ACCT20074 Contemporary Accounting Theory: Practical Report T1

VerifiedAdded on 2023/03/30

|14

|2652

|468

Report

AI Summary

This report provides an overview of the conceptual framework for financial reporting, its history, development, and application in various countries, including the USA, UK, and Australia, under the IASB. It discusses the Australian accounting profession's concerns and academic critiques regarding the framework's quality, benefits, and limitations. The report also examines how Spotless Group Holdings Limited applies the conceptual framework. Furthermore, it compares sustainability reporting guidelines with the International Integrated Reporting Framework, analyzes the rigour of conventional accounting in sustainability reporting, and assesses the applicability of theories explaining sustainability reports. Finally, it includes an analysis of Sibanye-Stillwater Ltd's integrated reporting practices and compares them with Spotless' practices.

Running Head: Contemporary Accounting 1

Contemporary Accounting

Name

Institution

Date

Contemporary Accounting

Name

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Accounting 2

Executive Summary

The conceptual framework for financial reporting has been an important analytical tool in many

aspects. The concept has been used in many countries and it has helped standardizes the

accounting procedures. Australia, UK, and the US all have used the conceptual framework

among other boards like the IASB to formulate a consistent and accurate reporting. The

framework is used by domestic and international corporations because of it benefits in the

financial reporting. Although the system has benefits, there are also limitations with the

framework. The financial professionals have had concerns about the conceptual framework.

However many organizations engage in sustainability reporting so that they can they can survive

and compete in this competitive environment.

Executive Summary

The conceptual framework for financial reporting has been an important analytical tool in many

aspects. The concept has been used in many countries and it has helped standardizes the

accounting procedures. Australia, UK, and the US all have used the conceptual framework

among other boards like the IASB to formulate a consistent and accurate reporting. The

framework is used by domestic and international corporations because of it benefits in the

financial reporting. Although the system has benefits, there are also limitations with the

framework. The financial professionals have had concerns about the conceptual framework.

However many organizations engage in sustainability reporting so that they can they can survive

and compete in this competitive environment.

Contemporary Accounting 3

Table of Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Part A: Conceptual framework....................................................................................................................5

Review of the history and development of the Conceptual Framework for Financial Reporting.............5

Explanation of Australian accounting profession’s concerns regarding the Conceptual Framework.......6

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework............................................................................................................................7

Explanation of how the conceptual framework has been applied by the Spotless Group Holdings

Limited....................................................................................................................................................7

Part B: Integrated/sustainability reporting...................................................................................................8

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting Framework.

.................................................................................................................................................................8

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports....................................................9

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as well as

integrated reports...................................................................................................................................10

A table of various components of an integrated report and discussion of whether and how the selected

South African company has disclosed information against each of those components..........................10

Comparison of Spotless’ reporting practices with the index and the integrated reporting practices in

Sibanye- Stillwaters Ltd........................................................................................................................12

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

Table of Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Part A: Conceptual framework....................................................................................................................5

Review of the history and development of the Conceptual Framework for Financial Reporting.............5

Explanation of Australian accounting profession’s concerns regarding the Conceptual Framework.......6

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework............................................................................................................................7

Explanation of how the conceptual framework has been applied by the Spotless Group Holdings

Limited....................................................................................................................................................7

Part B: Integrated/sustainability reporting...................................................................................................8

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting Framework.

.................................................................................................................................................................8

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports....................................................9

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as well as

integrated reports...................................................................................................................................10

A table of various components of an integrated report and discussion of whether and how the selected

South African company has disclosed information against each of those components..........................10

Comparison of Spotless’ reporting practices with the index and the integrated reporting practices in

Sibanye- Stillwaters Ltd........................................................................................................................12

Conclusion.................................................................................................................................................12

References.................................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Accounting 4

Introduction

A conceptual framework is a tool that is applied in very many different categories of work.

(Patrick, 2015). It is a way of declaring or reporting the overall picture of a phenomenon while

following the accepted guidelines. So a conceptual framework for financial reporting is a system

of objectives aimed at creating standards throughout the sector. This paper will focus on the

evolution of the conceptual framework and also how it is applied in financial reporting. The

research will also examine whether corporate organizations have adopted and applied it in their

financial reporting. Many different journals and text books will used as secondary data to

facilitate the research to reach a conclusion. Qualitative data analysis will be used in order to

present a meaningful interpretation of the findings.

