Business Transactions: Types, Users, and Financial Statements Report

VerifiedAdded on 2023/01/18

|18

|3692

|45

Report

AI Summary

This report provides a comprehensive overview of business transactions and financial reporting. It begins with a discussion of different types of business organizations, including sole proprietorships, partnerships, and corporations, highlighting the advantages of profit-based structures. The report then analyzes the main users of accounting information, categorizing them into internal (owners, management, employees) and external (creditors, investors, government, trading partners) users, and explaining how they utilize this information for decision-making. The report further delves into the uses of journals, ledgers, and financial statements to aid in understanding and interpreting financial data, with the goal of assisting users in making informed decisions about their investments. Overall, the report offers valuable insights into the fundamentals of business transactions and financial analysis.

RECORDING BUSINESS TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1........................................................................................................................................3

b. Main users of accounting information:...................................................................................6

PART 2........................................................................................................................................9

PART 3......................................................................................................................................10

PART 4......................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1........................................................................................................................................3

b. Main users of accounting information:...................................................................................6

PART 2........................................................................................................................................9

PART 3......................................................................................................................................10

PART 4......................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

In this report there has been a brief discussion about the various type of organisations that exists

and these are being discussed thoroughly. I have included all the possible information regarding

the type of organisation. Then there is an evaluation about the users of the accounting

information and what they do with this information. The report provides a comprehensive idea

about these issue. The report helps in understanding the knowledge about the double entry book

keeping, the general ledger, trial balance, income statement and the balance sheet. I have

interpreted these and this interpretation will help the user of financial statements to make there

decision about to invest, hold or sell there investment in the company.(Cochran, 2018) There

have been a draft shown in the report including all these. I have described the uses of journal,

ledger and the financial statements.

In this report there has been a brief discussion about the various type of organisations that exists

and these are being discussed thoroughly. I have included all the possible information regarding

the type of organisation. Then there is an evaluation about the users of the accounting

information and what they do with this information. The report provides a comprehensive idea

about these issue. The report helps in understanding the knowledge about the double entry book

keeping, the general ledger, trial balance, income statement and the balance sheet. I have

interpreted these and this interpretation will help the user of financial statements to make there

decision about to invest, hold or sell there investment in the company.(Cochran, 2018) There

have been a draft shown in the report including all these. I have described the uses of journal,

ledger and the financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MAIN BODY

PART 1

A Briefly discuss the different types of business organisations that exist and highlight

three advantages for organisations utilising profit-based business structures.

There are different types of organisation through which a business can be operated. Each and

every individual cannot follow the same type of business organisation to operate there business,

there are many factors that affects how an individual can operate his business, these factors are

the economies scales, investment etc., There are mainly three types of business organisation

which are Sole proprietor, partnership and corporation. These are being explained below:

SOLE PROPRIETORSHIP

This type of business organisation is operated by a single person, that's why the word sole comes

into picture. In this type of business the owner makes all the decisions for the business and all the

responsibility regarding the decision is on the owner only. (Garrity, 2015) The owner do not

have to ask anyone else for making decisions like which place to operate his business, who

should be employed, what product to sell etc., since all the responsibility and risk is taken by the

owner all the profit generated or the losses incurred will be taken by the owner only. He/ she

does not have to share the profit generated to anyone else as they are not legally bound to do so.

These all were the benefits of operating business through sole proprietorship. The major problem

with sole proprietorship is that if the business incurs any losses then he or she is going to bear it

all by themselves, as they have unlimited liabilities toward there business and they may even

have to sell there personal asset to pay there business debt. Also, if the business is sued it means

that the owner himself is being sued as there is no separation between the business or the owner

so the owner will have to face legal actions if there business is being sued. And if the owner of

the business dies then the business is seized to exist as the owner handle each and every

operation of the company. There may also be a problem in raising finance as banks and financial

institutions are the only way they cannot go to the public to raise finance.

PARTNERSHIP

A partnership business is owned by 2 or more individual. In this type of business the whole

business is being operated by all the partners. (Bansal and Sunkara AppDynamics , 2015.) This

type of business helps in firstly raising finance as there are more than one individual working the

finance is available more easily as compared to the sole proprietorship as each partner brings

PART 1

A Briefly discuss the different types of business organisations that exist and highlight

three advantages for organisations utilising profit-based business structures.

There are different types of organisation through which a business can be operated. Each and

every individual cannot follow the same type of business organisation to operate there business,

there are many factors that affects how an individual can operate his business, these factors are

the economies scales, investment etc., There are mainly three types of business organisation

which are Sole proprietor, partnership and corporation. These are being explained below:

SOLE PROPRIETORSHIP

This type of business organisation is operated by a single person, that's why the word sole comes

into picture. In this type of business the owner makes all the decisions for the business and all the

responsibility regarding the decision is on the owner only. (Garrity, 2015) The owner do not

have to ask anyone else for making decisions like which place to operate his business, who

should be employed, what product to sell etc., since all the responsibility and risk is taken by the

owner all the profit generated or the losses incurred will be taken by the owner only. He/ she

does not have to share the profit generated to anyone else as they are not legally bound to do so.

