Accounting for Managers Report: Budgeting, Variances, and Decisions

VerifiedAdded on 2020/07/23

|11

|3023

|36

Report

AI Summary

This report, designed for accounting managers, provides a comprehensive overview of key financial concepts and practices. It begins with a detailed analysis of various budgets, including sales, production, direct materials, direct labor, manufacturing overhead, ending finished goods inventory, and cost of goods sold, culminating in a budgeted income statement and cash budget. The report then delves into a case study involving alternative electricity production assets and their cost implications, contrasting the perspectives of managers Rita Aurther and Mr. Paulo on production strategies. Furthermore, the report includes a variance analysis, comparing budgeted versus actual costs for materials and labor, highlighting areas of overspending and underspending, and evaluating the effectiveness of operational performance. The conclusion summarizes the key findings and implications for managerial decision-making within the context of the presented data and scenarios.

Accounting for Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

a) Sales budget........................................................................................................................1

b) Production budget..............................................................................................................1

c) Direct material purchases budget.......................................................................................1

d) Direct labour budget...........................................................................................................2

e) Manufacturing overhead budget.........................................................................................2

f) Ending finished goods inventory budget............................................................................2

g) Cost of goods sold budget..................................................................................................3

h) Budgeted income statement...............................................................................................3

i) Cash budget.........................................................................................................................3

PART B............................................................................................................................................3

PART C ...........................................................................................................................................4

PART D...........................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

a) Sales budget........................................................................................................................1

b) Production budget..............................................................................................................1

c) Direct material purchases budget.......................................................................................1

d) Direct labour budget...........................................................................................................2

e) Manufacturing overhead budget.........................................................................................2

f) Ending finished goods inventory budget............................................................................2

g) Cost of goods sold budget..................................................................................................3

h) Budgeted income statement...............................................................................................3

i) Cash budget.........................................................................................................................3

PART B............................................................................................................................................3

PART C ...........................................................................................................................................4

PART D...........................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

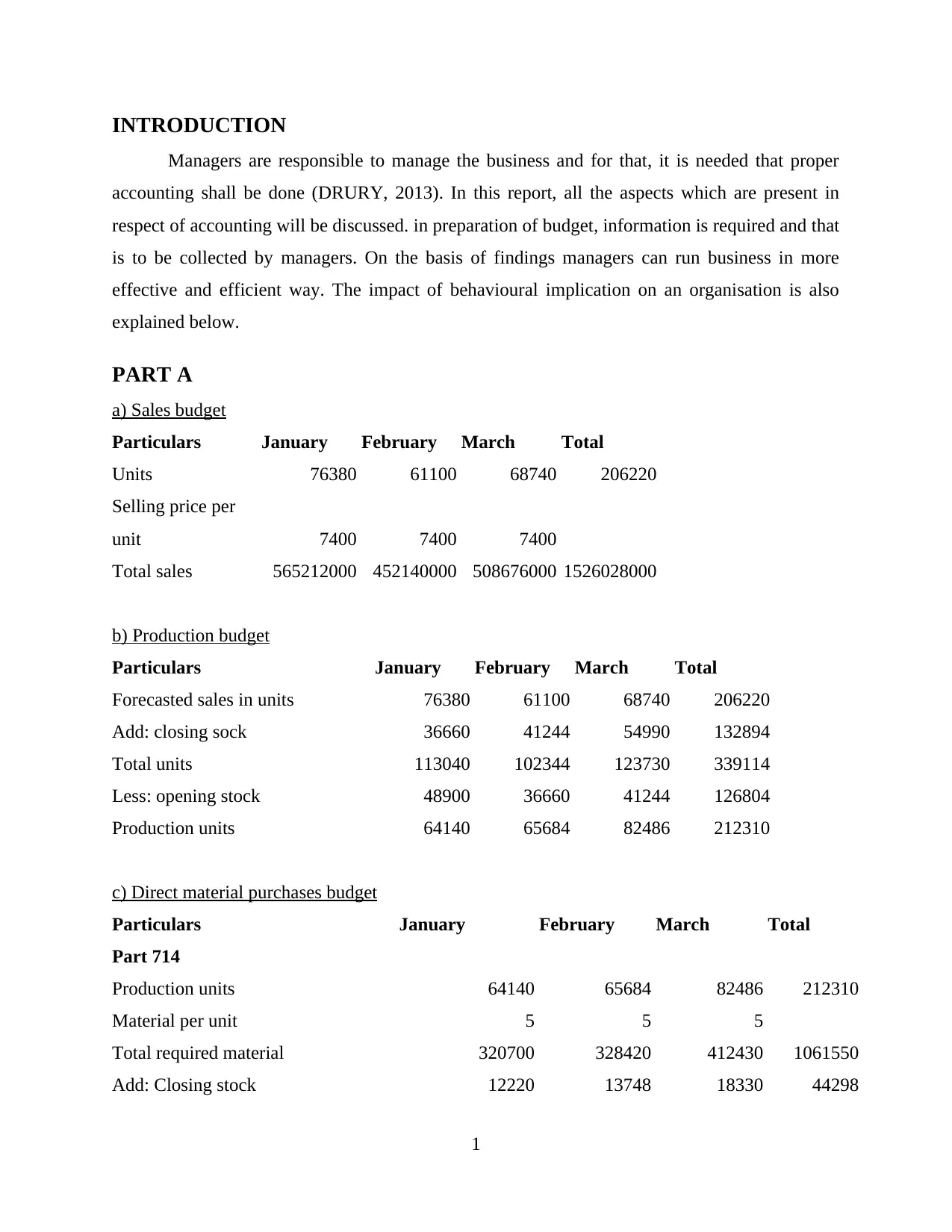

INTRODUCTION

Managers are responsible to manage the business and for that, it is needed that proper

accounting shall be done (DRURY, 2013). In this report, all the aspects which are present in

respect of accounting will be discussed. in preparation of budget, information is required and that

is to be collected by managers. On the basis of findings managers can run business in more

effective and efficient way. The impact of behavioural implication on an organisation is also

explained below.

