Analysis of Book Value and Earnings Valuation in Accounting Research

VerifiedAdded on 2020/05/16

|12

|2886

|91

Report

AI Summary

This research proposal investigates the significance of book value and earnings valuation within the framework of contemporary accounting. It examines these variables in the context of accounting systems in France, Germany, and the U.K., emphasizing their role in stock market valuation and decision-making processes for investors and managers. The study explores the theoretical underpinnings of accounting conservatism and the value relevance of financial statement information, proposing hypotheses related to the impact of earnings per share, book value per share, and adverse earnings on stock price valuation. The research methodology involves analyzing data from Global Vantage Industrial Commercial database, with the aim of establishing correlations between accounting variables and market values. The conclusion anticipates that the research will validate the connection between corporate governance practices and enhanced accounting information, and that the findings will show that book value is increasingly value relevant than earnings per share in stock price valuation.

Running head: CONTEMPORARY ACCOUNTING ISSUES 1

Contemporary Accounting Issues

Name

Institution

Contemporary Accounting Issues

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING ISSUES 2

CONTEMPORARY ACCOUNTING ISSUES

ACKNOWLEDGEMENT

This research proposal is successful due to overwhelming support from the school

administration. I am thankful to my colleagues who helped me complete the project. I especially

thank the Lecturers for the provision of expertise and insight that helped the research process. I

am thankful to everyone who supported me during the project either directly or indirectly. Your

professional advice and guidance taught me a real-life situation and scientific research. I would

also like to give thanks to my supervisors who helped me with varied encouragement and

information. You supported me during the hardest time. Lastly, I confirm that I have keenly

monitored and taken into consideration the University misconduct policy. I acknowledge the

importance of quotation marks, sources of ideas and references when quoting someone else’s

work.

CONTEMPORARY ACCOUNTING ISSUES

ACKNOWLEDGEMENT

This research proposal is successful due to overwhelming support from the school

administration. I am thankful to my colleagues who helped me complete the project. I especially

thank the Lecturers for the provision of expertise and insight that helped the research process. I

am thankful to everyone who supported me during the project either directly or indirectly. Your

professional advice and guidance taught me a real-life situation and scientific research. I would

also like to give thanks to my supervisors who helped me with varied encouragement and

information. You supported me during the hardest time. Lastly, I confirm that I have keenly

monitored and taken into consideration the University misconduct policy. I acknowledge the

importance of quotation marks, sources of ideas and references when quoting someone else’s

work.

CONTEMPORARY ACCOUNTING ISSUES 3

INTRODUCTION

This research proposal aims at studying book value and valuation of earnings. This topic

plays a core role in recent empirical financial and theoretical accounting research. Both book

value and earnings are core variables in the model of theoretical accounting valuation. This

research proposal investigates the valuation functions of book value and earnings from the

perspective of intercontinental accounting systems of France, Germany, and the U.K. There is a

need to price the items of financial statement in the form of predicted and valuation equation.

Nevertheless, the confirmation of value relevance of accounting info is to check the reliability

and validity of financial statement prepared by the company. It explains that accounting variables

are important when related to data used by various financiers in calculating share prices.

The hypotheses of this study established based on accounting aspects that highlight book

value and valuation of earnings: 1) the extent of accounting conservatism, and 2) the actual value

significant of an income statement and balance sheet information. This paper examines them in

the context of the system of accounting of France, Germany, and U.K. The paper is arranged as

follows: Part one presents the motivation. The second part discusses literature review. The third

part offers the Research method. The fourth part is the conclusion followed by list of reference.

Practical Motivation

The issue is essential to accountant, managers, public and regulators because it provides

information concerning stock market efficiency. The data collected by both parties can be used

for the decision-making process (Pervan & Vasilj 2013). The investors can also use the stock

market valuation of earning in the calculation of the present and future share prices. Thus,

investors can decide whether to invest in specific investments based on the profitability of the

INTRODUCTION

This research proposal aims at studying book value and valuation of earnings. This topic

plays a core role in recent empirical financial and theoretical accounting research. Both book

value and earnings are core variables in the model of theoretical accounting valuation. This

research proposal investigates the valuation functions of book value and earnings from the

perspective of intercontinental accounting systems of France, Germany, and the U.K. There is a

need to price the items of financial statement in the form of predicted and valuation equation.

Nevertheless, the confirmation of value relevance of accounting info is to check the reliability

and validity of financial statement prepared by the company. It explains that accounting variables

are important when related to data used by various financiers in calculating share prices.

