ACCT20074 Contemporary Accounting Theory: Financial Reporting

VerifiedAdded on 2023/03/31

|20

|3945

|228

Report

AI Summary

This report provides an analysis of contemporary accounting theory, focusing on the conceptual framework for financial reporting and its application to ASX-listed corporations like REGENEUS LIMITED (RGS). Part A reviews the history and development of the conceptual framework, examines concerns within the Australian accounting profession, discusses academic perspectives on its quality, and explains its application by RGS. Part B compares sustainability reporting guidelines with the International Integrated Reporting Framework and assesses the strengths and limitations of financial statements within the conceptual framework, using Aspen Pharmacare Holdings Ltd as a case study. The report covers key aspects such as the history of the conceptual framework, qualitative characteristics of financial information, and the role of businesses in society today. This document is available on Desklib, a platform offering a wealth of study resources for students.

Running head: CONTEMPORARY ACCOUNTING THEORY 1

Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 2

1. Executive Summary

The prime logic behind formation of the Conceptual Framework within the accounts

department is the objective to recognise primary issues; appropriate during evaluation of

fiscal statements. This Framework provides an opportunity to company executives to assess

their fiscal welfare thus ensuring the firm’s profitability. Taking the latter into account, this

study will implement this scheme to an ASX-listed Corporation: REGENEUS LIMITED

(RGS) additionally clarified in part A, just how the company implements the scheme during

singling out of fiscal statements, chief issues and occasions. Section B outlines a contrast of

sustainable reporting as well as assessment of the reporting framework of the international

integration. In addition, this sector contains an assessment of potency and constraints of fiscal

statements examining the conceptual framework. So as to immensely evaluate the logic

presented by section B, Aspen Pharmacare Holdings Ltd from South Africa will be studied,

in regard to a given index of elements accessible in a comprehensive report.

1. Executive Summary

The prime logic behind formation of the Conceptual Framework within the accounts

department is the objective to recognise primary issues; appropriate during evaluation of

fiscal statements. This Framework provides an opportunity to company executives to assess

their fiscal welfare thus ensuring the firm’s profitability. Taking the latter into account, this

study will implement this scheme to an ASX-listed Corporation: REGENEUS LIMITED

(RGS) additionally clarified in part A, just how the company implements the scheme during

singling out of fiscal statements, chief issues and occasions. Section B outlines a contrast of

sustainable reporting as well as assessment of the reporting framework of the international

integration. In addition, this sector contains an assessment of potency and constraints of fiscal

statements examining the conceptual framework. So as to immensely evaluate the logic

presented by section B, Aspen Pharmacare Holdings Ltd from South Africa will be studied,

in regard to a given index of elements accessible in a comprehensive report.

CONTEMPORARY ACCOUNTING THEORY 3

2. Introduction

The Conceptual Framework (CF) is the key to the fabrication of normalised fiscal

protocols that allow auditors and bookkeepers establish and monitor a firm’s fiscal

statements, important for assessing income statements, crucial for assessing a firm's rate of

returns. Therefore, fiscal statements are pertinent to a firm’s users and stakeholders in order

to basically formulate the conceptual framework, crucial in assessing a company’s monies.

This document hereby considers going about the thesis with regard to application of the

Conceptual framework on two corporations; Aspen Pharmacare Holdings Ltd and

REGENEUS LIMITED (RGS). IASB has chief accreditation in formulation of normalised

and reviewed fiscal guidelines which in turn crucially enable analysts to manage and solve

monetary problems. The Framework hereby enables company administrators in making

fundamental decisions compliant with rigorous protocols.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

The history of developmental progress of the Conceptual Framework dates back to

1976 following the inauguration of the standard by FASB in the USA.in this matter, the CF

formulated was as an obligatory structure with an authority to initiate the desirable protocols

to assert fiscal issues. Between 1970 and 2010, the supervisory organ of the standard

presented eight income statements. SFAC No. 4, a belated scheme supports and is regarded

by the International Accounting Standard Committee (IASC). Established in 1973, this book

keeping body represented a preceding body of accounting criteria body worldwide. Not later

than 1st April 2010, IASB took over responsibility of IASC mandated to put in place the

universal accounting schemes, despite current criteria being a referral to the International

2. Introduction

The Conceptual Framework (CF) is the key to the fabrication of normalised fiscal

protocols that allow auditors and bookkeepers establish and monitor a firm’s fiscal

statements, important for assessing income statements, crucial for assessing a firm's rate of

returns. Therefore, fiscal statements are pertinent to a firm’s users and stakeholders in order

to basically formulate the conceptual framework, crucial in assessing a company’s monies.

