ACCT20074: Conceptual Framework Application in NAB & Nedbank Analysis

VerifiedAdded on 2023/04/04

|19

|3590

|358

Report

AI Summary

This report provides a financial analysis of National Aust. Bank (NAB) and Nedbank Group Ltd., focusing on the application of the conceptual framework in financial reporting. Part A reviews the history and development of the conceptual framework in the USA, UK, Australia, and globally under the IASB, discussing the Australian accounting profession's concerns and academic perspectives on its quality, benefits, and limitations. It examines how NAB applies the framework, including prepared statements/reports, recognition principles, measurement bases for revenue, assets, and liabilities, and qualitative characteristics of information. Part B contrasts global integrated reporting systems with sustainable reporting rules, analyzing the strengths and limitations of financial accounting rules based on the conceptual framework, comparing Nedbank Group Ltd.'s integrated report against NAB's.

Running Head: FINANCIAL ACCOUNTING 1

National Aust. Bank (NAB) and Nedbank Group Ltd. Financial Analysis

Institution

Name

National Aust. Bank (NAB) and Nedbank Group Ltd. Financial Analysis

Institution

Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 2

Executive Summary

The main notion behind the implementation of the conceptual framework (CF) in financial

accounting if centered on the need of identifying essential elements in the process of assessing

financial statements. The main objective of the conceptual framework is helping firms in

acquiring and assessing financial health status. Therefore, the prospective objective of this paper

will be assessing critically the conceptual framework and how it has been applied in an ASX

stock company: National Aust. Bank (NAB) and how the company has employed the framework

in selecting financial events, statements and events. On the other hand, in section B the paper

will specifically entail contrast of global integrated reporting system over sustainable reporting

rules that entail critical analysis of the strengths and limitations of financial accounting rules

centered on the conceptual framework. Moreover, the paper will also assess the framework

against a South African Company (Nedbank Group Ltd.), based on an index, against the

Australian company’s integrated report.

Executive Summary

The main notion behind the implementation of the conceptual framework (CF) in financial

accounting if centered on the need of identifying essential elements in the process of assessing

financial statements. The main objective of the conceptual framework is helping firms in

acquiring and assessing financial health status. Therefore, the prospective objective of this paper

will be assessing critically the conceptual framework and how it has been applied in an ASX

stock company: National Aust. Bank (NAB) and how the company has employed the framework

in selecting financial events, statements and events. On the other hand, in section B the paper

will specifically entail contrast of global integrated reporting system over sustainable reporting

rules that entail critical analysis of the strengths and limitations of financial accounting rules

centered on the conceptual framework. Moreover, the paper will also assess the framework

against a South African Company (Nedbank Group Ltd.), based on an index, against the

Australian company’s integrated report.

Financial Accounting 3

Introduction

This paper is prospected to outline critical financial rules that are critical and underlie the

procedures used in assessing and laying down the two company’s financial statements and

economic valuation. Considering these financial statements is effectively applied by company’s

key shareholders in efficiently formulating the conceptual framework, which is relevant in

assessing both companies: National Aust. Bank (NAB) and Nedbank Group Ltd. that is the

Australian and the South African companies precisely. Moreover, it is relevant for assessing the

IASB in enactment of revised and standardized accounting rules and procedures that are relevant

for application of financial statements in the two companies while application of financial

protocols or solving problems evident in the compliance of events to prospective accounting

statements. Moreover, the paper will specifically evaluate the conceptual framework as purposed

in financial reporting and it relevancy and application in an Australian company (National Aust.

Bank (NAB). On the other the second section will be evaluating sustainability and integrated

reporting of the conceptual framework for the South African company (Nedbank Group Ltd.).

Part A: Conceptual Framework

a. Review of the history and CF’s

The development of the conceptual framework in the US, UK, Australia was basically prescribed

considering the accounting methods and practices in context 1961 and 1962. In 1965, a theory

was created by Grady centered on analysis of present accounting practices which resulted to

implementation of the Accounting Principles Board (APB). In the long run, there was formation

of a true blood committee in 1972 that formulated the True blood report. The major components

of the report included:

Introduction

This paper is prospected to outline critical financial rules that are critical and underlie the

procedures used in assessing and laying down the two company’s financial statements and

economic valuation. Considering these financial statements is effectively applied by company’s

key shareholders in efficiently formulating the conceptual framework, which is relevant in

assessing both companies: National Aust. Bank (NAB) and Nedbank Group Ltd. that is the

Australian and the South African companies precisely. Moreover, it is relevant for assessing the

IASB in enactment of revised and standardized accounting rules and procedures that are relevant

for application of financial statements in the two companies while application of financial

protocols or solving problems evident in the compliance of events to prospective accounting

statements. Moreover, the paper will specifically evaluate the conceptual framework as purposed

in financial reporting and it relevancy and application in an Australian company (National Aust.