The hypotheses of this study established based on accounting aspects that highlight book

value and valuation of earnings: 1) the extent of accounting conservatism, and 2) the actual value

significant of an income statement and balance sheet information. This paper examines them in

the context of the system of accounting of France, Germany, and U.K. The paper is arranged as

follows: Part one presents the motivation. The second part discusses literature review. The third

part offers the Research method. The fourth part is the conclusion followed by list of reference.

Practical Motivation

The issue is essential to accountant, managers, public and regulators because it provides

information concerning stock market efficiency. The data collected by both parties can be used

for the decision-making process (Pervan & Vasilj 2013). The investors can also use the stock

market valuation of earning in the calculation of the present and future share prices. Thus,

investors can decide whether to invest in specific investments based on the profitability of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING ISSUES 4

business opportunity. Managers are also capable of measuring the economic events of the

organization as defined in the accounting regulation.

Theoretical Motivation

Conservatism in financial reporting is significant in that it acts as the firm’s efficient

technologies used in the governance process. The theoretical basis of this study embraces a

measurement approach that encompasses financial reporting reasoning and contextual

accounting. It also entail a valuation that enables the researcher and users of accounting

information to help in forecasting how different information component and accounting variables

describe the market value. The valuation theory can also assist in structuring necessary analysis

(Rabier, 2017). It enables the researcher to detect various attributes to concentrate on any task

that is vital to valuation. Most of the recent value research derives from the known theories of

valuation. Such a valuation theory is no extraordinary as the research proposal indirectly and

directly, depends on the book value and the stock market valuation.

LITERATURE REVIEW

Existing literature on empirical evidence on the importance of accounting information

originates from the U.K Market. The value importance of earnings on a stock return for a

specified time from have been investigated. The studies have discovered that the business

earnings are positively correlated to the stock return. Nevertheless, when combined data of the

firm’s profit are taken into consideration, the movements of stock are closely connected to

returns (Barth & Landsman, 2018). Most of the studies have discovered that both book value and

earnings considerably depend on the market value. Other studies have found that explanatory

power of book value and earnings variables systematically vary across industries (Zolotoy,

Frederickson & Lyon, 2017).

business opportunity. Managers are also capable of measuring the economic events of the

organization as defined in the accounting regulation.

Theoretical Motivation

Conservatism in financial reporting is significant in that it acts as the firm’s efficient

technologies used in the governance process. The theoretical basis of this study embraces a

measurement approach that encompasses financial reporting reasoning and contextual

accounting. It also entail a valuation that enables the researcher and users of accounting

information to help in forecasting how different information component and accounting variables

describe the market value. The valuation theory can also assist in structuring necessary analysis

(Rabier, 2017). It enables the researcher to detect various attributes to concentrate on any task

that is vital to valuation. Most of the recent value research derives from the known theories of

valuation. Such a valuation theory is no extraordinary as the research proposal indirectly and

directly, depends on the book value and the stock market valuation.

LITERATURE REVIEW

Existing literature on empirical evidence on the importance of accounting information

originates from the U.K Market. The value importance of earnings on a stock return for a

specified time from have been investigated. The studies have discovered that the business

earnings are positively correlated to the stock return. Nevertheless, when combined data of the

firm’s profit are taken into consideration, the movements of stock are closely connected to

returns (Barth & Landsman, 2018). Most of the studies have discovered that both book value and

earnings considerably depend on the market value. Other studies have found that explanatory

power of book value and earnings variables systematically vary across industries (Zolotoy,

Frederickson & Lyon, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING ISSUES 5

Research works of different authors have explored the unusual relationship between

accounting variables and share prices by use of data from Germany, United Kingdom, and

France. The joint explanatory power of 3 variables is approximately 60% (France), 70% (United

Kingdom) and 40% (Germany). They also enlighten through their finding that explanatory

control of both the variables differ regarding the accounting systems within the three countries.

The book value gives more details of earnings in France and Germany as compared to earnings

in the United Kingdom (Bhatia & Mulenga, 2017). Another study conducted by Graham on

international accounting differences and inspected value relevance, current residual income and

book value regarding shares. The Graham study revealed that the variable’s coefficients are

statistically significant for all the three countries (Carpenter & Whitelaw, 2017).

The value importance of book value, earnings and the actual return on equity regarding

share prices have also been investigated. There was an application of time series cross-sectional

and cross-sectional regression for the analysis of the data. The study discovered that return on

equity, book value and earnings have significant positive value on the securities of the market

value (Delkhosh, Malek, Rahimi & Farokhi, 2017). The conservatism differences in the

accounting system in France, U.K, and Germany have been studied. The hypothesis envisaged

that regression of book value and price on earnings should have the coefficient being much more

significant in France and Germany than in U.K (Alkali, Zuru & Kegudu, 2018).