This document hereby considers going about the thesis with regard to application of the

Conceptual framework on two corporations; Aspen Pharmacare Holdings Ltd and

REGENEUS LIMITED (RGS). IASB has chief accreditation in formulation of normalised

and reviewed fiscal guidelines which in turn crucially enable analysts to manage and solve

monetary problems. The Framework hereby enables company administrators in making

fundamental decisions compliant with rigorous protocols.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

The history of developmental progress of the Conceptual Framework dates back to

1976 following the inauguration of the standard by FASB in the USA.in this matter, the CF

formulated was as an obligatory structure with an authority to initiate the desirable protocols

to assert fiscal issues. Between 1970 and 2010, the supervisory organ of the standard

presented eight income statements. SFAC No. 4, a belated scheme supports and is regarded

by the International Accounting Standard Committee (IASC). Established in 1973, this book

keeping body represented a preceding body of accounting criteria body worldwide. Not later

than 1st April 2010, IASB took over responsibility of IASC mandated to put in place the

universal accounting schemes, despite current criteria being a referral to the International

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 4

Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In the year 1975, the body

submitted its first reporting of the IAS, which represented the accounting politicking

disclosure (Crombie, 2012).By April 1989, the IASC gave its 28th IAS in which was a

representation of income statements meant for placings in related associates. As a result, the

conceptual framework that had been drafted demonstration and preparation of bookkeeping

frameworks had been endorsed by the IASC by April 1989. Thus the reporting was thereby

published in the year 1989 and the IASB put it into action in 2001, regardless of its relevance

in creation of the framework of the IAS.

The key purpose of the CF is to help the financial body t form International

Accounting Standards in the coming future and facilitate the revising of current criterion

paragraphs (IASB ,2010 b and B 1713) showing the skeleton. The body of accounting

engaged itself in a contract with FASB of the United States known by 2002 as the 2nd

Norwalk Agreement. It mandated the merging of two companies on the foundation of a

quality CF. Due to the joint conference in the year 2004, FASB and IASB accounting

companies accepted to input respective prime features and issues to interconnect the project

to form a uniform Conceptual framework.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The Quasi-legislation states that the need for Constitution-centred CF within Australia

renders it almost impossible to guarantee that recorded accounting schemes are invariable and

logically formulated. Inasmuch As it seems convenient to assess the key principles of

accounting in the word ‘objectives’ with regard to the relevant incomes

statements ,specialists claim the non-strictness of the standards has posed more problems in

Australia. In such a scenario, the Australian Accounting Profession becomes concerned more

Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In the year 1975, the body

submitted its first reporting of the IAS, which represented the accounting politicking

disclosure (Crombie, 2012).By April 1989, the IASC gave its 28th IAS in which was a

representation of income statements meant for placings in related associates. As a result, the

conceptual framework that had been drafted demonstration and preparation of bookkeeping

frameworks had been endorsed by the IASC by April 1989. Thus the reporting was thereby

published in the year 1989 and the IASB put it into action in 2001, regardless of its relevance

in creation of the framework of the IAS.

The key purpose of the CF is to help the financial body t form International

Accounting Standards in the coming future and facilitate the revising of current criterion

paragraphs (IASB ,2010 b and B 1713) showing the skeleton. The body of accounting

engaged itself in a contract with FASB of the United States known by 2002 as the 2nd

Norwalk Agreement. It mandated the merging of two companies on the foundation of a

quality CF. Due to the joint conference in the year 2004, FASB and IASB accounting

companies accepted to input respective prime features and issues to interconnect the project

to form a uniform Conceptual framework.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The Quasi-legislation states that the need for Constitution-centred CF within Australia

renders it almost impossible to guarantee that recorded accounting schemes are invariable and

logically formulated. Inasmuch As it seems convenient to assess the key principles of

accounting in the word ‘objectives’ with regard to the relevant incomes

statements ,specialists claim the non-strictness of the standards has posed more problems in

Australia. In such a scenario, the Australian Accounting Profession becomes concerned more

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 5

with assessment of the functions of CF instead of goals while evaluating a body’s fiscal

statements. It furthermore implies that professions presently reject reasoning lines and

referencing of CF judging from merely objectives in income statements.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF contains potential advantages and limitations in order to be considered a scholarly

concern. In this case, the benefits seen after the implementation of conceptual framework in

the accounting sector:

Because many countries have developed CF, uniform globally, arisen is the

requirement for nations to accept substantial global compatibility on the basic of

various accounting standards (Prosic, 2015). In this case, educational concerns on

principle traits on the criterion’s comparability and conformity over the worldwide

financial reporting .

