Accounts Computations: FIFO, LIFO, and Merchandising Company Analysis

VerifiedAdded on 2023/04/21

|6

|826

|269

Homework Assignment

AI Summary

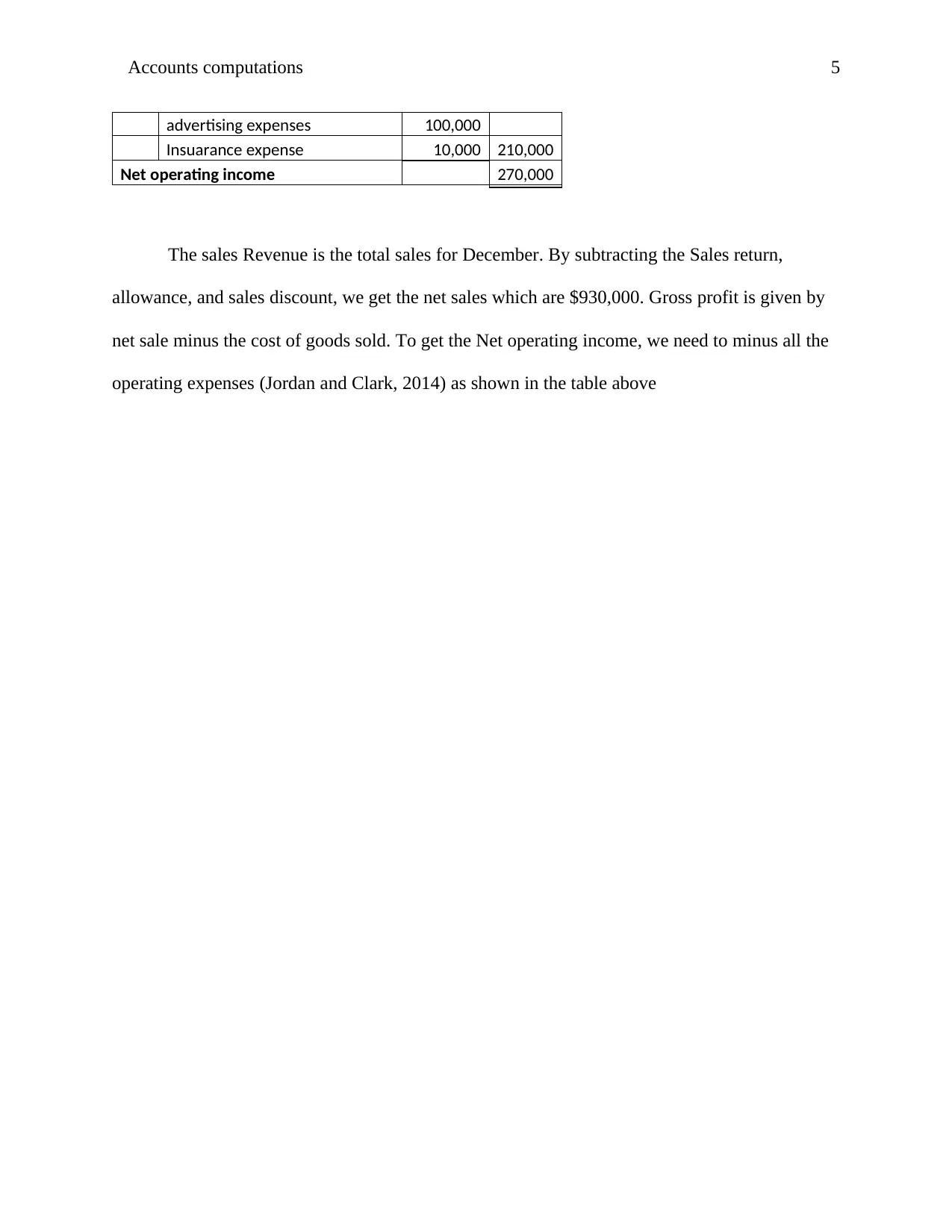

This assignment focuses on accounts computations, covering topics such as inventory costing methods (FIFO and LIFO), and the preparation of income statements for merchandising companies. It includes journal entries for merchandise purchases on credit, demonstrating how discounts are applied when payments are made within the specified credit terms. The assignment also explains the differences between merchandising and service companies, particularly in terms of inventory and cost of goods sold. A detailed income statement for Yazeed Merchandising Company is presented, illustrating the calculation of net sales, gross profit, and net operating income. Desklib provides students access to similar solved assignments and study tools.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.