Part A: Conceptual framework

Review of the history and development of the Conceptual Framework for Financial

Reporting

A conceptual framework is a way of declaring or reporting the overall picture of a

phenomenon while following the accepted guidelines. (Becker, 2013). So a conceptual

framework for financial reporting can be regarded as an integrated system of comparable

objectives and basics that should result into conformable standards that prescribe the function,

nature of financial statements. The international Accounting Standards Committee (IASC) which

is now a board, was established in the year 1973 by the different professional accounting bodies

from Australia, Germany, United Kingdom, United States and others. The main objectives why

the IASB was formed was to set an accounting standards framework, to form standard guidelines

for resolving disputes in accounting and also to form internationally acceptable principles for

financial reporting.

Introduction

A conceptual framework is a tool that is applied in very many different categories of work.

(Patrick, 2015). It is a way of declaring or reporting the overall picture of a phenomenon while

following the accepted guidelines. So a conceptual framework for financial reporting is a system

of objectives aimed at creating standards throughout the sector. This paper will focus on the

evolution of the conceptual framework and also how it is applied in financial reporting. The

research will also examine whether corporate organizations have adopted and applied it in their

financial reporting. Many different journals and text books will used as secondary data to

facilitate the research to reach a conclusion. Qualitative data analysis will be used in order to

present a meaningful interpretation of the findings.

Part A: Conceptual framework

Review of the history and development of the Conceptual Framework for Financial

Reporting

A conceptual framework is a way of declaring or reporting the overall picture of a

phenomenon while following the accepted guidelines. (Becker, 2013). So a conceptual

framework for financial reporting can be regarded as an integrated system of comparable

objectives and basics that should result into conformable standards that prescribe the function,

nature of financial statements. The international Accounting Standards Committee (IASC) which

is now a board, was established in the year 1973 by the different professional accounting bodies

from Australia, Germany, United Kingdom, United States and others. The main objectives why

the IASB was formed was to set an accounting standards framework, to form standard guidelines

for resolving disputes in accounting and also to form internationally acceptable principles for

financial reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Accounting 5

For all the years until 1929, there had been no private or public body that was charged with

the responsibility of setting accounting standards. So when the stock markets crushed that year,

the stake holders established the securities and Exchange Act in 1934.(Cheung, Evans, Wright,

2015)In the US then the Securities and Exchange Commission (SEC) supervised the public

companies. The Financial Accounting Standards Board (FASB) became the organization

responsible for setting the basic standards for the public companies' financial accounting. The

FASB is non-profit making, private organization with a mission to “to establish and improve

standards of financial accounting and reporting for the guidance and education of the public,

including issuers, auditors, and users of financial information.” the organization was created in

1973 and it replaced the Committee on Accounting Procedure, the American Institute of

Certified Public Accountants (AICPA).

In the past years the Accounting Standards Board (ASB) standards were based on rules rather

than principles. This would encourage the mentality of "tick the box" in the financial reporting

and the idea of judgment was not observed. This method would make it difficult for one to

evaluate whether the objectives of reporting was up to standard. For the United Kingdom to

move away from the rule- based standards of financial reporting, it was important to form a

conceptual frame work. (Gerber, 2015). The UK's Accounting Standards Board issued the

statement of Principles since 1999.

In Australia, in an effort to improve on the financial reporting, the government adopted the

International Financial Reporting Standards (IFRS) in the year 2005. (Australian Accounting

Standards Board, (2018). The Australia's quest for quality financial reporting has undergone

through many years from as early as 1961. The Australian Accounting Standards Board (AASB)

was formed in 2004 to improve the quality of financial reporting in Australia.

For all the years until 1929, there had been no private or public body that was charged with

the responsibility of setting accounting standards. So when the stock markets crushed that year,

the stake holders established the securities and Exchange Act in 1934.(Cheung, Evans, Wright,

2015)In the US then the Securities and Exchange Commission (SEC) supervised the public

companies. The Financial Accounting Standards Board (FASB) became the organization

responsible for setting the basic standards for the public companies' financial accounting. The

FASB is non-profit making, private organization with a mission to “to establish and improve

standards of financial accounting and reporting for the guidance and education of the public,

including issuers, auditors, and users of financial information.” the organization was created in

1973 and it replaced the Committee on Accounting Procedure, the American Institute of

Certified Public Accountants (AICPA).

