ACCT 1211 Accounting I Assignment 8: Solutions and Analysis

VerifiedAdded on 2023/05/28

|10

|1026

|301

Homework Assignment

AI Summary

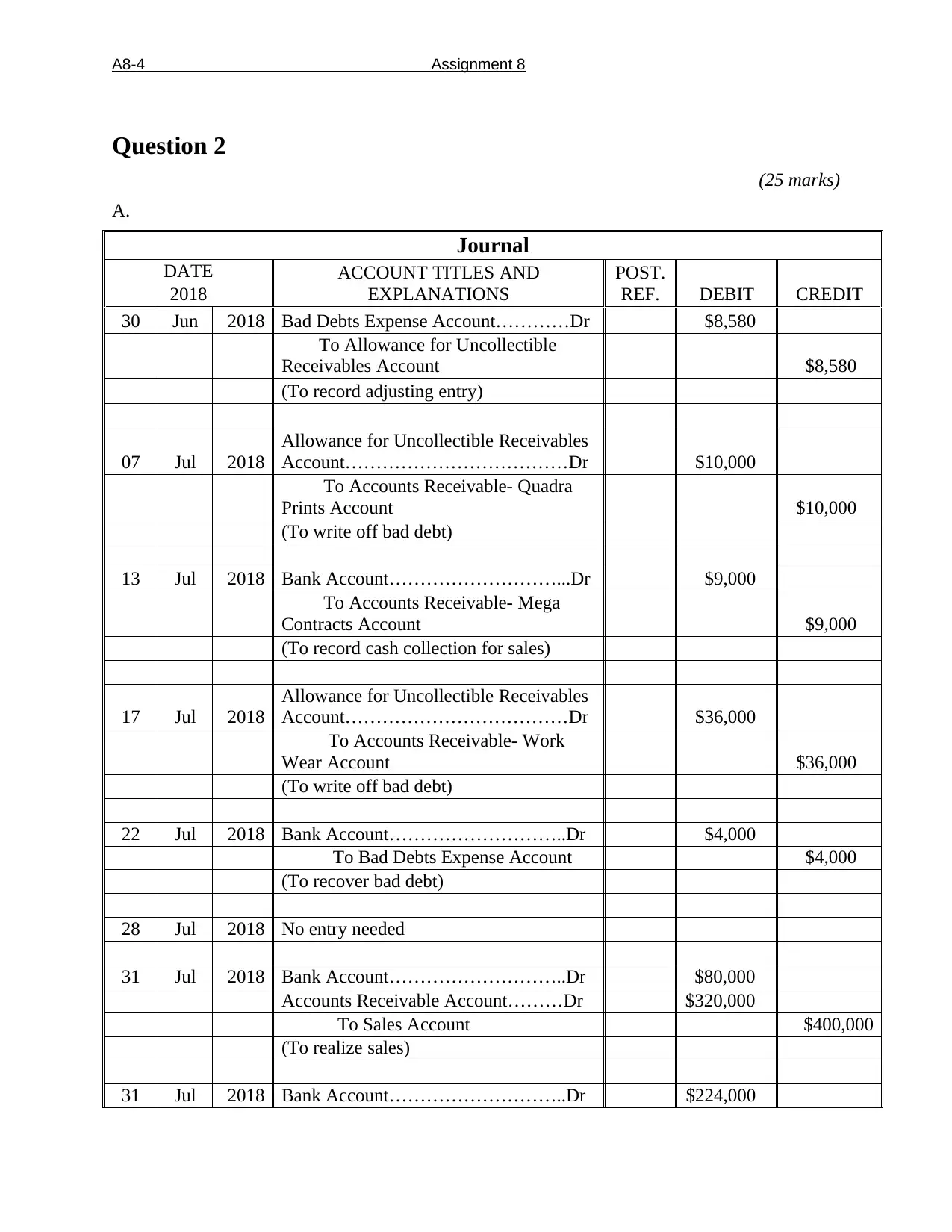

This document provides comprehensive solutions for ACCT 1211 Assignment 8, covering key accounting concepts such as bad debt expense, allowance for doubtful accounts, and various journal entries. Question 1 presents general journal entries, account analysis, and balance sheet presentation related to writing off receivables and calculating bad debt expense. Question 2 involves journal entries for bad debts, along with balance sheet and income statement impacts. Question 3 presents general journal entries for note receivables and related interest income, while Question 4 focuses on financial ratio analysis, including current and acid-test ratios, along with the interpretation of these ratios and their changes from the prior year. The assignment covers topics like journalizing transactions, preparing financial statements, and understanding financial ratios.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.