These all were the benefits of operating business through sole proprietorship. The major problem

with sole proprietorship is that if the business incurs any losses then he or she is going to bear it

all by themselves, as they have unlimited liabilities toward there business and they may even

have to sell there personal asset to pay there business debt. Also, if the business is sued it means

that the owner himself is being sued as there is no separation between the business or the owner

so the owner will have to face legal actions if there business is being sued. And if the owner of

the business dies then the business is seized to exist as the owner handle each and every

operation of the company. There may also be a problem in raising finance as banks and financial

institutions are the only way they cannot go to the public to raise finance.

PARTNERSHIP

A partnership business is owned by 2 or more individual. In this type of business the whole

business is being operated by all the partners. (Bansal and Sunkara AppDynamics , 2015.) This

type of business helps in firstly raising finance as there are more than one individual working the

finance is available more easily as compared to the sole proprietorship as each partner brings

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

there capital into the business. Other advantages of partnership business is that since more than

one individual is working there will be more ideas in the organisation, if losses occurs then it will

be shared by all the partners of the firm. Talking about the demerits of operating as a partnership

business is that though the losses are beard by all the partners each and every partners have again

unlimited liabilities to pay there debts. Also, there is again no separation between the firm and

the partners so if the business is sued all the partners will be sued. The major problem is that

even if there are losses incurred by the mistake of any one partner the consequences will be

beard by all the partners. There may also be conflicts between the partners which can seriously

affect the effective and efficient working of the organisation. If in any partnership the partners

don't want all such types of problem and still wants to operate as a partnership business then they

might form limited liability partnership, in this kind of partnership the partners will have

limited liability and they will be separated from the firm. So the major demerits will be solved.

CORPORATION

This is considered to be the best way of operating any business as a company. Company acts as a

legal entity from its owner which is its biggest advantage. (Sun, 2019) The owners are liable only

up to the capital amount they have invested in the company, so if the debts are not settled then

they do not have to sell there personal assets to pay out for the business. The other major

advantage of operating as a company is that they can easily raise finance as they have the option

of raising finance through public issue. Also, the company don't stop even if the owner dies as

they are legally separated from the business. The owners are not sued if the company is sued as

the company operates as a separate legal person. The problems being faced as operating as a

company is that there are strict regulatory restrictions being imposed on this corporation by the

government and non compliance with these laws and regulations can cause the company large

amount of fines. The cost of operating business as a company is much higher than operating

business as a sole proprietor or partnership. (Harkiolakis, and Halkias, 2016) There are legal cost

to be incurred in forming a company, tax expenses, operational expenses, and other recurring

expenses. There is also a chance of double taxation that can be incurred to the company, as the

company pays corporation taxes on there income and then the shareholders may pay taxes on the

dividends received as they will show the dividends received as there income, so there are

chances of paying taxes 2 times. (Tori, 2018)

one individual is working there will be more ideas in the organisation, if losses occurs then it will

be shared by all the partners of the firm. Talking about the demerits of operating as a partnership

business is that though the losses are beard by all the partners each and every partners have again

unlimited liabilities to pay there debts. Also, there is again no separation between the firm and

the partners so if the business is sued all the partners will be sued. The major problem is that

even if there are losses incurred by the mistake of any one partner the consequences will be

beard by all the partners. There may also be conflicts between the partners which can seriously

affect the effective and efficient working of the organisation. If in any partnership the partners

don't want all such types of problem and still wants to operate as a partnership business then they

might form limited liability partnership, in this kind of partnership the partners will have

limited liability and they will be separated from the firm. So the major demerits will be solved.

CORPORATION

This is considered to be the best way of operating any business as a company. Company acts as a

legal entity from its owner which is its biggest advantage. (Sun, 2019) The owners are liable only

up to the capital amount they have invested in the company, so if the debts are not settled then

they do not have to sell there personal assets to pay out for the business. The other major

advantage of operating as a company is that they can easily raise finance as they have the option

of raising finance through public issue. Also, the company don't stop even if the owner dies as

they are legally separated from the business. The owners are not sued if the company is sued as

the company operates as a separate legal person. The problems being faced as operating as a

company is that there are strict regulatory restrictions being imposed on this corporation by the

government and non compliance with these laws and regulations can cause the company large

amount of fines. The cost of operating business as a company is much higher than operating

business as a sole proprietor or partnership. (Harkiolakis, and Halkias, 2016) There are legal cost

to be incurred in forming a company, tax expenses, operational expenses, and other recurring

expenses. There is also a chance of double taxation that can be incurred to the company, as the

company pays corporation taxes on there income and then the shareholders may pay taxes on the

dividends received as they will show the dividends received as there income, so there are

chances of paying taxes 2 times. (Tori, 2018)

ADVANTAGES FOR ORGANISATION UTILIZING PROFIT-BASED BUSINESS

STRUCTURES

There are many advantages of business operating as profit-based organisation some of these are

discussed below

The most basic and obvious advantage of the profit making organisation is that the

possibility of earning money. The revenue generated over and above the expense are of

the owner use. (Pandian, 2019.) These monetary reward will be based on the success of

the company the more the success, the more the reward will be.