Hypotheses

In this study, the core theme is the book value and valuation of earnings. The rule of

accounting system in the world requires organization’s financial statements to combine both the

income statement and the balance sheet (Hribar, Melessa, Mergenthaler & Small, 2018). The

hypotheses are:

Research works of different authors have explored the unusual relationship between

accounting variables and share prices by use of data from Germany, United Kingdom, and

France. The joint explanatory power of 3 variables is approximately 60% (France), 70% (United

Kingdom) and 40% (Germany). They also enlighten through their finding that explanatory

control of both the variables differ regarding the accounting systems within the three countries.

The book value gives more details of earnings in France and Germany as compared to earnings

in the United Kingdom (Bhatia & Mulenga, 2017). Another study conducted by Graham on

international accounting differences and inspected value relevance, current residual income and

book value regarding shares. The Graham study revealed that the variable’s coefficients are

statistically significant for all the three countries (Carpenter & Whitelaw, 2017).

The value importance of book value, earnings and the actual return on equity regarding

share prices have also been investigated. There was an application of time series cross-sectional

and cross-sectional regression for the analysis of the data. The study discovered that return on

equity, book value and earnings have significant positive value on the securities of the market

value (Delkhosh, Malek, Rahimi & Farokhi, 2017). The conservatism differences in the

accounting system in France, U.K, and Germany have been studied. The hypothesis envisaged

that regression of book value and price on earnings should have the coefficient being much more

significant in France and Germany than in U.K (Alkali, Zuru & Kegudu, 2018).

Hypotheses

In this study, the core theme is the book value and valuation of earnings. The rule of

accounting system in the world requires organization’s financial statements to combine both the

income statement and the balance sheet (Hribar, Melessa, Mergenthaler & Small, 2018). The

hypotheses are:

CONTEMPORARY ACCOUNTING ISSUES 6

Hypothesis 1: The accounting info represents a determinant which affects stock price valuation

of companies in capital market

H1a: The stock price valuations is directly related to the earnings per share

H2b: The stock price valuation is directly related to book value per share

Hypothesis 2: Book value is increasingly value relevant than earnings per share in stock price

valuation

Hypothesis 3: The relevance of book values and earnings declines when companies have adverse

earnings.

RESEARCH METHOD

In this part, I explain the statistical test that I will perform to determine the prediction

outlined in the hypotheses. The experiments concentrate mostly on the book value, the power of

earnings and the coefficient of book value and earnings. The actual data from the German,

France and United States are derived from the database of Global Vantage Industrial

Commercial (Ball, Gerakos, Linnainmaa & Nikolaev, 2017). The monthly prices and annual

financial statement are obtained from the database. The aim of the research on the valuation of

the stock is to establish a correlation between accounting variables and market values

(Muhammed, 2012).

CONCLUSION

In this research proposal, I focus much attention on the book value and stock market

valuation of the earnings regarding international context. For example, accounting setting of

Germany, United Kingdom, and France. Concentration is on accounting aspect that explains the

book value and valuation earnings (Heitzman & Huang, 2018). The first accounting aspect is the

degree of accounting conservatism and the relevance values of income statement versus the

Hypothesis 1: The accounting info represents a determinant which affects stock price valuation

of companies in capital market

H1a: The stock price valuations is directly related to the earnings per share

H2b: The stock price valuation is directly related to book value per share

Hypothesis 2: Book value is increasingly value relevant than earnings per share in stock price

valuation

Hypothesis 3: The relevance of book values and earnings declines when companies have adverse

earnings.

RESEARCH METHOD

In this part, I explain the statistical test that I will perform to determine the prediction

outlined in the hypotheses. The experiments concentrate mostly on the book value, the power of

earnings and the coefficient of book value and earnings. The actual data from the German,

France and United States are derived from the database of Global Vantage Industrial

Commercial (Ball, Gerakos, Linnainmaa & Nikolaev, 2017). The monthly prices and annual

financial statement are obtained from the database. The aim of the research on the valuation of

the stock is to establish a correlation between accounting variables and market values

(Muhammed, 2012).