Bank (NAB). On the other the second section will be evaluating sustainability and integrated

reporting of the conceptual framework for the South African company (Nedbank Group Ltd.).

Part A: Conceptual Framework

a. Review of the history and CF’s

The development of the conceptual framework in the US, UK, Australia was basically prescribed

considering the accounting methods and practices in context 1961 and 1962. In 1965, a theory

was created by Grady centered on analysis of present accounting practices which resulted to

implementation of the Accounting Principles Board (APB). In the long run, there was formation

of a true blood committee in 1972 that formulated the True blood report. The major components

of the report included:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 4

⮚ An outline of the 12 objectives relating to accounting and 7 qualitative characteristics

possessed by financial data

⮚ Objective 1: aimed at the needs of financial statements users.

⮚ Objective 1: should cater for clients with restricted ability of requesting financial

data.

On the other hand, in 1974 the Accounting principle board was replaced by the FASB that

directly focused on the conceptual framework project. Moreover, considering this about 6

statement of financial accounting concept was drafted from 1978 to 1985. Initially the first

SFACS was normative although SFAC was linked to the recognition and identification of vast

description of the present practices. Due to this there was much criticism, from 2005 the IASB

and merged with a specific objective of enhancing the revised CF which would be utilized by the

board entirely known as the convergence project. In 1976, UK initial moves considering the aims

and identification of users provided by the corporate reports. The report was specifically focused

in addressing the following:

⮚ Addressing community’s rights and terms of accessing financial data

⮚ In the end, content is entirely not acceptable by the accounting experts.

On the other hand, in 1991 there was adoption of the IASC’s in evaluating the conceptual

framework. The IASC framework was specifically incompliance with the US and Australian

framework consequently was known as an IASB framework. In Australia, the degree of progress

⮚ An outline of the 12 objectives relating to accounting and 7 qualitative characteristics

possessed by financial data

⮚ Objective 1: aimed at the needs of financial statements users.

⮚ Objective 1: should cater for clients with restricted ability of requesting financial

data.

On the other hand, in 1974 the Accounting principle board was replaced by the FASB that

directly focused on the conceptual framework project. Moreover, considering this about 6

statement of financial accounting concept was drafted from 1978 to 1985. Initially the first

SFACS was normative although SFAC was linked to the recognition and identification of vast

description of the present practices. Due to this there was much criticism, from 2005 the IASB

and merged with a specific objective of enhancing the revised CF which would be utilized by the

board entirely known as the convergence project. In 1976, UK initial moves considering the aims

and identification of users provided by the corporate reports. The report was specifically focused

in addressing the following:

⮚ Addressing community’s rights and terms of accessing financial data

⮚ In the end, content is entirely not acceptable by the accounting experts.

On the other hand, in 1991 there was adoption of the IASC’s in evaluating the conceptual

framework. The IASC framework was specifically incompliance with the US and Australian

framework consequently was known as an IASB framework. In Australia, the degree of progress

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 5

is very slow. There are only four statement of accounting concepts (SACs) that were released

which include:

SAC 1: explanation of entity reporting

SAC 2: General aim of financial reporting

SAC 3: various qualitative characteristics of financial data

SAC 4: various definition and recognition of financial elements

SAC 5: considering measurements that were not released.

Australian accounting systems had various similarities to that of the US conceptual framework.