Profit based organisation are their own bosses. (Chow, 2015)The reward or losses are

beard by them only, again these all will be depended upon the type of organisation the

business is operating through. They are being backed up by the strong power of money

generated through the operations.

If any profit making organisation goes into liquidation then they have highly liquid asset

to manage the liquidation.(Chatterjee, 2019) it. A company does not even need to be

performing poorly to be considered liquid. This advantage again depends upon the type

of organisation the business is operating in.

b. Main users of accounting information:

Accounting information refers to the information and the data about the whole

transactions of the business. It is the important methods for the business to analyses, identify and

record the data and information to make the effective reports for different users of the business.

The users of the accounting information are generally classified into two types i.e. internal and

external users of the business. It is the system to collect, store and process the data and

information of the financial and accounting which is used by the makers of the decision in the

company (Reid, 2018). In the business external user like creditors, investors, government,

trading partners etc. internal users of the business such as owners, directors, employees of the

company.

Internal users of the accounting information:

Internal user are those users which runs, maintain and manage the business

operation within the company on the daily basis. Internal users of the accounting information

identify and measures the effectiveness of the decisions of the business operations. These

STRUCTURES

There are many advantages of business operating as profit-based organisation some of these are

discussed below

The most basic and obvious advantage of the profit making organisation is that the

possibility of earning money. The revenue generated over and above the expense are of

the owner use. (Pandian, 2019.) These monetary reward will be based on the success of

the company the more the success, the more the reward will be.

Profit based organisation are their own bosses. (Chow, 2015)The reward or losses are

beard by them only, again these all will be depended upon the type of organisation the

business is operating through. They are being backed up by the strong power of money

generated through the operations.

If any profit making organisation goes into liquidation then they have highly liquid asset

to manage the liquidation.(Chatterjee, 2019) it. A company does not even need to be

performing poorly to be considered liquid. This advantage again depends upon the type

of organisation the business is operating in.

b. Main users of accounting information:

Accounting information refers to the information and the data about the whole

transactions of the business. It is the important methods for the business to analyses, identify and

record the data and information to make the effective reports for different users of the business.

The users of the accounting information are generally classified into two types i.e. internal and

external users of the business. It is the system to collect, store and process the data and

information of the financial and accounting which is used by the makers of the decision in the

company (Reid, 2018). In the business external user like creditors, investors, government,

trading partners etc. internal users of the business such as owners, directors, employees of the

company.

Internal users of the accounting information:

Internal user are those users which runs, maintain and manage the business

operation within the company on the daily basis. Internal users of the accounting information

identify and measures the effectiveness of the decisions of the business operations. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

internal users use the resources of the business in the most effective ways. With the helps these

users the business can analysis the financial performance, cash flow and measure the strength of

the business to take the opportunities of the business. Examples of the internal users who uses

the accounting information in the business are:

Owners: Owners of the business are fully responsible for the success and growth of the business,

so they will use the report of the accounting to measure the profits for the investment. They use

the information of the accounting for making the effective decisions for the future for example

deciding which strategy and techniques is useful for the business (Penn and Pennix, 2017).

Management: the accounting information is uses by the management for the execution of the

decision which is taken by the owners of the business. Management of the business takes the

direction from the owners for monitoring and results of the reports from the accounting

information.

Employees: the accounting information of the company is used by the employees also to make

sure that how stable the company is for security of their jobs. When the employees of the

business get the bonus, commission, share of profits provided then they are interested in the

financial information of the business.

External users of the accounting information:

External users are those users which are not the part of the company but have interest in

the accounting information of the business. In the accounting information of the business

externals users have the direct and the indirect interest. The examples of the external users of

accounting information are creditors, investors, government, trading partners etc.

Creditors: the accounting information is used by the creditors to check the ability of the

borrowers to repay the loan, income evidence, position in the economy, income evidence etc.

before they give money to the economic entity by the business (Brakeville and Perepa, 2016).

Investors: Investors check the financial report of the company to measure the possibility of the

business in the future before investing in it. To make sure that the investment is secure financial

information is essential for the investors.

