Financial Accounting Report: Transactions, Statements, and Standards

VerifiedAdded on 2023/06/18

|27

|4441

|406

Report

AI Summary

This financial accounting report covers recording business transactions using double-entry bookkeeping, preparing final accounts, and performing reconciliations. It discusses various business transactions, single and double-entry systems, and trial balances. Scenario 1 includes journal entries, ledger accounts, and a trial balance. It also differentiates between financial statements and reporting, explains fundamental accounting principles like accrual, conservatism, cost, full disclosure, and going concern. Scenario 2 involves bank reconciliation statements and control accounts. The report emphasizes the importance of accurate financial records for effective decision-making and competitive advantage.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................14

Question 6.............................................................................................................................................16

Question 7.............................................................................................................................................18

SCENARIO 2............................................................................................................................................19

Question 1.............................................................................................................................................19

Question 2.............................................................................................................................................20

Question 3.............................................................................................................................................21

Question 4.............................................................................................................................................21

Question 5.............................................................................................................................................23

CONCLUSION.........................................................................................................................................25

REFERENCES..........................................................................................................................................27

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................14

Question 6.............................................................................................................................................16

Question 7.............................................................................................................................................18

SCENARIO 2............................................................................................................................................19

Question 1.............................................................................................................................................19

Question 2.............................................................................................................................................20

Question 3.............................................................................................................................................21

Question 4.............................................................................................................................................21

Question 5.............................................................................................................................................23

CONCLUSION.........................................................................................................................................25

REFERENCES..........................................................................................................................................27

INTRODUCTION

Financial Accounting (FA) is process of recording, summarizing and analyzing the

monetary transactions in order to have efficient decision making procedure. In the current

scenario, there is crucial requirement to gain competitive advantages through developing

systematic procedure for having effectual practices in industry to lead the company from similar

organization. The current report will include the description regarding business transactions,

double and single entry system, trail balance, difference between financial statement and

reporting, fundamental principles of accounting, etc. the practical exposure will be given by

preparing journal ledge, profit & loss account, cash flow and reconciliation statement, etc

MAIN BODY

SCENARIO 1

Question 1

Business transaction is related with interchanging goods and services between two or

more parties for the purpose accomplishing organizational goals such as profitability, higher

conversion rate, etc. There are several types of business transactions which are undertaken by

firms in industry in order to derive sufficient accomplishment of objectives. There are several

types of business transactions which are performed in form of cash and credit for the purpose of

purchasing & selling of raw materials, current and fixed assets and paying off debts, salaries,

interest, dividends, etc. In addition to this, these all practices are exerted for exchange of value.

It is measurable in terms of money which highly impacts the financial position of organization.

There are several events which can be referred as commercial transactions as they do not have

the characteristics like affecting financial position, monetary value, etc.

Single entry is the characterized by the fact that there is only one side recording of

transaction. It does not enable the firm to have effective understanding of particular transaction

to make appropriate decision making (Roberts, J., 2021). It does not associated with the formal

training and utilized by the small businesses to make the process of carrying forward activities

in comparatively easy manner due to characteristics of simplicity and cost effectiveness. In book

Financial Accounting (FA) is process of recording, summarizing and analyzing the

monetary transactions in order to have efficient decision making procedure. In the current

scenario, there is crucial requirement to gain competitive advantages through developing

systematic procedure for having effectual practices in industry to lead the company from similar

organization. The current report will include the description regarding business transactions,

double and single entry system, trail balance, difference between financial statement and

reporting, fundamental principles of accounting, etc. the practical exposure will be given by

preparing journal ledge, profit & loss account, cash flow and reconciliation statement, etc

MAIN BODY

SCENARIO 1

Question 1

Business transaction is related with interchanging goods and services between two or

more parties for the purpose accomplishing organizational goals such as profitability, higher

conversion rate, etc. There are several types of business transactions which are undertaken by

firms in industry in order to derive sufficient accomplishment of objectives. There are several

types of business transactions which are performed in form of cash and credit for the purpose of

purchasing & selling of raw materials, current and fixed assets and paying off debts, salaries,

interest, dividends, etc. In addition to this, these all practices are exerted for exchange of value.

It is measurable in terms of money which highly impacts the financial position of organization.

There are several events which can be referred as commercial transactions as they do not have

the characteristics like affecting financial position, monetary value, etc.