Education is interested in accounting logic as well as consistency, thus implying

that book keeping standards created following the implementation of CF must be

relevant and consistent.

CF gives the universal fundamentals of accounting schemes.Meaning; standard-setters

are anticipated to be answerable for all their fiscal decisions (Romolini, Fissi & Gori,

2017).

The CF brings an appropriate method of communicating the basic concepts based on

current fiscal reports. Hence, this scheme provides quality guidance for bodies for

good evaluation and accounting standards (Crombie, 2012).

with assessment of the functions of CF instead of goals while evaluating a body’s fiscal

statements. It furthermore implies that professions presently reject reasoning lines and

referencing of CF judging from merely objectives in income statements.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF contains potential advantages and limitations in order to be considered a scholarly

concern. In this case, the benefits seen after the implementation of conceptual framework in

the accounting sector:

Because many countries have developed CF, uniform globally, arisen is the

requirement for nations to accept substantial global compatibility on the basic of

various accounting standards (Prosic, 2015). In this case, educational concerns on

principle traits on the criterion’s comparability and conformity over the worldwide

financial reporting .

Education is interested in accounting logic as well as consistency, thus implying

that book keeping standards created following the implementation of CF must be

relevant and consistent.

CF gives the universal fundamentals of accounting schemes.Meaning; standard-setters

are anticipated to be answerable for all their fiscal decisions (Romolini, Fissi & Gori,

2017).

The CF brings an appropriate method of communicating the basic concepts based on

current fiscal reports. Hence, this scheme provides quality guidance for bodies for

good evaluation and accounting standards (Crombie, 2012).

CONTEMPORARY ACCOUNTING THEORY 6

Accounting-setters will thus undergo minimal political pressure at the time of

formulation additional accounting standards because the key concerns in the goals of

fiscal reports, as well as criterion to recognising them have been well considered after

the CF formulation.

A few of limitations related to accounting conceptual frameworks of include:

Conceptual frameworks are unrealistic to formulate.

Enhancement of CF is influenced by governmental actions. Hence, some bookkeepers

air the concern that CFs is politically oriented.

Related to above mentioned downfall, every time the CF deems involving book

keeping concerns, an issue is related to financial estimation of specific assets occur

as argued by (Molineux & Wilson, 2017).

The CFs takes into account more on money-related matters. In this case, this scheme will

consider disapproving various performance segments like ecological as well as social

disclosing components. Furthermore, through assessment of fiscal execution, CFs crucially

transits the review of financial analysts with regard to corporate execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