PART A

a) Sales budget

Particulars January February March Total

Units 76380 61100 68740 206220

Selling price per

unit 7400 7400 7400

Total sales 565212000 452140000 508676000 1526028000

b) Production budget

Particulars January February March Total

Forecasted sales in units 76380 61100 68740 206220

Add: closing sock 36660 41244 54990 132894

Total units 113040 102344 123730 339114

Less: opening stock 48900 36660 41244 126804

Production units 64140 65684 82486 212310

c) Direct material purchases budget

Particulars January February March Total

Part 714

Production units 64140 65684 82486 212310

Material per unit 5 5 5

Total required material 320700 328420 412430 1061550

Add: Closing stock 12220 13748 18330 44298

1

Managers are responsible to manage the business and for that, it is needed that proper

accounting shall be done (DRURY, 2013). In this report, all the aspects which are present in

respect of accounting will be discussed. in preparation of budget, information is required and that

is to be collected by managers. On the basis of findings managers can run business in more

effective and efficient way. The impact of behavioural implication on an organisation is also

explained below.

PART A

a) Sales budget

Particulars January February March Total

Units 76380 61100 68740 206220

Selling price per

unit 7400 7400 7400

Total sales 565212000 452140000 508676000 1526028000

b) Production budget

Particulars January February March Total

Forecasted sales in units 76380 61100 68740 206220

Add: closing sock 36660 41244 54990 132894

Total units 113040 102344 123730 339114

Less: opening stock 48900 36660 41244 126804

Production units 64140 65684 82486 212310

c) Direct material purchases budget

Particulars January February March Total

Part 714

Production units 64140 65684 82486 212310

Material per unit 5 5 5

Total required material 320700 328420 412430 1061550

Add: Closing stock 12220 13748 18330 44298

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

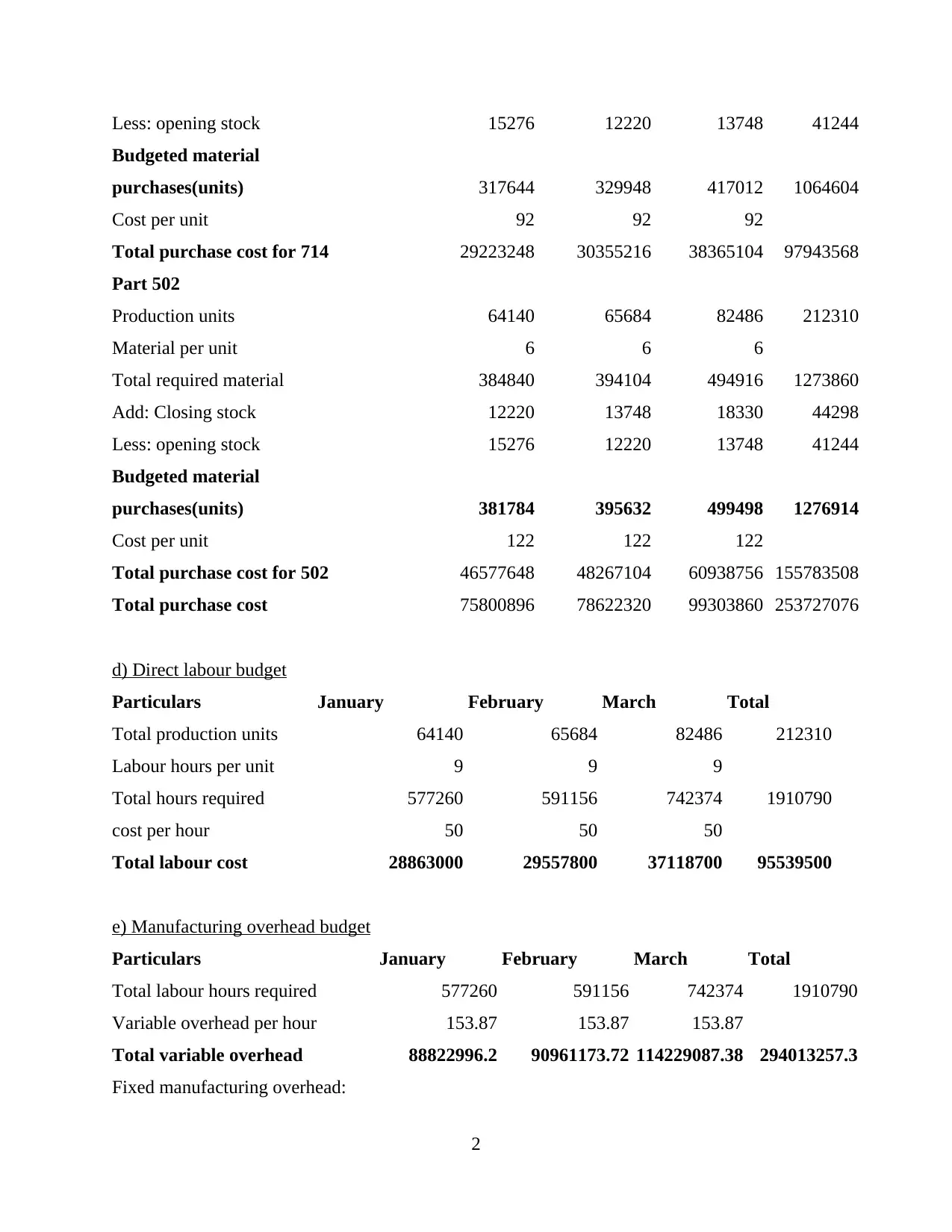

Less: opening stock 15276 12220 13748 41244

Budgeted material

purchases(units) 317644 329948 417012 1064604

Cost per unit 92 92 92

Total purchase cost for 714 29223248 30355216 38365104 97943568

