Accounting Skills Assignment: Financial Analysis and Variance Analysis

VerifiedAdded on 2023/06/10

|20

|3947

|124

Homework Assignment

AI Summary

This accounting assignment comprehensively addresses key accounting principles and practices. It begins with journalizing transactions and posting them to ledger accounts for Phoenix Inc., followed by an analysis of bookkeeping versus accounting. The assignment then delves into preparing income statements and balance sheets for Indus Corp, emphasizing the importance of financial statements for business decision-making. A cash budget is created for ABC Industries, alongside an explanation of zero-based budgeting. The final section focuses on variance analysis, calculating direct material and labor variances, as well as overhead variances, providing a thorough understanding of cost control and performance evaluation. The assignment covers a wide range of accounting concepts, including financial statement preparation, budgeting, and variance analysis.

Running head: ACCOUNTING SKILLS

Accounting Skills

Name of the Student:

Name of the University:

Author’s Note:

Accounting Skills

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING SKILLS

Table of Contents

Answer to Question 1:.....................................................................................................................3

Requirement A:............................................................................................................................3

i) Journal Entries:.................................................................................................................3

ii) General Ledger:.............................................................................................................4

Requirement B:............................................................................................................................5

Answer to Question 2:.....................................................................................................................6

Requirement A:............................................................................................................................6

Requirement B:............................................................................................................................7

Answer to Question 3:.....................................................................................................................9

Requirement A:............................................................................................................................9

Requirement B:..........................................................................................................................10

Answer to Question 4:...................................................................................................................11

Requirement A:..........................................................................................................................11

Requirement A.i:....................................................................................................................11

Requirement A.ii:..................................................................................................................13

Requirement A.iii:.................................................................................................................14

Requirement B:..........................................................................................................................14

Answer to Question 5:...................................................................................................................15

Requirement A:..........................................................................................................................15

Table of Contents

Answer to Question 1:.....................................................................................................................3

Requirement A:............................................................................................................................3

i) Journal Entries:.................................................................................................................3

ii) General Ledger:.............................................................................................................4

Requirement B:............................................................................................................................5

Answer to Question 2:.....................................................................................................................6

Requirement A:............................................................................................................................6

Requirement B:............................................................................................................................7

Answer to Question 3:.....................................................................................................................9

Requirement A:............................................................................................................................9

Requirement B:..........................................................................................................................10

Answer to Question 4:...................................................................................................................11

Requirement A:..........................................................................................................................11

Requirement A.i:....................................................................................................................11

Requirement A.ii:..................................................................................................................13

Requirement A.iii:.................................................................................................................14

Requirement B:..........................................................................................................................14

Answer to Question 5:...................................................................................................................15

Requirement A:..........................................................................................................................15

2ACCOUNTING SKILLS

Requirement B:..........................................................................................................................15

Answer to Question 6:...................................................................................................................16

Requirement A:..........................................................................................................................16

Requirement B:..........................................................................................................................16

Requirement C:..........................................................................................................................16

Reference.......................................................................................................................................18

Requirement B:..........................................................................................................................15

Answer to Question 6:...................................................................................................................16

Requirement A:..........................................................................................................................16

Requirement B:..........................................................................................................................16

Requirement C:..........................................................................................................................16

Reference.......................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING SKILLS