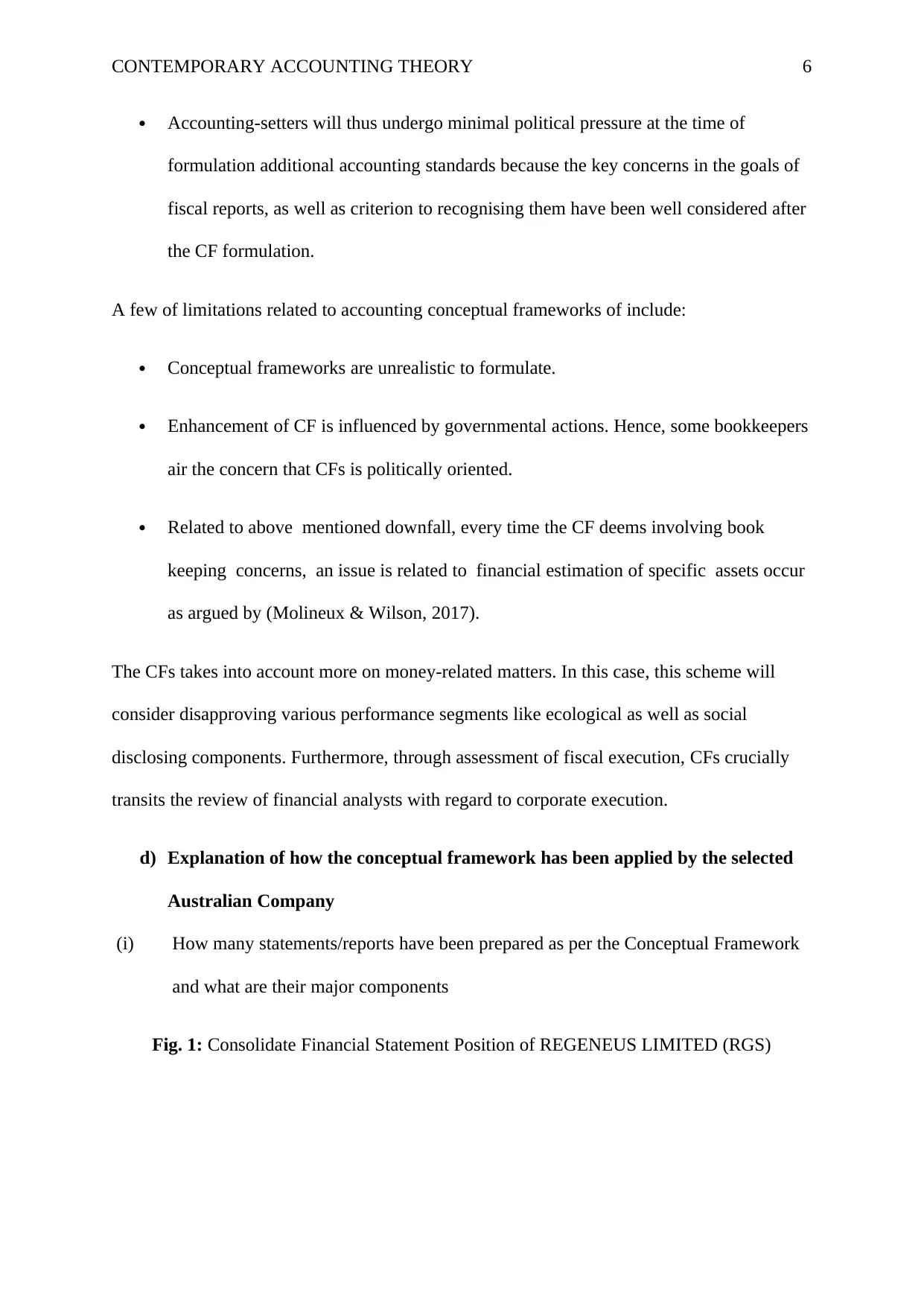

Fig. 1: Consolidate Financial Statement Position of REGENEUS LIMITED (RGS)

Accounting-setters will thus undergo minimal political pressure at the time of

formulation additional accounting standards because the key concerns in the goals of

fiscal reports, as well as criterion to recognising them have been well considered after

the CF formulation.

A few of limitations related to accounting conceptual frameworks of include:

Conceptual frameworks are unrealistic to formulate.

Enhancement of CF is influenced by governmental actions. Hence, some bookkeepers

air the concern that CFs is politically oriented.

Related to above mentioned downfall, every time the CF deems involving book

keeping concerns, an issue is related to financial estimation of specific assets occur

as argued by (Molineux & Wilson, 2017).

The CFs takes into account more on money-related matters. In this case, this scheme will

consider disapproving various performance segments like ecological as well as social

disclosing components. Furthermore, through assessment of fiscal execution, CFs crucially

transits the review of financial analysts with regard to corporate execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

Fig. 1: Consolidate Financial Statement Position of REGENEUS LIMITED (RGS)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 7

Conferring to the Fig. 1 above, the corporation has prepared the fiscal data with respect to the

company’s consolidated income statements, which dealt with the placings subsidiary,

dividends, asset evaluation, and liabilities total.

The company has presented not less than five reports containing major components seen in

all. The features include:

The aims of bookkeeping reporting: FASB's initial Announcement of fiscal and

Accounting Ideas (SFAC 1) (1978) contrasted the extensive destinations of

accounting assessment. The initial and broadest goal expressed in SFAC 1 is to

present helpful data to current as well as potential speculators and different clientele

in formulating the balanced enterprise, comparable choices and credit. From this

Conferring to the Fig. 1 above, the corporation has prepared the fiscal data with respect to the

company’s consolidated income statements, which dealt with the placings subsidiary,

dividends, asset evaluation, and liabilities total.