Part 502

Production units 64140 65684 82486 212310

Material per unit 6 6 6

Total required material 384840 394104 494916 1273860

Add: Closing stock 12220 13748 18330 44298

Less: opening stock 15276 12220 13748 41244

Budgeted material

purchases(units) 381784 395632 499498 1276914

Cost per unit 122 122 122

Total purchase cost for 502 46577648 48267104 60938756 155783508

Total purchase cost 75800896 78622320 99303860 253727076

d) Direct labour budget

Particulars January February March Total

Total production units 64140 65684 82486 212310

Labour hours per unit 9 9 9

Total hours required 577260 591156 742374 1910790

cost per hour 50 50 50

Total labour cost 28863000 29557800 37118700 95539500

e) Manufacturing overhead budget

Particulars January February March Total

Total labour hours required 577260 591156 742374 1910790

Variable overhead per hour 153.87 153.87 153.87

Total variable overhead 88822996.2 90961173.72 114229087.38 294013257.3

Fixed manufacturing overhead:

2

Budgeted material

purchases(units) 317644 329948 417012 1064604

Cost per unit 92 92 92

Total purchase cost for 714 29223248 30355216 38365104 97943568

Part 502

Production units 64140 65684 82486 212310

Material per unit 6 6 6

Total required material 384840 394104 494916 1273860

Add: Closing stock 12220 13748 18330 44298

Less: opening stock 15276 12220 13748 41244

Budgeted material

purchases(units) 381784 395632 499498 1276914

Cost per unit 122 122 122

Total purchase cost for 502 46577648 48267104 60938756 155783508

Total purchase cost 75800896 78622320 99303860 253727076

d) Direct labour budget

Particulars January February March Total

Total production units 64140 65684 82486 212310

Labour hours per unit 9 9 9

Total hours required 577260 591156 742374 1910790

cost per hour 50 50 50

Total labour cost 28863000 29557800 37118700 95539500

e) Manufacturing overhead budget

Particulars January February March Total

Total labour hours required 577260 591156 742374 1910790

Variable overhead per hour 153.87 153.87 153.87

Total variable overhead 88822996.2 90961173.72 114229087.38 294013257.3

Fixed manufacturing overhead:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