CONCLUSION

In this research proposal, I focus much attention on the book value and stock market

valuation of the earnings regarding international context. For example, accounting setting of

Germany, United Kingdom, and France. Concentration is on accounting aspect that explains the

book value and valuation earnings (Heitzman & Huang, 2018). The first accounting aspect is the

degree of accounting conservatism and the relevance values of income statement versus the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING ISSUES 7

balance sheet (Ahmadi, 2017). The research also states that investigation on the value relevance

of accounting reveals the effects of firm size and the mechanisms of corporate governance

(Givoly, Hayn & Katz, 2017). It is expected that this proposal will validate that practical

corporate governance norms are connected to better accounting information.

balance sheet (Ahmadi, 2017). The research also states that investigation on the value relevance

of accounting reveals the effects of firm size and the mechanisms of corporate governance

(Givoly, Hayn & Katz, 2017). It is expected that this proposal will validate that practical

corporate governance norms are connected to better accounting information.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING ISSUES 8

REFERENCES

Ahmadi, A. (2017). The Stock Price Valuation of Earnings Per Share and Book Value: Evidence

From Tunisian Firms. The Journal of Internet Banking and Commerce, 22(1), 1-11.

Alkali, M., Zuru, N., & Kegudu, D. (2018). Book value, earnings, dividends, and audit quality on

the value relevance of accounting information among Nigerian listed

firms. Accounting, 4(2), 73-82.

Ball, R., Gerakos, J. J., Linnainmaa, J. T., & Nikolaev, V. V. (2017). Earnings, retained earnings,

and book-to-market in the cross section of expected returns.

Barth, M. E., & Landsman, W. R. (2018). Using Fair Value Earnings to Assess Firm Value.

Bhatia, M., & Mulenga, M. J. (2017). Value Relevance of Earnings and Book Value per Share:

Comparative Study of Indian Public and Private Sector Banks.

Delkhosh, M., Malek, Z., Rahimi, M., & Farokhi, Z. (2017). A comparative study of information

content of cash flow, cash value added, accounting earnings, and market value added to

book value of total assets in evaluating the firm performance. International Journal of

Accounting and Economics Studies, 5(2), 112-117.

Ferris, S. P., Hanousek, J., Shamshur, A., & Tresl, J. (2018). Asymmetries in the Firm's use of

debt to changing market values. Journal of Corporate Finance, 48, 542-555.

Givoly, D., Hayn, C., & Katz, S. (2017). The changing relevance of accounting information to

debt holders over time. Review of Accounting Studies, 22(1), 64-108.

Heitzman, S., & Huang, M. (2018). Internal Information Quality and the Sensitivity of

Investment to Market Prices and Accounting Profits.

REFERENCES

Ahmadi, A. (2017). The Stock Price Valuation of Earnings Per Share and Book Value: Evidence

From Tunisian Firms. The Journal of Internet Banking and Commerce, 22(1), 1-11.

Alkali, M., Zuru, N., & Kegudu, D. (2018). Book value, earnings, dividends, and audit quality on

the value relevance of accounting information among Nigerian listed

firms. Accounting, 4(2), 73-82.

Ball, R., Gerakos, J. J., Linnainmaa, J. T., & Nikolaev, V. V. (2017). Earnings, retained earnings,

and book-to-market in the cross section of expected returns.

Barth, M. E., & Landsman, W. R. (2018). Using Fair Value Earnings to Assess Firm Value.

Bhatia, M., & Mulenga, M. J. (2017). Value Relevance of Earnings and Book Value per Share:

Comparative Study of Indian Public and Private Sector Banks.

Delkhosh, M., Malek, Z., Rahimi, M., & Farokhi, Z. (2017). A comparative study of information

content of cash flow, cash value added, accounting earnings, and market value added to

book value of total assets in evaluating the firm performance. International Journal of

Accounting and Economics Studies, 5(2), 112-117.

Ferris, S. P., Hanousek, J., Shamshur, A., & Tresl, J. (2018). Asymmetries in the Firm's use of

debt to changing market values. Journal of Corporate Finance, 48, 542-555.

Givoly, D., Hayn, C., & Katz, S. (2017). The changing relevance of accounting information to

debt holders over time. Review of Accounting Studies, 22(1), 64-108.

Heitzman, S., & Huang, M. (2018). Internal Information Quality and the Sensitivity of

Investment to Market Prices and Accounting Profits.

CONTEMPORARY ACCOUNTING ISSUES 9

Hribar, P., Melessa, S., Mergenthaler, R., & Small, R. C. (2018). An Examination of the Relative

Abilities of Earnings and Cash Flows to Explain Returns and Market Values.

Rabier, M. R. (2017). Value is in the eye of the beholder: The relative valuation roles of earnings

and book value in merger pricing. The Accounting Review, 93(1), 335-362.

Zolotoy, L., Frederickson, J. R., & Lyon, J. D. (2017). Aggregate earnings and stock market

returns: The good, the bad, and the state-dependent. Journal of Banking & Finance, 77,

157-175.