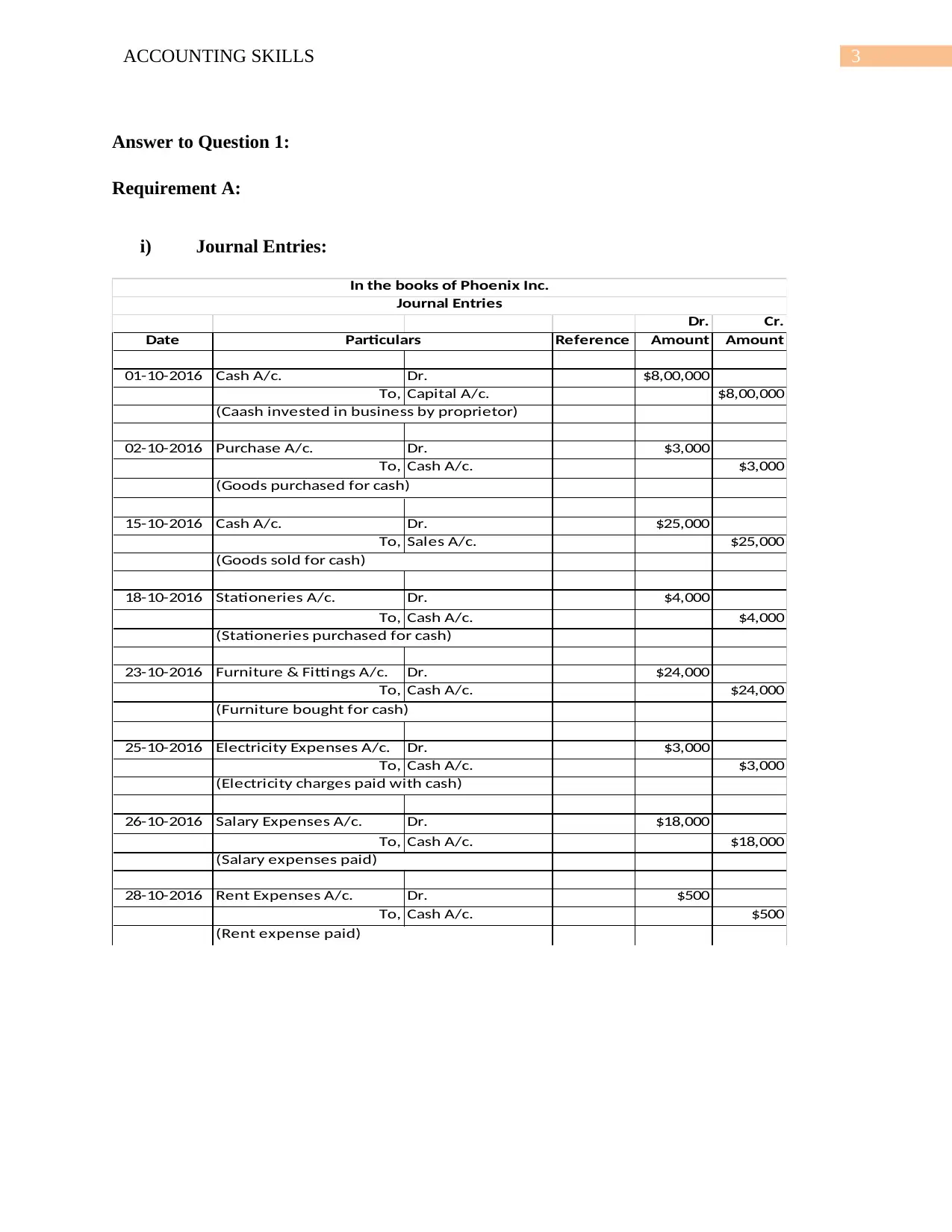

Answer to Question 1:

Requirement A:

i) Journal Entries:

Dr. Cr.

Date Reference Amount Amount

01-10-2016 Cash A/c. Dr. $8,00,000

To, Capital A/c. $8,00,000

02-10-2016 Purchase A/c. Dr. $3,000

To, Cash A/c. $3,000

15-10-2016 Cash A/c. Dr. $25,000

To, Sales A/c. $25,000

18-10-2016 Stationeries A/c. Dr. $4,000

To, Cash A/c. $4,000

23-10-2016 Furniture & Fittings A/c. Dr. $24,000

To, Cash A/c. $24,000

25-10-2016 Electricity Expenses A/c. Dr. $3,000

To, Cash A/c. $3,000

26-10-2016 Salary Expenses A/c. Dr. $18,000

To, Cash A/c. $18,000

28-10-2016 Rent Expenses A/c. Dr. $500

To, Cash A/c. $500

(Stationeries purchased for cash)

(Furniture bought for cash)

(Electricity charges paid with cash)

(Salary expenses paid)

(Rent expense paid)

Particulars

In the books of Phoenix Inc.

Journal Entries

(Caash invested in business by proprietor)

(Goods purchased for cash)

(Goods sold for cash)

Answer to Question 1:

Requirement A:

i) Journal Entries:

Dr. Cr.

Date Reference Amount Amount

01-10-2016 Cash A/c. Dr. $8,00,000

To, Capital A/c. $8,00,000

02-10-2016 Purchase A/c. Dr. $3,000

To, Cash A/c. $3,000

15-10-2016 Cash A/c. Dr. $25,000

To, Sales A/c. $25,000

18-10-2016 Stationeries A/c. Dr. $4,000

To, Cash A/c. $4,000

23-10-2016 Furniture & Fittings A/c. Dr. $24,000

To, Cash A/c. $24,000

25-10-2016 Electricity Expenses A/c. Dr. $3,000

To, Cash A/c. $3,000

26-10-2016 Salary Expenses A/c. Dr. $18,000

To, Cash A/c. $18,000

28-10-2016 Rent Expenses A/c. Dr. $500

To, Cash A/c. $500

(Stationeries purchased for cash)

(Furniture bought for cash)

(Electricity charges paid with cash)

(Salary expenses paid)

(Rent expense paid)

Particulars

In the books of Phoenix Inc.

Journal Entries

(Caash invested in business by proprietor)

(Goods purchased for cash)

(Goods sold for cash)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING SKILLS

ii) General Ledger:

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

01-10-2016 To, Capital A/c. $8,00,000 02-10-2016 By, Purchase A/c. $3,000

15-10-2016 To, Sales A/c. $25,000 18-10-2016 By, Stationeries A/c. $4,000

23-10-2016 By, Furniture & Fittings A/c. $24,000

25-10-2016 By, Electricity Expenses A/c. $3,000

26-10-2016 By, Salary Expenses A/c. $18,000

28-10-2016 By, Rent Expenses A/c. $500

31-10-2016 By, Balance c/d $7,72,500

$8,25,000 $8,25,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

02-10-2016 To, Cash A/c. $3,000 31-10-2016 By, Balance c/d $3,000

$3,000 $3,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

18-10-2016 To, Cash A/c. $4,000 31-10-2016 By, Balance c/d $4,000

$4,000 $4,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $24,000 31-10-2016 By, Balance c/d $24,000

$24,000 $24,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $3,000 31-10-2016 By, Balance c/d $3,000

$3,000 $3,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $18,000 31-10-2016 By, Balance c/d $18,000

$18,000 $18,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $500 31-10-2016 By, Balance c/d $500

$500 $500

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

31-10-2016 To, Balance c/d $8,00,000 01-10-2016 By, Cash A/c. $8,00,000

$8,00,000 $8,00,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

31-10-2016 To, Balance c/d $25,000 01-10-2016 By, Cash A/c. $25,000

$25,000 $25,000

Salary Expenses A/c.

Rent Expenses A/c.

Capital A/c.

Sales A/c.

Cash A/c.

Purchase A/c.

Stationeries A/c.

Furniture & Fittings A/c.