Single entry is the characterized by the fact that there is only one side recording of

transaction. It does not enable the firm to have effective understanding of particular transaction

to make appropriate decision making (Roberts, J., 2021). It does not associated with the formal

training and utilized by the small businesses to make the process of carrying forward activities

in comparatively easy manner due to characteristics of simplicity and cost effectiveness. In book

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system double entry system is where entry to an account needs corresponding entry to different

head. This type of system has the equal and corresponding sides known as debit & credit. It

standardize the process and maintain the accuracy of through improving efficiency via providing

reliable information by preparing financial statements. It helps in reducing errors and omission

in respect to derive sufficient ability to decline the possibility of inaccurate decisions that can

influence business procedure.

Trial Balance is a basically a worksheet that is concerned to provide information through

summarizing ledger balances. The common purpose for formulating trail balance is to ensure

entries in mathematically manner are correct. Firm get the base for preparing financial statements

through identifying and improving errors at initial stage by giving emphasis on trail balance. The

validity of accuracy of trial balance is ensured by focusing on its both debit and debit side

through assuring that these are equal (Blaufus and Hoffmann, –2020). There are several purposes

for which company prepares this so that various benefits can be obtained. The significant which

organizations get through executing trial balance includes arithmetic accuracy, preparation of

financial statements, rectifying errors, making adjustments, comparatively analysis, effective