Trading partners: After checking the financial information the trading companies make the

decision to trade with the fix entity of the economy.

users the business can analysis the financial performance, cash flow and measure the strength of

the business to take the opportunities of the business. Examples of the internal users who uses

the accounting information in the business are:

Owners: Owners of the business are fully responsible for the success and growth of the business,

so they will use the report of the accounting to measure the profits for the investment. They use

the information of the accounting for making the effective decisions for the future for example

deciding which strategy and techniques is useful for the business (Penn and Pennix, 2017).

Management: the accounting information is uses by the management for the execution of the

decision which is taken by the owners of the business. Management of the business takes the

direction from the owners for monitoring and results of the reports from the accounting

information.

Employees: the accounting information of the company is used by the employees also to make

sure that how stable the company is for security of their jobs. When the employees of the

business get the bonus, commission, share of profits provided then they are interested in the

financial information of the business.

External users of the accounting information:

External users are those users which are not the part of the company but have interest in

the accounting information of the business. In the accounting information of the business

externals users have the direct and the indirect interest. The examples of the external users of

accounting information are creditors, investors, government, trading partners etc.

Creditors: the accounting information is used by the creditors to check the ability of the

borrowers to repay the loan, income evidence, position in the economy, income evidence etc.

before they give money to the economic entity by the business (Brakeville and Perepa, 2016).

Investors: Investors check the financial report of the company to measure the possibility of the

business in the future before investing in it. To make sure that the investment is secure financial

information is essential for the investors.

Trading partners: After checking the financial information the trading companies make the

decision to trade with the fix entity of the economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Government: The agencies of the government monitor the market and the economy with the

help of the financial information of the business. The government examine the success and

growth of the companies to provide the financial help to them.

Accounting plays an essential role in the effective running of the business it helps to

measure the income and expenditure. It provides the effective and quality information to the

investors, government and management which is used to take the decisions of the business. The

financial transactions of the operations of the business and the transaction of the assets and

liabilities all are recorded in the books of the accounting of the company. The business

management requires the accurate information of the accounting for different reasons like

effective planning, decision-making, and for measuring the profits and losses of the company.

Planning: To start the operations of the business there is need of the effective planning in the

business to determine the success of the business (Pennington, 2018). With the help of the

accounting information company will determine the present trends of economy such as, demand

of consumer, size of the market, numbers of competitors.

Decisions of management: The information of the accounting is generally used to make the

effective decisions of the business. Expenses of the accounting and statement of the income

gives the brief of the business for financial management. The management of the business uses

the accounting information to take the effective decisions to improve the business operations by

entering the new markets with the facility of the existing production.

Profitability: to measure the total profitability of the business there is the need of the accounting

information. The level of the profits can be determined by the sales, manufacturing cost,

expensive and inventory which is recorded in the management of the company.

Performance analysis: when the transaction of the business are accurately recorded in the

statement of the financial then accountant of the company will examine the strength of the

operations of the business (Bergner, and et.al., 2018). The performance analysis helps the

company to identify the areas of the company which is weak and helps to give the solutions to

enhance the activities of the business.

help of the financial information of the business. The government examine the success and

growth of the companies to provide the financial help to them.

Accounting plays an essential role in the effective running of the business it helps to

measure the income and expenditure. It provides the effective and quality information to the

investors, government and management which is used to take the decisions of the business. The

financial transactions of the operations of the business and the transaction of the assets and

liabilities all are recorded in the books of the accounting of the company. The business

management requires the accurate information of the accounting for different reasons like

effective planning, decision-making, and for measuring the profits and losses of the company.

Planning: To start the operations of the business there is need of the effective planning in the

business to determine the success of the business (Pennington, 2018). With the help of the

accounting information company will determine the present trends of economy such as, demand

of consumer, size of the market, numbers of competitors.

Decisions of management: The information of the accounting is generally used to make the

effective decisions of the business. Expenses of the accounting and statement of the income

gives the brief of the business for financial management. The management of the business uses

the accounting information to take the effective decisions to improve the business operations by

entering the new markets with the facility of the existing production.

Profitability: to measure the total profitability of the business there is the need of the accounting

information. The level of the profits can be determined by the sales, manufacturing cost,

expensive and inventory which is recorded in the management of the company.

Performance analysis: when the transaction of the business are accurately recorded in the

statement of the financial then accountant of the company will examine the strength of the

operations of the business (Bergner, and et.al., 2018). The performance analysis helps the

company to identify the areas of the company which is weak and helps to give the solutions to

enhance the activities of the business.