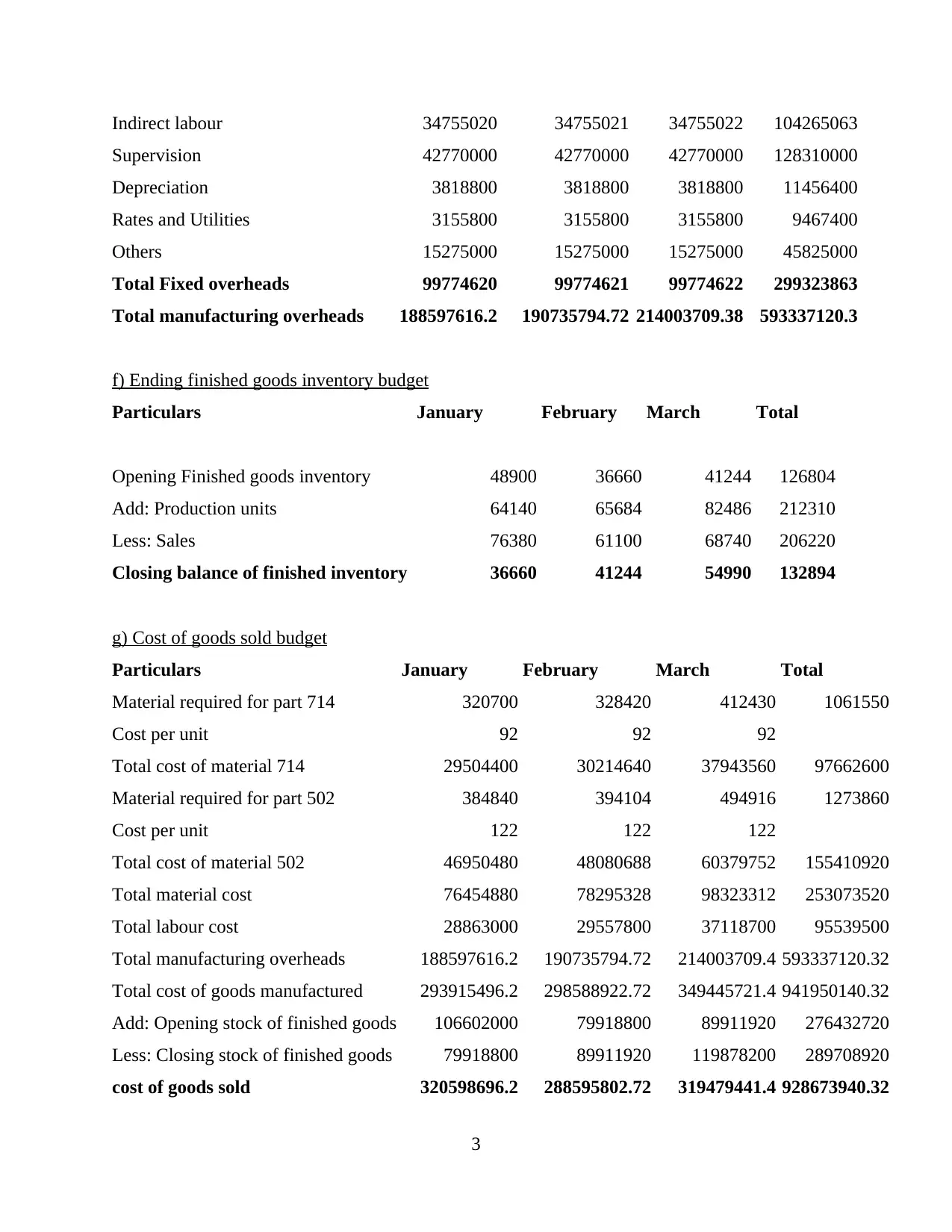

Indirect labour 34755020 34755021 34755022 104265063

Supervision 42770000 42770000 42770000 128310000

Depreciation 3818800 3818800 3818800 11456400

Rates and Utilities 3155800 3155800 3155800 9467400

Others 15275000 15275000 15275000 45825000

Total Fixed overheads 99774620 99774621 99774622 299323863

Total manufacturing overheads 188597616.2 190735794.72 214003709.38 593337120.3

f) Ending finished goods inventory budget

Particulars January February March Total

Opening Finished goods inventory 48900 36660 41244 126804

Add: Production units 64140 65684 82486 212310

Less: Sales 76380 61100 68740 206220

Closing balance of finished inventory 36660 41244 54990 132894

g) Cost of goods sold budget

Particulars January February March Total

Material required for part 714 320700 328420 412430 1061550

Cost per unit 92 92 92

Total cost of material 714 29504400 30214640 37943560 97662600

Material required for part 502 384840 394104 494916 1273860

Cost per unit 122 122 122

Total cost of material 502 46950480 48080688 60379752 155410920

Total material cost 76454880 78295328 98323312 253073520

Total labour cost 28863000 29557800 37118700 95539500

Total manufacturing overheads 188597616.2 190735794.72 214003709.4 593337120.32

Total cost of goods manufactured 293915496.2 298588922.72 349445721.4 941950140.32

Add: Opening stock of finished goods 106602000 79918800 89911920 276432720

Less: Closing stock of finished goods 79918800 89911920 119878200 289708920

cost of goods sold 320598696.2 288595802.72 319479441.4 928673940.32

3

Supervision 42770000 42770000 42770000 128310000

Depreciation 3818800 3818800 3818800 11456400

Rates and Utilities 3155800 3155800 3155800 9467400

Others 15275000 15275000 15275000 45825000

Total Fixed overheads 99774620 99774621 99774622 299323863

Total manufacturing overheads 188597616.2 190735794.72 214003709.38 593337120.3

f) Ending finished goods inventory budget

Particulars January February March Total

Opening Finished goods inventory 48900 36660 41244 126804

Add: Production units 64140 65684 82486 212310

Less: Sales 76380 61100 68740 206220

Closing balance of finished inventory 36660 41244 54990 132894

g) Cost of goods sold budget

Particulars January February March Total

Material required for part 714 320700 328420 412430 1061550

Cost per unit 92 92 92

Total cost of material 714 29504400 30214640 37943560 97662600

Material required for part 502 384840 394104 494916 1273860

Cost per unit 122 122 122

Total cost of material 502 46950480 48080688 60379752 155410920

Total material cost 76454880 78295328 98323312 253073520

Total labour cost 28863000 29557800 37118700 95539500

Total manufacturing overheads 188597616.2 190735794.72 214003709.4 593337120.32

Total cost of goods manufactured 293915496.2 298588922.72 349445721.4 941950140.32

