Accounting for Business Decisions: Tutorial Questions - HI5001

VerifiedAdded on 2023/01/11

|13

|1620

|22

Homework Assignment

AI Summary

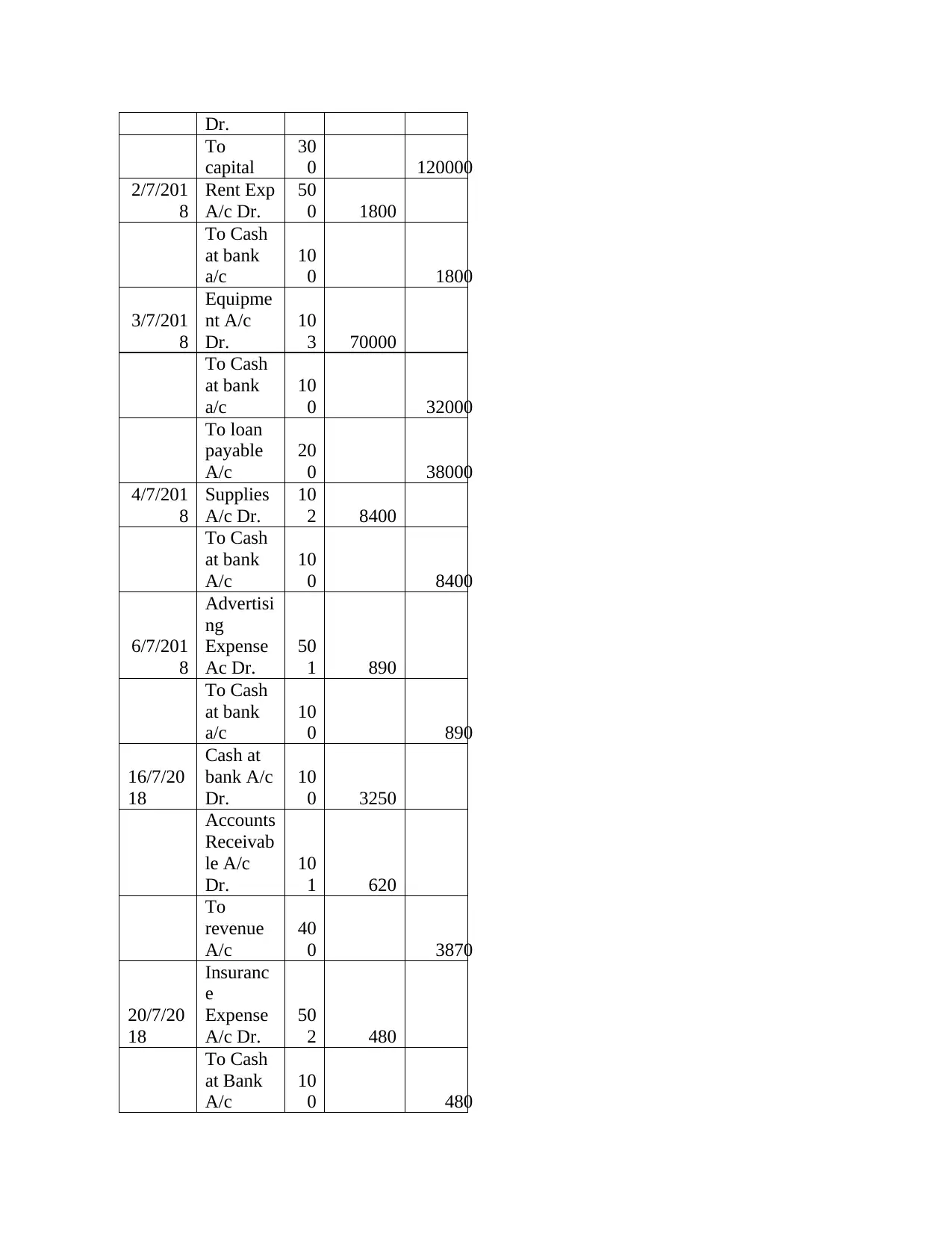