decision am king via formulating audit reports, etc

Question 2

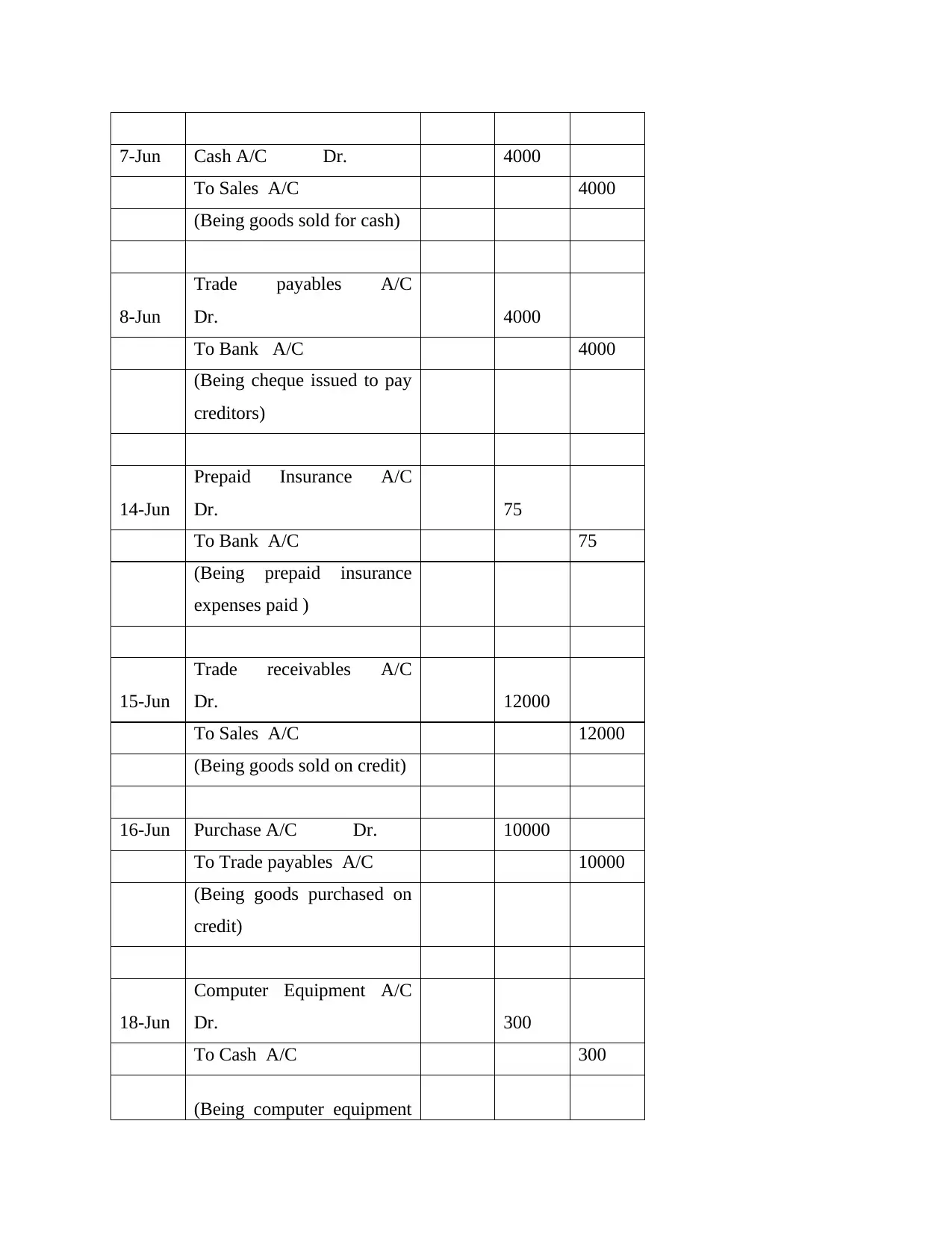

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

head. This type of system has the equal and corresponding sides known as debit & credit. It

standardize the process and maintain the accuracy of through improving efficiency via providing

reliable information by preparing financial statements. It helps in reducing errors and omission

in respect to derive sufficient ability to decline the possibility of inaccurate decisions that can

influence business procedure.

Trial Balance is a basically a worksheet that is concerned to provide information through

summarizing ledger balances. The common purpose for formulating trail balance is to ensure

entries in mathematically manner are correct. Firm get the base for preparing financial statements

through identifying and improving errors at initial stage by giving emphasis on trail balance. The

validity of accuracy of trial balance is ensured by focusing on its both debit and debit side

through assuring that these are equal (Blaufus and Hoffmann, –2020). There are several purposes

for which company prepares this so that various benefits can be obtained. The significant which

organizations get through executing trial balance includes arithmetic accuracy, preparation of

financial statements, rectifying errors, making adjustments, comparatively analysis, effective