Add: Opening stock of finished goods 106602000 79918800 89911920 276432720

Less: Closing stock of finished goods 79918800 89911920 119878200 289708920

cost of goods sold 320598696.2 288595802.72 319479441.4 928673940.32

3

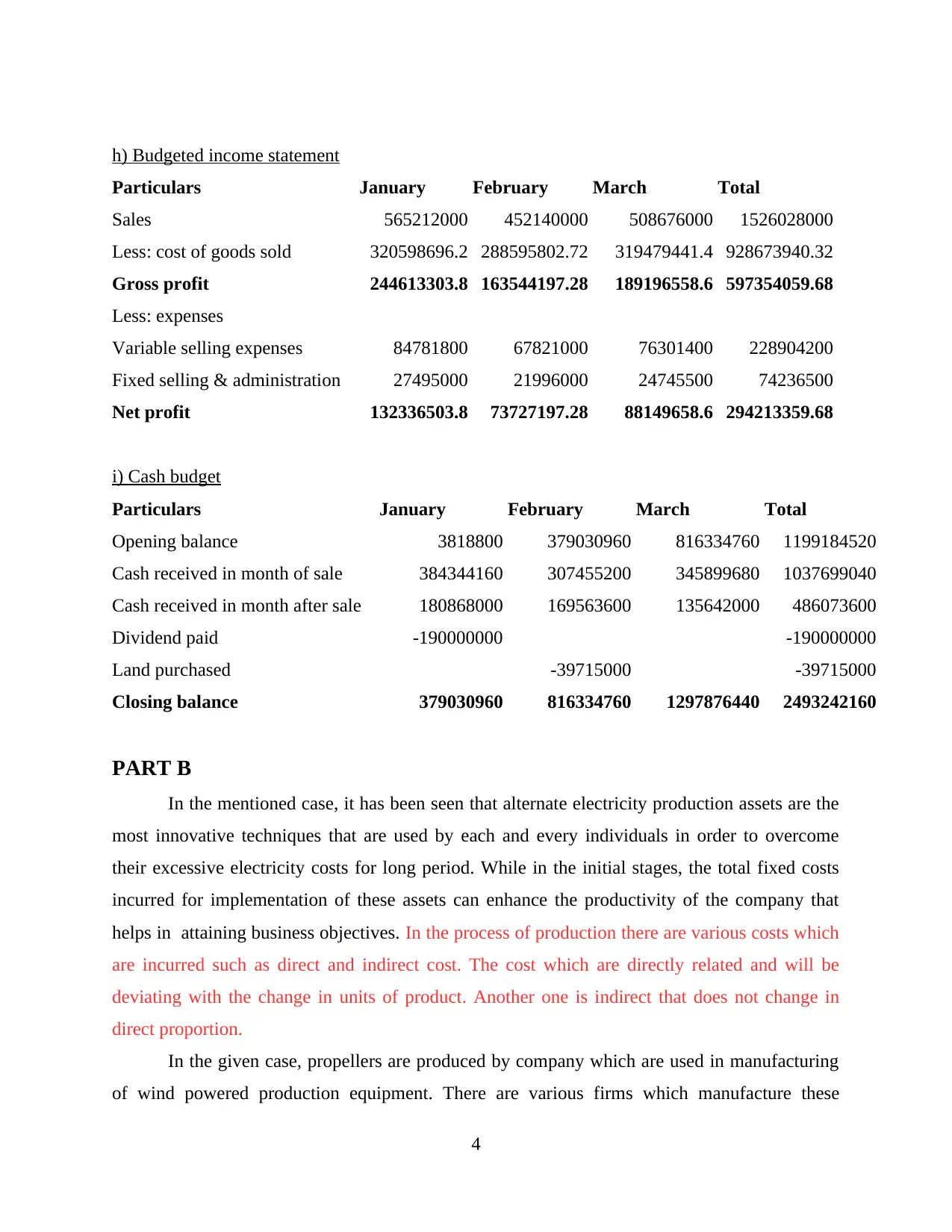

h) Budgeted income statement

Particulars January February March Total

Sales 565212000 452140000 508676000 1526028000

Less: cost of goods sold 320598696.2 288595802.72 319479441.4 928673940.32

Gross profit 244613303.8 163544197.28 189196558.6 597354059.68

Less: expenses

Variable selling expenses 84781800 67821000 76301400 228904200

Fixed selling & administration 27495000 21996000 24745500 74236500

Net profit 132336503.8 73727197.28 88149658.6 294213359.68

i) Cash budget

Particulars January February March Total

Opening balance 3818800 379030960 816334760 1199184520

Cash received in month of sale 384344160 307455200 345899680 1037699040

Cash received in month after sale 180868000 169563600 135642000 486073600

Dividend paid -190000000 -190000000

Land purchased -39715000 -39715000

Closing balance 379030960 816334760 1297876440 2493242160

PART B

In the mentioned case, it has been seen that alternate electricity production assets are the

most innovative techniques that are used by each and every individuals in order to overcome

their excessive electricity costs for long period. While in the initial stages, the total fixed costs

incurred for implementation of these assets can enhance the productivity of the company that

helps in attaining business objectives. In the process of production there are various costs which

are incurred such as direct and indirect cost. The cost which are directly related and will be

deviating with the change in units of product. Another one is indirect that does not change in

direct proportion.

In the given case, propellers are produced by company which are used in manufacturing

of wind powered production equipment. There are various firms which manufacture these

4

Particulars January February March Total

Sales 565212000 452140000 508676000 1526028000

Less: cost of goods sold 320598696.2 288595802.72 319479441.4 928673940.32

Gross profit 244613303.8 163544197.28 189196558.6 597354059.68

Less: expenses

Variable selling expenses 84781800 67821000 76301400 228904200

Fixed selling & administration 27495000 21996000 24745500 74236500

Net profit 132336503.8 73727197.28 88149658.6 294213359.68

i) Cash budget

Particulars January February March Total

Opening balance 3818800 379030960 816334760 1199184520

Cash received in month of sale 384344160 307455200 345899680 1037699040

Cash received in month after sale 180868000 169563600 135642000 486073600

Dividend paid -190000000 -190000000

Land purchased -39715000 -39715000

Closing balance 379030960 816334760 1297876440 2493242160

PART B

In the mentioned case, it has been seen that alternate electricity production assets are the

most innovative techniques that are used by each and every individuals in order to overcome

their excessive electricity costs for long period. While in the initial stages, the total fixed costs

incurred for implementation of these assets can enhance the productivity of the company that

helps in attaining business objectives. In the process of production there are various costs which

are incurred such as direct and indirect cost. The cost which are directly related and will be

deviating with the change in units of product. Another one is indirect that does not change in

direct proportion.