Electricity Expenses A/c.

ii) General Ledger:

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

01-10-2016 To, Capital A/c. $8,00,000 02-10-2016 By, Purchase A/c. $3,000

15-10-2016 To, Sales A/c. $25,000 18-10-2016 By, Stationeries A/c. $4,000

23-10-2016 By, Furniture & Fittings A/c. $24,000

25-10-2016 By, Electricity Expenses A/c. $3,000

26-10-2016 By, Salary Expenses A/c. $18,000

28-10-2016 By, Rent Expenses A/c. $500

31-10-2016 By, Balance c/d $7,72,500

$8,25,000 $8,25,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

02-10-2016 To, Cash A/c. $3,000 31-10-2016 By, Balance c/d $3,000

$3,000 $3,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

18-10-2016 To, Cash A/c. $4,000 31-10-2016 By, Balance c/d $4,000

$4,000 $4,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $24,000 31-10-2016 By, Balance c/d $24,000

$24,000 $24,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $3,000 31-10-2016 By, Balance c/d $3,000

$3,000 $3,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $18,000 31-10-2016 By, Balance c/d $18,000

$18,000 $18,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

23-10-2016 To, Cash A/c. $500 31-10-2016 By, Balance c/d $500

$500 $500

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

31-10-2016 To, Balance c/d $8,00,000 01-10-2016 By, Cash A/c. $8,00,000

$8,00,000 $8,00,000

Dr. Cr.

Date Particulars Ref Amount Date Particulars Ref Amount

31-10-2016 To, Balance c/d $25,000 01-10-2016 By, Cash A/c. $25,000

$25,000 $25,000

Salary Expenses A/c.

Rent Expenses A/c.

Capital A/c.

Sales A/c.

Cash A/c.

Purchase A/c.

Stationeries A/c.

Furniture & Fittings A/c.

Electricity Expenses A/c.

5ACCOUNTING SKILLS

Requirement B:

Book Keeping is an essential part of the accounting process where in various accounting

transactions are recorded in ledgers accounts. The ledger accounts provide the account balances,

required for the preparation of various financial statements (Sangster 2015). The purpose of

accounting is to summarise financial information and interpretation of the same. Information

which generated in reports and interpreted are done by using accounting information which is

provided in the database of records which is created in book keeping process. The process of

book keeping can be described as the recording of various business transactions during a

particular year as per the accounting guidelines (Edwards 2013). On the other hand, the role of

accounting goes beyond the role of book keeping as they have to classify, summarise and present

the accounting information which is extracted from book keeping records. Thus, it can be said

that the process of book keeping forms a part of the overall accounting process. Therefore, it is

clear that the field of accounting is much wider than the field of Book Keeping.

Book keeping involves recording transactions which the business is involved in during a

particular period in a journal or ledger account (Ijiri 2014). The process of book keeping does not

follow any accounting regulations or standards and does not involve any skills or specialised

knowledge for the same. On the other hand, accounting starts from the point where book keeping

process ends. The transactions are posted into respective accounts as per double entry system and

accounting standards and principles are followed for the purpose of treating various transactions

and bring about presentability of the accounting information. Therefore, book keeping process

forms a part of the accounting process of the business.

Requirement B:

Book Keeping is an essential part of the accounting process where in various accounting

transactions are recorded in ledgers accounts. The ledger accounts provide the account balances,

required for the preparation of various financial statements (Sangster 2015). The purpose of

accounting is to summarise financial information and interpretation of the same. Information

which generated in reports and interpreted are done by using accounting information which is

provided in the database of records which is created in book keeping process. The process of

book keeping can be described as the recording of various business transactions during a

particular year as per the accounting guidelines (Edwards 2013). On the other hand, the role of

accounting goes beyond the role of book keeping as they have to classify, summarise and present

the accounting information which is extracted from book keeping records. Thus, it can be said

that the process of book keeping forms a part of the overall accounting process. Therefore, it is

clear that the field of accounting is much wider than the field of Book Keeping.

Book keeping involves recording transactions which the business is involved in during a

particular period in a journal or ledger account (Ijiri 2014). The process of book keeping does not

follow any accounting regulations or standards and does not involve any skills or specialised

knowledge for the same. On the other hand, accounting starts from the point where book keeping

process ends. The transactions are posted into respective accounts as per double entry system and

accounting standards and principles are followed for the purpose of treating various transactions

and bring about presentability of the accounting information. Therefore, book keeping process

forms a part of the accounting process of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING SKILLS