decision am king via formulating audit reports, etc

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

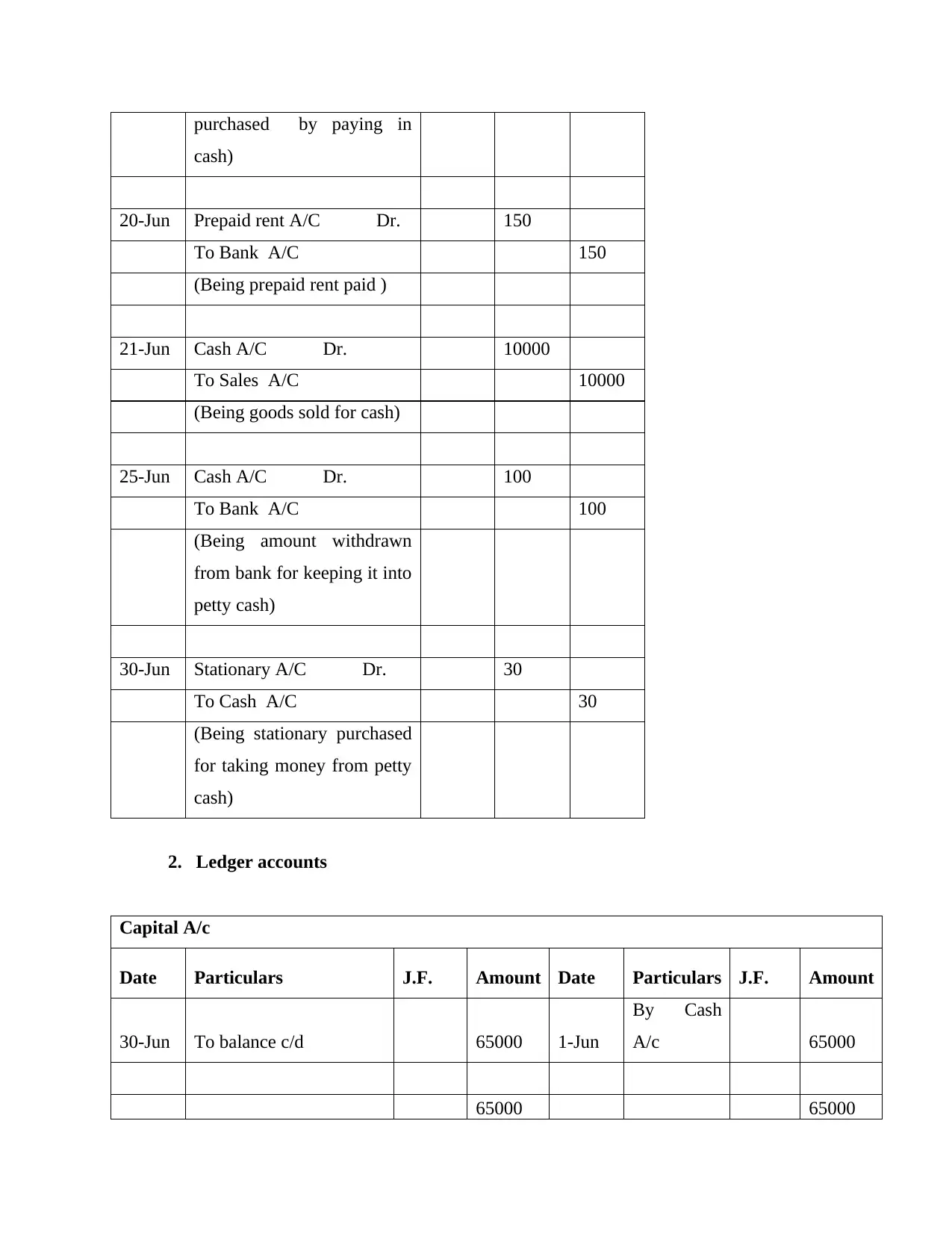

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

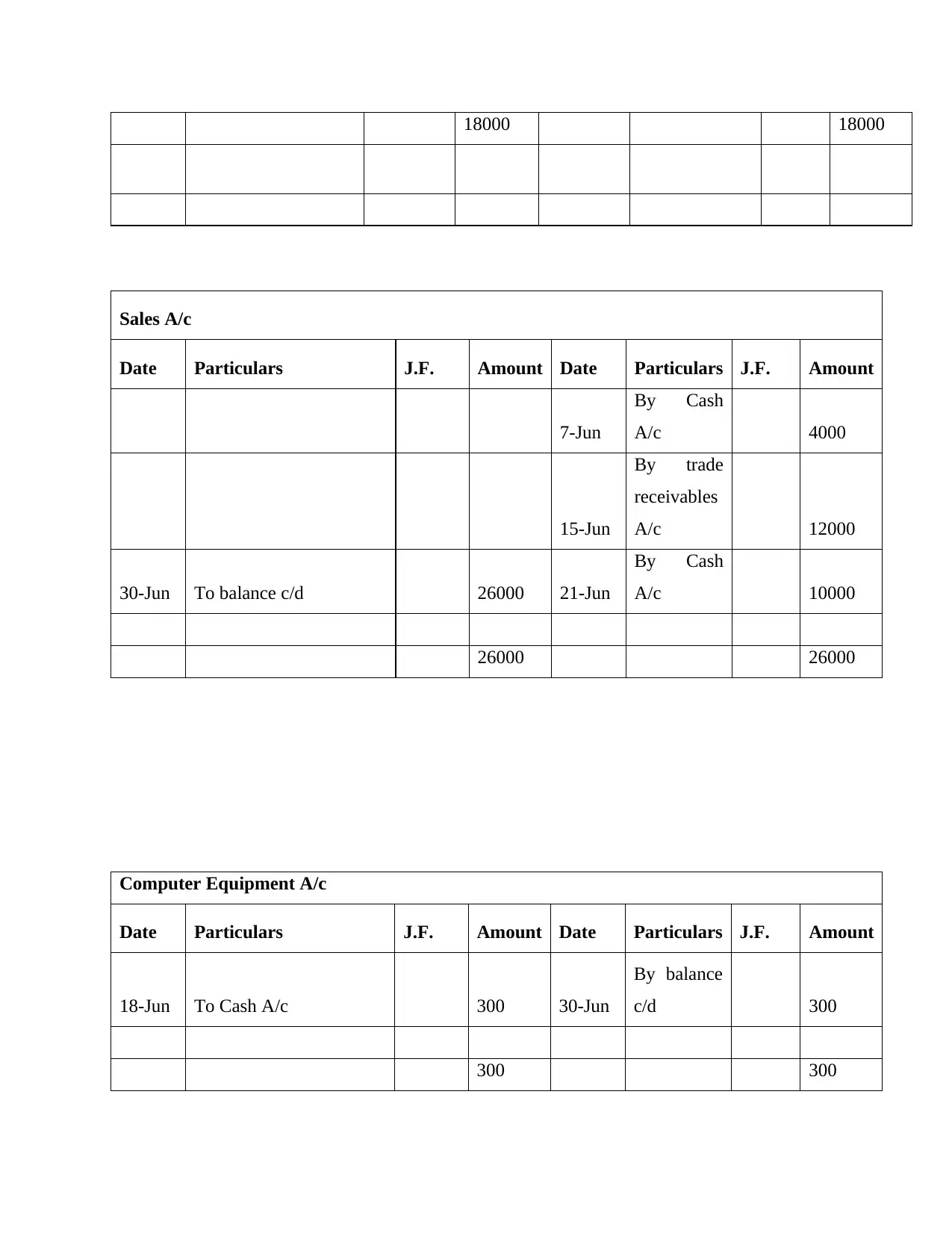

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

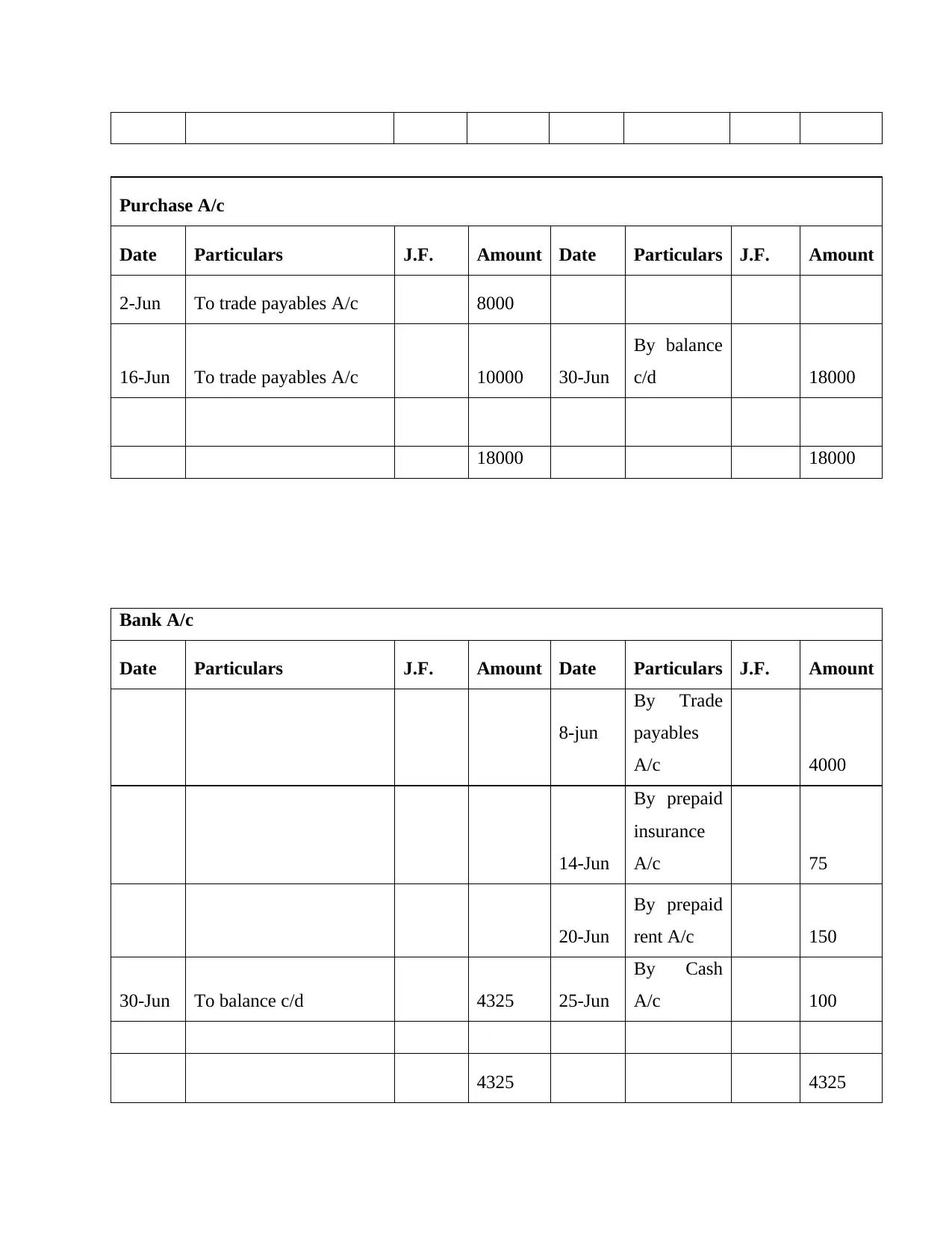

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

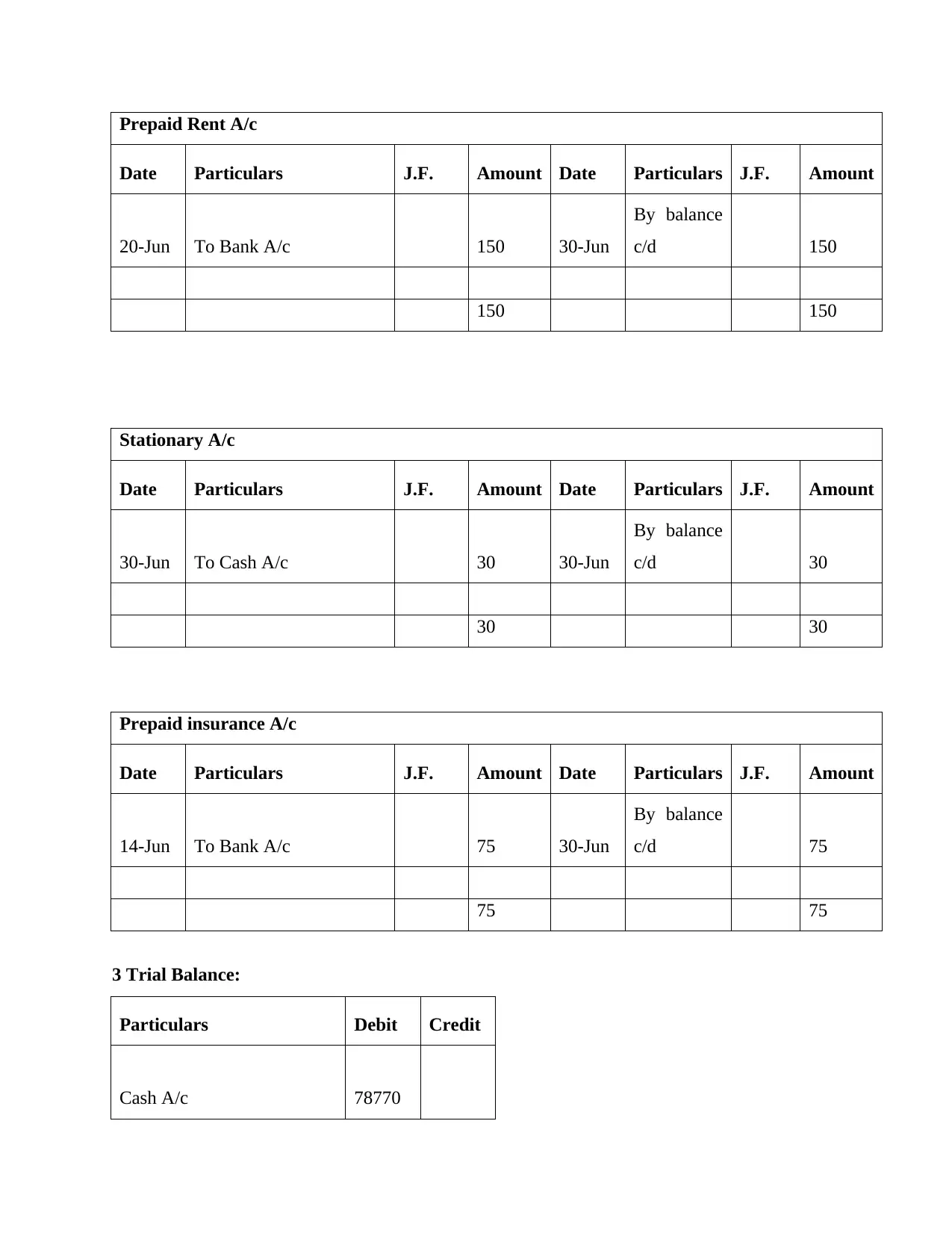