In the past years the Accounting Standards Board (ASB) standards were based on rules rather

than principles. This would encourage the mentality of "tick the box" in the financial reporting

and the idea of judgment was not observed. This method would make it difficult for one to

evaluate whether the objectives of reporting was up to standard. For the United Kingdom to

move away from the rule- based standards of financial reporting, it was important to form a

conceptual frame work. (Gerber, 2015). The UK's Accounting Standards Board issued the

statement of Principles since 1999.

In Australia, in an effort to improve on the financial reporting, the government adopted the

International Financial Reporting Standards (IFRS) in the year 2005. (Australian Accounting

Standards Board, (2018). The Australia's quest for quality financial reporting has undergone

through many years from as early as 1961. The Australian Accounting Standards Board (AASB)

was formed in 2004 to improve the quality of financial reporting in Australia.

Contemporary Accounting 6

Explanation of Australian accounting profession’s concerns regarding the Conceptual

Framework

The major objectives of the international Accounting Standards Board is the transparency in

the financial reporting however the board has three concerns which have remained unsolved.

There are three concerns will include, the financial statements still don’t have enough

information, there appears to be too much irrelevant information and in some statements, the

information is not communicated well. (Goetz, 2018). These concerns have been and are still top

on the agenda of the IASB. These concerns have caused a lot of controversy, others contend that

may be the information users want from the statements have not been judged to ascertain the

most relevant information.

Discussion of academics’ concerns about the quality (potential benefits and limitations) of

the Conceptual Framework.

The conceptual framework has both benefits and limitations and one of the benefits of the

conceptual frame work is the orderly style that makes financial reporting logical and consistent

with international standards. (Ngeno, 2019). With the conceptual frame work, the setters of the

standard often are able to contain the external pressure which would have led to haphazard rules

and guidelines but because the frame work is well defined, the standards set are more

accountable to the financial accounting report users. The frame work also contributes to the

credibility and yields public confidence regarding financial reporting.

However, the framework also has limitations and has been criticized by scholars that it is based

on many assumptions. It is too general and therefore may not help in practical senses but only in

theoretical academic sense. (Villiers, Rinaldi,Unerman,2014). This even makes it vulnerable to

fraud. (Clendon, T. 2017).

Explanation of Australian accounting profession’s concerns regarding the Conceptual

Framework

The major objectives of the international Accounting Standards Board is the transparency in

the financial reporting however the board has three concerns which have remained unsolved.

There are three concerns will include, the financial statements still don’t have enough

information, there appears to be too much irrelevant information and in some statements, the

information is not communicated well. (Goetz, 2018). These concerns have been and are still top

on the agenda of the IASB. These concerns have caused a lot of controversy, others contend that

may be the information users want from the statements have not been judged to ascertain the

most relevant information.

Discussion of academics’ concerns about the quality (potential benefits and limitations) of

the Conceptual Framework.

The conceptual framework has both benefits and limitations and one of the benefits of the

conceptual frame work is the orderly style that makes financial reporting logical and consistent

with international standards. (Ngeno, 2019). With the conceptual frame work, the setters of the

standard often are able to contain the external pressure which would have led to haphazard rules

and guidelines but because the frame work is well defined, the standards set are more

accountable to the financial accounting report users. The frame work also contributes to the

credibility and yields public confidence regarding financial reporting.

However, the framework also has limitations and has been criticized by scholars that it is based

on many assumptions. It is too general and therefore may not help in practical senses but only in

theoretical academic sense. (Villiers, Rinaldi,Unerman,2014). This even makes it vulnerable to

fraud. (Clendon, T. 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Accounting 7

Explanation of how the conceptual framework has been applied by the Spotless Group

Holdings Limited.

(i)

The profit and loss statement and other statements of incomes are among the two important

documents that have been prepared in consideration of the conceptual frame work. The main

components of these documents are the expenses, incomes, assets and others which are very

significant to the company. The statement of profit and loss states all the income generating

assets, every expenses, and other aspects of the business to show whether the company has made

profit. (www.spotless.com, 2018).