The company has presented not less than five reports containing major components seen in

all. The features include:

The aims of bookkeeping reporting: FASB's initial Announcement of fiscal and

Accounting Ideas (SFAC 1) (1978) contrasted the extensive destinations of

accounting assessment. The initial and broadest goal expressed in SFAC 1 is to

present helpful data to current as well as potential speculators and different clientele

in formulating the balanced enterprise, comparable choices and credit. From this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

ignition stage in SFAC 1, the REGENEUS LIMITED (RGS) conveyed other

progressively distinct targets.

The cardinal of Useful Fiscal Data: The second constituent within the conceptual

framework is the subjective attributes that budgetary data should have, incise it is to

be precious in elementary leadership. In SFAC 2, the FASB said the data is useful on

the off chance that it is (I) important, (ii) dependable, and (iii) tantamount (Carnevale

& Mazzuca, 2012). Data is relevant on the small chance that it can have a wide range

of effect in a choice. The data thus has this characteristic the moment it enables clients

anticipate the future or evaluate the past and is acquired in order to influence their

choice (Crombie, 2012).

Financial Statement Elements: Another significant advancement in building up a

conceptual framework is to decide the components of budget reports. This includes

characterizing the classes of REGENEUS LIMITED (RGS) data that ought to be

contained in monetary reports. FASB's exchange of fiscal summary components

incorporates meanings of significant components, for example, resources, liabilities,

value, incomes, costs, additions, and misfortunes (Crombie, 2012).

Financial Measurement and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for choosing (1) when things

ought to be introduced (or perceived) in the budget summaries, and (2) how to allocate

numbers to (or measure) financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

ignition stage in SFAC 1, the REGENEUS LIMITED (RGS) conveyed other

progressively distinct targets.

The cardinal of Useful Fiscal Data: The second constituent within the conceptual

framework is the subjective attributes that budgetary data should have, incise it is to

be precious in elementary leadership. In SFAC 2, the FASB said the data is useful on

the off chance that it is (I) important, (ii) dependable, and (iii) tantamount (Carnevale

& Mazzuca, 2012). Data is relevant on the small chance that it can have a wide range

of effect in a choice. The data thus has this characteristic the moment it enables clients

anticipate the future or evaluate the past and is acquired in order to influence their

choice (Crombie, 2012).

Financial Statement Elements: Another significant advancement in building up a

conceptual framework is to decide the components of budget reports. This includes

characterizing the classes of REGENEUS LIMITED (RGS) data that ought to be

contained in monetary reports. FASB's exchange of fiscal summary components

incorporates meanings of significant components, for example, resources, liabilities,

value, incomes, costs, additions, and misfortunes (Crombie, 2012).

Financial Measurement and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for choosing (1) when things

ought to be introduced (or perceived) in the budget summaries, and (2) how to allocate

numbers to (or measure) financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

CONTEMPORARY ACCOUNTING THEORY 9

Generally, the FASB has said that things ought to be perceived in the fiscal summaries in the

event that they meet the accompanying criteria:

Characterizations: The thing meets the meaning of a component of budget reports;

Measurability: It has an important quality quantifiable with adequate dependability

Position: The data about it is equipped for having any kind of effect on client choices;

and

Dependability: The REGENEUS LIMITED (RGS)’s data is illustratively resolute,

irrefutable, and impartial.

In SFAC 5, the FASB has expressed that a full arrangement of budget summaries should

appear: Money related position toward the finish of the period, Profit for the period and

Exhaustive salary for the period. This new idea is more extensive than profit and incorporates

all adjustments in proprietors' value other than those that came about because of exchanges

with the proprietors (Hodge, Rajgopal & Shevlin, 2009). A few changes in resource esteems

are incorporated into this idea however are barred from REGENEUS LIMITED (RGS)

income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

Quantitative characteristics of information shows by the company’s financial reports

include:

Operationalization of the subjective attributes: To build an estimation apparatus, we

use earlier writing which characterizes money related detailing quality as far as the crucial

and upgrading subjective attributes fundamental choice convenience as characterized in the

ED. The basic subjective attributes (for example significance and loyal portrayal) are most

Generally, the FASB has said that things ought to be perceived in the fiscal summaries in the

event that they meet the accompanying criteria:

Characterizations: The thing meets the meaning of a component of budget reports;

Measurability: It has an important quality quantifiable with adequate dependability

Position: The data about it is equipped for having any kind of effect on client choices;

and

Dependability: The REGENEUS LIMITED (RGS)’s data is illustratively resolute,

irrefutable, and impartial.

