Financial Analysis Report: Asset Valuations and Impairments

VerifiedAdded on 2021/05/31

|12

|1801

|133

Report

AI Summary

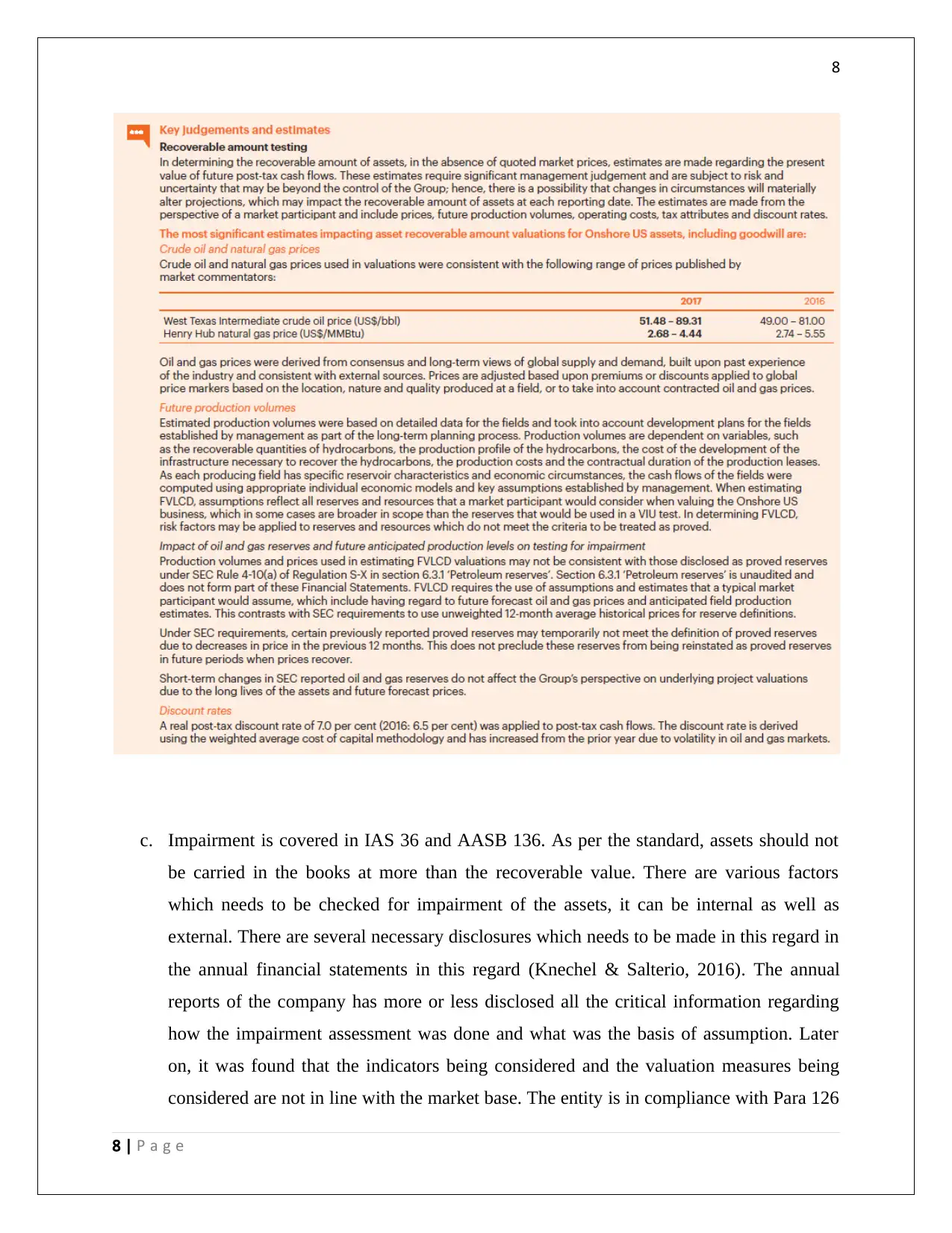

This report provides a comprehensive analysis of accounting treatments related to asset valuations and impairments, focusing on the findings of the ASIC commissioner and the application of accounting standards. The report analyzes the financial reporting of BHP Billiton, a major company in the material and energy sector, and examines its approach to impairment assessment, including the impact of changing market conditions and internal controls. The analysis covers key aspects such as the determination of recoverable value, disclosures, and compliance with accounting standards like IAS 36 and AASB 136. The report highlights the importance of transparency, market-based assumptions, and the role of auditors in ensuring accurate financial reporting. The conclusion emphasizes the company's compliance with disclosure requirements while acknowledging past issues with assumptions and valuations, and it also offers recommendations for improved internal controls and audit procedures.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.