(ii)

In the income statement for Spotless Group Holdings Limited for the year ended 30th June,

2018, the revenues excluding finance income was seen to have decreased. The assets increased

and also the liabilities increased as well. All these parameters were measured and comparability

with 2017 report was done and the liabilities increased and also the assets increased. (Spotless

Report, 2018). The assets were measure basing on their historical value and the figures were

depreciated to ascertain the true values for consideration in the income statement.

(iii)

Spotless Group prepared a comprehensive and detailed financial statement and it followed the

conceptual frame work. The most important aspect of the financial statement is the reliability,

consistency and faithfulness of the information contained in the report. Spotless Group report is

easy to understand by the financial report users and the whole pick of the company is depictive.

Relevant notes were provided for the users to understand and make informed decisions regarding

Spotless Group.

Explanation of how the conceptual framework has been applied by the Spotless Group

Holdings Limited.

(i)

The profit and loss statement and other statements of incomes are among the two important

documents that have been prepared in consideration of the conceptual frame work. The main

components of these documents are the expenses, incomes, assets and others which are very

significant to the company. The statement of profit and loss states all the income generating

assets, every expenses, and other aspects of the business to show whether the company has made

profit. (www.spotless.com, 2018).

(ii)

In the income statement for Spotless Group Holdings Limited for the year ended 30th June,

2018, the revenues excluding finance income was seen to have decreased. The assets increased

and also the liabilities increased as well. All these parameters were measured and comparability

with 2017 report was done and the liabilities increased and also the assets increased. (Spotless

Report, 2018). The assets were measure basing on their historical value and the figures were

depreciated to ascertain the true values for consideration in the income statement.

(iii)

Spotless Group prepared a comprehensive and detailed financial statement and it followed the

conceptual frame work. The most important aspect of the financial statement is the reliability,

consistency and faithfulness of the information contained in the report. Spotless Group report is

easy to understand by the financial report users and the whole pick of the company is depictive.

Relevant notes were provided for the users to understand and make informed decisions regarding

Spotless Group.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Accounting 8

Part B: Integrated/sustainability reporting.

Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework.

The International Integrated Reporting Council (IIRC) is an organization formed by a group of

many stake holders, the regulators, companies, Non-Governmental Organizations, standard

setters. (Villiers, Rinaldi, Unerman, (2014). The whole intention of the group is to encourage

communication about creating value in the corporate world. (integratedreporting.org, 2019).

While the Global Initiative (GRI) is an international body whose mission is to help businesses,

organizations understand the importance of reporting activities or influence of their existence on

the climatic change, corruption and also human rights.

Similarities

All these organizations are responsible for ensuring that the organizations report

according to the sustainability reporting guidelines on how they have impacted the areas where

they operate. They are more focused on how the organizations are to contribute to the future

climatically and economically. The relationship organizations has with the people is important

and always portrayed in the organizations corporate social responsibility. The IIR frame work

puts emphasis on the stakeholders so that they facilitate companies to achieve the CSRs

programs. (Globalreporting.org, 2019).

Difference

Sustainability Reporting is mainly focused on reporting on the organization’s program

regarding the social issues and also the environmental issues. It reports to the public how the

company intends to deal or help with issues concerning the environment and other social issues.

In other words what the company takes as important in its agenda. (Johnson, 2015). On the other

hand, integrated reporting goes further than communicating. It shows what the organization’s

Part B: Integrated/sustainability reporting.

Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework.

The International Integrated Reporting Council (IIRC) is an organization formed by a group of

many stake holders, the regulators, companies, Non-Governmental Organizations, standard

setters. (Villiers, Rinaldi, Unerman, (2014). The whole intention of the group is to encourage

communication about creating value in the corporate world. (integratedreporting.org, 2019).

While the Global Initiative (GRI) is an international body whose mission is to help businesses,

organizations understand the importance of reporting activities or influence of their existence on

the climatic change, corruption and also human rights.

Similarities

All these organizations are responsible for ensuring that the organizations report

according to the sustainability reporting guidelines on how they have impacted the areas where

they operate. They are more focused on how the organizations are to contribute to the future

climatically and economically. The relationship organizations has with the people is important

and always portrayed in the organizations corporate social responsibility. The IIR frame work

puts emphasis on the stakeholders so that they facilitate companies to achieve the CSRs

programs. (Globalreporting.org, 2019).