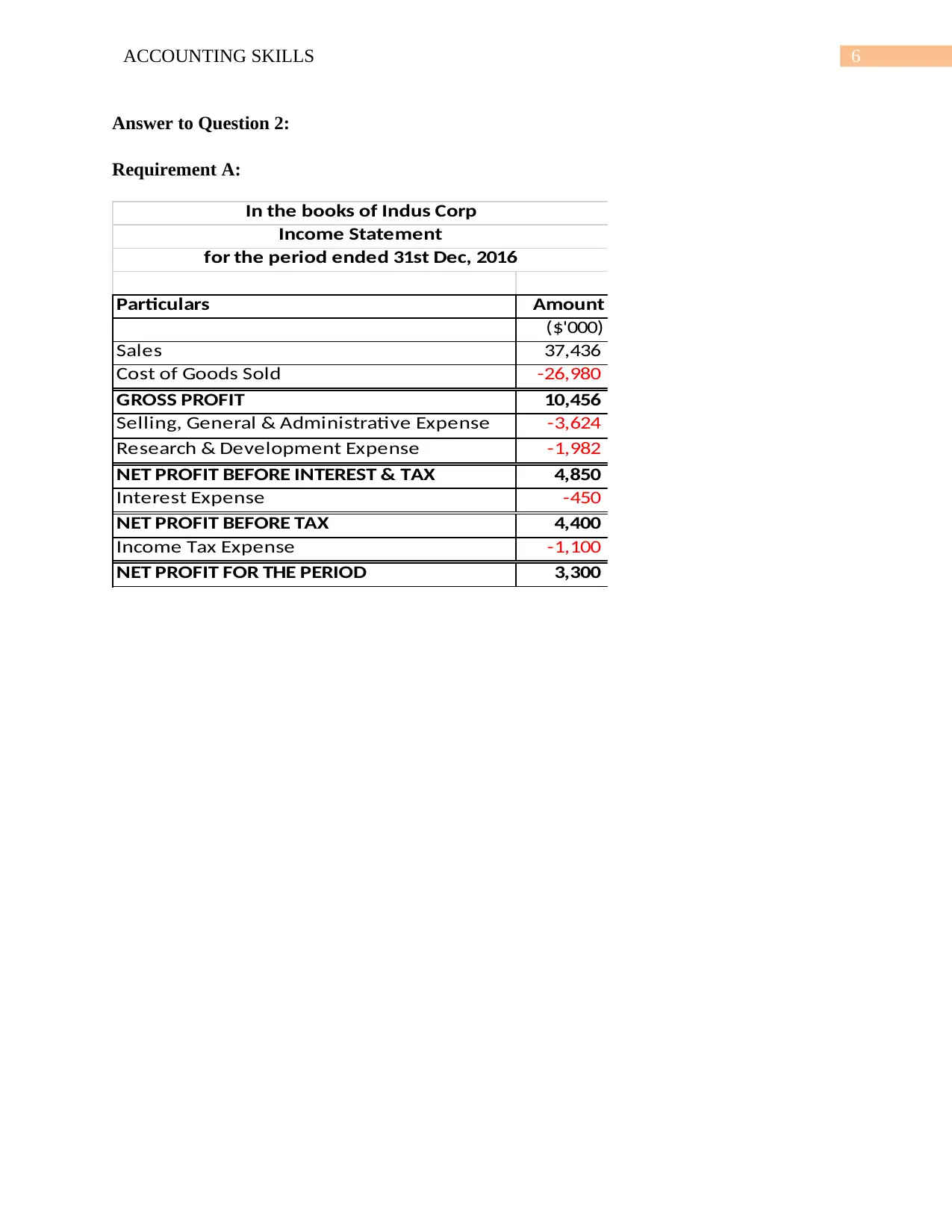

Answer to Question 2:

Requirement A:

Particulars Amount

($'000)

Sales 37,436

Cost of Goods Sold -26,980

GROSS PROFIT 10,456

Selling, General & Administrative Expense -3,624

Research & Development Expense -1,982

NET PROFIT BEFORE INTEREST & TAX 4,850

Interest Expense -450

NET PROFIT BEFORE TAX 4,400

Income Tax Expense -1,100

NET PROFIT FOR THE PERIOD 3,300

In the books of Indus Corp

Income Statement

for the period ended 31st Dec, 2016

Answer to Question 2:

Requirement A:

Particulars Amount

($'000)

Sales 37,436

Cost of Goods Sold -26,980

GROSS PROFIT 10,456

Selling, General & Administrative Expense -3,624

Research & Development Expense -1,982

NET PROFIT BEFORE INTEREST & TAX 4,850

Interest Expense -450

NET PROFIT BEFORE TAX 4,400

Income Tax Expense -1,100

NET PROFIT FOR THE PERIOD 3,300

In the books of Indus Corp

Income Statement

for the period ended 31st Dec, 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING SKILLS

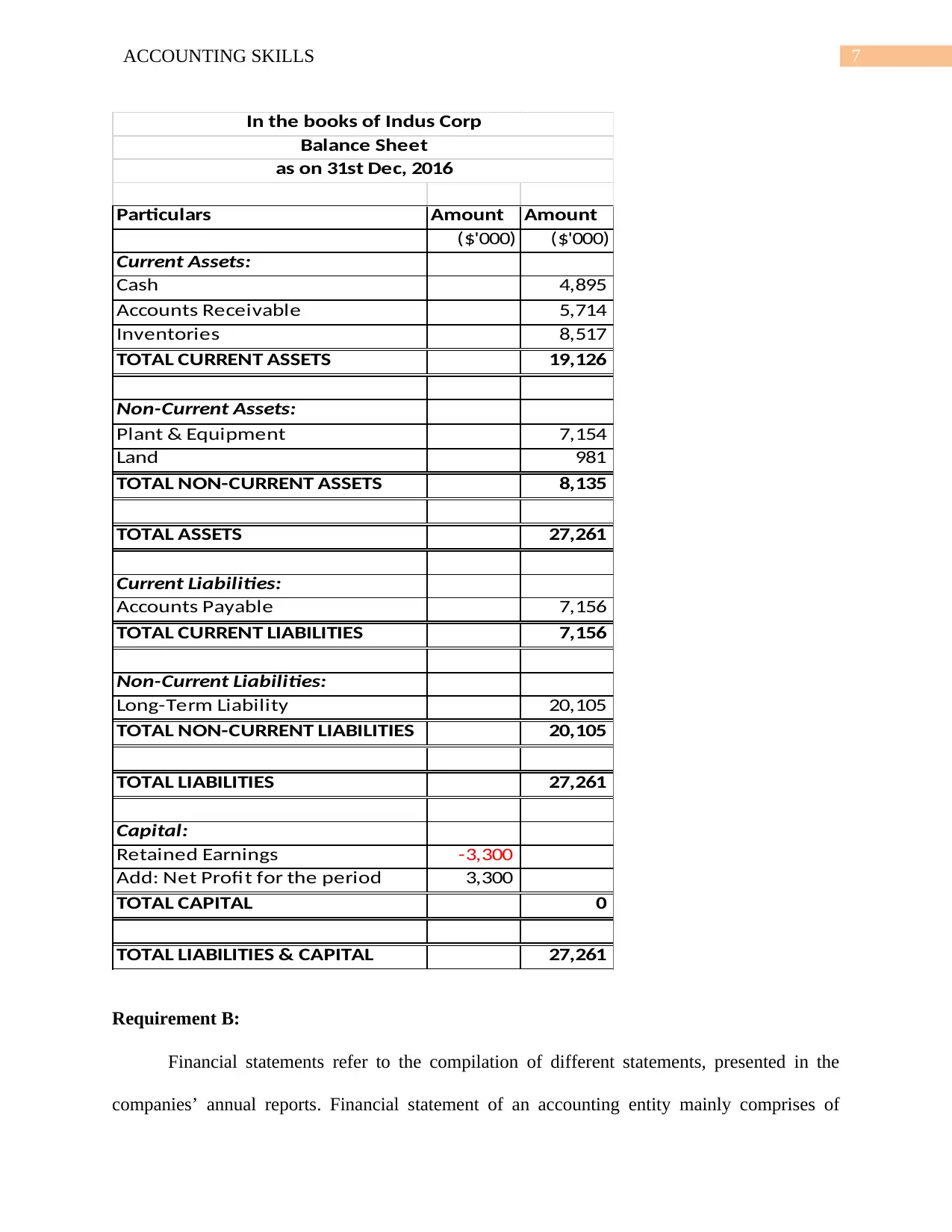

Particulars Amount Amount

($'000) ($'000)