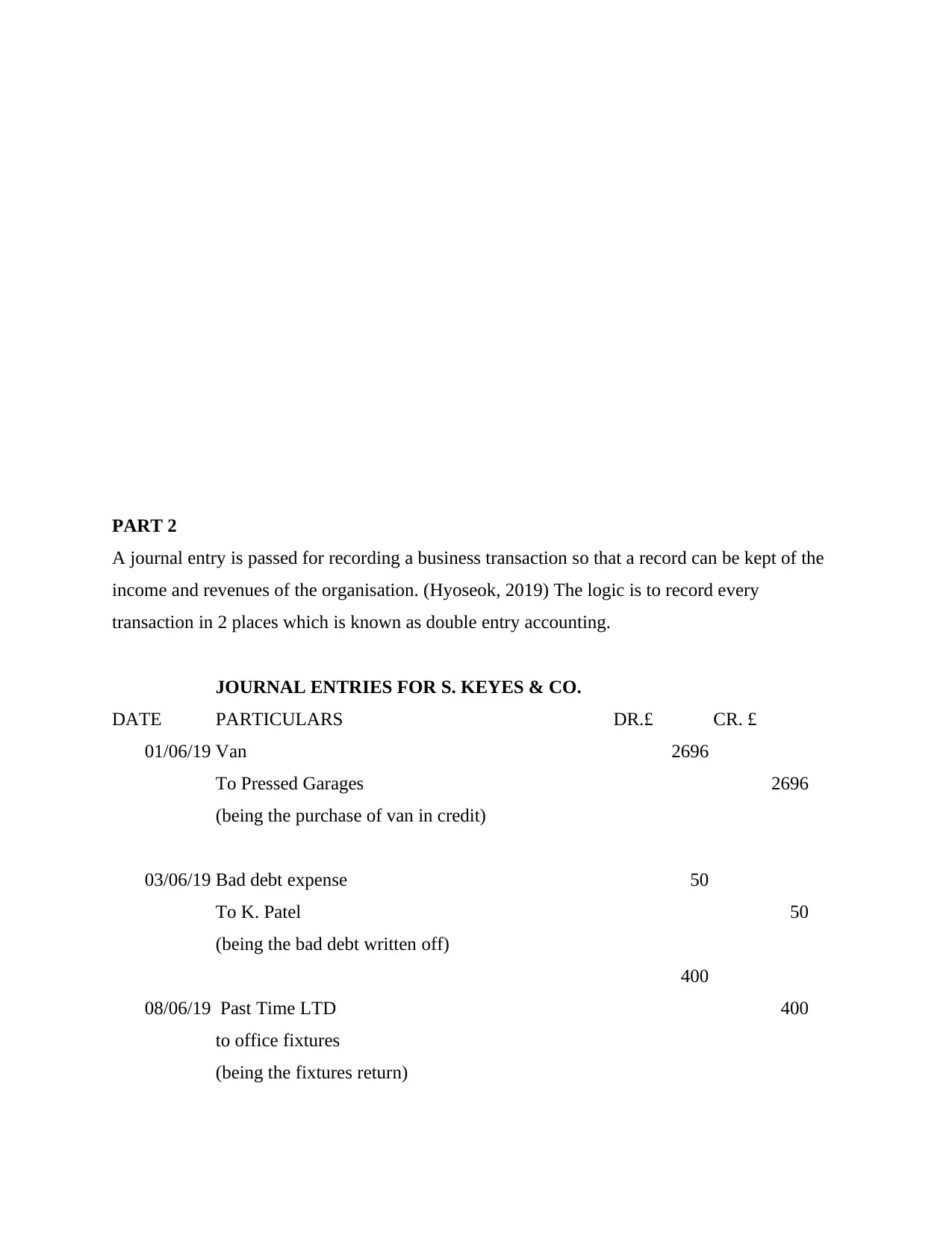

PART 2

A journal entry is passed for recording a business transaction so that a record can be kept of the

income and revenues of the organisation. (Hyoseok, 2019) The logic is to record every

transaction in 2 places which is known as double entry accounting.

JOURNAL ENTRIES FOR S. KEYES & CO.

DATE PARTICULARS DR.£ CR. £

01/06/19 Van 2696

To Pressed Garages 2696

(being the purchase of van in credit)

03/06/19 Bad debt expense 50

To K. Patel 50

(being the bad debt written off)

400

08/06/19 Past Time LTD 400

to office fixtures

(being the fixtures return)

A journal entry is passed for recording a business transaction so that a record can be kept of the

income and revenues of the organisation. (Hyoseok, 2019) The logic is to record every

transaction in 2 places which is known as double entry accounting.

JOURNAL ENTRIES FOR S. KEYES & CO.