Pervan I., & Vasilj M. (2013). Value relevance of accounting information: Evidence from South

Eastern European (SEE) countries. Economic research, (in print) Indexing: Web of

science-SSCI.

file:///C:/Users/noahh/Downloads/Value_relevance_of_accounting_information_evidence

_from_South_Eastern_European_countries.pdf

Muhammed S., M. (2012). Value Relevance of Accounting Information and Stock Market

Vulnerability – A Study on Listed Companies in Dhaka Stock Exchange, in: International

Journal of Research in Commerce and Management 3: 23-27.

http://meritresearchjournals.org/bm/content/2013/December/Tharmila%20and

%20Nimalathasan.pdf

Hribar, P., Melessa, S., Mergenthaler, R., & Small, R. C. (2018). An Examination of the Relative

Abilities of Earnings and Cash Flows to Explain Returns and Market Values.

Rabier, M. R. (2017). Value is in the eye of the beholder: The relative valuation roles of earnings

and book value in merger pricing. The Accounting Review, 93(1), 335-362.

Zolotoy, L., Frederickson, J. R., & Lyon, J. D. (2017). Aggregate earnings and stock market

returns: The good, the bad, and the state-dependent. Journal of Banking & Finance, 77,

157-175.

Pervan I., & Vasilj M. (2013). Value relevance of accounting information: Evidence from South

Eastern European (SEE) countries. Economic research, (in print) Indexing: Web of

science-SSCI.

file:///C:/Users/noahh/Downloads/Value_relevance_of_accounting_information_evidence

_from_South_Eastern_European_countries.pdf

Muhammed S., M. (2012). Value Relevance of Accounting Information and Stock Market

Vulnerability – A Study on Listed Companies in Dhaka Stock Exchange, in: International

Journal of Research in Commerce and Management 3: 23-27.

http://meritresearchjournals.org/bm/content/2013/December/Tharmila%20and

%20Nimalathasan.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING ISSUES 10

Appendix

Autho

r

Date Title Jour

nal

Type of

paper

(Theoretic

al/Empiric

al )