Current Assets:

Cash 4,895

Accounts Receivable 5,714

Inventories 8,517

TOTAL CURRENT ASSETS 19,126

Non-Current Assets:

Plant & Equipment 7,154

Land 981

TOTAL NON-CURRENT ASSETS 8,135

TOTAL ASSETS 27,261

Current Liabilities:

Accounts Payable 7,156

TOTAL CURRENT LIABILITIES 7,156

Non-Current Liabilities:

Long-Term Liability 20,105

TOTAL NON-CURRENT LIABILITIES 20,105

TOTAL LIABILITIES 27,261

Capital:

Retained Earnings -3,300

Add: Net Profit for the period 3,300

TOTAL CAPITAL 0

TOTAL LIABILITIES & CAPITAL 27,261

In the books of Indus Corp

Balance Sheet

as on 31st Dec, 2016

Requirement B:

Financial statements refer to the compilation of different statements, presented in the

companies’ annual reports. Financial statement of an accounting entity mainly comprises of

Particulars Amount Amount

($'000) ($'000)

Current Assets:

Cash 4,895

Accounts Receivable 5,714

Inventories 8,517

TOTAL CURRENT ASSETS 19,126

Non-Current Assets:

Plant & Equipment 7,154

Land 981

TOTAL NON-CURRENT ASSETS 8,135

TOTAL ASSETS 27,261

Current Liabilities:

Accounts Payable 7,156

TOTAL CURRENT LIABILITIES 7,156

Non-Current Liabilities:

Long-Term Liability 20,105

TOTAL NON-CURRENT LIABILITIES 20,105

TOTAL LIABILITIES 27,261

Capital:

Retained Earnings -3,300

Add: Net Profit for the period 3,300

TOTAL CAPITAL 0

TOTAL LIABILITIES & CAPITAL 27,261

In the books of Indus Corp

Balance Sheet

as on 31st Dec, 2016

Requirement B:

Financial statements refer to the compilation of different statements, presented in the

companies’ annual reports. Financial statement of an accounting entity mainly comprises of

8ACCOUNTING SKILLS

income statement, balance sheet and cash flow statement (Carraher and Van Auken 2013). The

primary objective of the financial statement is to disclose the financial performance of the

business during a particular period. Financial statements are the main sources of the information

relating to the financial position of the company and cash flows in a business. Therefore, it is

very valuable for the investors. Financial statements are very useful for the investors in order to

take decisions regarding whether to invest in the company or not (Kraft 2014).

Financial statements are also important to the management of the company as the

information which are presented in the financial statements are used for the purpose of

comparison with previous year’s performance and then decisions regarding improvements can be

made on the basis of the information which are already shown in the annual report of the

business. Moreover, financial statements are essential for obtaining credit from financial

institutions and in the presence of a favourable financial statements, required amount of credit is

easily granted (Ball 2013). Thus, financial statements are used both potential investors,

stakeholders and banking institution to analyse the current performance of the firm and also

check the viability of the business for future. In other words, it can be said that the financial

statements provide the information, required to measure the financial performance of a business

for a particular period.

income statement, balance sheet and cash flow statement (Carraher and Van Auken 2013). The

primary objective of the financial statement is to disclose the financial performance of the

business during a particular period. Financial statements are the main sources of the information

relating to the financial position of the company and cash flows in a business. Therefore, it is

very valuable for the investors. Financial statements are very useful for the investors in order to

take decisions regarding whether to invest in the company or not (Kraft 2014).

Financial statements are also important to the management of the company as the

information which are presented in the financial statements are used for the purpose of

comparison with previous year’s performance and then decisions regarding improvements can be

made on the basis of the information which are already shown in the annual report of the

business. Moreover, financial statements are essential for obtaining credit from financial

institutions and in the presence of a favourable financial statements, required amount of credit is

easily granted (Ball 2013). Thus, financial statements are used both potential investors,

stakeholders and banking institution to analyse the current performance of the firm and also

check the viability of the business for future. In other words, it can be said that the financial

statements provide the information, required to measure the financial performance of a business

for a particular period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING SKILLS