Difference

Sustainability Reporting is mainly focused on reporting on the organization’s program

regarding the social issues and also the environmental issues. It reports to the public how the

company intends to deal or help with issues concerning the environment and other social issues.

In other words what the company takes as important in its agenda. (Johnson, 2015). On the other

hand, integrated reporting goes further than communicating. It shows what the organization’s

Contemporary Accounting 9

comprehensive plan on how the matters of the environment and social issues are integrated in the

whole of its business plan.

Rigour (strengths & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Conventional accounting helps in generating financial reports to be used by investors of any

business to gauge whether the company is making profit. (Dumay, Bernardi, Guthrie and

Demarthini, 2016). All the internal controls of the organizations are set based on the report

generated by the conventional accounting. Where there are low profits realized, then company

may wish to reduce on the cost of operations and the reverse is true or not. For an organization to

implement a better financial reporting, it has to adopt the conceptual framework for financial

reporting. The organization enjoys flexibility with conventional accounting as there is room for

adjusting between the financial needs of the organization. The limitation of conventional

accounting is, it is expensive to the company because it calls for skilled and experienced

personnel. To formulate a conceptual framework financial report, there are a number of complex

processes which are tedious and require strong mathematical background. This expense erodes

the would be profit for the organization.

Applicability (usefulness or limitations) of the theories to explain contents of sustainability

as well as integrated reports

The institutional theories help portray the real image of the organization or the relationship

the company has with the people. The institutional theories are applied in order to realize the

sustainability and survival of the organization. The problem with the theories is that it does not

give freedom to the institution to utilize its choices to accomplish its own objectives. The

theories are rule based and are not flexible.

comprehensive plan on how the matters of the environment and social issues are integrated in the

whole of its business plan.

Rigour (strengths & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Conventional accounting helps in generating financial reports to be used by investors of any

business to gauge whether the company is making profit. (Dumay, Bernardi, Guthrie and

Demarthini, 2016). All the internal controls of the organizations are set based on the report

generated by the conventional accounting. Where there are low profits realized, then company

may wish to reduce on the cost of operations and the reverse is true or not. For an organization to

implement a better financial reporting, it has to adopt the conceptual framework for financial

reporting. The organization enjoys flexibility with conventional accounting as there is room for

adjusting between the financial needs of the organization. The limitation of conventional

accounting is, it is expensive to the company because it calls for skilled and experienced

personnel. To formulate a conceptual framework financial report, there are a number of complex

processes which are tedious and require strong mathematical background. This expense erodes

the would be profit for the organization.

Applicability (usefulness or limitations) of the theories to explain contents of sustainability

as well as integrated reports

The institutional theories help portray the real image of the organization or the relationship

the company has with the people. The institutional theories are applied in order to realize the

sustainability and survival of the organization. The problem with the theories is that it does not

give freedom to the institution to utilize its choices to accomplish its own objectives. The

theories are rule based and are not flexible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Accounting 10