In SFAC 5, the FASB has expressed that a full arrangement of budget summaries should

appear: Money related position toward the finish of the period, Profit for the period and

Exhaustive salary for the period. This new idea is more extensive than profit and incorporates

all adjustments in proprietors' value other than those that came about because of exchanges

with the proprietors (Hodge, Rajgopal & Shevlin, 2009). A few changes in resource esteems

are incorporated into this idea however are barred from REGENEUS LIMITED (RGS)

income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

Quantitative characteristics of information shows by the company’s financial reports

include:

Operationalization of the subjective attributes: To build an estimation apparatus, we

use earlier writing which characterizes money related detailing quality as far as the crucial

and upgrading subjective attributes fundamental choice convenience as characterized in the

ED. The basic subjective attributes (for example significance and loyal portrayal) are most

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 10

significant and decide the substance of money related detailing data (Alfiero, Cane, Doronzo

& Esposito, 2018). The improving subjective attributes (for example equivalence,

understand-ability, practicality and unquestionable status) can improve choice value when the

crucial subjective attributes are set up. Be that as it may, they cannot decide accounting

detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to

comprehend various concerns raised by clients as suppliers of capital in the company.

Considering the past literature, the relevance of operationalized applying various accounting

elements denotes corroborative and prescient framework. As discussed earlier in this paper,

accountants will critically evaluate the quality of financial earnings instead of accounting

reporting and its quality. This aspect is restrained due to the fact that it ignores non-financial

information and future financial-connected data that is accessible by shareholders. (Mostyn,

2012). In order to enhance the quality extend, extensive and prescient analysis of the

REGENEUS LIMITED (RGS) financial statement is required.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are

applicable in the business world today (Pérez-López, Moreno-Romero, & Barkemeyer,

2013). The role of businesses in the society today is gradually increasing, as compared its

initial obligation of evaluating its profitability or recording its finances. The Sustainability

Reporting Guideline presents the relevant standards applicable to the help companies to

enhance competitive advantage (Ceulemans, Lozano & Alonso-Almeida, 2015). Moreover,

the component of environmental sustainability in the guideline is critically recommended for

significant and decide the substance of money related detailing data (Alfiero, Cane, Doronzo

& Esposito, 2018). The improving subjective attributes (for example equivalence,

understand-ability, practicality and unquestionable status) can improve choice value when the

crucial subjective attributes are set up. Be that as it may, they cannot decide accounting

detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to

comprehend various concerns raised by clients as suppliers of capital in the company.

Considering the past literature, the relevance of operationalized applying various accounting

elements denotes corroborative and prescient framework. As discussed earlier in this paper,

accountants will critically evaluate the quality of financial earnings instead of accounting

reporting and its quality. This aspect is restrained due to the fact that it ignores non-financial

information and future financial-connected data that is accessible by shareholders. (Mostyn,

2012). In order to enhance the quality extend, extensive and prescient analysis of the

REGENEUS LIMITED (RGS) financial statement is required.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are

applicable in the business world today (Pérez-López, Moreno-Romero, & Barkemeyer,

2013). The role of businesses in the society today is gradually increasing, as compared its

initial obligation of evaluating its profitability or recording its finances. The Sustainability

Reporting Guideline presents the relevant standards applicable to the help companies to

enhance competitive advantage (Ceulemans, Lozano & Alonso-Almeida, 2015). Moreover,

the component of environmental sustainability in the guideline is critically recommended for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 11

firms to apply the world today. However, this form of reporting concentrates more on a

selected segment of the entity’s status but unable to indicated the specific and relevant

climatic transitions and environmental factors (Crombie, 2012). Apart from that sustainability

reports do not effectively indicated financial information relevant for evaluating the

opportunities and risks of an entity.