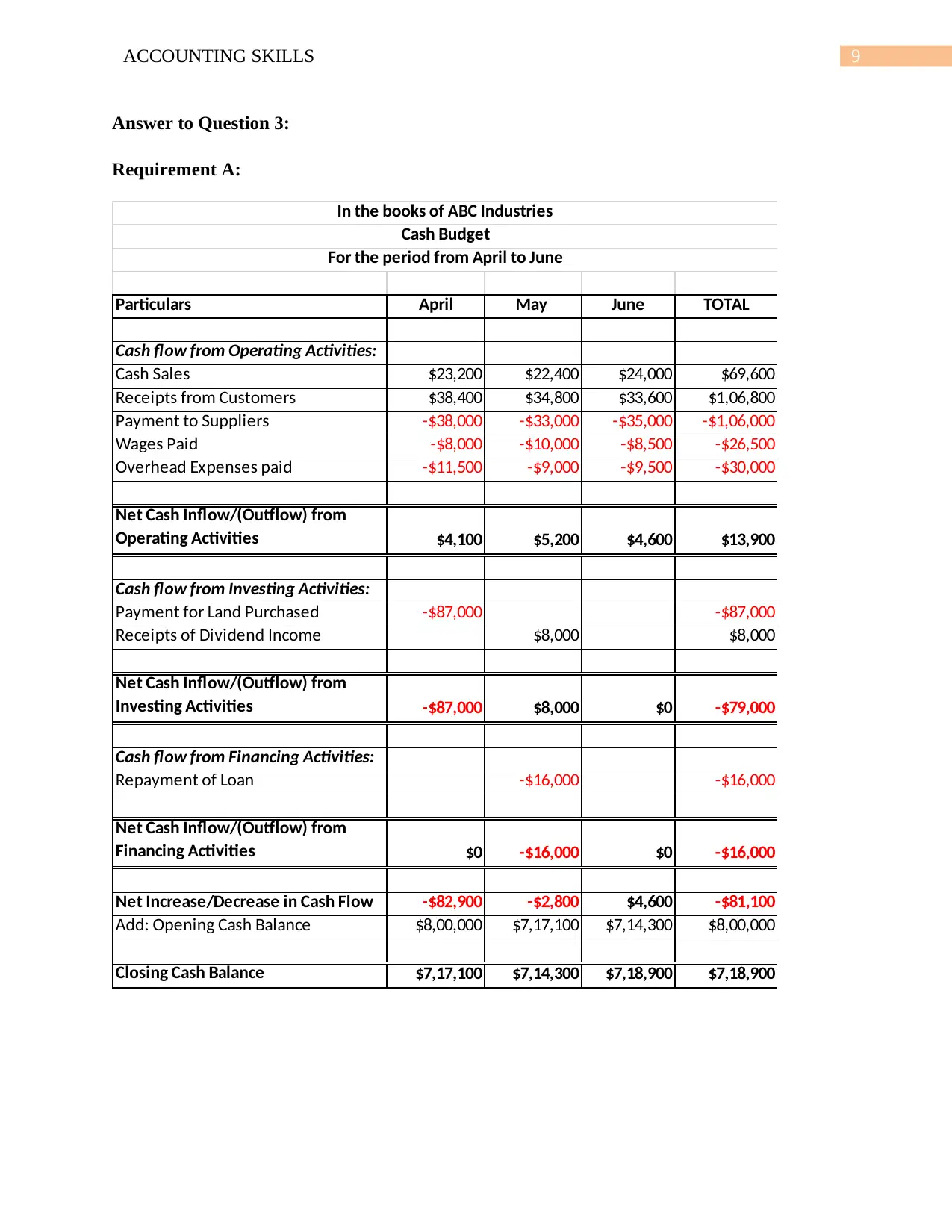

Answer to Question 3:

Requirement A:

Particulars April May June TOTAL

Cash flow from Operating Activities:

Cash Sales $23,200 $22,400 $24,000 $69,600

Receipts from Customers $38,400 $34,800 $33,600 $1,06,800

Payment to Suppliers -$38,000 -$33,000 -$35,000 -$1,06,000

Wages Paid -$8,000 -$10,000 -$8,500 -$26,500

Overhead Expenses paid -$11,500 -$9,000 -$9,500 -$30,000

Net Cash Inflow/(Outflow) from

Operating Activities $4,100 $5,200 $4,600 $13,900

Cash flow from Investing Activities:

Payment for Land Purchased -$87,000 -$87,000

Receipts of Dividend Income $8,000 $8,000

Net Cash Inflow/(Outflow) from

Investing Activities -$87,000 $8,000 $0 -$79,000

Cash flow from Financing Activities:

Repayment of Loan -$16,000 -$16,000

Net Cash Inflow/(Outflow) from

Financing Activities $0 -$16,000 $0 -$16,000

Net Increase/Decrease in Cash Flow -$82,900 -$2,800 $4,600 -$81,100

Add: Opening Cash Balance $8,00,000 $7,17,100 $7,14,300 $8,00,000

Closing Cash Balance $7,17,100 $7,14,300 $7,18,900 $7,18,900

In the books of ABC Industries

Cash Budget

For the period from April to June

Answer to Question 3:

Requirement A:

Particulars April May June TOTAL

Cash flow from Operating Activities:

Cash Sales $23,200 $22,400 $24,000 $69,600

Receipts from Customers $38,400 $34,800 $33,600 $1,06,800

Payment to Suppliers -$38,000 -$33,000 -$35,000 -$1,06,000

Wages Paid -$8,000 -$10,000 -$8,500 -$26,500

Overhead Expenses paid -$11,500 -$9,000 -$9,500 -$30,000

Net Cash Inflow/(Outflow) from

Operating Activities $4,100 $5,200 $4,600 $13,900

Cash flow from Investing Activities:

Payment for Land Purchased -$87,000 -$87,000

Receipts of Dividend Income $8,000 $8,000

Net Cash Inflow/(Outflow) from

Investing Activities -$87,000 $8,000 $0 -$79,000

Cash flow from Financing Activities:

Repayment of Loan -$16,000 -$16,000

Net Cash Inflow/(Outflow) from

Financing Activities $0 -$16,000 $0 -$16,000

Net Increase/Decrease in Cash Flow -$82,900 -$2,800 $4,600 -$81,100

Add: Opening Cash Balance $8,00,000 $7,17,100 $7,14,300 $8,00,000

Closing Cash Balance $7,17,100 $7,14,300 $7,18,900 $7,18,900

In the books of ABC Industries

Cash Budget

For the period from April to June

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING SKILLS

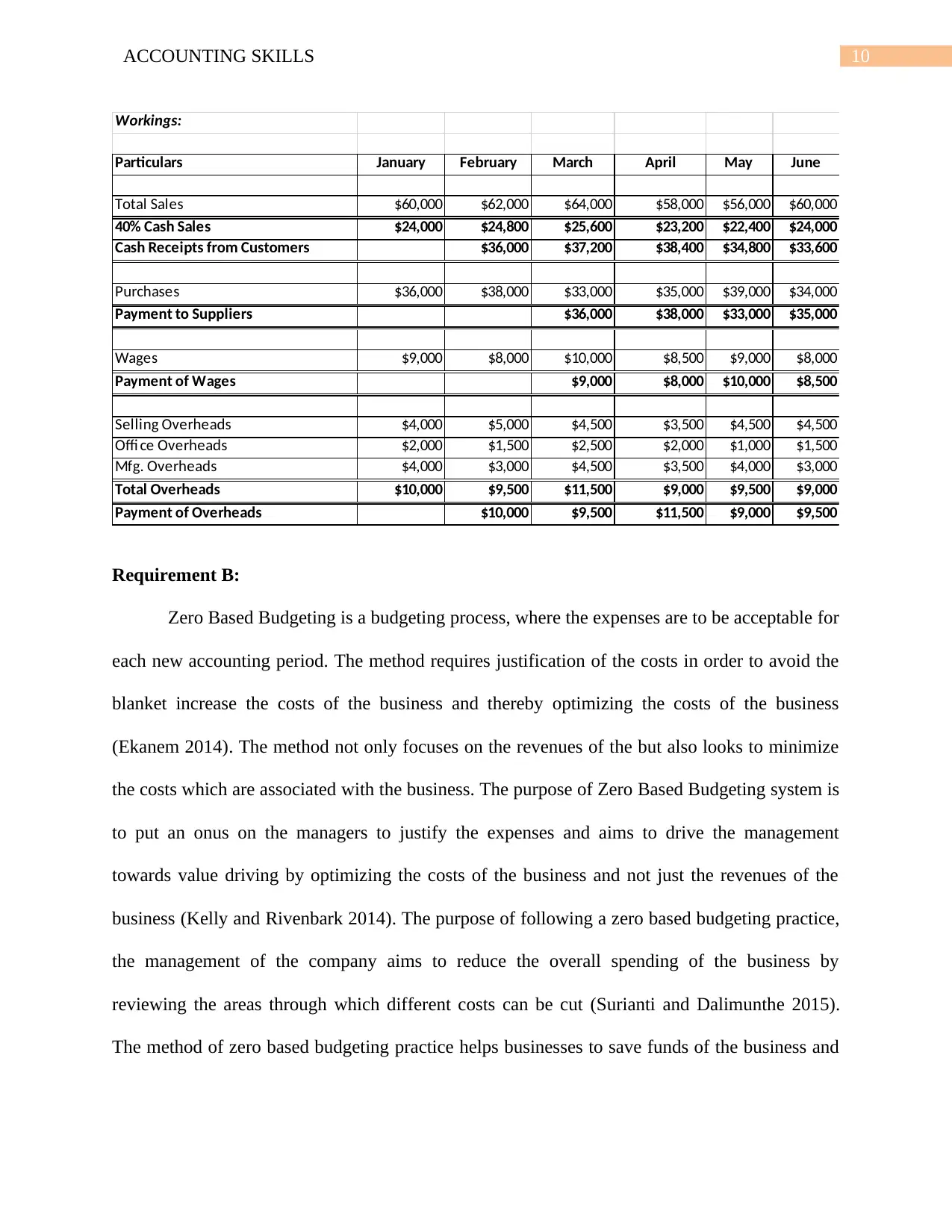

Workings:

Particulars January February March April May June

Total Sales $60,000 $62,000 $64,000 $58,000 $56,000 $60,000

40% Cash Sales $24,000 $24,800 $25,600 $23,200 $22,400 $24,000

Cash Receipts from Customers $36,000 $37,200 $38,400 $34,800 $33,600

Purchases $36,000 $38,000 $33,000 $35,000 $39,000 $34,000

Payment to Suppliers $36,000 $38,000 $33,000 $35,000

Wages $9,000 $8,000 $10,000 $8,500 $9,000 $8,000

Payment of Wages $9,000 $8,000 $10,000 $8,500

Selling Overheads $4,000 $5,000 $4,500 $3,500 $4,500 $4,500

Offi ce Overheads $2,000 $1,500 $2,500 $2,000 $1,000 $1,500

Mfg. Overheads $4,000 $3,000 $4,500 $3,500 $4,000 $3,000

Total Overheads $10,000 $9,500 $11,500 $9,000 $9,500 $9,000

Payment of Overheads $10,000 $9,500 $11,500 $9,000 $9,500

Requirement B:

Zero Based Budgeting is a budgeting process, where the expenses are to be acceptable for

each new accounting period. The method requires justification of the costs in order to avoid the

blanket increase the costs of the business and thereby optimizing the costs of the business

(Ekanem 2014). The method not only focuses on the revenues of the but also looks to minimize

the costs which are associated with the business. The purpose of Zero Based Budgeting system is

to put an onus on the managers to justify the expenses and aims to drive the management

towards value driving by optimizing the costs of the business and not just the revenues of the

business (Kelly and Rivenbark 2014). The purpose of following a zero based budgeting practice,

the management of the company aims to reduce the overall spending of the business by

reviewing the areas through which different costs can be cut (Surianti and Dalimunthe 2015).

The method of zero based budgeting practice helps businesses to save funds of the business and

Workings:

Particulars January February March April May June

Total Sales $60,000 $62,000 $64,000 $58,000 $56,000 $60,000

40% Cash Sales $24,000 $24,800 $25,600 $23,200 $22,400 $24,000

Cash Receipts from Customers $36,000 $37,200 $38,400 $34,800 $33,600

Purchases $36,000 $38,000 $33,000 $35,000 $39,000 $34,000

Payment to Suppliers $36,000 $38,000 $33,000 $35,000

Wages $9,000 $8,000 $10,000 $8,500 $9,000 $8,000

Payment of Wages $9,000 $8,000 $10,000 $8,500

Selling Overheads $4,000 $5,000 $4,500 $3,500 $4,500 $4,500

Offi ce Overheads $2,000 $1,500 $2,500 $2,000 $1,000 $1,500

Mfg. Overheads $4,000 $3,000 $4,500 $3,500 $4,000 $3,000

Total Overheads $10,000 $9,500 $11,500 $9,000 $9,500 $9,000

Payment of Overheads $10,000 $9,500 $11,500 $9,000 $9,500

Requirement B:

Zero Based Budgeting is a budgeting process, where the expenses are to be acceptable for

each new accounting period. The method requires justification of the costs in order to avoid the

blanket increase the costs of the business and thereby optimizing the costs of the business

(Ekanem 2014). The method not only focuses on the revenues of the but also looks to minimize

the costs which are associated with the business. The purpose of Zero Based Budgeting system is

to put an onus on the managers to justify the expenses and aims to drive the management

towards value driving by optimizing the costs of the business and not just the revenues of the

business (Kelly and Rivenbark 2014). The purpose of following a zero based budgeting practice,

the management of the company aims to reduce the overall spending of the business by

reviewing the areas through which different costs can be cut (Surianti and Dalimunthe 2015).

The method of zero based budgeting practice helps businesses to save funds of the business and

11ACCOUNTING SKILLS

effectively scrutinise the budget, accounting for every costs which the business has incurred for a

year.

Most of the business Zero Budgeting policies in order to prepare a new budget for every

new period so that the additional increase in the cost of the business can be reduced and

optimized.

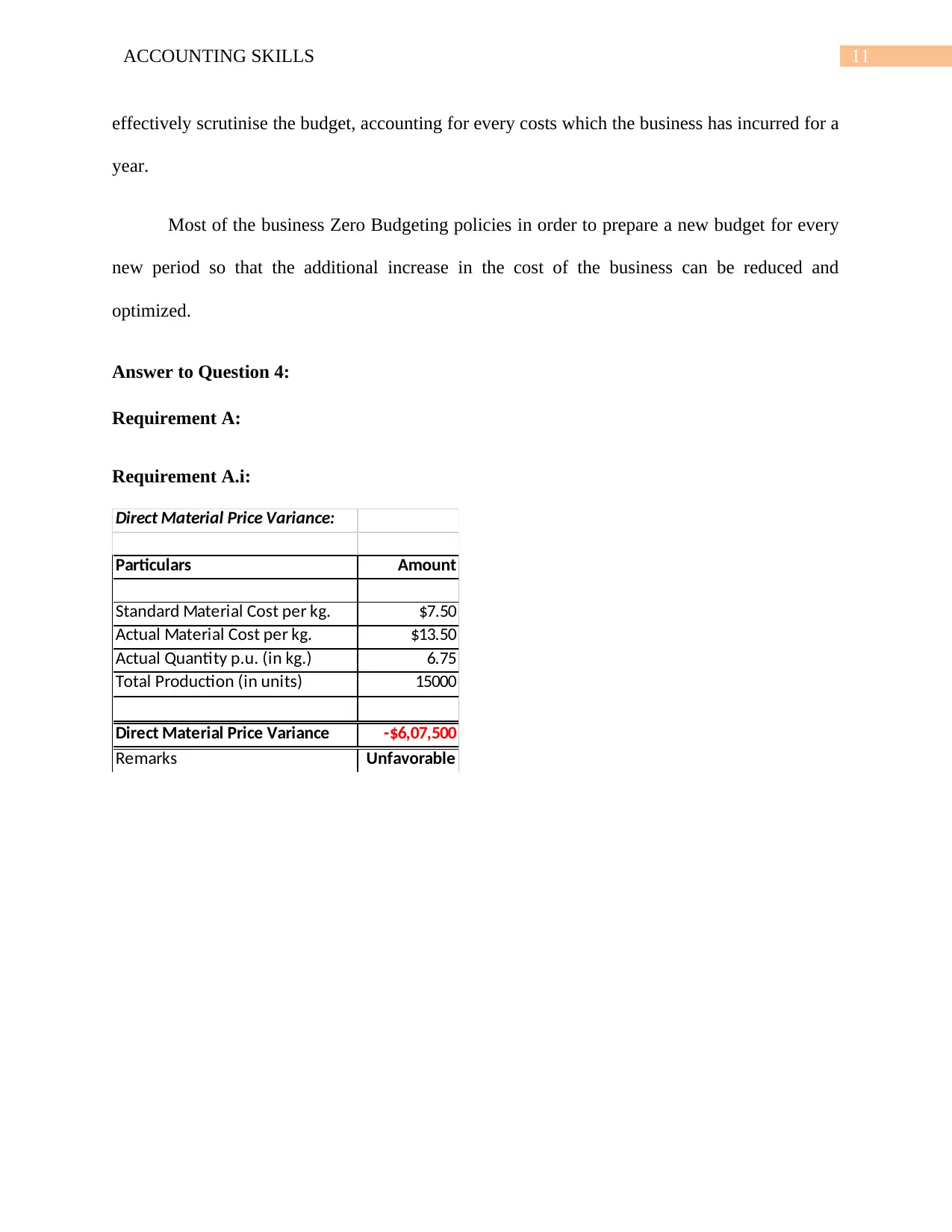

Answer to Question 4:

Requirement A:

Requirement A.i:

Direct Material Price Variance:

Particulars Amount

Standard Material Cost per kg. $7.50

Actual Material Cost per kg. $13.50

Actual Quantity p.u. (in kg.) 6.75

Total Production (in units) 15000

Direct Material Price Variance -$6,07,500

Remarks Unfavorable

effectively scrutinise the budget, accounting for every costs which the business has incurred for a

year.

Most of the business Zero Budgeting policies in order to prepare a new budget for every

new period so that the additional increase in the cost of the business can be reduced and

optimized.

Answer to Question 4:

Requirement A:

Requirement A.i:

Direct Material Price Variance:

Particulars Amount

Standard Material Cost per kg. $7.50

Actual Material Cost per kg. $13.50

Actual Quantity p.u. (in kg.) 6.75

Total Production (in units) 15000

Direct Material Price Variance -$6,07,500

Remarks Unfavorable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.