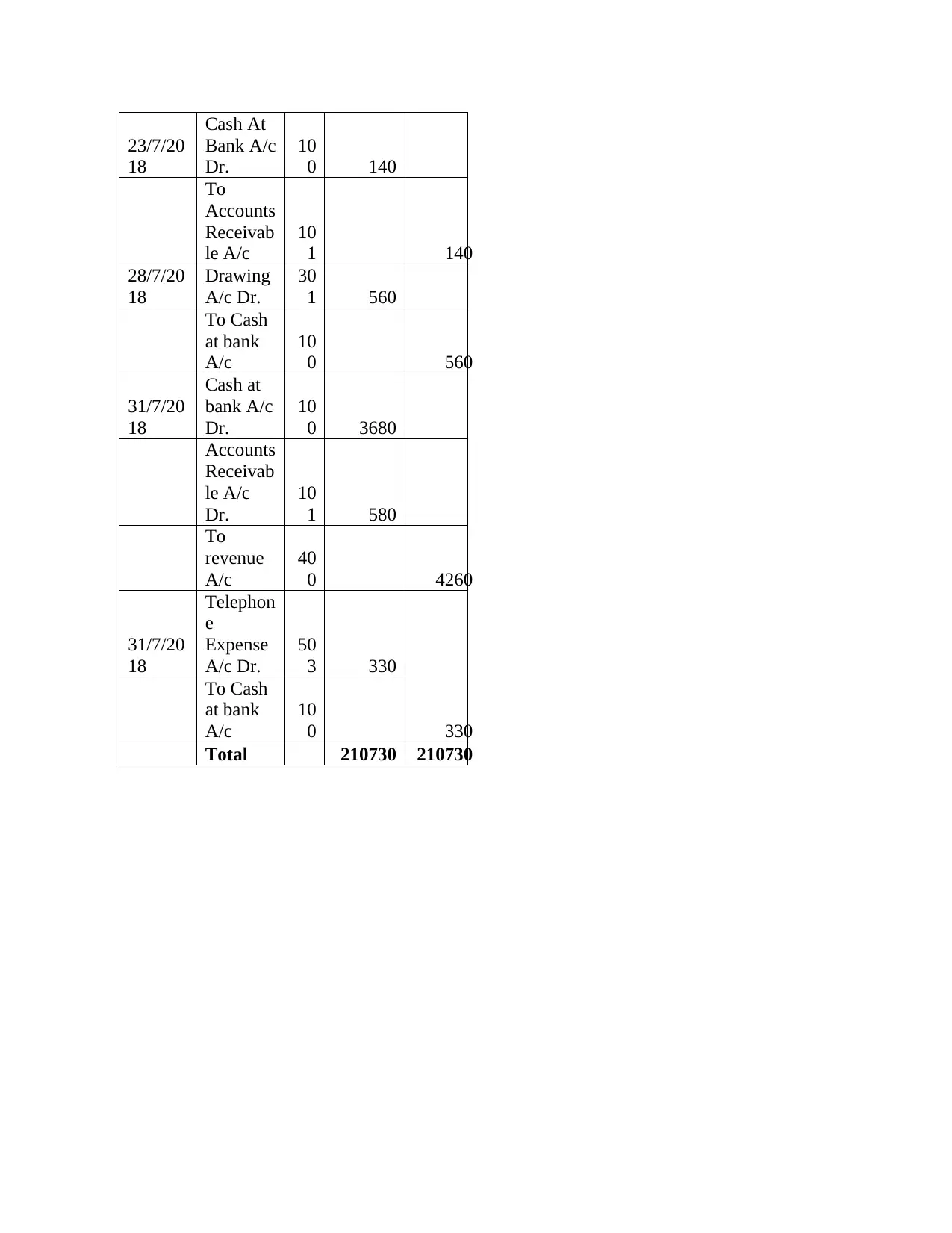

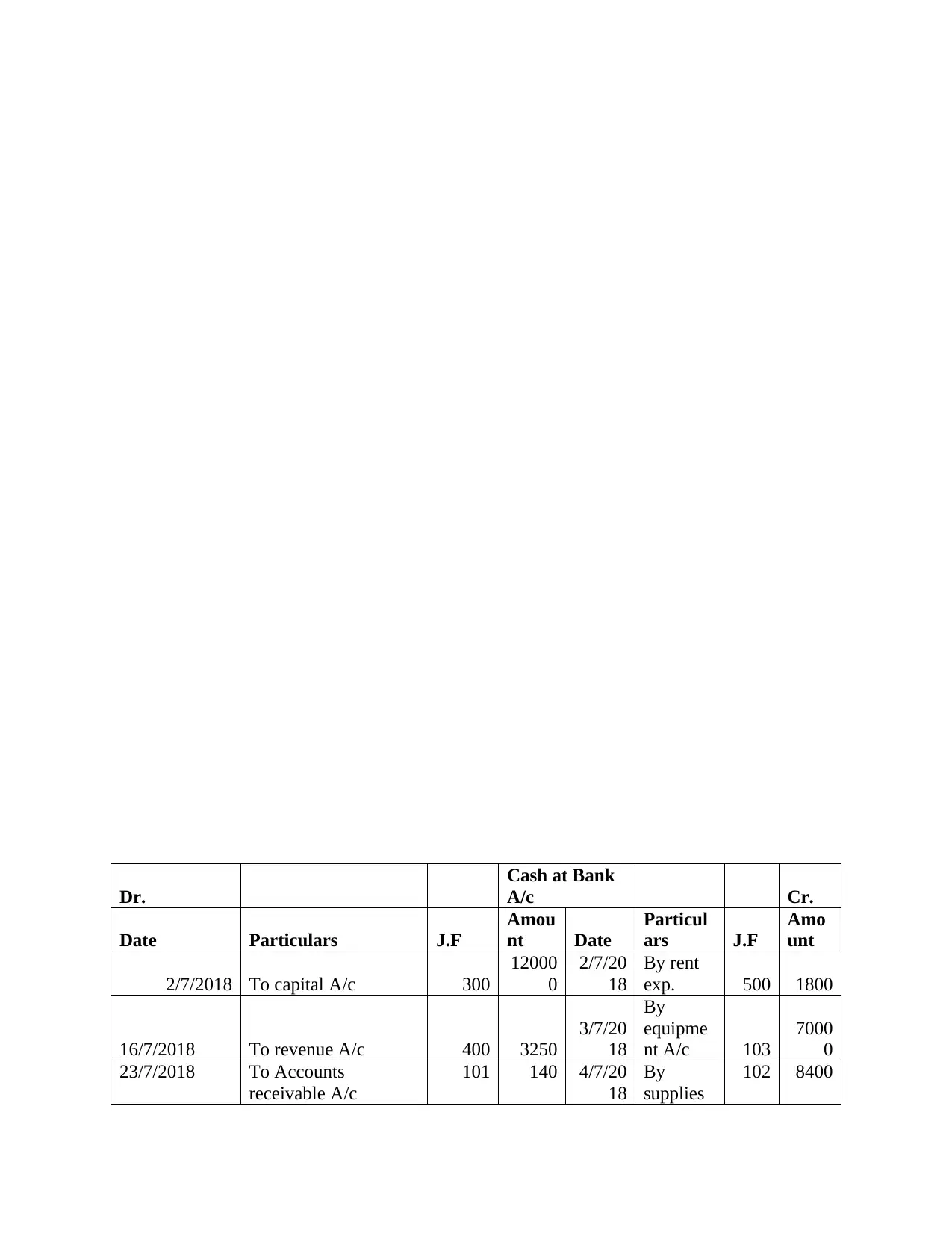

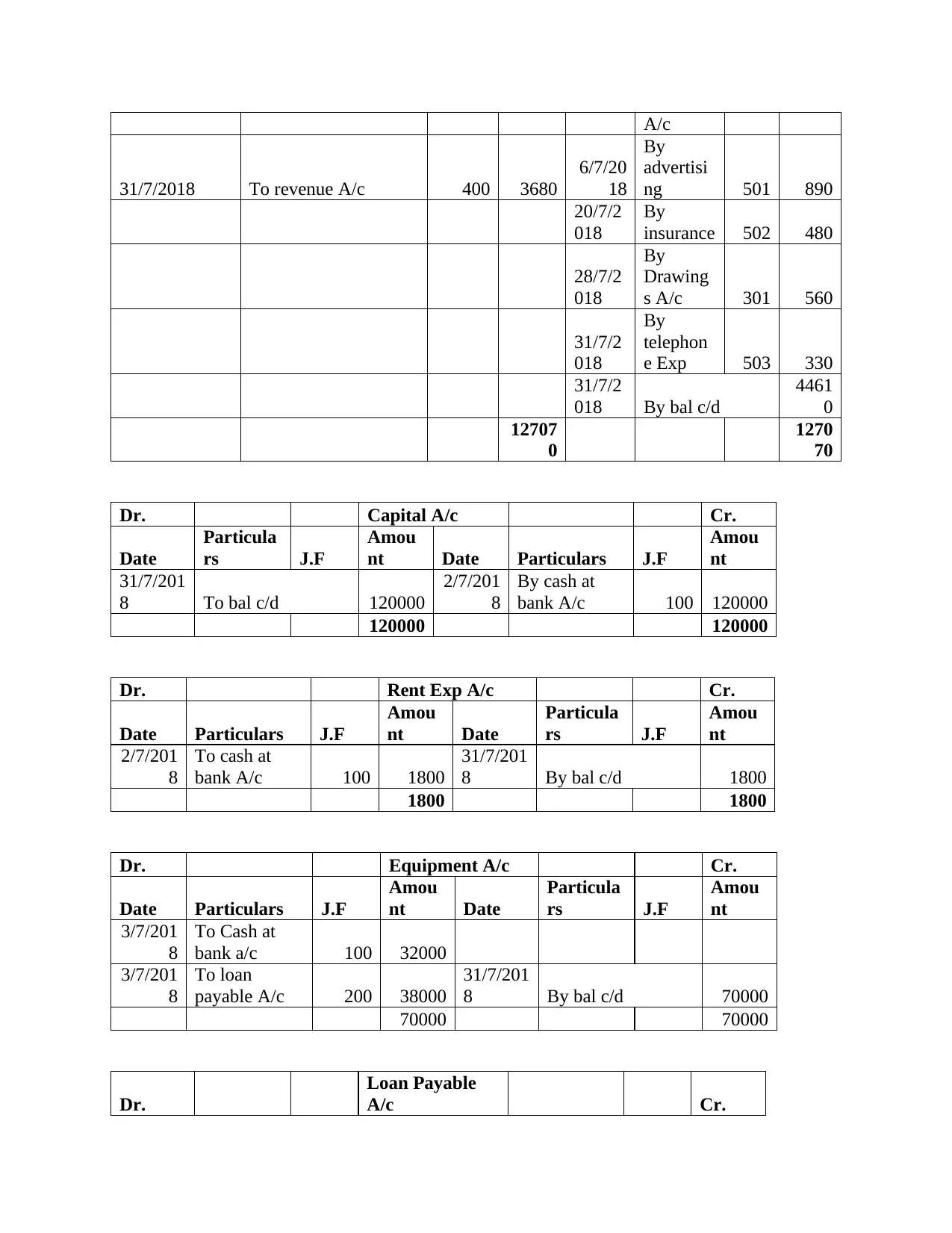

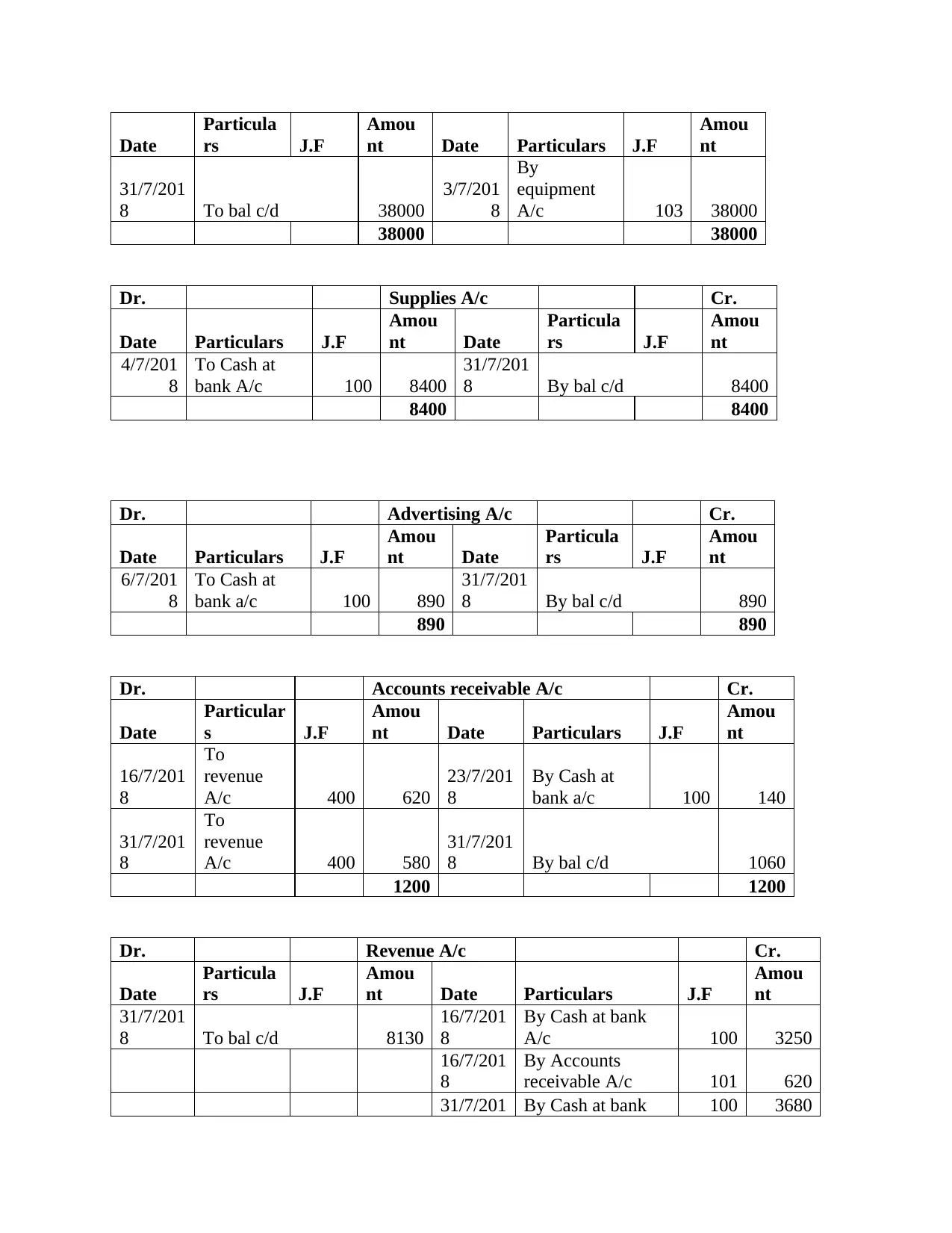

