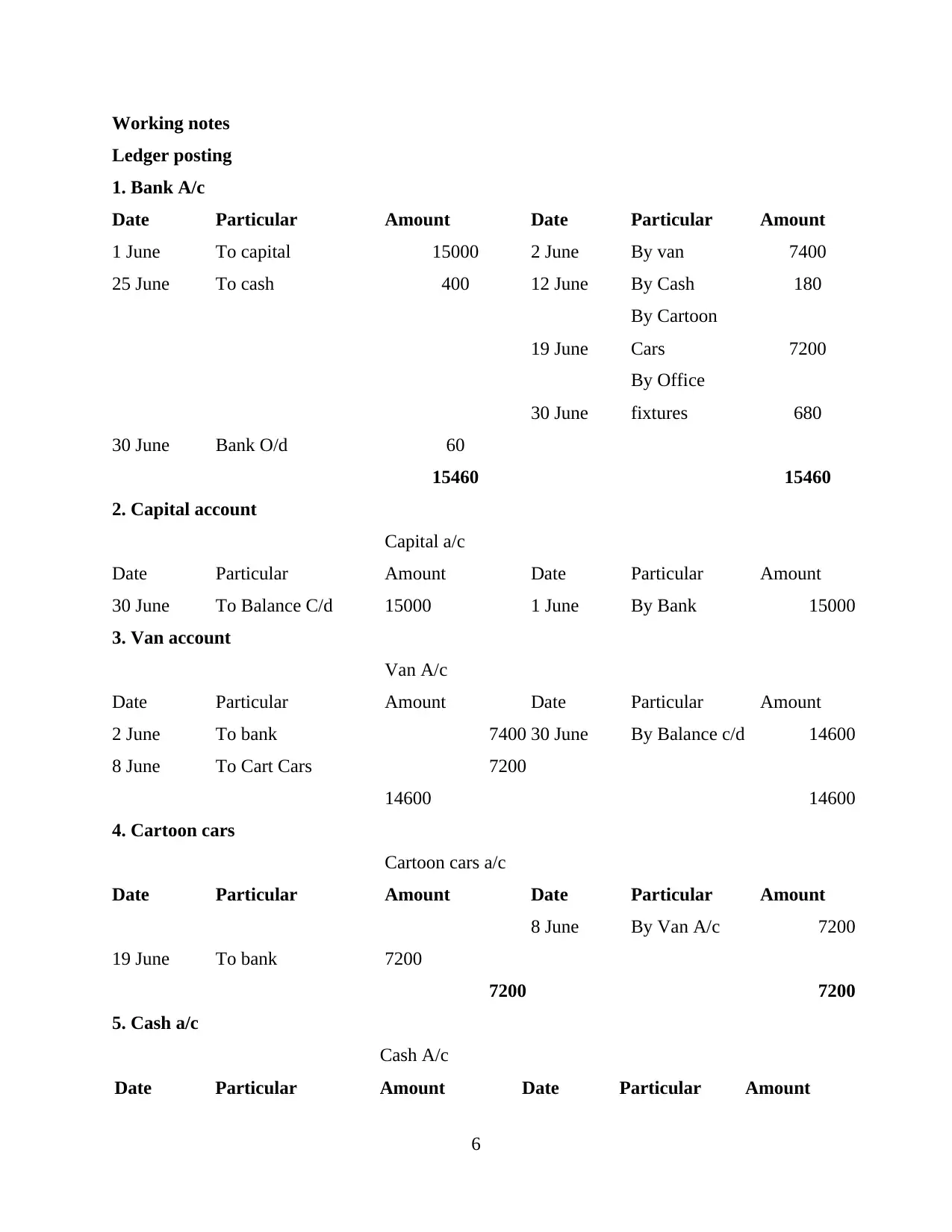

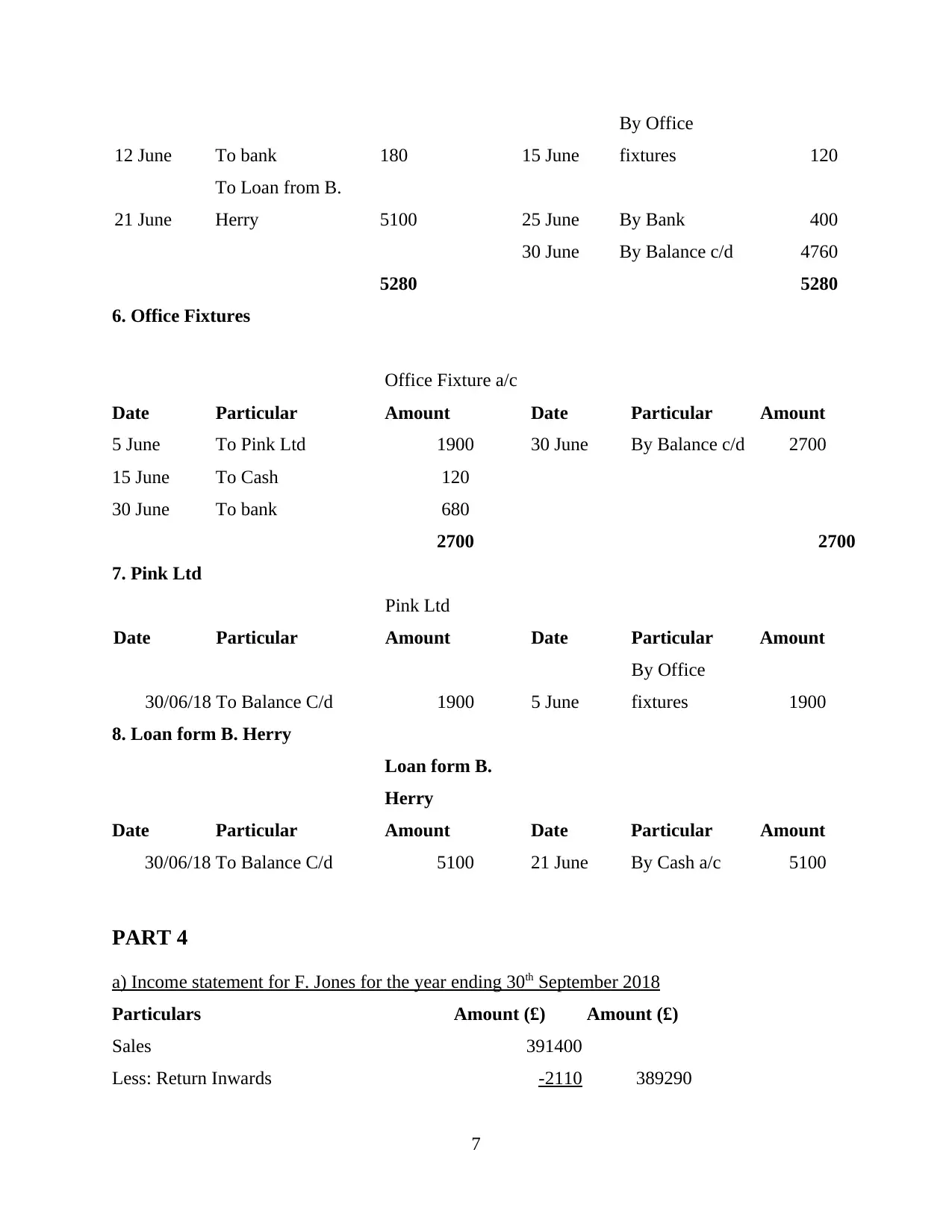

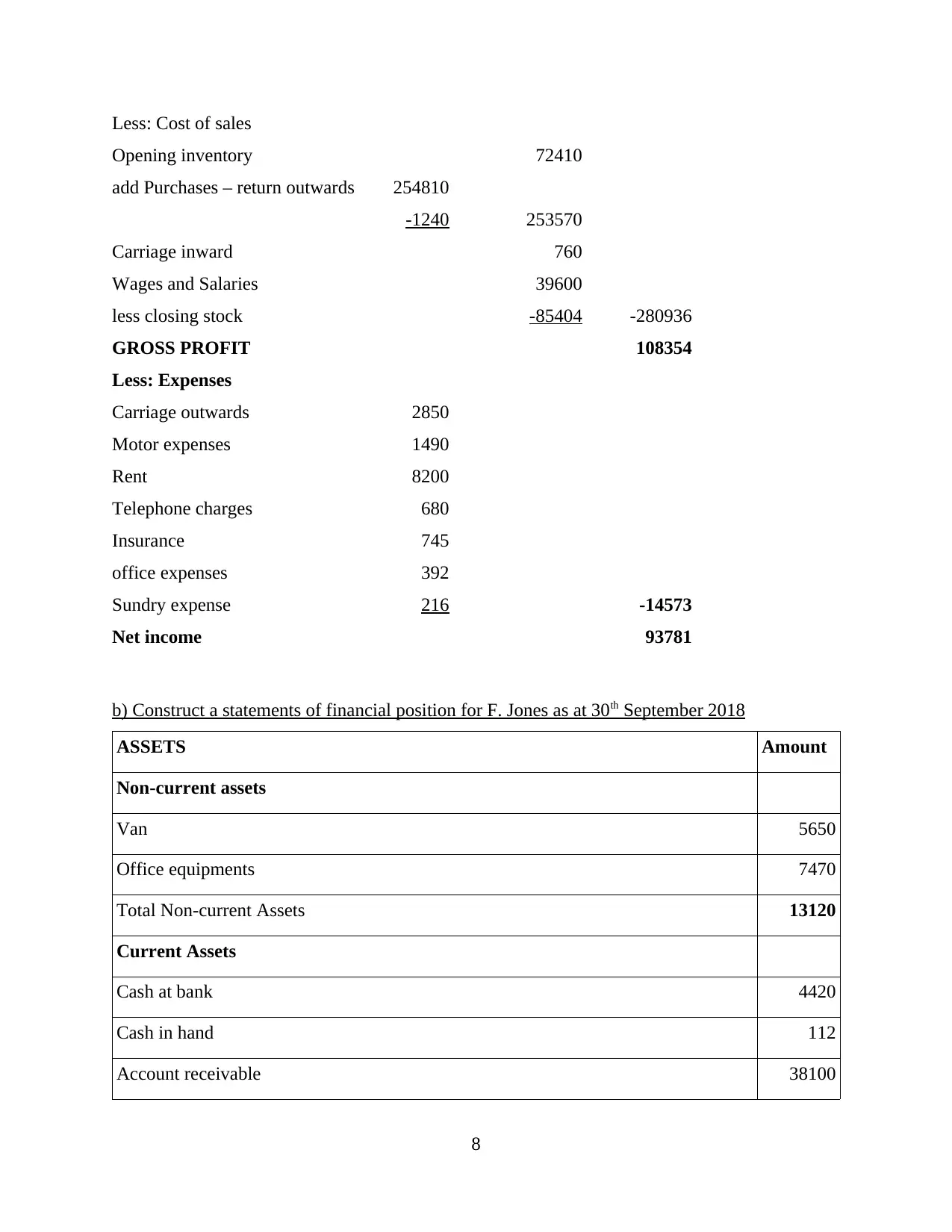

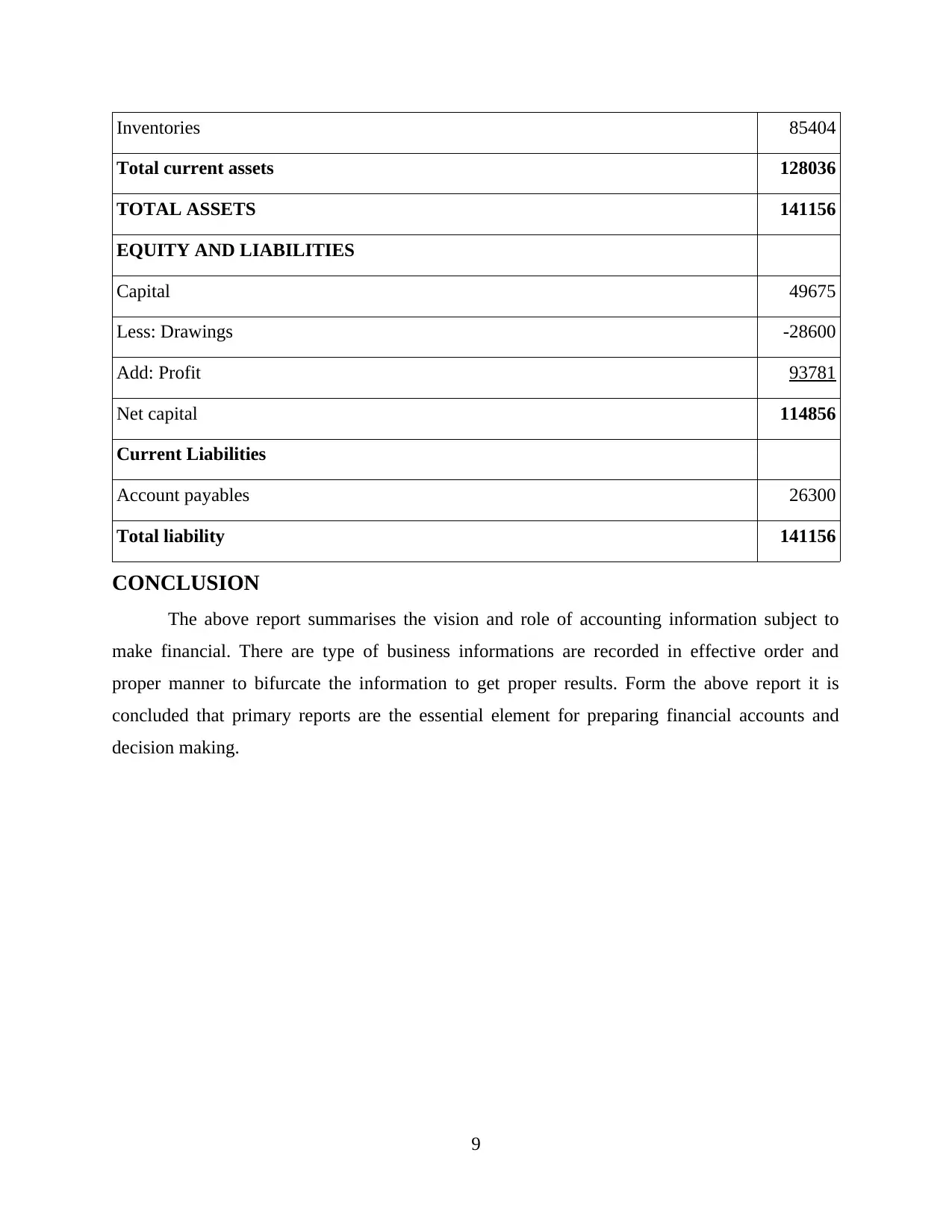

This report provides a comprehensive analysis of accounting for business transactions. It begins with an introduction to the recording of financial transactions and their organization in primary books of accounts. The report then explores the advantages and disadvantages of profit business structures and identifies the main users of accounting information, along with their respective uses. It includes detailed journal entries for R. Locke & Co. and S. Young, along with a trial balance for S. Young. Furthermore, the report constructs an income statement and a statement of financial position for F. Jones, offering a practical application of accounting principles. The conclusion summarizes the importance of accounting information in financial decision-making. The report covers the key elements of financial accounting in a practical way.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.