In the given case, propellers are produced by company which are used in manufacturing

of wind powered production equipment. There are various firms which manufacture these

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generators and so, company supplies its units to them (Nobes and Stadler, 2015). The sales

manager of company, Rita Aurther, is worried as some elections are going to be conducted and

there is possibility that the new government which will be framed can eliminate the wind-

generated division. Another major issue of her concern is that there are chances that market

which is present for alternate equipment may come to an end. Due to all these issues, she is

highly insecure about the company. There are chances that losses will be incurred because of it.

This is because if new product is introduced in market then competition will increase and in

order to deal with that various factors are to be analysed by the manager so that issues regarding

which she is concerned can be dealt in most appropriate manner.

On the other hand, Mr Paulo is there who wants to include advanced production services

in their business and for that, various plans are being made. By the introduction of this, all

operations will be carried out effectively and efficiently. With the help of this, they will be able

to carry out in house production. In this, assembling is purchased and in current state, the work is

carried out by labour and after making the process automatic, this problem can be resolved. All

the costs which are incurred for material and labour will be restricted by the automatic process

which is more effective. Thus, the cost related to them is saved and this is reduced by 25 percent

as material and labour are direct cost so as the production will be changing this will also deviate.

In spite of this, increase is noticed in relation to fixed production overheads up to 50 percent and

this is not considered to be a positive factor for business. The main reason which is identified for

this is increased production capacity. As the project is initially started so, the fixed cost is

increased and there are many benefits which will be received by business as cost related to

material and labour is decreased through the same. This will make the business more profitable

and also, effectiveness can be gained because of this that provides long term benefits. By the

analysation of cost it is possible for rita and Paulo to take the decisions as they will choose that

method in which cost will be minimised and profits are increased. In process of decisions only

those cost which are variable or direct are to be taken into consideration as they are ones that

affect the profits. Fixed cost remains same so that is not considered. In the given case the

decision of Paulo is right as by that material and labour cost are declining which is a good factor

and the fact that manufacturing expenses are increased is for one time as they are fixed and are

incurred for initial installation but after that they will remain at same level. So as the production

5

manager of company, Rita Aurther, is worried as some elections are going to be conducted and

there is possibility that the new government which will be framed can eliminate the wind-

generated division. Another major issue of her concern is that there are chances that market

which is present for alternate equipment may come to an end. Due to all these issues, she is

highly insecure about the company. There are chances that losses will be incurred because of it.

This is because if new product is introduced in market then competition will increase and in

order to deal with that various factors are to be analysed by the manager so that issues regarding

which she is concerned can be dealt in most appropriate manner.

On the other hand, Mr Paulo is there who wants to include advanced production services

in their business and for that, various plans are being made. By the introduction of this, all

operations will be carried out effectively and efficiently. With the help of this, they will be able

to carry out in house production. In this, assembling is purchased and in current state, the work is

carried out by labour and after making the process automatic, this problem can be resolved. All

the costs which are incurred for material and labour will be restricted by the automatic process

which is more effective. Thus, the cost related to them is saved and this is reduced by 25 percent

as material and labour are direct cost so as the production will be changing this will also deviate.

In spite of this, increase is noticed in relation to fixed production overheads up to 50 percent and

this is not considered to be a positive factor for business. The main reason which is identified for

this is increased production capacity. As the project is initially started so, the fixed cost is

increased and there are many benefits which will be received by business as cost related to

material and labour is decreased through the same. This will make the business more profitable

and also, effectiveness can be gained because of this that provides long term benefits. By the

analysation of cost it is possible for rita and Paulo to take the decisions as they will choose that

method in which cost will be minimised and profits are increased. In process of decisions only

those cost which are variable or direct are to be taken into consideration as they are ones that

affect the profits. Fixed cost remains same so that is not considered. In the given case the

decision of Paulo is right as by that material and labour cost are declining which is a good factor

and the fact that manufacturing expenses are increased is for one time as they are fixed and are

incurred for initial installation but after that they will remain at same level. So as the production

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will increase the saving will also increase which is good aspect for coming period in which there

are chances of new competitors coming in market.

PART C

In business, there are various tools which can be used for the purpose of increasing

effectiveness. In given situations, budgets are made in which all the expenses and incomes are

estimated on the basis of past data and other relevant aspects which are there in relation to

coming period. With the help of them, it is possible to manage all the transactions in an

appropriate manner as limit of them is already specified. In the budgets which are made above

along with the actual figures, there are certain deviations which are noted. So, in order to draw