If

Empirical

,

Research

method

and

Sample

If

empirica

l,

Depende

nt and

indepen

dent

variable

100 words summary contribution to research question

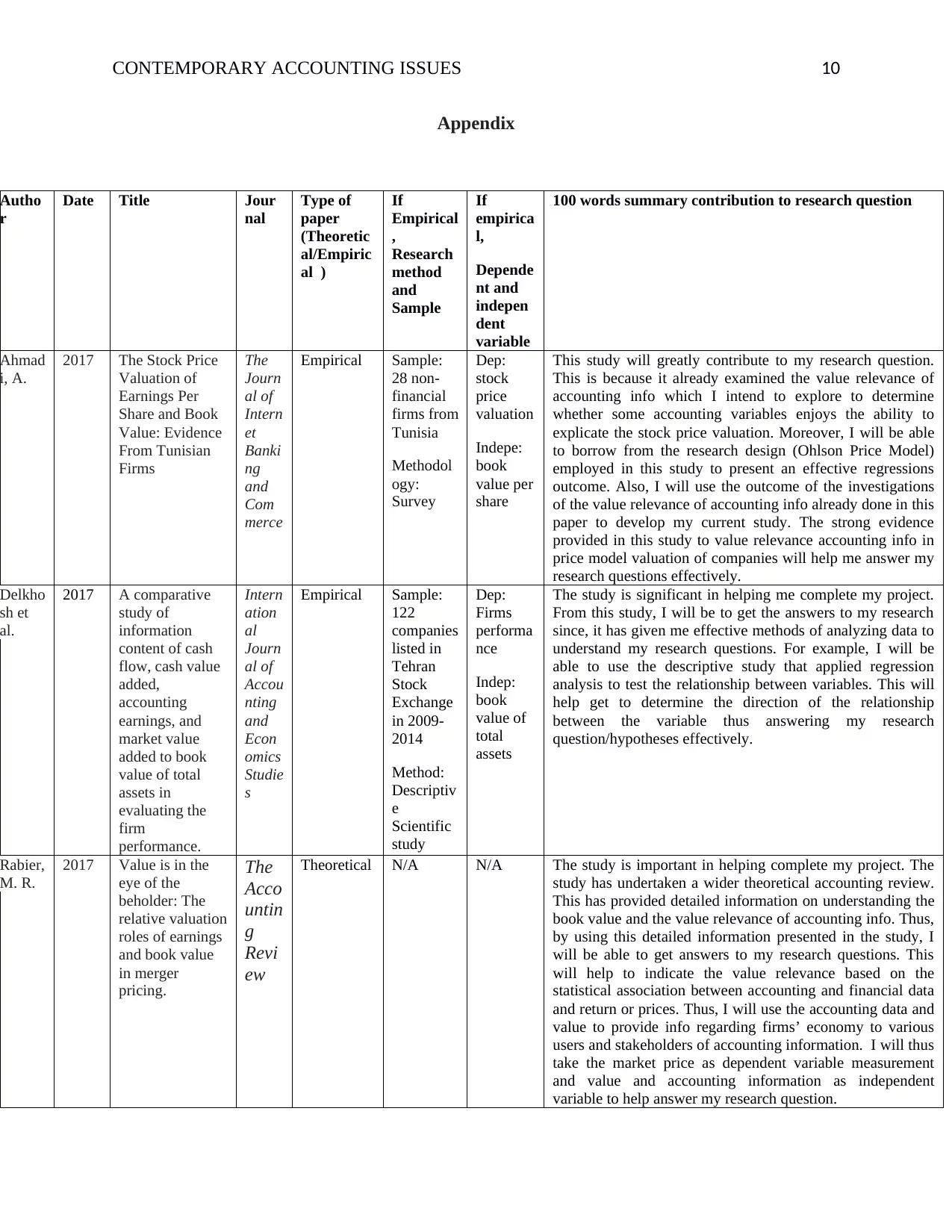

Ahmad

i, A.

2017 The Stock Price

Valuation of

Earnings Per

Share and Book

Value: Evidence

From Tunisian

Firms

The

Journ

al of

Intern

et

Banki

ng

and

Com

merce

Empirical Sample:

28 non-

financial

firms from

Tunisia

Methodol

ogy:

Survey

Dep:

stock

price

valuation

Indepe:

book

value per

share

This study will greatly contribute to my research question.

This is because it already examined the value relevance of

accounting info which I intend to explore to determine

whether some accounting variables enjoys the ability to

explicate the stock price valuation. Moreover, I will be able

to borrow from the research design (Ohlson Price Model)

employed in this study to present an effective regressions

outcome. Also, I will use the outcome of the investigations

of the value relevance of accounting info already done in this

paper to develop my current study. The strong evidence

provided in this study to value relevance accounting info in

price model valuation of companies will help me answer my

research questions effectively.

Delkho

sh et

al.

2017 A comparative

study of

information

content of cash

flow, cash value

added,

accounting

earnings, and

market value

added to book

value of total

assets in

evaluating the

firm

performance.

Intern

ation

al

Journ

al of

Accou

nting

and

Econ

omics

Studie

s

Empirical Sample:

122

companies

listed in

Tehran

Stock

Exchange

in 2009-

2014

Method:

Descriptiv

e

Scientific

study

Dep:

Firms

performa

nce

Indep:

book

value of

total

assets

The study is significant in helping me complete my project.

From this study, I will be to get the answers to my research

since, it has given me effective methods of analyzing data to

understand my research questions. For example, I will be

able to use the descriptive study that applied regression

analysis to test the relationship between variables. This will

help get to determine the direction of the relationship

between the variable thus answering my research

question/hypotheses effectively.

Rabier,

M. R.

2017 Value is in the

eye of the

beholder: The

relative valuation

roles of earnings

and book value

in merger

pricing.

The

Acco

untin

g

Revi

ew

Theoretical N/A N/A The study is important in helping complete my project. The

study has undertaken a wider theoretical accounting review.

This has provided detailed information on understanding the

book value and the value relevance of accounting info. Thus,

by using this detailed information presented in the study, I

will be able to get answers to my research questions. This

will help to indicate the value relevance based on the

statistical association between accounting and financial data

and return or prices. Thus, I will use the accounting data and

value to provide info regarding firms’ economy to various

users and stakeholders of accounting information. I will thus

take the market price as dependent variable measurement

and value and accounting information as independent

variable to help answer my research question.

Appendix

Autho

r

Date Title Jour

nal

Type of

paper

(Theoretic

al/Empiric

al )

If

Empirical

,

Research

method

and

Sample

If

empirica

l,

Depende

nt and

indepen

dent

variable

100 words summary contribution to research question

Ahmad

i, A.

2017 The Stock Price

Valuation of

Earnings Per

Share and Book

Value: Evidence

From Tunisian

Firms

The

Journ

al of

Intern

et

Banki

ng

and

Com

merce

Empirical Sample:

28 non-

financial

firms from

Tunisia

Methodol

ogy:

Survey

Dep:

stock

price

valuation

Indepe:

book

value per

share

This study will greatly contribute to my research question.