On the other hand, International Integrated Reporting Framework improves the

corporation’s reputation; thus, the profitability of the firm can be evaluated based on global

norms and laws (Messner, 2010). The reporting necessitates investors to build the

relationship with both the accounting and non-accounting data analysts to be able to

effectively evaluate potential risks. Numerous organizations have energetically begun to get

readily integrated reports in different configurations and each report has been shaped as per

the requirements of business properties. Moreover, integrated announcing standards and rules

have been distributed by the Worldwide Integrated Detailing Board, so as to give direction to

report evaluators (Soyka, 2013). With the expanding significance and spread of integrated

detailing, banters about the advantages and issues experienced in the readiness expanded. In

this investigation, the followings are clarified: the terms of monetary announcing,

sustainability analysis, and accounting detailing; the development of these terms; advantages

of integrated revealing and issues that might be experienced while readiness; and the

connection between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

firms to apply the world today. However, this form of reporting concentrates more on a

selected segment of the entity’s status but unable to indicated the specific and relevant

climatic transitions and environmental factors (Crombie, 2012). Apart from that sustainability

reports do not effectively indicated financial information relevant for evaluating the

opportunities and risks of an entity.

On the other hand, International Integrated Reporting Framework improves the

corporation’s reputation; thus, the profitability of the firm can be evaluated based on global

norms and laws (Messner, 2010). The reporting necessitates investors to build the

relationship with both the accounting and non-accounting data analysts to be able to

effectively evaluate potential risks. Numerous organizations have energetically begun to get

readily integrated reports in different configurations and each report has been shaped as per

the requirements of business properties. Moreover, integrated announcing standards and rules

have been distributed by the Worldwide Integrated Detailing Board, so as to give direction to

report evaluators (Soyka, 2013). With the expanding significance and spread of integrated

detailing, banters about the advantages and issues experienced in the readiness expanded. In

this investigation, the followings are clarified: the terms of monetary announcing,

sustainability analysis, and accounting detailing; the development of these terms; advantages

of integrated revealing and issues that might be experienced while readiness; and the

connection between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

CONTEMPORARY ACCOUNTING THEORY 12

The conventional accounting, centred on the CF provides a firm foundation for formulating

future financial statement standards, which enhance the sustainability status of specific

companies. The strength evident in this framework is to permit the introduction of accounting

standards and international integrated reports, which clarify the key matters in financial

statements. Conventional accounting also evaluates key material concerns, i.e. both positive

and negative, in financial statements.

Limitations

Debilitated Basic leadership: Convectional accounting offers decision chiefs little data on an

association's specialties. This is on the grounds that the sort of use the planning procedure

tasks is theoretical and isn't solid for settling on specific choices. This powers chiefs in

governments and associations utilizing traditional planning strategies to change their

arrangements regularly, in order to emphasize their selections.

c) Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Association financial analysists around the globe utilize institutional hypothesis or

neo-institutional theory in their exploration to demonstrate that establishments of monetary,

social, instructive, money related, and political nature keeps up a huge impact upon overall

associations. Badiyani (2012) directs exact research upon 309 organizations chose from

different sources, in particular, GRI reports list, GRI dataset with best customary

sustainability reports, CRRA Reporting Award 2010. Results demonstrate that integrated

revealing is exceedingly associated with the phase of monetary improvement, national

corporate duty, nations' qualities framework, worker's guilds, the private use of tertiary

training, proprietorship scattering. The creators neglected to demonstrate the impact of the

political factor, underlining the irregularity of information with respect to the years for which

The conventional accounting, centred on the CF provides a firm foundation for formulating

future financial statement standards, which enhance the sustainability status of specific

companies. The strength evident in this framework is to permit the introduction of accounting

standards and international integrated reports, which clarify the key matters in financial

statements. Conventional accounting also evaluates key material concerns, i.e. both positive

and negative, in financial statements.

Limitations

Debilitated Basic leadership: Convectional accounting offers decision chiefs little data on an

association's specialties. This is on the grounds that the sort of use the planning procedure

tasks is theoretical and isn't solid for settling on specific choices. This powers chiefs in

governments and associations utilizing traditional planning strategies to change their

arrangements regularly, in order to emphasize their selections.

c) Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Association financial analysists around the globe utilize institutional hypothesis or

neo-institutional theory in their exploration to demonstrate that establishments of monetary,

social, instructive, money related, and political nature keeps up a huge impact upon overall

associations. Badiyani (2012) directs exact research upon 309 organizations chose from

different sources, in particular, GRI reports list, GRI dataset with best customary

sustainability reports, CRRA Reporting Award 2010. Results demonstrate that integrated

revealing is exceedingly associated with the phase of monetary improvement, national

corporate duty, nations' qualities framework, worker's guilds, the private use of tertiary

training, proprietorship scattering. The creators neglected to demonstrate the impact of the

political factor, underlining the irregularity of information with respect to the years for which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.