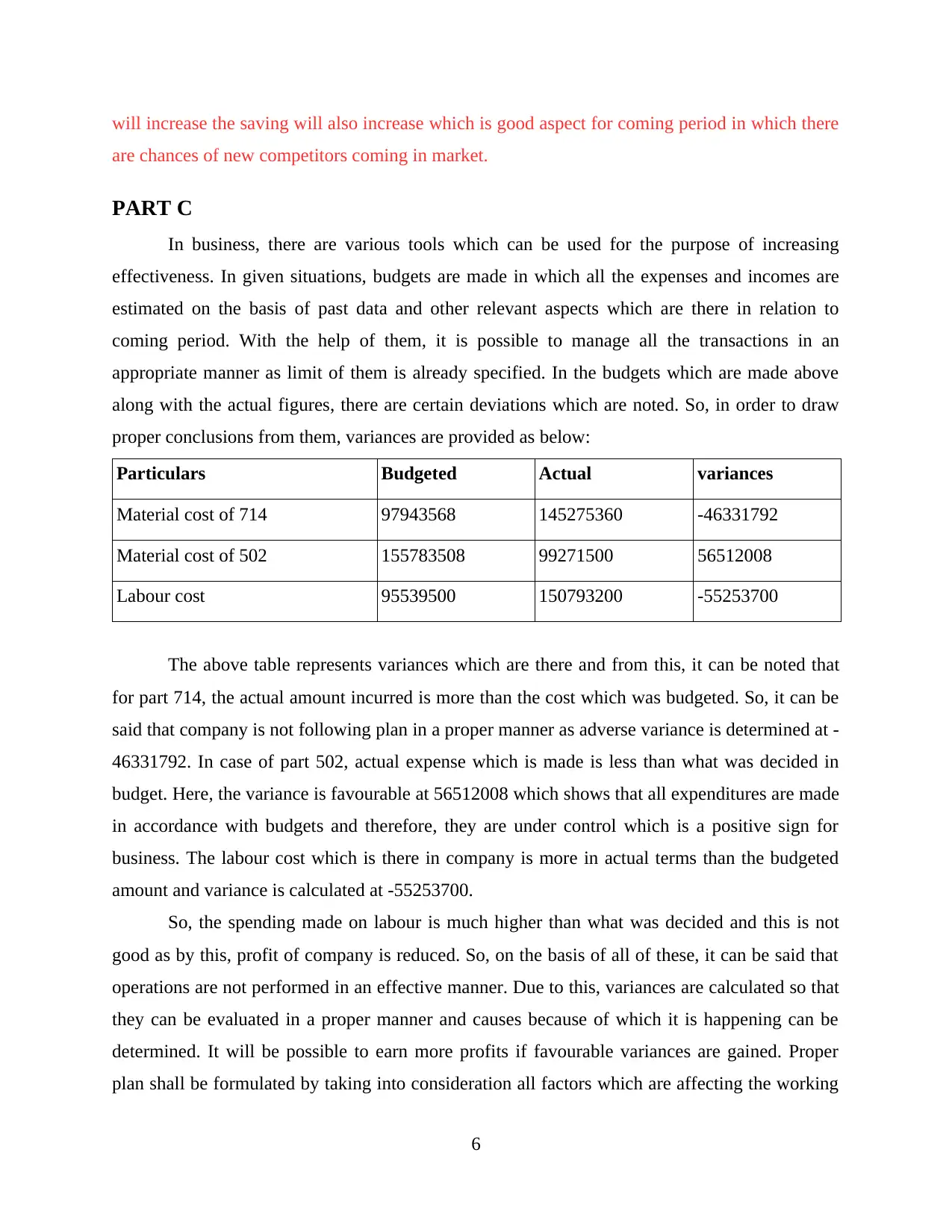

proper conclusions from them, variances are provided as below:

Particulars Budgeted Actual variances

Material cost of 714 97943568 145275360 -46331792

Material cost of 502 155783508 99271500 56512008

Labour cost 95539500 150793200 -55253700

The above table represents variances which are there and from this, it can be noted that

for part 714, the actual amount incurred is more than the cost which was budgeted. So, it can be

said that company is not following plan in a proper manner as adverse variance is determined at -

46331792. In case of part 502, actual expense which is made is less than what was decided in

budget. Here, the variance is favourable at 56512008 which shows that all expenditures are made

in accordance with budgets and therefore, they are under control which is a positive sign for

business. The labour cost which is there in company is more in actual terms than the budgeted

amount and variance is calculated at -55253700.

So, the spending made on labour is much higher than what was decided and this is not

good as by this, profit of company is reduced. So, on the basis of all of these, it can be said that

operations are not performed in an effective manner. Due to this, variances are calculated so that

they can be evaluated in a proper manner and causes because of which it is happening can be

determined. It will be possible to earn more profits if favourable variances are gained. Proper

plan shall be formulated by taking into consideration all factors which are affecting the working

6

are chances of new competitors coming in market.

PART C

In business, there are various tools which can be used for the purpose of increasing

effectiveness. In given situations, budgets are made in which all the expenses and incomes are

estimated on the basis of past data and other relevant aspects which are there in relation to

coming period. With the help of them, it is possible to manage all the transactions in an

appropriate manner as limit of them is already specified. In the budgets which are made above

along with the actual figures, there are certain deviations which are noted. So, in order to draw

proper conclusions from them, variances are provided as below:

Particulars Budgeted Actual variances

Material cost of 714 97943568 145275360 -46331792

Material cost of 502 155783508 99271500 56512008

Labour cost 95539500 150793200 -55253700

The above table represents variances which are there and from this, it can be noted that

for part 714, the actual amount incurred is more than the cost which was budgeted. So, it can be

said that company is not following plan in a proper manner as adverse variance is determined at -

46331792. In case of part 502, actual expense which is made is less than what was decided in

budget. Here, the variance is favourable at 56512008 which shows that all expenditures are made

in accordance with budgets and therefore, they are under control which is a positive sign for

business. The labour cost which is there in company is more in actual terms than the budgeted

amount and variance is calculated at -55253700.