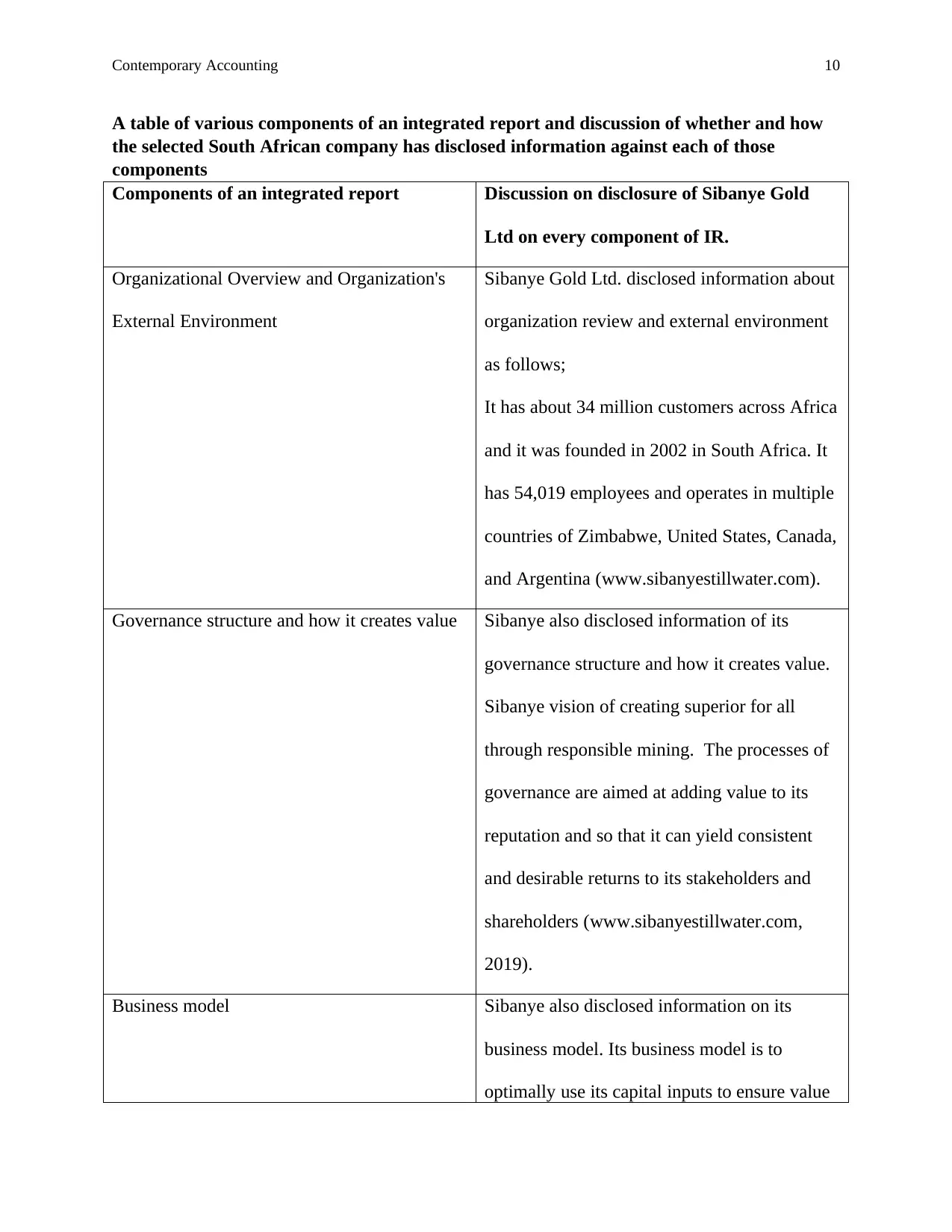

A table of various components of an integrated report and discussion of whether and how

the selected South African company has disclosed information against each of those

components

Components of an integrated report Discussion on disclosure of Sibanye Gold

Ltd on every component of IR.

Organizational Overview and Organization's

External Environment

Sibanye Gold Ltd. disclosed information about

organization review and external environment

as follows;

It has about 34 million customers across Africa

and it was founded in 2002 in South Africa. It

has 54,019 employees and operates in multiple

countries of Zimbabwe, United States, Canada,

and Argentina (www.sibanyestillwater.com).

Governance structure and how it creates value Sibanye also disclosed information of its

governance structure and how it creates value.

Sibanye vision of creating superior for all

through responsible mining. The processes of

governance are aimed at adding value to its

reputation and so that it can yield consistent

and desirable returns to its stakeholders and

shareholders (www.sibanyestillwater.com,

2019).

Business model Sibanye also disclosed information on its

business model. Its business model is to

optimally use its capital inputs to ensure value

A table of various components of an integrated report and discussion of whether and how

the selected South African company has disclosed information against each of those

components

Components of an integrated report Discussion on disclosure of Sibanye Gold

Ltd on every component of IR.

Organizational Overview and Organization's

External Environment

Sibanye Gold Ltd. disclosed information about

organization review and external environment

as follows;

It has about 34 million customers across Africa

and it was founded in 2002 in South Africa. It

has 54,019 employees and operates in multiple

countries of Zimbabwe, United States, Canada,

and Argentina (www.sibanyestillwater.com).

Governance structure and how it creates value Sibanye also disclosed information of its

governance structure and how it creates value.