DATE PARTICULARS DR.£ CR. £

01/06/19 Van 2696

To Pressed Garages 2696

(being the purchase of van in credit)

03/06/19 Bad debt expense 50

To K. Patel 50

(being the bad debt written off)

400

08/06/19 Past Time LTD 400

to office fixtures

(being the fixtures return)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

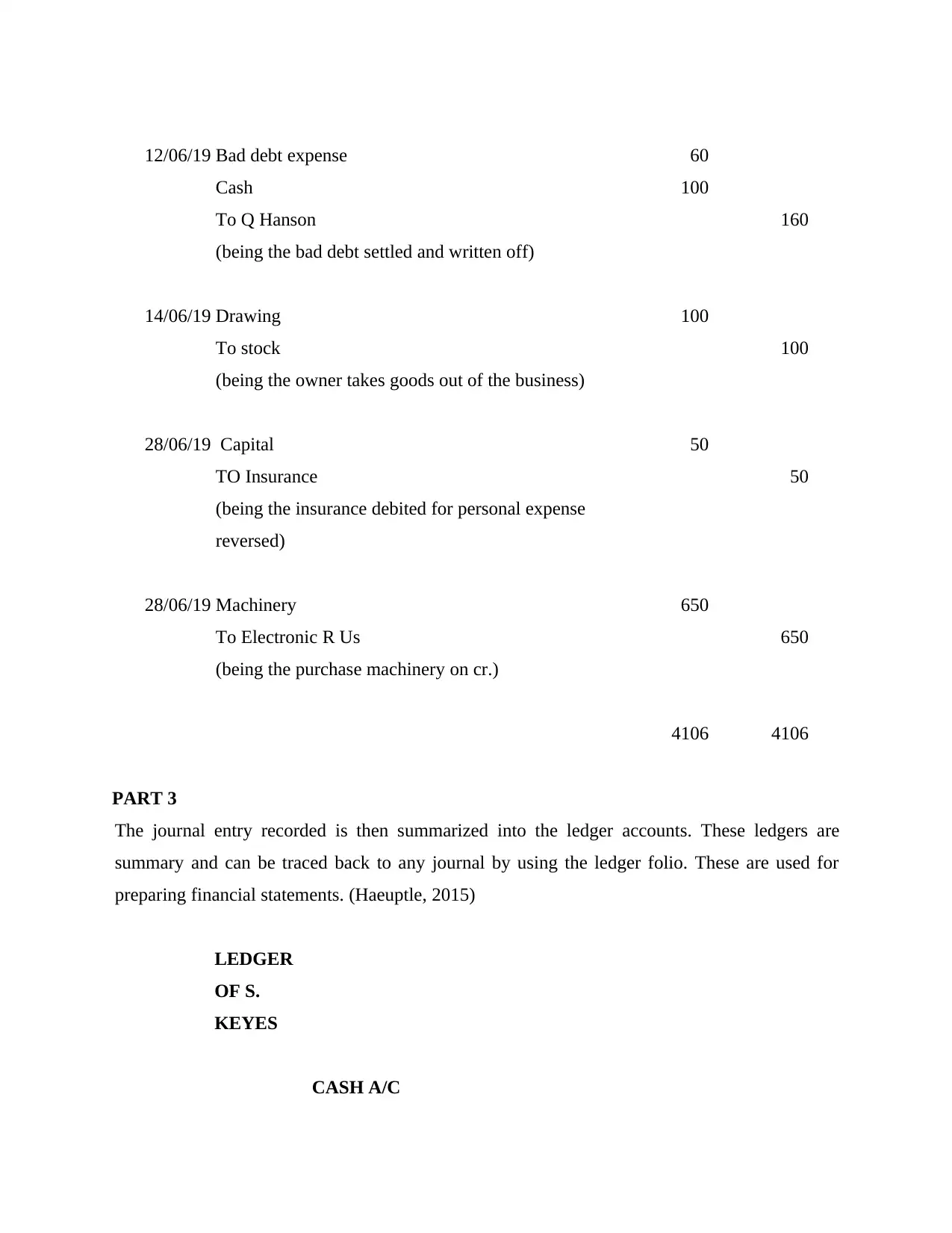

12/06/19 Bad debt expense 60

Cash 100

To Q Hanson 160

(being the bad debt settled and written off)

14/06/19 Drawing 100

To stock 100

(being the owner takes goods out of the business)

28/06/19 Capital 50

TO Insurance 50

(being the insurance debited for personal expense

reversed)

28/06/19 Machinery 650

To Electronic R Us 650

(being the purchase machinery on cr.)

