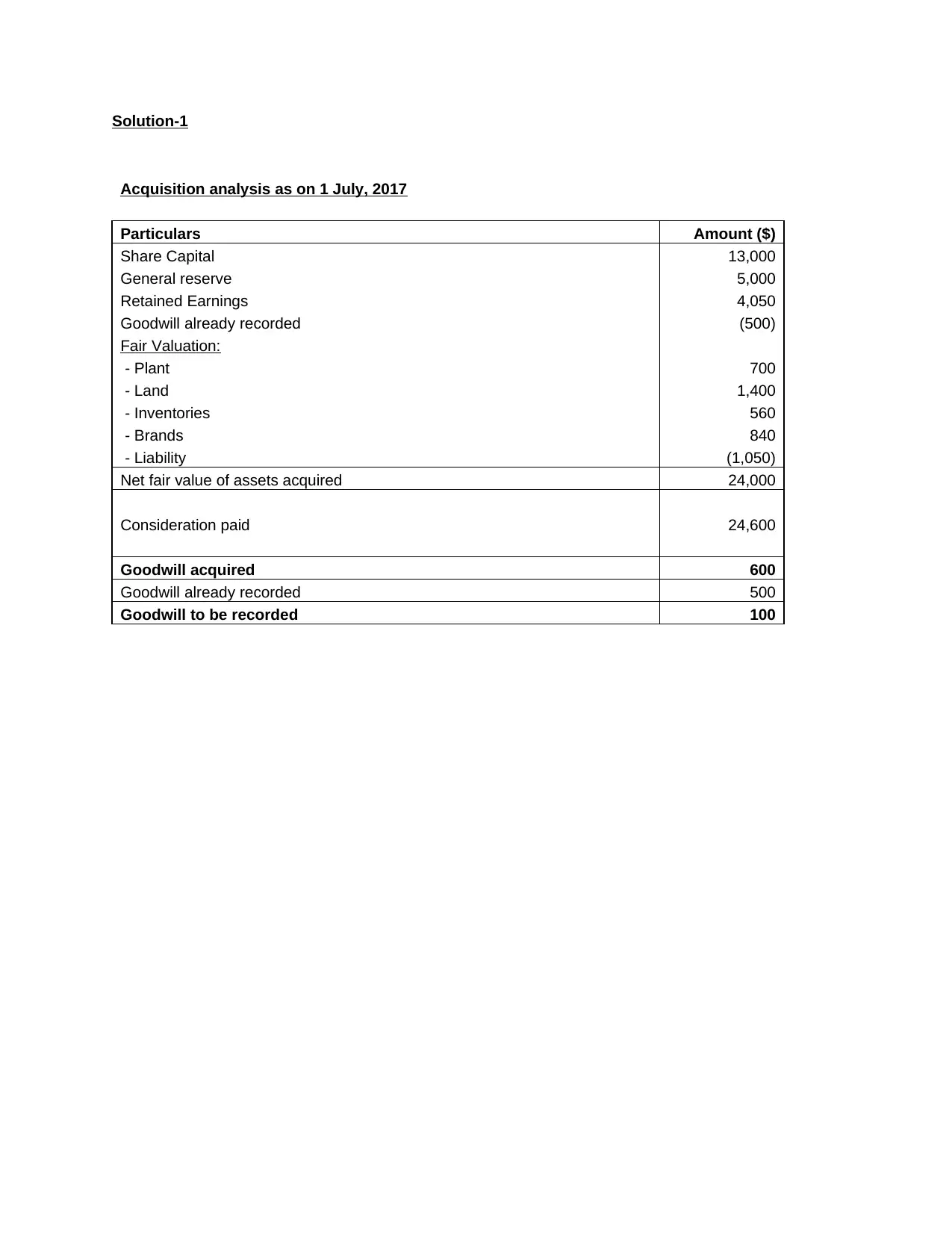

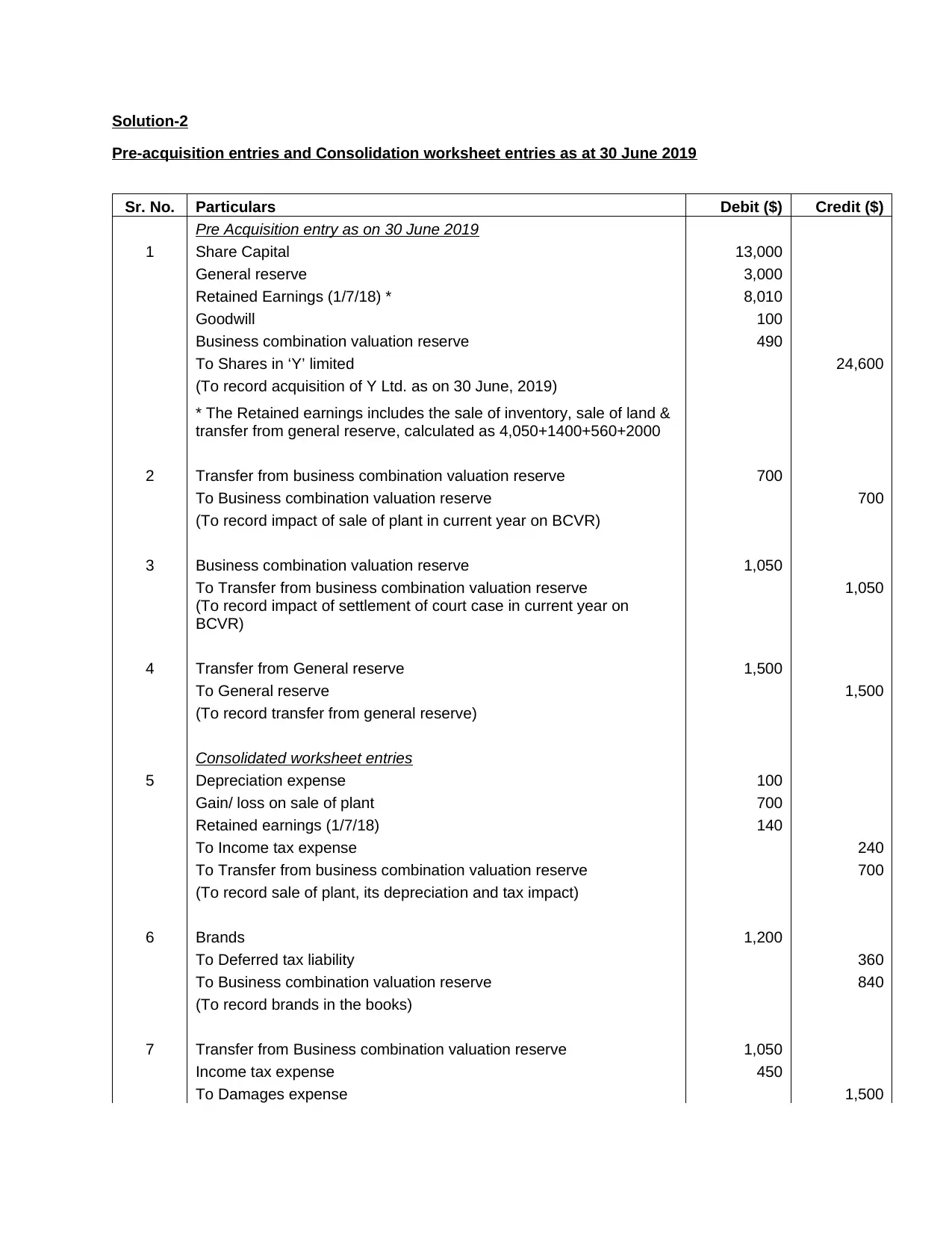

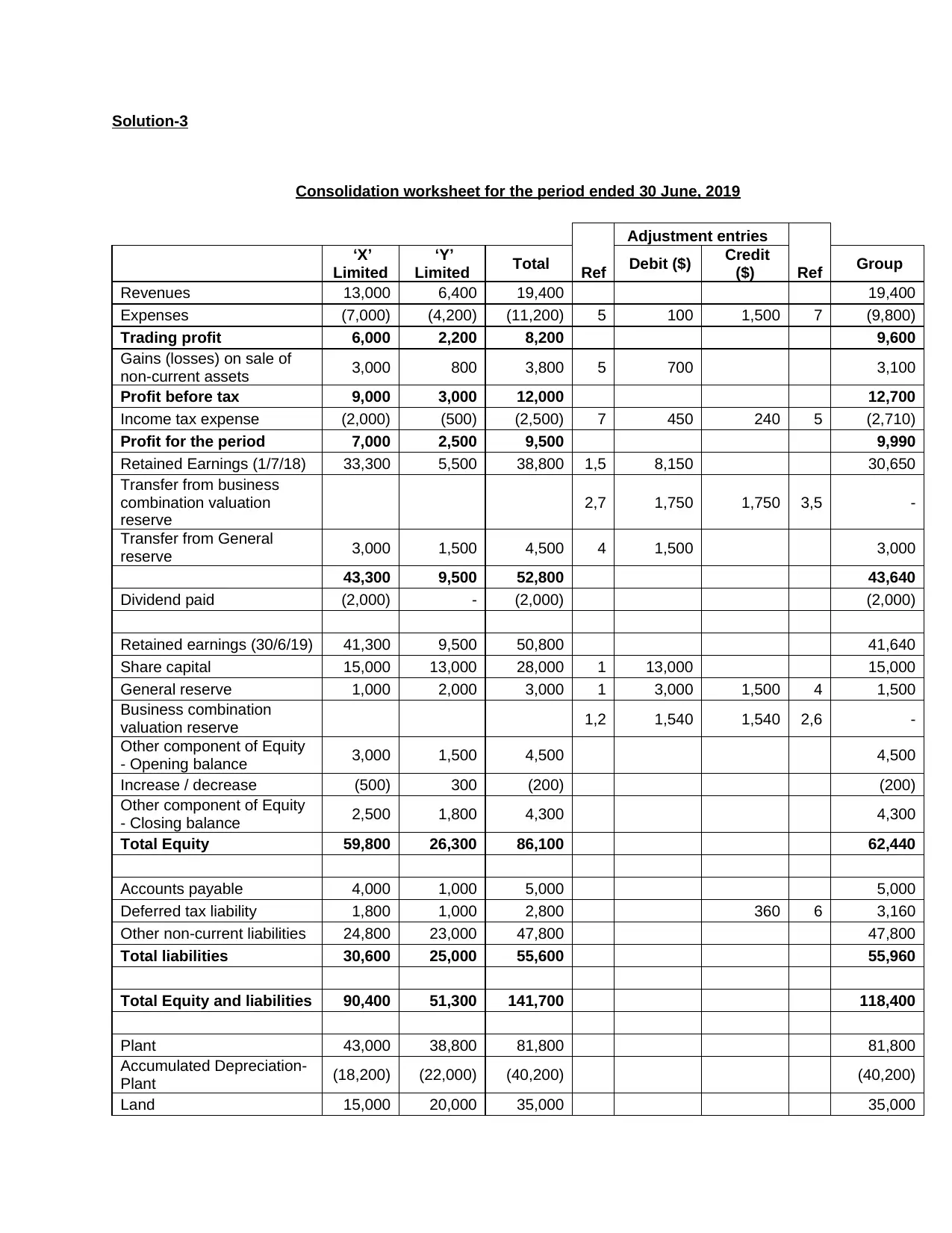

Acquisition Analysis, Consolidation Worksheet, and Financial Reporting

VerifiedAdded on 2022/10/17

|5

|696

|193

Homework Assignment

AI Summary

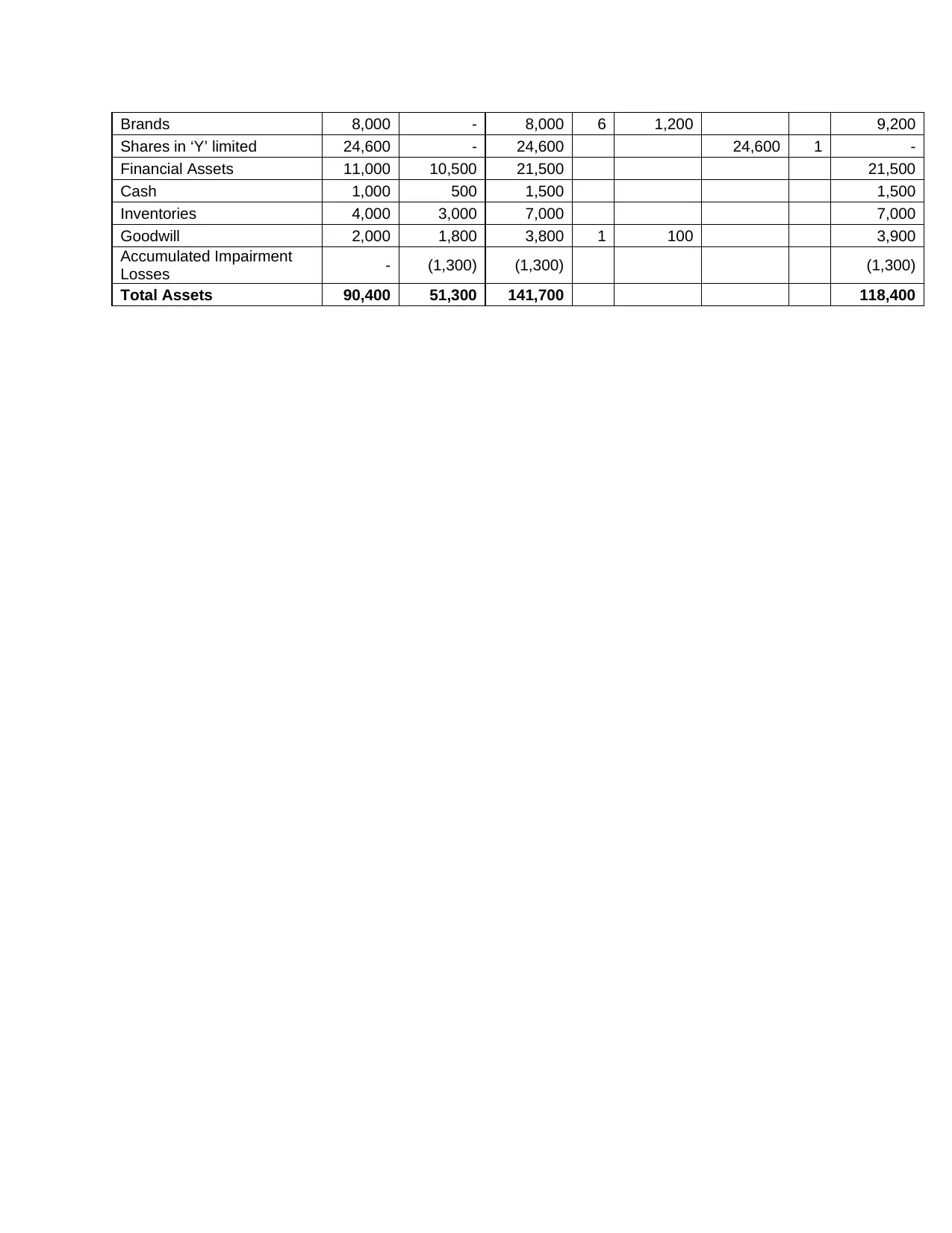

This assignment solution provides a detailed analysis of an acquisition scenario, including the calculation of goodwill, fair valuation adjustments, and pre-acquisition entries. The solution presents the acquisition analysis as of July 1, 2017, followed by pre-acquisition entries and consolidation worksheet entries as of June 30, 2019. The solution includes journal entries to record the acquisition of Y Ltd., transfer from business combination valuation reserve, and transfer from general reserve. Furthermore, the solution provides a comprehensive consolidated worksheet for the period ending June 30, 2019, which includes adjustments for revenues, expenses, and gains/losses. The worksheet also presents the consolidated financial statements, including the statement of profit or loss and other comprehensive income, statement of changes in equity, and the statement of financial position. The solution also addresses the impact of depreciation, sale of plant, and settlement of a court case on the financial statements.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.