In 2005, there was an adoption of the IASB conceptual framework due to the decision executed

by the financial reporting of the IAS and the IFRS.

b. Explanation of the Australian Accounting Profession

According to Badiyani, (2012), quasi legislation symbolizes that the need of state-based

conceptual in Australian accounting system is not possible in making sure that the accounting

frameworks are accurate and consistent and have been enacted in a clear manner. In spite the fact

that it might be seemingly is inconvenient in assessing essentials of accounting considering the

objectives of the prospective accounting statements, scholars have claimed the ineffectiveness of

the Australian accounting standards has exhibited more accounting problems. Additionally

Adams & Simnett (2011), have provided more concerned with evaluation the conceptual

framework functions instead of its objectives in the evaluation of an entity’s financial statements

(Alfiero, Canel Doronzo, & Esposito, 2018). This further implies that the professions currently

reject the reference and reasoning lines of conceptual framework on the basis on accounting

is very slow. There are only four statement of accounting concepts (SACs) that were released

which include:

SAC 1: explanation of entity reporting

SAC 2: General aim of financial reporting

SAC 3: various qualitative characteristics of financial data

SAC 4: various definition and recognition of financial elements

SAC 5: considering measurements that were not released.

Australian accounting systems had various similarities to that of the US conceptual framework.

In 2005, there was an adoption of the IASB conceptual framework due to the decision executed

by the financial reporting of the IAS and the IFRS.

b. Explanation of the Australian Accounting Profession

According to Badiyani, (2012), quasi legislation symbolizes that the need of state-based

conceptual in Australian accounting system is not possible in making sure that the accounting

frameworks are accurate and consistent and have been enacted in a clear manner. In spite the fact

that it might be seemingly is inconvenient in assessing essentials of accounting considering the

objectives of the prospective accounting statements, scholars have claimed the ineffectiveness of

the Australian accounting standards has exhibited more accounting problems. Additionally

Adams & Simnett (2011), have provided more concerned with evaluation the conceptual

framework functions instead of its objectives in the evaluation of an entity’s financial statements

(Alfiero, Canel Doronzo, & Esposito, 2018). This further implies that the professions currently

reject the reference and reasoning lines of conceptual framework on the basis on accounting

Financial Accounting 6

’objectives’ in the evaluation of financial statements (Aasb.gov.au., 2019). The main reason for

this is that, the existence of the urged to establish the under-pinning accounting frameworks

falters short-term accounting objectives.

c. Academic Concerns

The conceptual framework has potential benefits and limitations to consider as an academic

concern. In that case, here are the benefits evident following the introduction of the framework in

the accounting industry.

⮚ According to Aasb.gov.au. (2019), many nations have established CF, which is similar

globally (or might have alternatively adopted the IASC frameworks), there is the need for

countries to embrace considerable global compatibility on the basic of various accounting

standards. In that case, academic’s concern on quality features on the standard’s

comparability and consistency over the global financial reporting (whereby professions

argues that it is relevant for the evaluation of foreign investment capitals and flows.

⮚ Adams, & Simnett (2011), argues that with accounting logic and consistency, which

implies that accounting standards established following the application of CF should be

logical and consistent.

⮚ CF provides the global fundamentals of accounting systems. In that case, the standard-

setters are expected to be accountable for all their financial decisions. In case these

decisions are retrieved from key concerns evaluated in the CF, the accounting professions

expect the standards to be clear thereby necessitating more explanation prior the

implementation (Alfiero, Cane, Doronzo, & Esposito, 2018).

’objectives’ in the evaluation of financial statements (Aasb.gov.au., 2019). The main reason for

this is that, the existence of the urged to establish the under-pinning accounting frameworks

falters short-term accounting objectives.

c. Academic Concerns

The conceptual framework has potential benefits and limitations to consider as an academic

concern. In that case, here are the benefits evident following the introduction of the framework in

the accounting industry.

⮚ According to Aasb.gov.au. (2019), many nations have established CF, which is similar

globally (or might have alternatively adopted the IASC frameworks), there is the need for

countries to embrace considerable global compatibility on the basic of various accounting

standards. In that case, academic’s concern on quality features on the standard’s

comparability and consistency over the global financial reporting (whereby professions

argues that it is relevant for the evaluation of foreign investment capitals and flows.

⮚ Adams, & Simnett (2011), argues that with accounting logic and consistency, which

implies that accounting standards established following the application of CF should be

logical and consistent.

⮚ CF provides the global fundamentals of accounting systems. In that case, the standard-

setters are expected to be accountable for all their financial decisions. In case these

decisions are retrieved from key concerns evaluated in the CF, the accounting professions

expect the standards to be clear thereby necessitating more explanation prior the

implementation (Alfiero, Cane, Doronzo, & Esposito, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 7

⮚ The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the

best guidance for entities to reports on particular accounting standards and evaluation any

financial concern.

