Accounting 2007 Assignment: Depreciation, Revaluation and Impairment

VerifiedAdded on 2022/08/31

|8

|892

|12

Homework Assignment

AI Summary

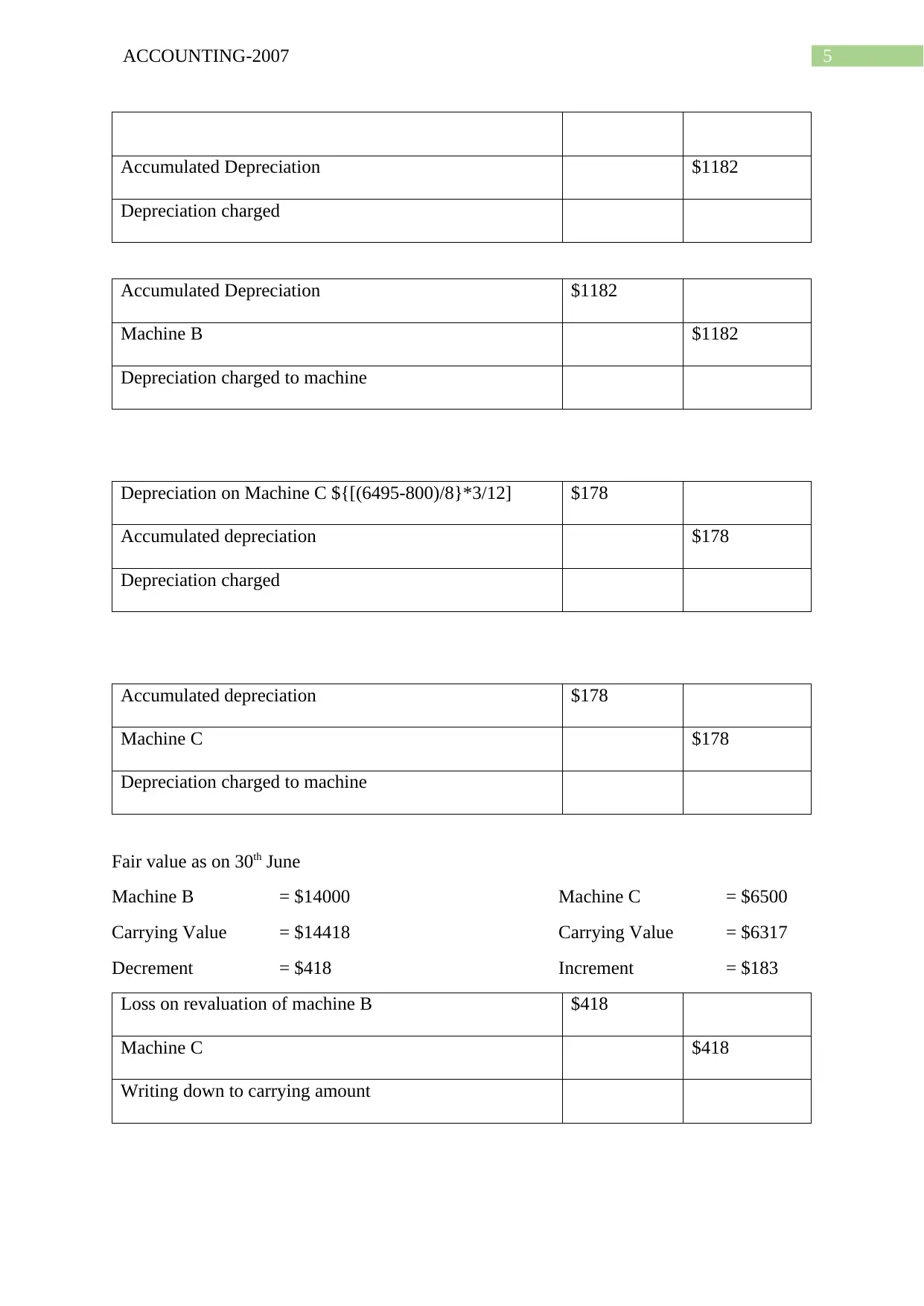

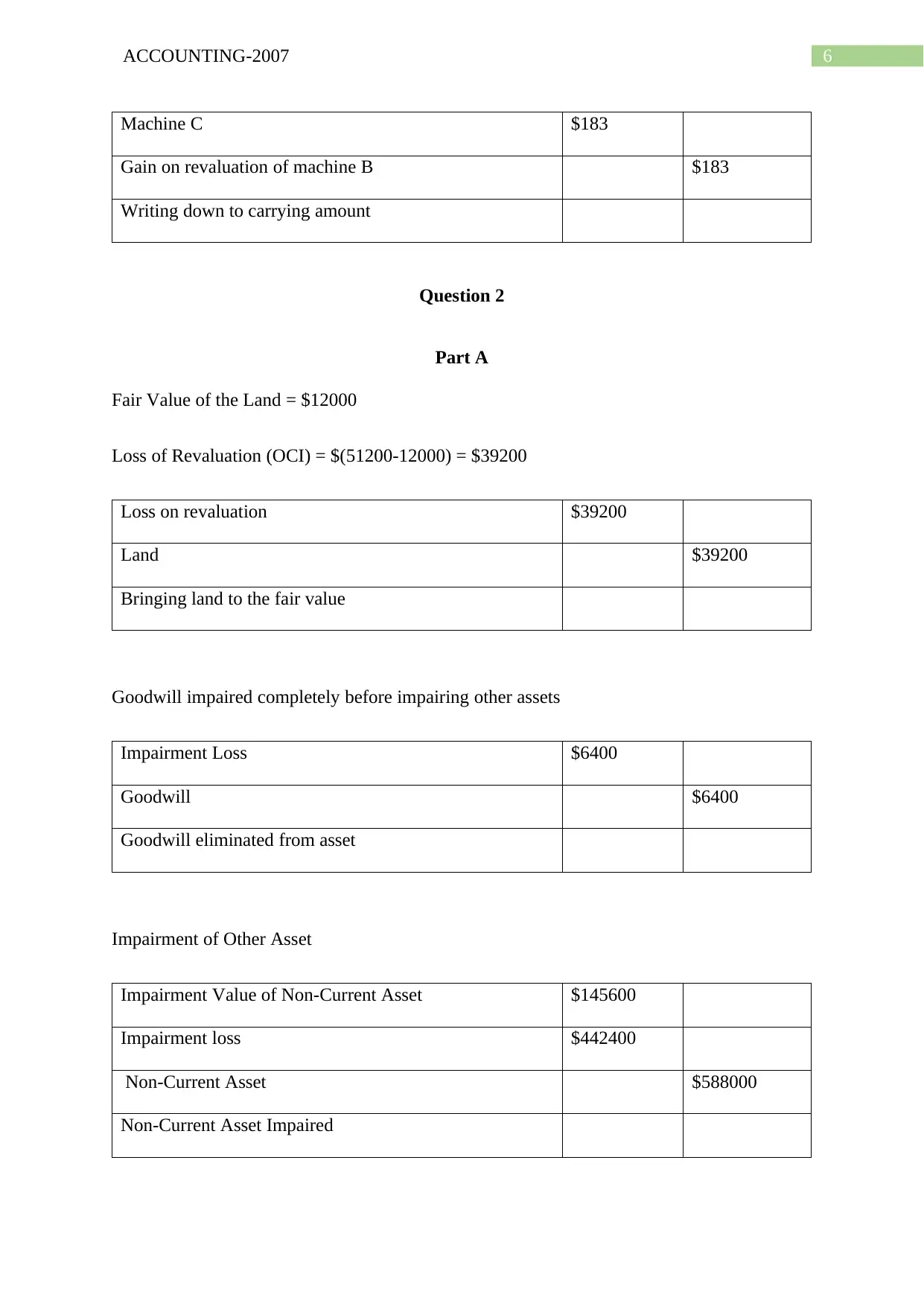

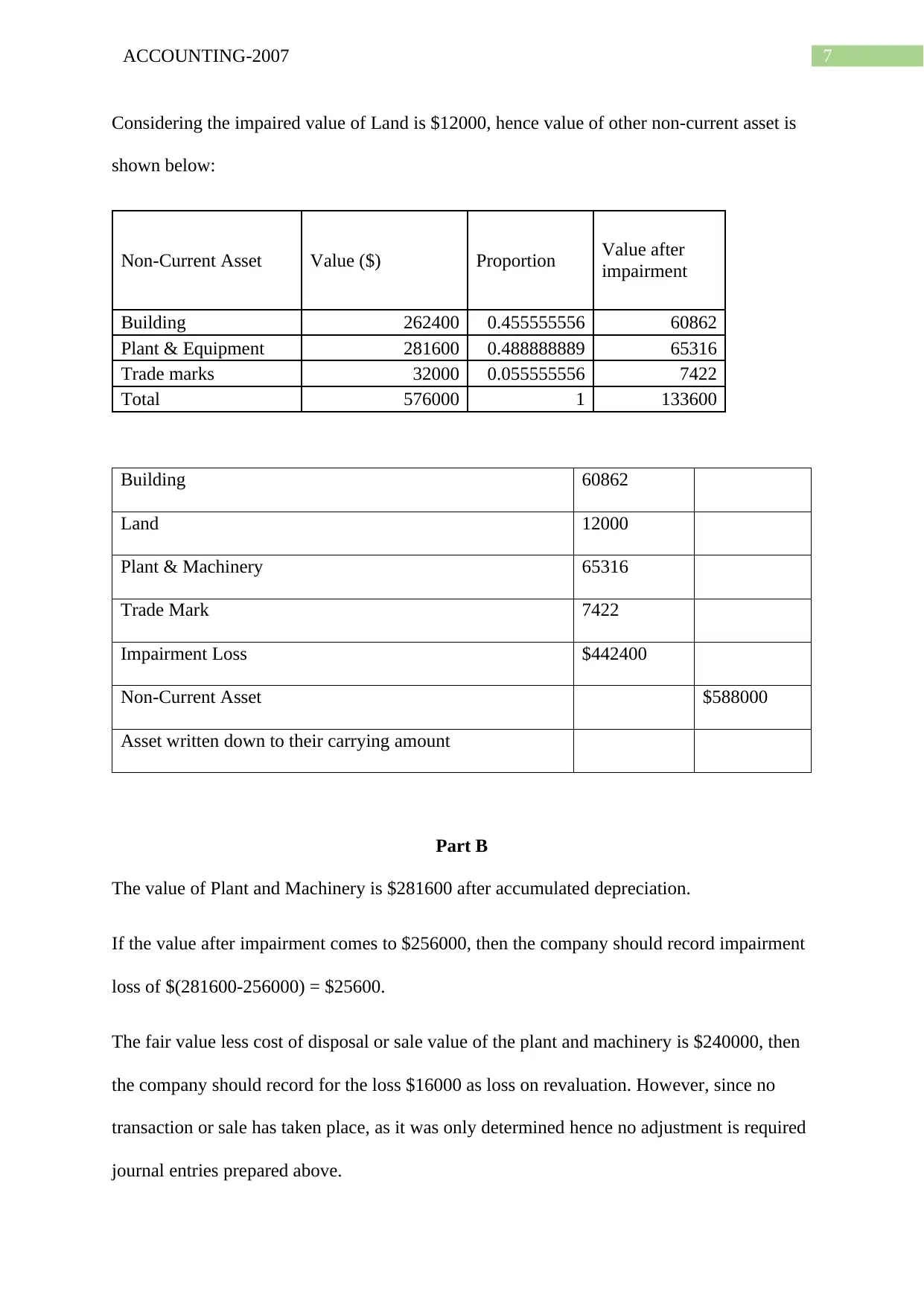

This accounting assignment solution addresses depreciation, revaluation, and impairment of assets. Question 1 involves calculating depreciation for machinery using different methods, considering revaluation, and accounting for asset disposals and additions. It includes journal entries and calculations for depreciation expense, accumulated depreciation, and losses/gains on revaluation and disposal. Question 2 focuses on the revaluation and impairment of land and other non-current assets. It presents journal entries for revaluation losses, impairment of goodwill, and impairment of other assets, and includes calculations to determine the impaired values and the allocation of impairment losses across assets. Part B explores the accounting treatment when the fair value of a plant and machinery is below its carrying value and the need for impairment loss recognition.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.