This is because it already examined the value relevance of

accounting info which I intend to explore to determine

whether some accounting variables enjoys the ability to

explicate the stock price valuation. Moreover, I will be able

to borrow from the research design (Ohlson Price Model)

employed in this study to present an effective regressions

outcome. Also, I will use the outcome of the investigations

of the value relevance of accounting info already done in this

paper to develop my current study. The strong evidence

provided in this study to value relevance accounting info in

price model valuation of companies will help me answer my

research questions effectively.

Delkho

sh et

al.

2017 A comparative

study of

information

content of cash

flow, cash value

added,

accounting

earnings, and

market value

added to book

value of total

assets in

evaluating the

firm

performance.

Intern

ation

al

Journ

al of

Accou

nting

and

Econ

omics

Studie

s

Empirical Sample:

122

companies

listed in

Tehran

Stock

Exchange

in 2009-

2014

Method:

Descriptiv

e

Scientific

study

Dep:

Firms

performa

nce

Indep:

book

value of

total

assets

The study is significant in helping me complete my project.

From this study, I will be to get the answers to my research

since, it has given me effective methods of analyzing data to

understand my research questions. For example, I will be

able to use the descriptive study that applied regression

analysis to test the relationship between variables. This will

help get to determine the direction of the relationship

between the variable thus answering my research

question/hypotheses effectively.

Rabier,

M. R.

2017 Value is in the

eye of the

beholder: The

relative valuation

roles of earnings

and book value

in merger

pricing.

The

Acco

untin

g

Revi

ew

Theoretical N/A N/A The study is important in helping complete my project. The

study has undertaken a wider theoretical accounting review.

This has provided detailed information on understanding the

book value and the value relevance of accounting info. Thus,

by using this detailed information presented in the study, I

will be able to get answers to my research questions. This

will help to indicate the value relevance based on the

statistical association between accounting and financial data

and return or prices. Thus, I will use the accounting data and

value to provide info regarding firms’ economy to various

users and stakeholders of accounting information. I will thus

take the market price as dependent variable measurement

and value and accounting information as independent

variable to help answer my research question.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING ISSUES 11