So, the spending made on labour is much higher than what was decided and this is not

good as by this, profit of company is reduced. So, on the basis of all of these, it can be said that

operations are not performed in an effective manner. Due to this, variances are calculated so that

they can be evaluated in a proper manner and causes because of which it is happening can be

determined. It will be possible to earn more profits if favourable variances are gained. Proper

plan shall be formulated by taking into consideration all factors which are affecting the working

6

of business. In this, various tools are to be used by which variables which affect the functioning

are analysed and controlled. By undertaking all of them, it is possible for business to improve its

position and this will lead to bring improvements in the coming period.

7

are analysed and controlled. By undertaking all of them, it is possible for business to improve its

position and this will lead to bring improvements in the coming period.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART D

The implications of behavioural impacts on business organization

The manner in which employees of an organizations work is different from their attitude

and behaviour that is followed in a social environment. There are different factors which

influence an organizations behaviour (Collier, 2015). It mainly consists of various structure,

policies and regulations along with other aspects which are present in the business. All these

things can motivate the employees to work according to their strengths and contribute maximum

to company. It will be more effective as they are getting more accurate and reliable data in order

to achieve higher productivity and competitiveness.

The reason behind all those impacts is lazy working ability of employees as they do not

take interest in their work. The behavioural implications of accounting system are very much

new that clarifies the role, management control and tendency of employees to be lazy and

hampering resources as categorized in the business. Company needs to prepare an effective

budget that will be able to convert the goals and objectives of and organization into valuable

data. Budgets are said to be one of the most effective aspects of decision making for any

company. It is simply a blueprint for making management strategies and plan.

With the help of budgets, most of the operations which are performed by company during

the coming year are determined and controlled. Performance of an individual as well as company

is analysed through use of actual budget with the standards (An Introduction to Business

Accounting for Managers, 2017). The budgets help managers to reach at a destination through

moving from starting point to set objectives. Some of the planning control measures a company's

management follow are:

I) An imposed budget approach: It refers to those budgets which are formulated by the

top management with few resources and no other inputs from the operating personnel are

used. It is mainly considered as Top- Down budgeting. It is based on estimating the cost

of maximum level activities at the first and using these information to constrain the

estimate of lower activities.

Advantages:

It takes less time to formulate and determine the results from the particular budgets.

1

The implications of behavioural impacts on business organization

The manner in which employees of an organizations work is different from their attitude

and behaviour that is followed in a social environment. There are different factors which

influence an organizations behaviour (Collier, 2015). It mainly consists of various structure,

policies and regulations along with other aspects which are present in the business. All these

things can motivate the employees to work according to their strengths and contribute maximum

to company. It will be more effective as they are getting more accurate and reliable data in order

to achieve higher productivity and competitiveness.

The reason behind all those impacts is lazy working ability of employees as they do not

take interest in their work. The behavioural implications of accounting system are very much

new that clarifies the role, management control and tendency of employees to be lazy and

hampering resources as categorized in the business. Company needs to prepare an effective

budget that will be able to convert the goals and objectives of and organization into valuable

data. Budgets are said to be one of the most effective aspects of decision making for any

company. It is simply a blueprint for making management strategies and plan.

With the help of budgets, most of the operations which are performed by company during

the coming year are determined and controlled. Performance of an individual as well as company

is analysed through use of actual budget with the standards (An Introduction to Business

Accounting for Managers, 2017). The budgets help managers to reach at a destination through

moving from starting point to set objectives. Some of the planning control measures a company's

management follow are:

I) An imposed budget approach: It refers to those budgets which are formulated by the

top management with few resources and no other inputs from the operating personnel are

used. It is mainly considered as Top- Down budgeting. It is based on estimating the cost

of maximum level activities at the first and using these information to constrain the

estimate of lower activities.

Advantages:

It takes less time to formulate and determine the results from the particular budgets.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It will be helpful in addressing objectives of an organization which are making maximum

impact on the profitability of company.

ii) A participative budgets approach: Under this process, the manner in which funds shall

be used for growth of business is decided (Ahmed and Duellman, 2013). Here various

budgets are prepared such as municipal and capital budgets. These types of budgets are

called as bottom - up which works from lower level of management to higher level.

Advantages:They help in increasing the level of motivation among employees.

It helps to develop better communication among various departments.

The senior managers are required to concentrate on the plan and strategies that are made

in order to attain objectives.

CONCLUSION

From the above mentioned report, it can be concluded that by use of budgets, all

operations can be carried out in the most profitable manner and results are used to draw

interpretations. It has also been identified that there are various ways in which accounting is to

be done by managers and this will help them in making the decisions for betterment of business.

1

impact on the profitability of company.

ii) A participative budgets approach: Under this process, the manner in which funds shall

be used for growth of business is decided (Ahmed and Duellman, 2013). Here various

budgets are prepared such as municipal and capital budgets. These types of budgets are

called as bottom - up which works from lower level of management to higher level.

Advantages:They help in increasing the level of motivation among employees.

It helps to develop better communication among various departments.

The senior managers are required to concentrate on the plan and strategies that are made

in order to attain objectives.

CONCLUSION

From the above mentioned report, it can be concluded that by use of budgets, all

operations can be carried out in the most profitable manner and results are used to draw

interpretations. It has also been identified that there are various ways in which accounting is to

be done by managers and this will help them in making the decisions for betterment of business.

1

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.