⮚ Accounting-setters will experience minimal political pressure during the formulation of

more accounting standards since the relevant concerns like the objectives of financial

reports, criterion to recognition have been considered following the establishment of the

CF.

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

⮚ Conceptual frameworks are outrageous to formulate.

⮚ The enhancement of the CF is affected by the governmental actions. With this, Badiyani,

(2012), present the concern that CFs is more inclined to political procedures.

⮚ Linked to the limitation outlined above, whenever the CF considers involving accounting

concerns, there is always an issue of financial estimation of given assets

The CFs considers more on financial-related matters. In that case, this framework will consider

disregarding various execution segments such as ecological and social revealing components.

Moreover, through the evaluation of financial execution, CFs critically transits the consideration

of financial analysts based on corporate execution.

⮚ The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the

best guidance for entities to reports on particular accounting standards and evaluation any

financial concern.

⮚ Accounting-setters will experience minimal political pressure during the formulation of

more accounting standards since the relevant concerns like the objectives of financial

reports, criterion to recognition have been considered following the establishment of the

CF.

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

⮚ Conceptual frameworks are outrageous to formulate.

⮚ The enhancement of the CF is affected by the governmental actions. With this, Badiyani,

(2012), present the concern that CFs is more inclined to political procedures.

⮚ Linked to the limitation outlined above, whenever the CF considers involving accounting

concerns, there is always an issue of financial estimation of given assets

The CFs considers more on financial-related matters. In that case, this framework will consider

disregarding various execution segments such as ecological and social revealing components.

Moreover, through the evaluation of financial execution, CFs critically transits the consideration

of financial analysts based on corporate execution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 8

