Analysis of Accounts Receivable: Auditing Theory and Practice Report

VerifiedAdded on 2021/06/17

|14

|1846

|131

Report

AI Summary

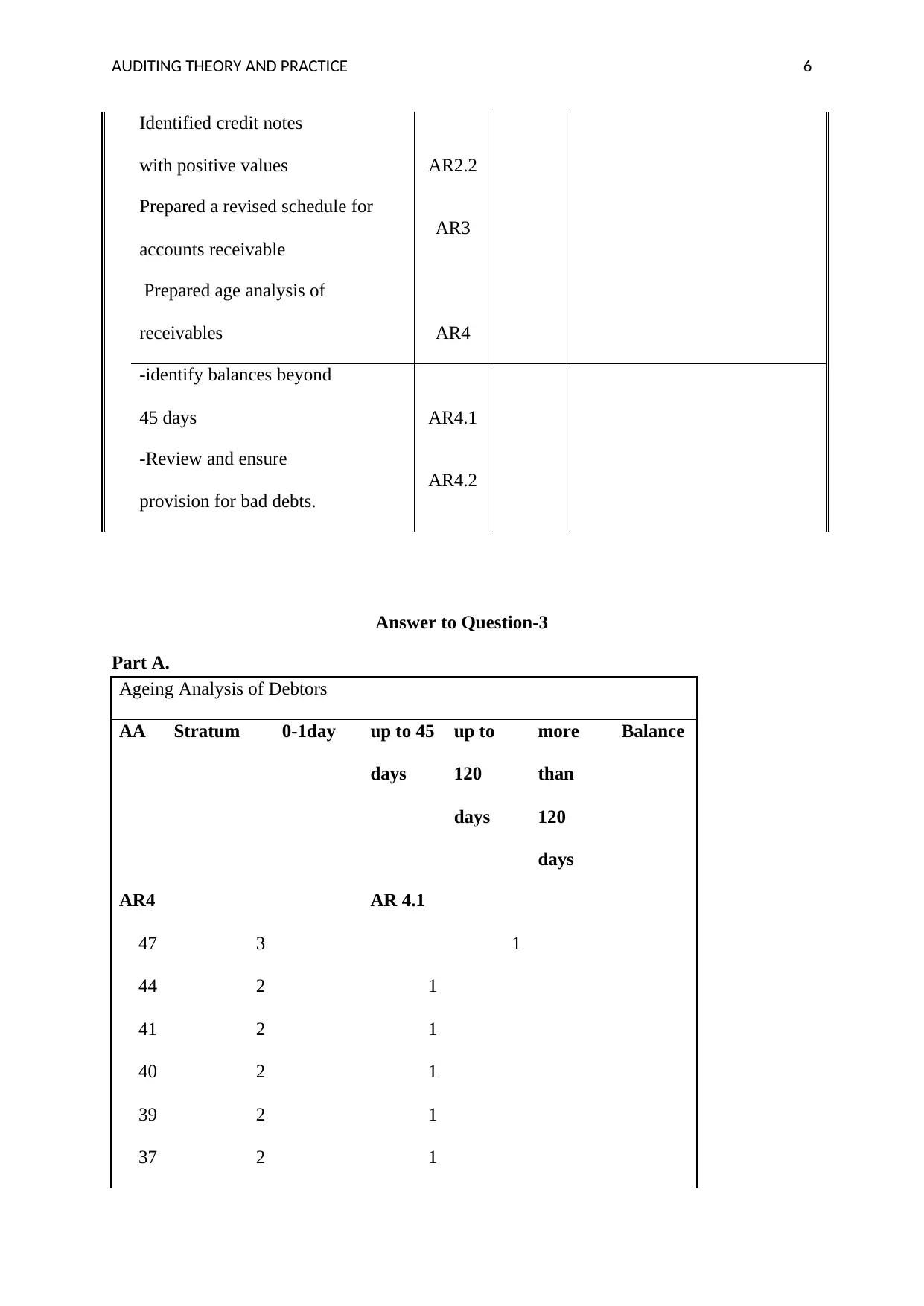

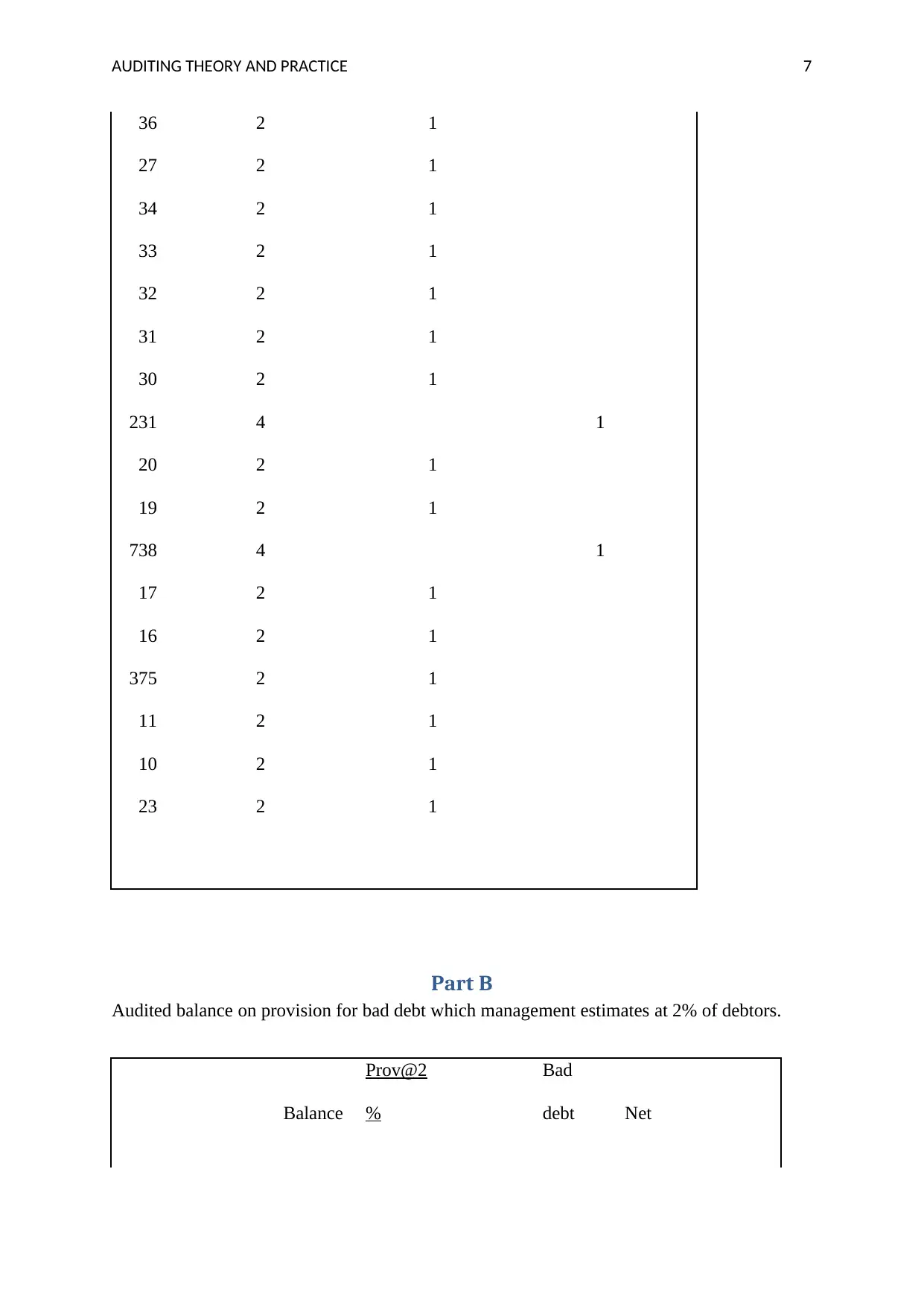