Sibanye vision of creating superior for all

through responsible mining. The processes of

governance are aimed at adding value to its

reputation and so that it can yield consistent

and desirable returns to its stakeholders and

shareholders (www.sibanyestillwater.com,

2019).

Business model Sibanye also disclosed information on its

business model. Its business model is to

optimally use its capital inputs to ensure value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Accounting 11

creation is sustained in the long run.

(www.sibanyestillwater.com, 2019).

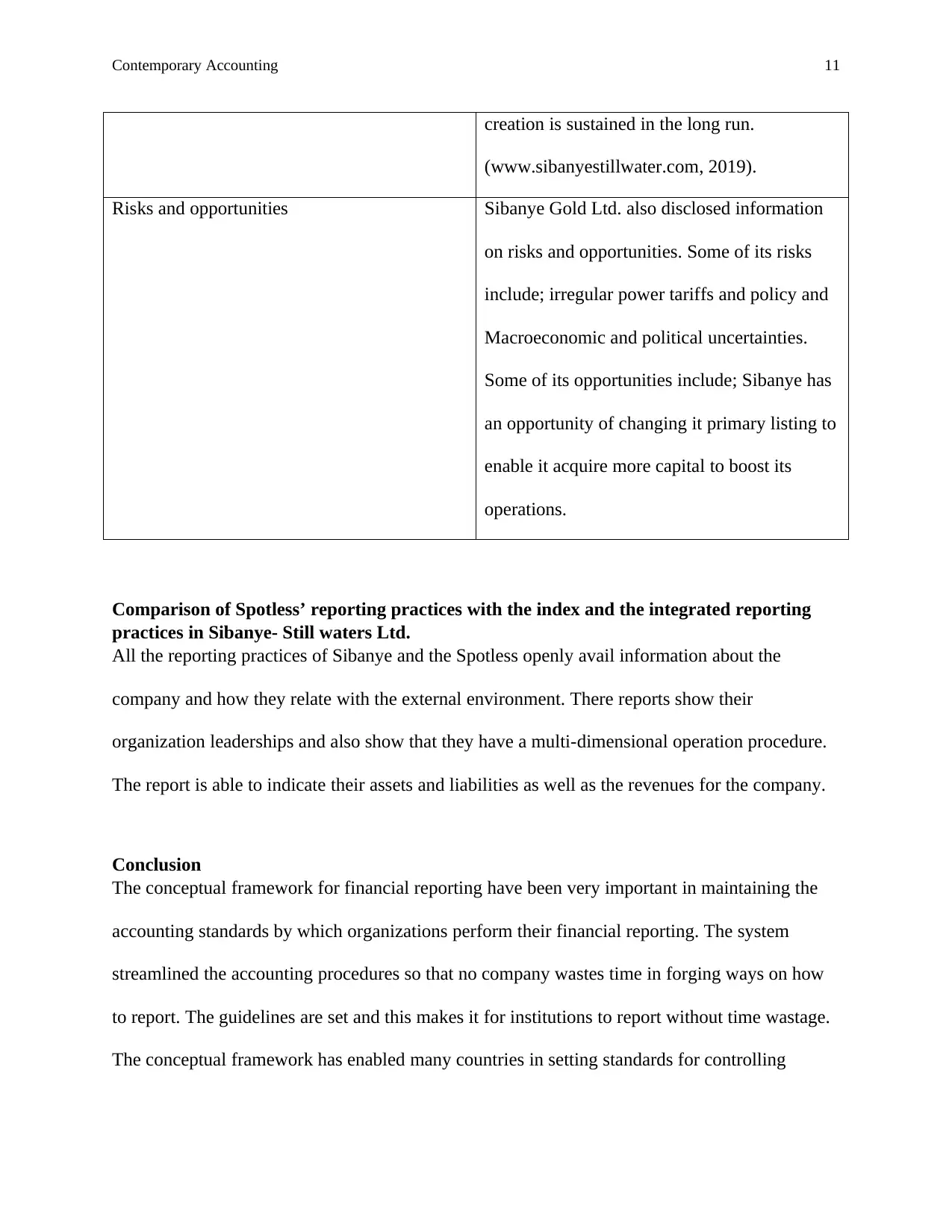

Risks and opportunities Sibanye Gold Ltd. also disclosed information

on risks and opportunities. Some of its risks

include; irregular power tariffs and policy and

Macroeconomic and political uncertainties.