4106 4106

PART 3

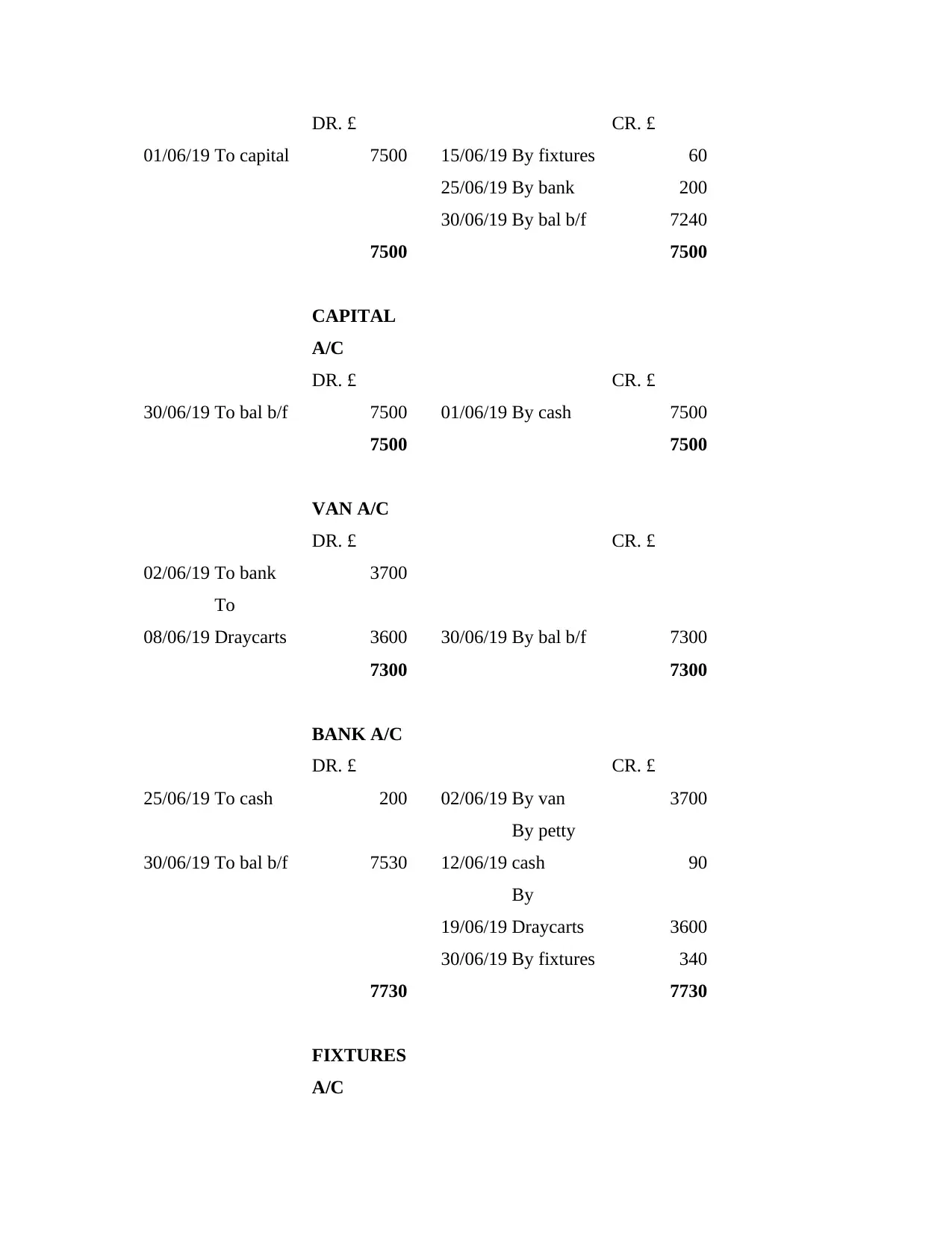

The journal entry recorded is then summarized into the ledger accounts. These ledgers are

summary and can be traced back to any journal by using the ledger folio. These are used for

preparing financial statements. (Haeuptle, 2015)

LEDGER

OF S.

KEYES

CASH A/C

Cash 100

To Q Hanson 160

(being the bad debt settled and written off)

14/06/19 Drawing 100

To stock 100

(being the owner takes goods out of the business)

28/06/19 Capital 50

TO Insurance 50

(being the insurance debited for personal expense

reversed)

28/06/19 Machinery 650

To Electronic R Us 650

(being the purchase machinery on cr.)

4106 4106

PART 3

The journal entry recorded is then summarized into the ledger accounts. These ledgers are

summary and can be traced back to any journal by using the ledger folio. These are used for

preparing financial statements. (Haeuptle, 2015)

LEDGER

OF S.