d. Application of the conceptual framework

a) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework and

what are their major components

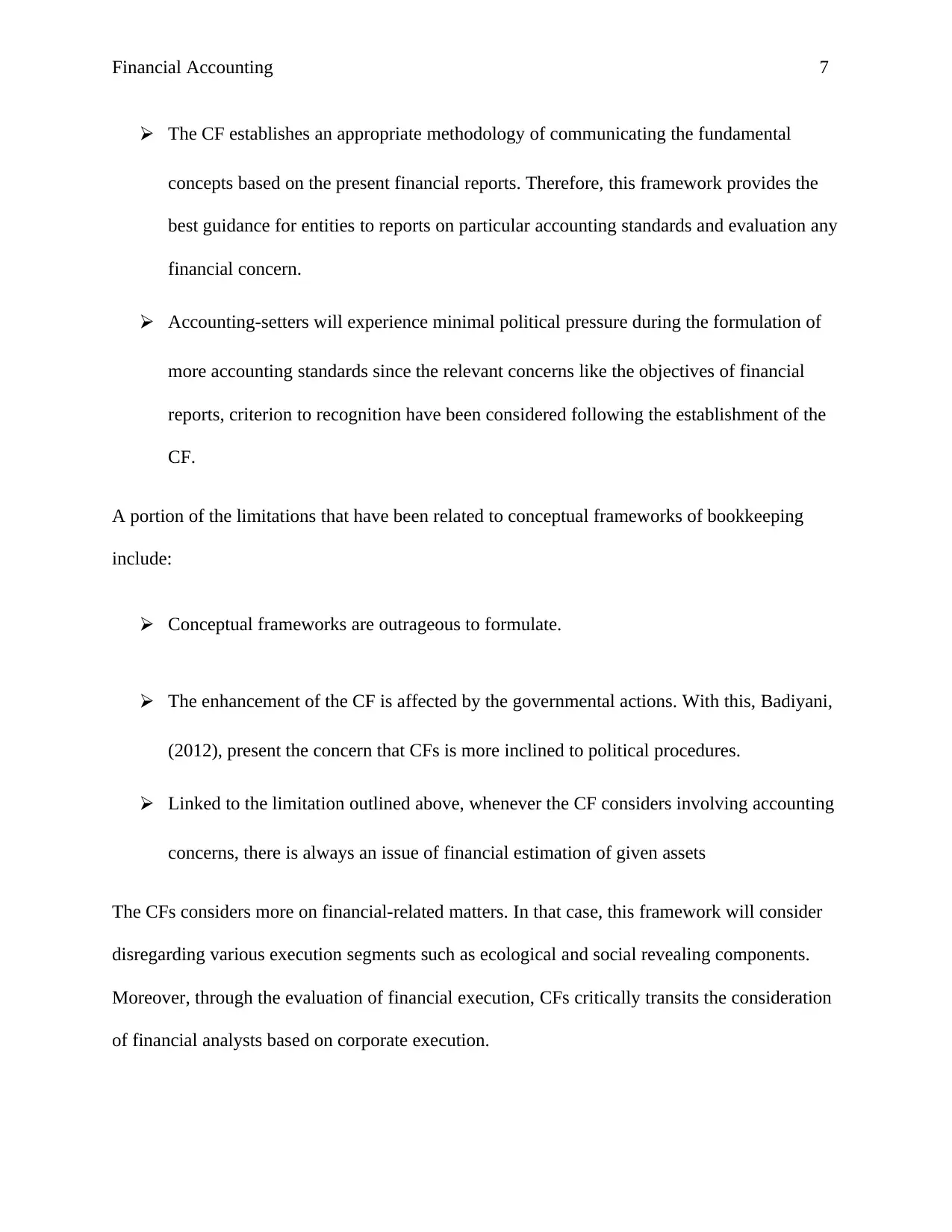

Fig. 1: Consolidate Financial Statement Position of National Aust. Bank (NAB)

Source: https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.

According to the Fig. 1 above, the company has prepared its financial data considering the

company’s consolidated financial statements, which only eliminated the investment subsidiary,

dividends, including profits and loss. The company has produced more than four reports having

major components evident in all. The Components include:

d. Application of the conceptual framework

a) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework and

what are their major components

Fig. 1: Consolidate Financial Statement Position of National Aust. Bank (NAB)

Source: https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.

According to the Fig. 1 above, the company has prepared its financial data considering the

company’s consolidated financial statements, which only eliminated the investment subsidiary,

dividends, including profits and loss. The company has produced more than four reports having

major components evident in all. The Components include:

Financial Accounting 9

⮚ The purposes of accounting reporting: FASB's first Announcement of financial and

Accounting Ideas (SFAC 1) (1978) distinguished the expansive destinations of

accounting evaluation. The first and broadest goal expressed in SFAC 1 is to give data

that is helpful to present and potential speculators and different clients in making the

balanced venture, credit, and comparable choices. From this starting point in SFAC 1, the

National Aust. Bank (NAB) communicated other progressively explicit targets.

⮚ The Fundamental of Useful Financial Data: The second component in the conceptual

framework is the characteristics (or subjective attributes) that budgetary data ought to

have in the event that it is to be valuable in basic leadership.

⮚ In SFAC 2, the FASB said that data is helpful on the off chance that it is (I) important,

(ii) dependable, and (iii) tantamount. Data is pertinent on the off chance that it can have

any kind of effect in a choice. The data has this quality when it enables clients to

anticipate the future or assess the past and is gotten so as to influence their choices.

⮚ Financial Statement Elements: Another significant advancement in building up a

conceptual framework is to decide the components of budget reports. This includes

characterizing the classes of National Aust. Bank (NAB) data that ought to be contained

in monetary reports. FASB's exchange of fiscal summary components incorporates

meanings of significant components, for example, resources, liabilities, value, incomes,

costs, additions, and misfortunes.

Financial Measurement and Recognition: In SFAC 3, ‘Acknowledgment and Estimation in Fiscal

summaries of Business Ventures’, the FASB set up ideas for choosing when things ought to be

⮚ The purposes of accounting reporting: FASB's first Announcement of financial and

Accounting Ideas (SFAC 1) (1978) distinguished the expansive destinations of

accounting evaluation. The first and broadest goal expressed in SFAC 1 is to give data

that is helpful to present and potential speculators and different clients in making the

balanced venture, credit, and comparable choices. From this starting point in SFAC 1, the

National Aust. Bank (NAB) communicated other progressively explicit targets.

⮚ The Fundamental of Useful Financial Data: The second component in the conceptual

framework is the characteristics (or subjective attributes) that budgetary data ought to

have in the event that it is to be valuable in basic leadership.

⮚ In SFAC 2, the FASB said that data is helpful on the off chance that it is (I) important,

(ii) dependable, and (iii) tantamount. Data is pertinent on the off chance that it can have

any kind of effect in a choice. The data has this quality when it enables clients to

anticipate the future or assess the past and is gotten so as to influence their choices.