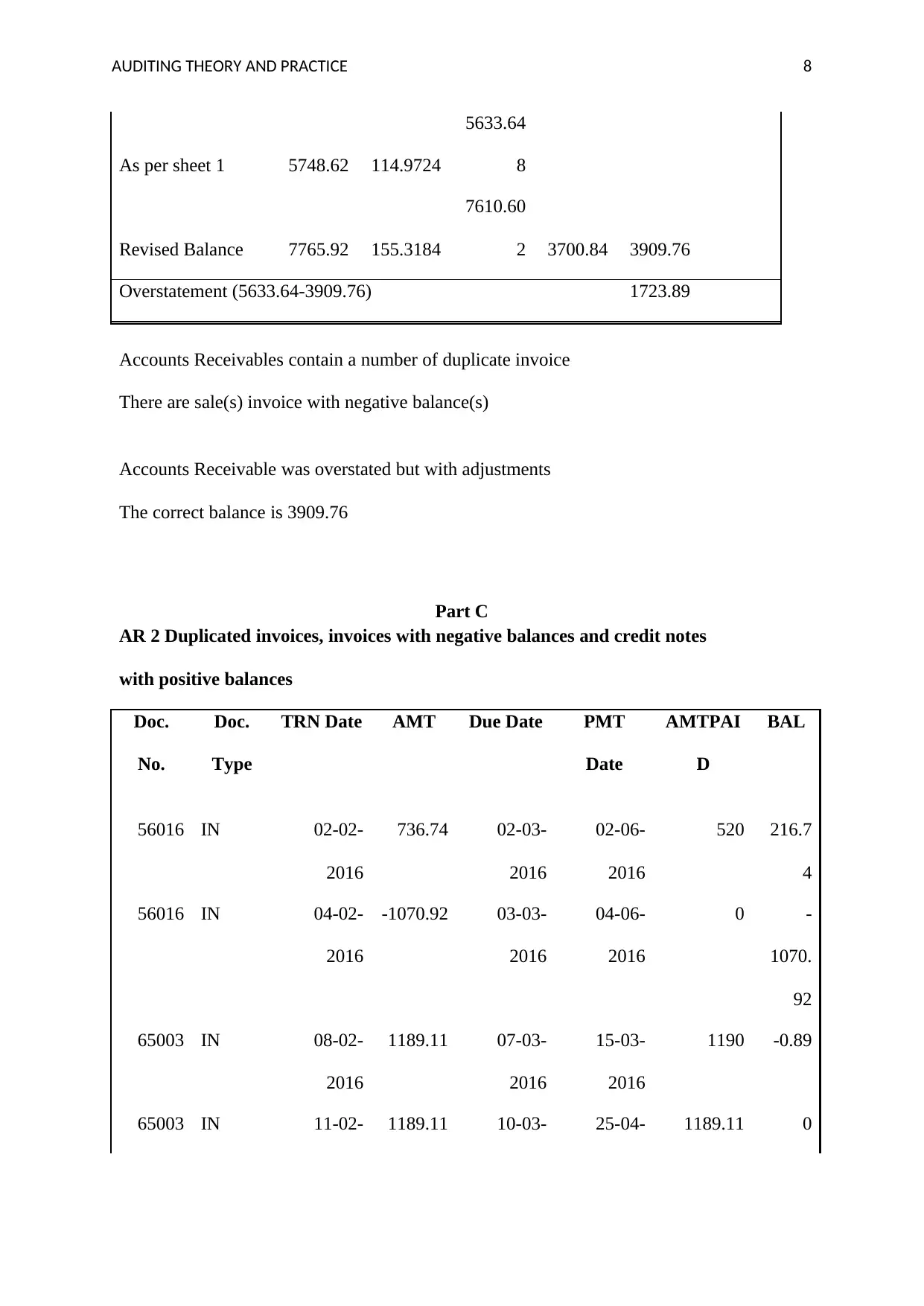

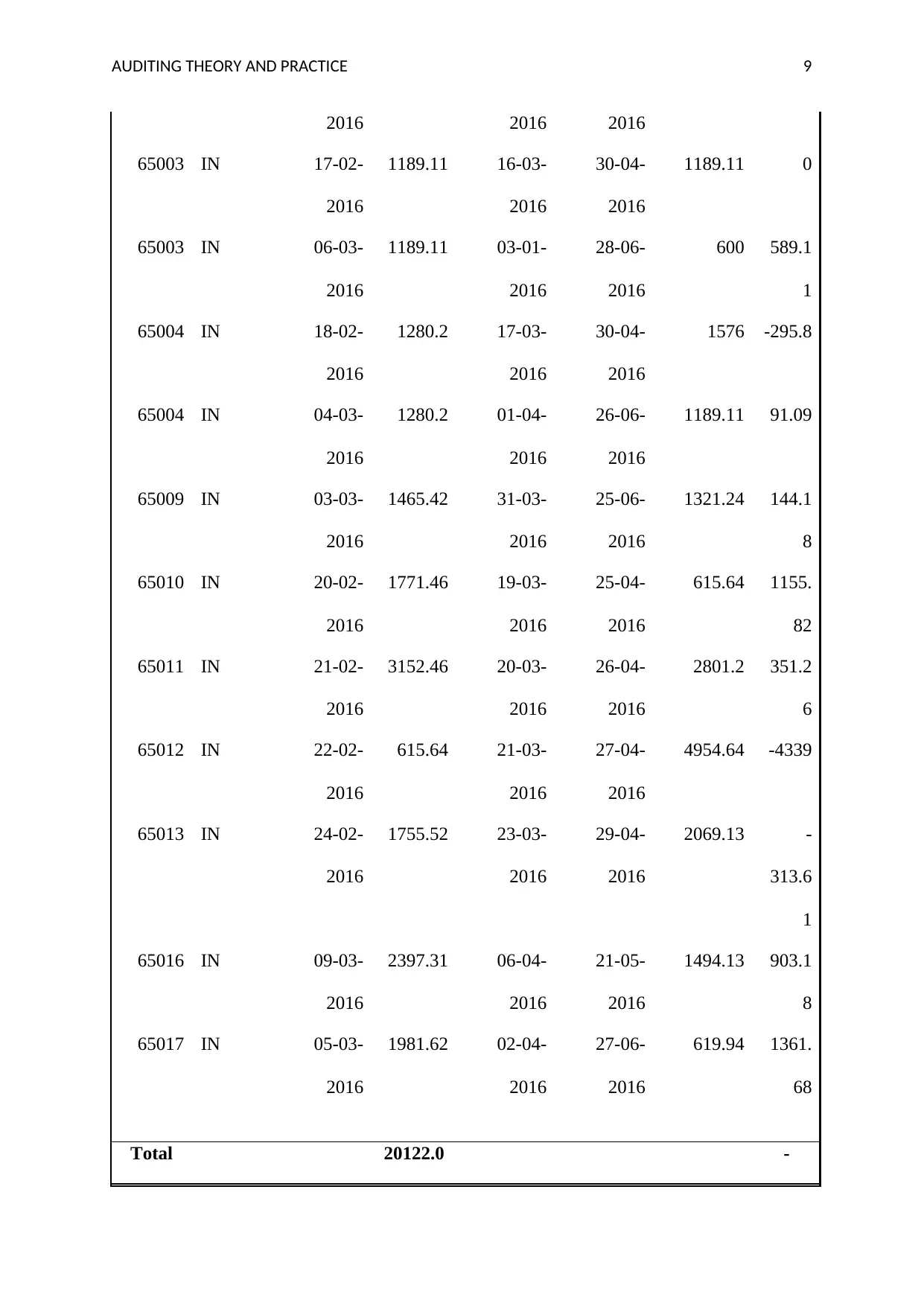

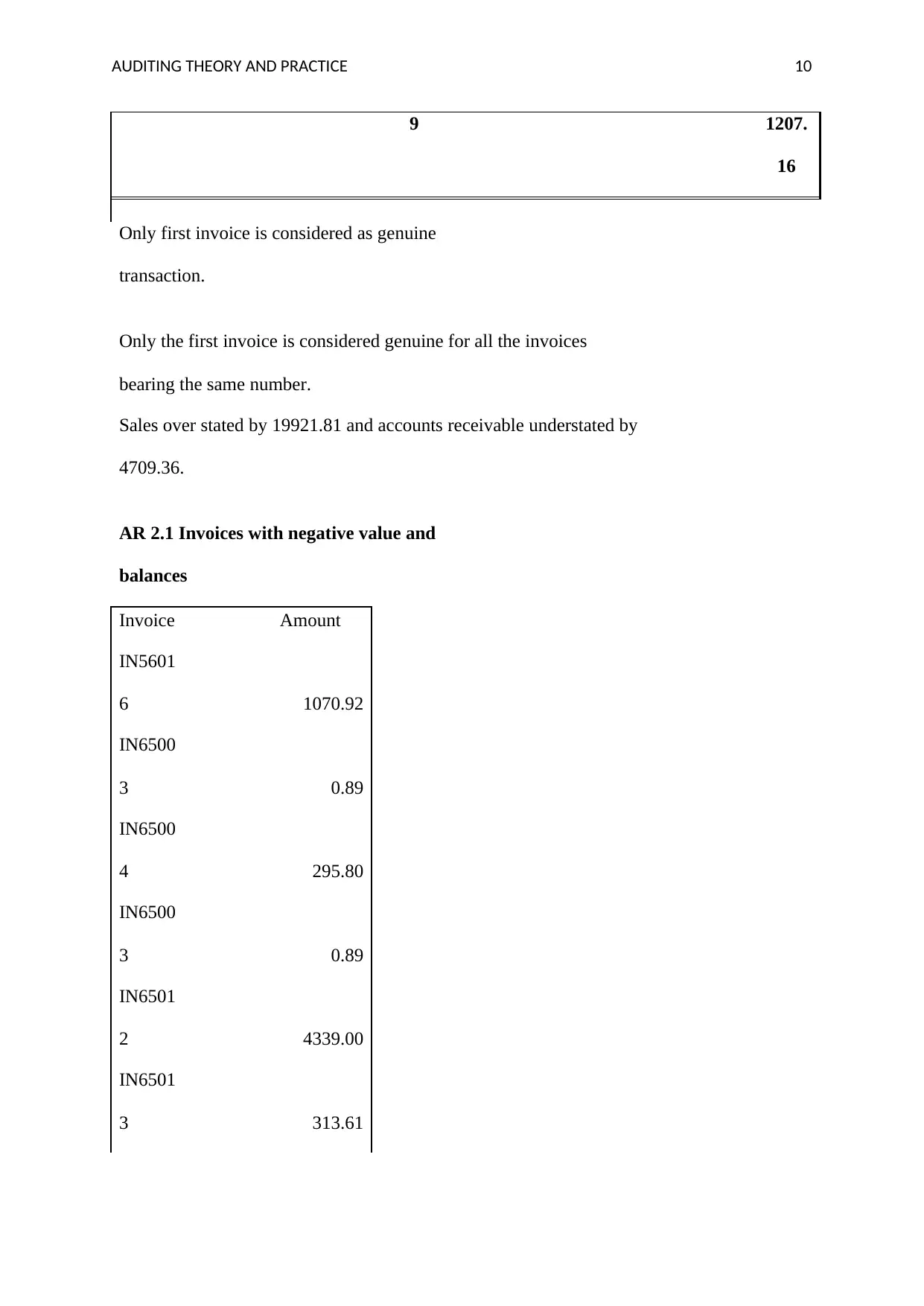

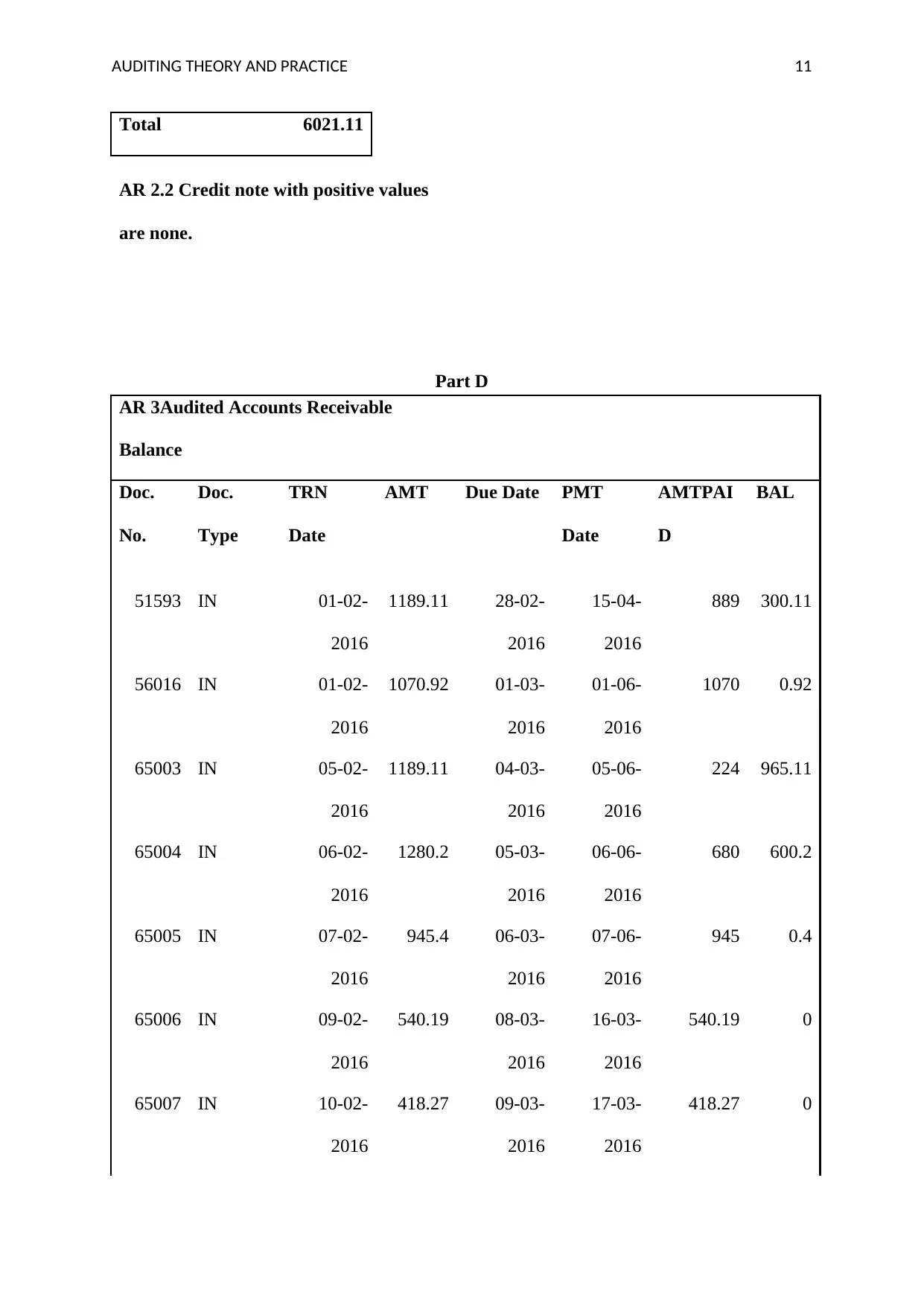

This report provides a comprehensive analysis of accounts receivable auditing, beginning with an introduction to accounts receivable and the associated risks, including credit facility issues, inadequate credit checks, inefficient procedures, and non-collectable debts. The report then presents a detailed audit, including an analysis of trade and other receivables, identification of duplicate invoices and negative balances, and an aging analysis of debtors. It further calculates the provision for bad debts and examines instances of overstatement in accounts receivable. The report highlights the importance of accurate financial reporting and concludes with the significance of thorough auditing procedures to ensure the reliability of financial statements. The analysis includes specific examples of invoice discrepancies and their impact on financial reporting, ultimately emphasizing the need for robust internal controls and diligent auditing practices.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.