KEYES

CASH A/C

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DR. £ CR. £

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL

A/C

DR. £ CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

DR. £ CR. £

02/06/19 To bank 3700

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

DR. £ CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

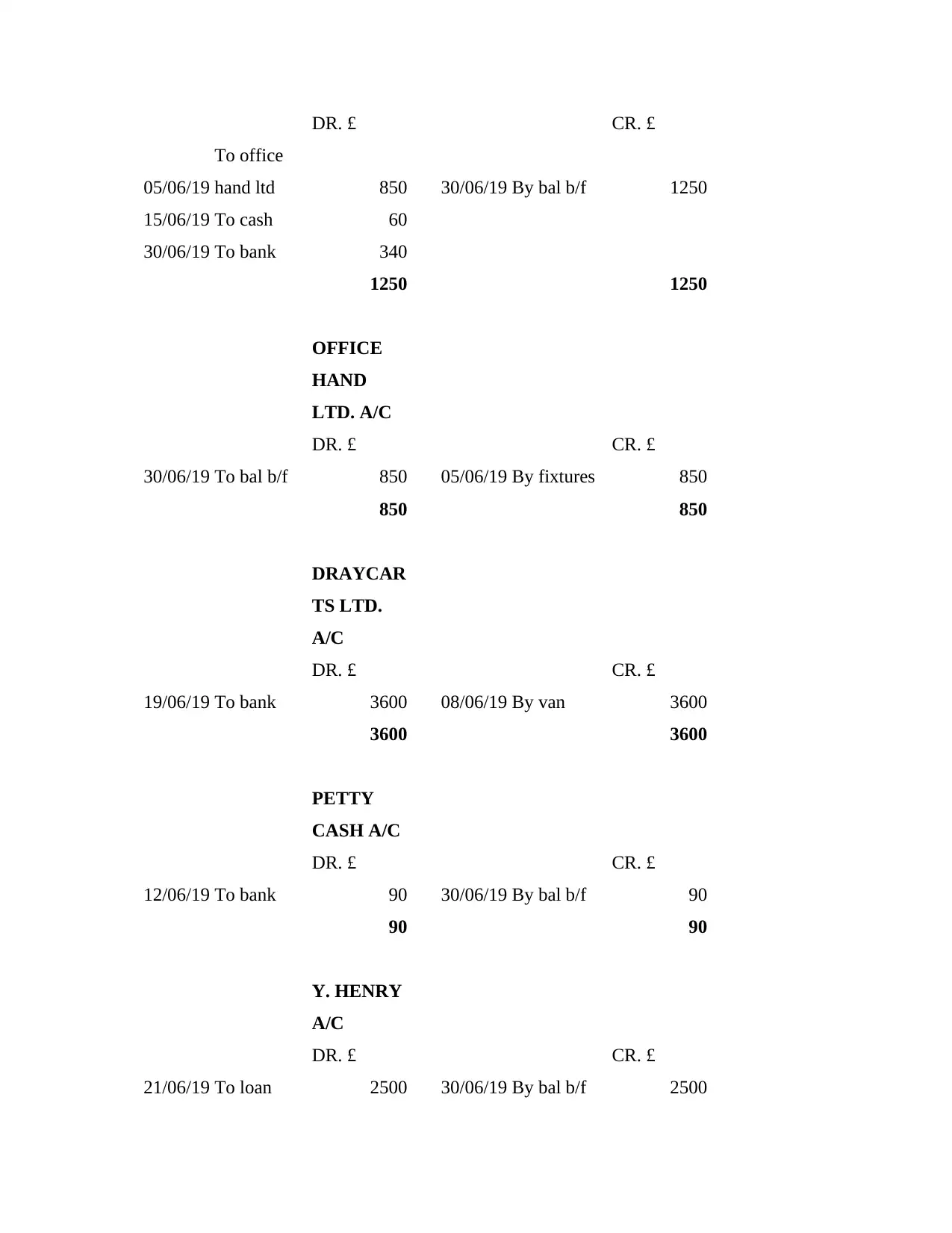

FIXTURES

A/C

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL

A/C

DR. £ CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

DR. £ CR. £

02/06/19 To bank 3700

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

DR. £ CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

FIXTURES

A/C

DR. £ CR. £

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

1250 1250

OFFICE

HAND

LTD. A/C

DR. £ CR. £

30/06/19 To bal b/f 850 05/06/19 By fixtures 850

850 850

DRAYCAR

TS LTD.

A/C

DR. £ CR. £

19/06/19 To bank 3600 08/06/19 By van 3600

3600 3600

PETTY

CASH A/C

DR. £ CR. £

12/06/19 To bank 90 30/06/19 By bal b/f 90

90 90

Y. HENRY

A/C

DR. £ CR. £

21/06/19 To loan 2500 30/06/19 By bal b/f 2500

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

1250 1250

OFFICE

HAND

LTD. A/C

DR. £ CR. £

30/06/19 To bal b/f 850 05/06/19 By fixtures 850

850 850

DRAYCAR

TS LTD.

A/C

DR. £ CR. £

19/06/19 To bank 3600 08/06/19 By van 3600

3600 3600

PETTY

CASH A/C

DR. £ CR. £

12/06/19 To bank 90 30/06/19 By bal b/f 90

90 90

Y. HENRY

A/C

DR. £ CR. £

21/06/19 To loan 2500 30/06/19 By bal b/f 2500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.