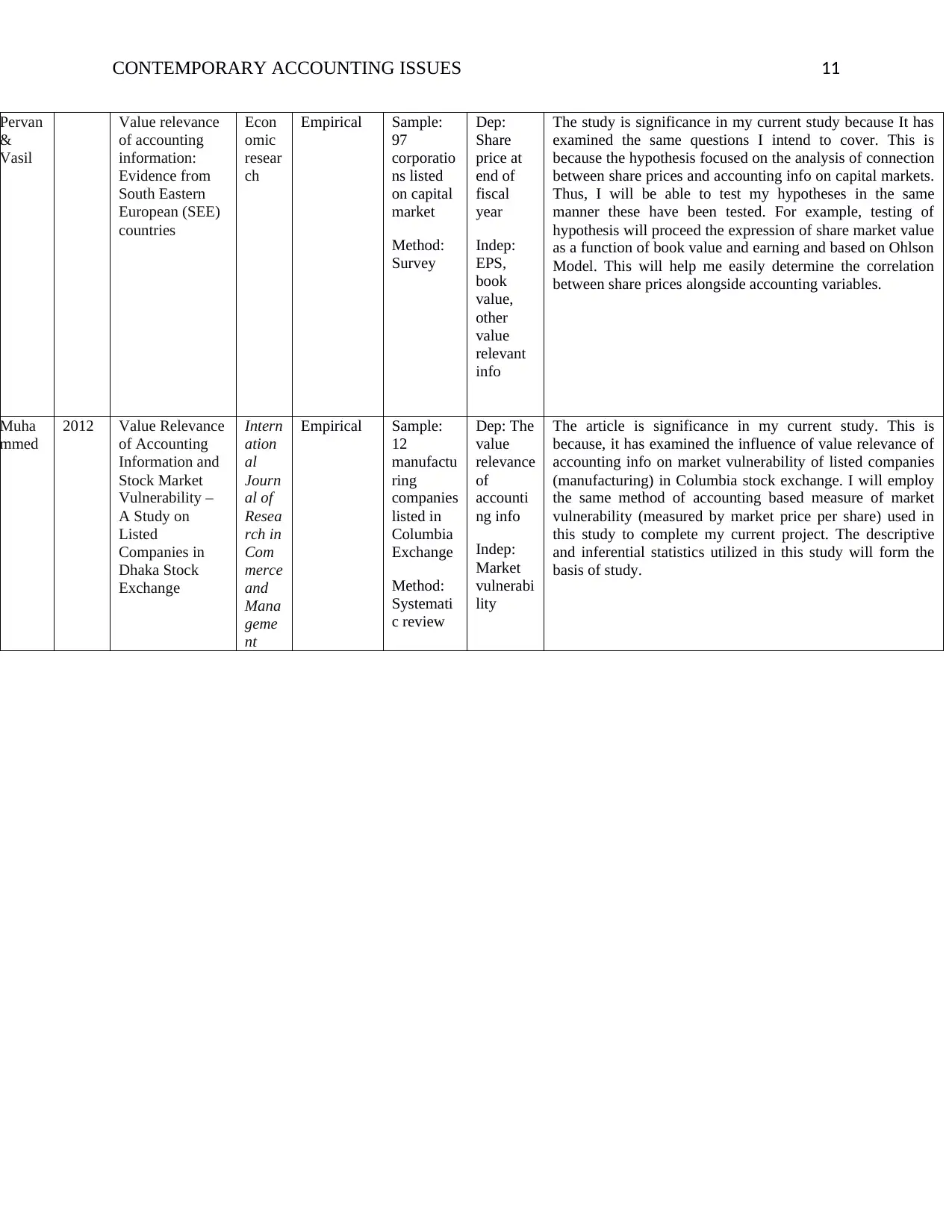

Pervan

&

Vasil

Value relevance

of accounting

information:

Evidence from

South Eastern

European (SEE)

countries

Econ

omic

resear

ch

Empirical Sample:

97

corporatio

ns listed

on capital

market

Method:

Survey

Dep:

Share

price at

end of

fiscal

year

Indep:

EPS,

book

value,

other

value

relevant

info

The study is significance in my current study because It has

examined the same questions I intend to cover. This is

because the hypothesis focused on the analysis of connection

between share prices and accounting info on capital markets.

Thus, I will be able to test my hypotheses in the same

manner these have been tested. For example, testing of

hypothesis will proceed the expression of share market value

as a function of book value and earning and based on Ohlson

Model. This will help me easily determine the correlation

between share prices alongside accounting variables.

Muha

mmed

2012 Value Relevance

of Accounting

Information and

Stock Market

Vulnerability –

A Study on

Listed

Companies in

Dhaka Stock

Exchange

Intern

ation

al

Journ

al of

Resea

rch in

Com

merce

and

Mana

geme

nt

Empirical Sample:

12

manufactu

ring

companies

listed in

Columbia

Exchange

Method:

Systemati

c review

Dep: The

value

relevance

of

accounti

ng info

Indep:

Market

vulnerabi

lity

The article is significance in my current study. This is

because, it has examined the influence of value relevance of

accounting info on market vulnerability of listed companies

(manufacturing) in Columbia stock exchange. I will employ

the same method of accounting based measure of market

vulnerability (measured by market price per share) used in

this study to complete my current project. The descriptive

and inferential statistics utilized in this study will form the

basis of study.

Pervan

&

Vasil

Value relevance

of accounting

information:

Evidence from

South Eastern

European (SEE)

countries

Econ

omic

resear

ch

Empirical Sample:

97

corporatio

ns listed

on capital

market

Method:

Survey

Dep:

Share

price at

end of

fiscal

year

Indep:

EPS,

book

value,

other

value

relevant

info

The study is significance in my current study because It has

examined the same questions I intend to cover. This is

because the hypothesis focused on the analysis of connection

between share prices and accounting info on capital markets.

Thus, I will be able to test my hypotheses in the same

manner these have been tested. For example, testing of

hypothesis will proceed the expression of share market value

as a function of book value and earning and based on Ohlson

Model. This will help me easily determine the correlation

between share prices alongside accounting variables.

Muha

mmed

2012 Value Relevance

of Accounting

Information and

Stock Market

Vulnerability –

A Study on

Listed

Companies in

Dhaka Stock

Exchange

Intern

ation

al

Journ

al of

Resea

rch in

Com

merce

and

Mana

geme

nt

Empirical Sample:

12

manufactu

ring

companies

listed in

Columbia

Exchange

Method:

Systemati

c review

Dep: The

value

relevance

of

accounti

ng info

Indep:

Market

vulnerabi

lity

The article is significance in my current study. This is

because, it has examined the influence of value relevance of

accounting info on market vulnerability of listed companies

(manufacturing) in Columbia stock exchange. I will employ

the same method of accounting based measure of market

vulnerability (measured by market price per share) used in

this study to complete my current project. The descriptive

and inferential statistics utilized in this study will form the

basis of study.

CONTEMPORARY ACCOUNTING ISSUES 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.