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

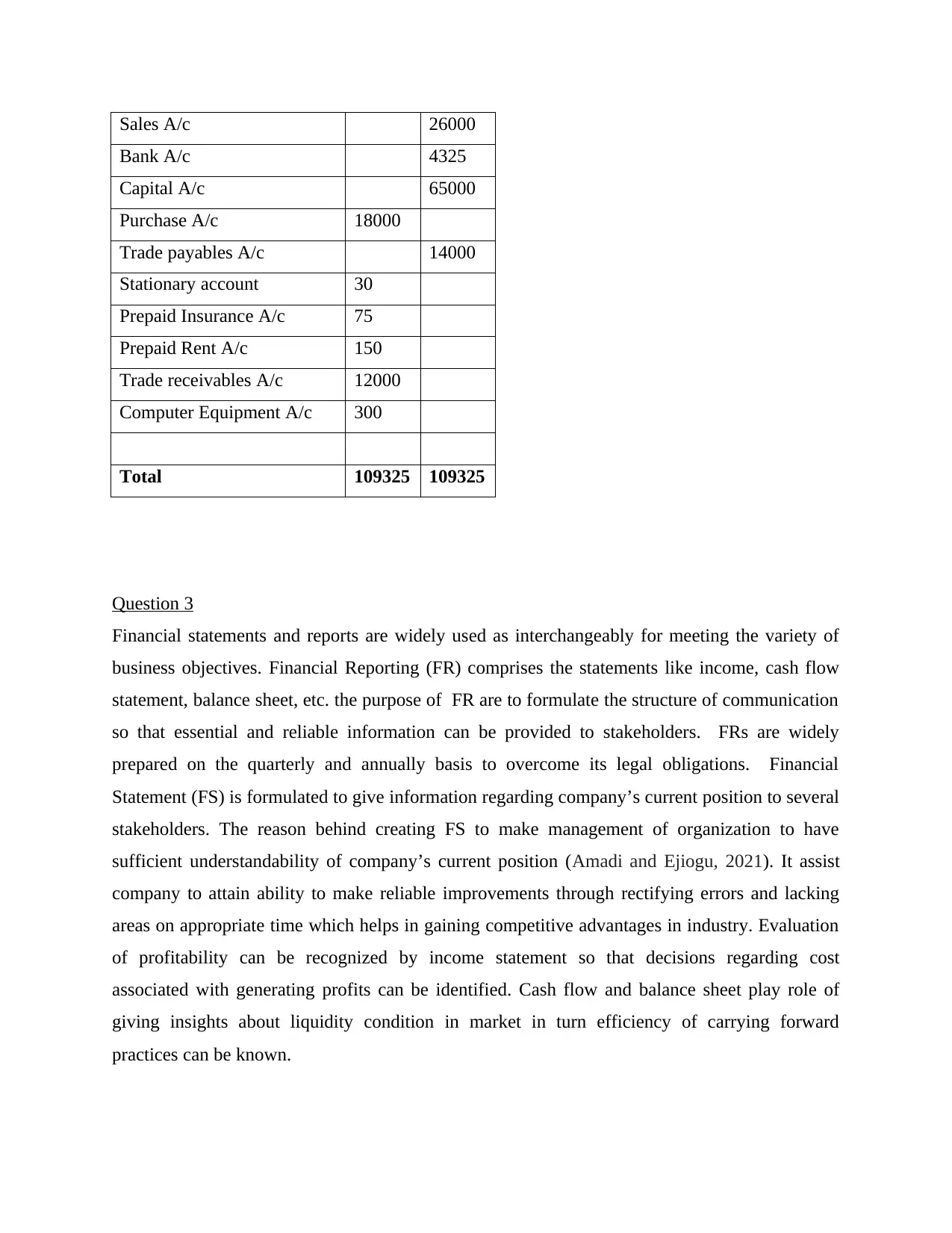

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

Financial statements and reports are widely used as interchangeably for meeting the variety of

business objectives. Financial Reporting (FR) comprises the statements like income, cash flow

statement, balance sheet, etc. the purpose of FR are to formulate the structure of communication

so that essential and reliable information can be provided to stakeholders. FRs are widely

prepared on the quarterly and annually basis to overcome its legal obligations. Financial

Statement (FS) is formulated to give information regarding company’s current position to several

stakeholders. The reason behind creating FS to make management of organization to have

sufficient understandability of company’s current position (Amadi and Ejiogu, 2021). It assist

company to attain ability to make reliable improvements through rectifying errors and lacking

areas on appropriate time which helps in gaining competitive advantages in industry. Evaluation

of profitability can be recognized by income statement so that decisions regarding cost

associated with generating profits can be identified. Cash flow and balance sheet play role of

giving insights about liquidity condition in market in turn efficiency of carrying forward

practices can be known.