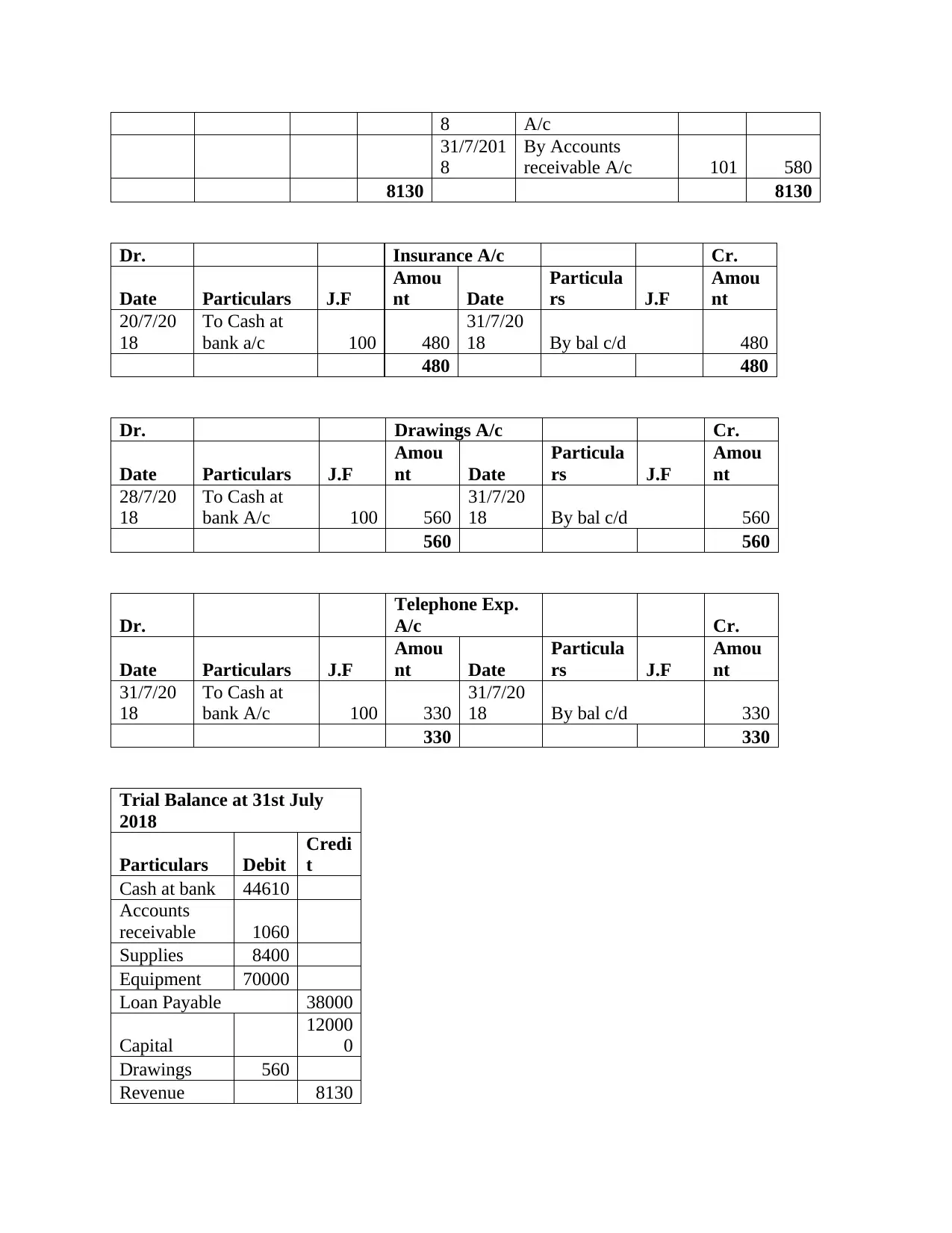

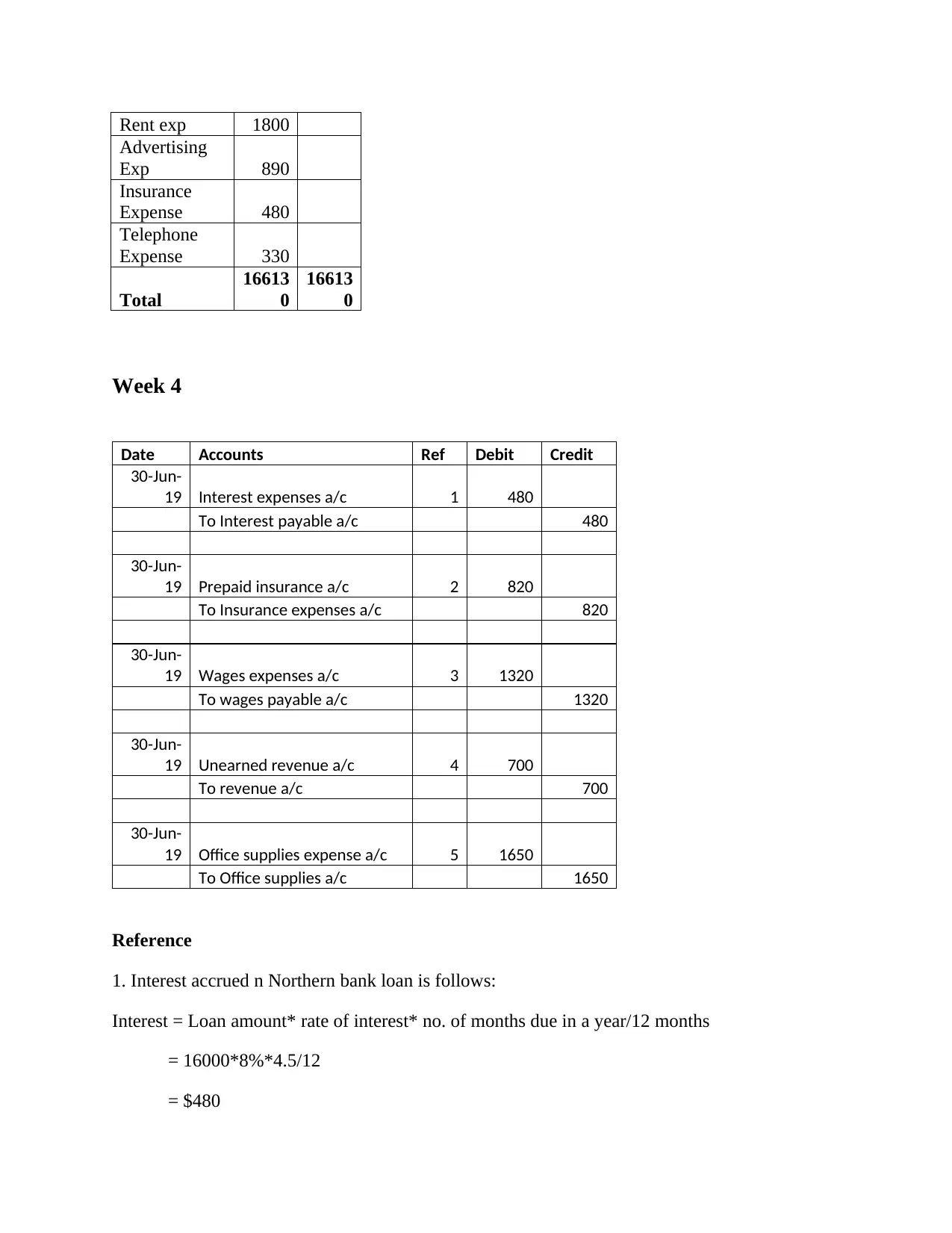

This document presents a comprehensive solution to accounting tutorial questions, addressing key concepts such as the accounting process, financial statements (income statement, balance sheet), and journal entries. The solution includes detailed examples, such as the income statement and balance sheet for a specific period, as well as journal entries for various transactions. Furthermore, the document extends to more complex topics like adjusted trial balance and closing entries, as demonstrated through the Elliot Painting Services case study. The provided solutions are designed to aid students in understanding and applying accounting principles, thereby improving their grasp of accounting for business decisions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.