Some of its opportunities include; Sibanye has

an opportunity of changing it primary listing to

enable it acquire more capital to boost its

operations.

Comparison of Spotless’ reporting practices with the index and the integrated reporting

practices in Sibanye- Still waters Ltd.

All the reporting practices of Sibanye and the Spotless openly avail information about the

company and how they relate with the external environment. There reports show their

organization leaderships and also show that they have a multi-dimensional operation procedure.

The report is able to indicate their assets and liabilities as well as the revenues for the company.

Conclusion

The conceptual framework for financial reporting have been very important in maintaining the

accounting standards by which organizations perform their financial reporting. The system

streamlined the accounting procedures so that no company wastes time in forging ways on how

to report. The guidelines are set and this makes it for institutions to report without time wastage.

The conceptual framework has enabled many countries in setting standards for controlling

creation is sustained in the long run.

(www.sibanyestillwater.com, 2019).

Risks and opportunities Sibanye Gold Ltd. also disclosed information

on risks and opportunities. Some of its risks

include; irregular power tariffs and policy and

Macroeconomic and political uncertainties.

Some of its opportunities include; Sibanye has

an opportunity of changing it primary listing to

enable it acquire more capital to boost its

operations.

Comparison of Spotless’ reporting practices with the index and the integrated reporting

practices in Sibanye- Still waters Ltd.

All the reporting practices of Sibanye and the Spotless openly avail information about the

company and how they relate with the external environment. There reports show their

organization leaderships and also show that they have a multi-dimensional operation procedure.

The report is able to indicate their assets and liabilities as well as the revenues for the company.

Conclusion

The conceptual framework for financial reporting have been very important in maintaining the

accounting standards by which organizations perform their financial reporting. The system

streamlined the accounting procedures so that no company wastes time in forging ways on how

to report. The guidelines are set and this makes it for institutions to report without time wastage.

The conceptual framework has enabled many countries in setting standards for controlling

Contemporary Accounting 12

accounting practices. The IASB has been able to formulate accounting standards for the various

entities at domestic and international level.

References

Australian Accounting Standards Board, (2018). Conceptual Framework for Financial

Reporting:Pre- Ballot draft- Conceptual Framework. AASB Meeting, 13 Nov. 2018.

(M168). Agenda item 5.2.

Becker, G, M (2013). The Conceptual Framework in the United Kingdom and the Introduction

of the Statement of Principles. Presentation (Hand Out). 2013. Retrieved from:

https://www.grin.com/document/37091.

Cheung, E., Evans, E., Wright, S. (2015). An historical review of quality in financial reporting in

Australia, Pacific Accounting Review, Vol. 22 Issue: 2, pp.147-169,

https://doi.org/10.1108/01140581011074520

Clendon, T. (2017). IASB's Conceptual Framework for Financial Reporting. Think Ahead.

Retrieved from:

https://www.accaglobal.com/an/en/student/exam-support-resources/fundamentals-exams-

study-resources/f7/technical-articles/iasb-conceptual-framework-financial-reporting.html

accounting practices. The IASB has been able to formulate accounting standards for the various

entities at domestic and international level.

References

Australian Accounting Standards Board, (2018). Conceptual Framework for Financial

Reporting:Pre- Ballot draft- Conceptual Framework. AASB Meeting, 13 Nov. 2018.

(M168). Agenda item 5.2.

Becker, G, M (2013). The Conceptual Framework in the United Kingdom and the Introduction

of the Statement of Principles. Presentation (Hand Out). 2013. Retrieved from:

https://www.grin.com/document/37091.

Cheung, E., Evans, E., Wright, S. (2015). An historical review of quality in financial reporting in

Australia, Pacific Accounting Review, Vol. 22 Issue: 2, pp.147-169,

https://doi.org/10.1108/01140581011074520

Clendon, T. (2017). IASB's Conceptual Framework for Financial Reporting. Think Ahead.

Retrieved from:

https://www.accaglobal.com/an/en/student/exam-support-resources/fundamentals-exams-

study-resources/f7/technical-articles/iasb-conceptual-framework-financial-reporting.html

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.