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

Financial statements and reports are widely used as interchangeably for meeting the variety of

business objectives. Financial Reporting (FR) comprises the statements like income, cash flow

statement, balance sheet, etc. the purpose of FR are to formulate the structure of communication

so that essential and reliable information can be provided to stakeholders. FRs are widely

prepared on the quarterly and annually basis to overcome its legal obligations. Financial

Statement (FS) is formulated to give information regarding company’s current position to several

stakeholders. The reason behind creating FS to make management of organization to have

sufficient understandability of company’s current position (Amadi and Ejiogu, 2021). It assist

company to attain ability to make reliable improvements through rectifying errors and lacking

areas on appropriate time which helps in gaining competitive advantages in industry. Evaluation

of profitability can be recognized by income statement so that decisions regarding cost

associated with generating profits can be identified. Cash flow and balance sheet play role of

giving insights about liquidity condition in market in turn efficiency of carrying forward

practices can be known.

Financial reporting is used to provide data for the purpose of decision making whereas

statements are means of communicating information regarding monetary condition, stability, etc.

there are several types of stakeholders who are interested in utilizing the information provided in

order to have effective decision making (Filusch, 2021). The stakeholders are comprises

employees, owners, suppliers, investors, financial institutions, analyst, banks, competitors, etc

that are related to either internal or external business environment. The main purpose of investor

is to utilized given information is to have ability to formulate effective decision making.

Company requires giving reliable, relevant, timeliness and other type of qualitative

characteristics in its reports and statements so that trustworthiness in industry can be achieved.

This form of features helps inventors, suppliers, lender, etc to be confident about company’s

process and make valid decisions (Weygandt, Kimmel, and Kieso, 2018). Lenders, suppliers, etc

largely focus on the liquid position so that can get assurance of easily obtaining of their provided

funds. Organization requires maintaining appropriate and timely information providing system

with help of these reports. Internal as well external stakeholders become able to compare current

performance with previous so that potential growth of company to fulfill motive of higher

profitability can be assessed. Management of firm can determine needed improvements through

identifying lacking areas in turn respective course of action for achieving improvement can done.

Competitors of industry as well concentrate on financial information of similar organization to

assess data about competitive advantages like pricing strategy, differentiation, etc can be known

to make suitable action for getting success in sector.

Question 4

Accounting principles are the rules which helps firm to get guidance in form of having smooth

functioning through maintain appropriate balance in its business practices. Different fundaments

principles of accounting are important for all types of entities irrespective of their scale of

operation.

Accrual Principle

It is associated with recording the business transactions in accounting period in which it

has took place. This particular principle is basically concerned with making the procedure of

recording, analyzing and controlling financial information in effectual manner. In addition to

this, it is significant for the company to evaluate accurate condition of company in industry in

statements are means of communicating information regarding monetary condition, stability, etc.

there are several types of stakeholders who are interested in utilizing the information provided in

order to have effective decision making (Filusch, 2021). The stakeholders are comprises

employees, owners, suppliers, investors, financial institutions, analyst, banks, competitors, etc

that are related to either internal or external business environment. The main purpose of investor

is to utilized given information is to have ability to formulate effective decision making.

Company requires giving reliable, relevant, timeliness and other type of qualitative

characteristics in its reports and statements so that trustworthiness in industry can be achieved.

This form of features helps inventors, suppliers, lender, etc to be confident about company’s

process and make valid decisions (Weygandt, Kimmel, and Kieso, 2018). Lenders, suppliers, etc

largely focus on the liquid position so that can get assurance of easily obtaining of their provided

funds. Organization requires maintaining appropriate and timely information providing system

with help of these reports. Internal as well external stakeholders become able to compare current

performance with previous so that potential growth of company to fulfill motive of higher

profitability can be assessed. Management of firm can determine needed improvements through

identifying lacking areas in turn respective course of action for achieving improvement can done.

Competitors of industry as well concentrate on financial information of similar organization to

assess data about competitive advantages like pricing strategy, differentiation, etc can be known

to make suitable action for getting success in sector.

Question 4

Accounting principles are the rules which helps firm to get guidance in form of having smooth

functioning through maintain appropriate balance in its business practices. Different fundaments

principles of accounting are important for all types of entities irrespective of their scale of

operation.

Accrual Principle

It is associated with recording the business transactions in accounting period in which it

has took place. This particular principle is basically concerned with making the procedure of

recording, analyzing and controlling financial information in effectual manner. In addition to

this, it is significant for the company to evaluate accurate condition of company in industry in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.