⮚ Financial Statement Elements: Another significant advancement in building up a

conceptual framework is to decide the components of budget reports. This includes

characterizing the classes of National Aust. Bank (NAB) data that ought to be contained

in monetary reports. FASB's exchange of fiscal summary components incorporates

meanings of significant components, for example, resources, liabilities, value, incomes,

costs, additions, and misfortunes.

Financial Measurement and Recognition: In SFAC 3, ‘Acknowledgment and Estimation in Fiscal

summaries of Business Ventures’, the FASB set up ideas for choosing when things ought to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 10

introduced (or perceived) in the budget summaries, and how to allocate numbers to (or measure)

financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

Generally, the FASB has said that things ought to be perceived in the fiscal summaries in the

event that they meet the accompanying criteria:

⮚ Characterizations: The thing meets the meaning of a component of budget reports;

⮚ Measurability: It has an important quality quantifiable with adequate dependability

⮚ Position: The data about it is equipped for having any kind of effect on client choices;

and

⮚ Dependability: The National Aust. Bank (NAB) data is illustratively resolute, irrefutable,

and impartial.

In SFAC 4, the FASB has expressed that a full arrangement of budget summaries should appear:

Money related position toward the finish of the period, Profit for the period and Exhaustive

salary for the period. This new idea is more extensive than profit and incorporates all

adjustments in proprietors' value other than those that came about because of exchanges with the

proprietors. A few changes in resource esteems are incorporated into this idea however are

barred from National Aust. Bank (NAB) income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

introduced (or perceived) in the budget summaries, and how to allocate numbers to (or measure)

financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

Generally, the FASB has said that things ought to be perceived in the fiscal summaries in the

event that they meet the accompanying criteria:

⮚ Characterizations: The thing meets the meaning of a component of budget reports;

⮚ Measurability: It has an important quality quantifiable with adequate dependability

⮚ Position: The data about it is equipped for having any kind of effect on client choices;

and

⮚ Dependability: The National Aust. Bank (NAB) data is illustratively resolute, irrefutable,

and impartial.

In SFAC 4, the FASB has expressed that a full arrangement of budget summaries should appear:

Money related position toward the finish of the period, Profit for the period and Exhaustive

salary for the period. This new idea is more extensive than profit and incorporates all

adjustments in proprietors' value other than those that came about because of exchanges with the

proprietors. A few changes in resource esteems are incorporated into this idea however are

barred from National Aust. Bank (NAB) income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 11

Quantitative characteristics of information shows by the company’s financial reports include:

Operationalization of the subjective attributes: To build an estimation apparatus, we use earlier

writing which characterizes money related detailing quality as far as the crucial and upgrading

subjective attributes fundamental choice convenience as characterized in the ED. The basic

subjective attributes (for example significance and loyal portrayal) are most significant and

decide the substance of money related detailing data. The improving subjective attributes (for

example equivalence, understand-ability, practicality and unquestionable status) can improve

choice value when the crucial subjective attributes are set up. Be that as it may, they cannot

decide accounting detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to comprehend

various concerns raised by clients as suppliers of capital in the company. Considering the past

literature, the relevance of operationalized applying various accounting elements denotes

corroborative and prescient framework. As discussed earlier in this paper, accountants will

critically evaluate the quality of financial earnings instead of accounting reporting and its quality.

This aspect is restrained due to the fact that it ignores non-financial information and future

financial-connected data that is accessible by shareholders. In order to enhance the quality,

extend, extensive and prescient analysis of the National Aust. Bank (NAB) financial statement is

required.

Quantitative characteristics of information shows by the company’s financial reports include:

Operationalization of the subjective attributes: To build an estimation apparatus, we use earlier

writing which characterizes money related detailing quality as far as the crucial and upgrading

subjective attributes fundamental choice convenience as characterized in the ED. The basic

subjective attributes (for example significance and loyal portrayal) are most significant and

decide the substance of money related detailing data. The improving subjective attributes (for

example equivalence, understand-ability, practicality and unquestionable status) can improve

choice value when the crucial subjective attributes are set up. Be that as it may, they cannot

decide accounting detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to comprehend

various concerns raised by clients as suppliers of capital in the company. Considering the past

literature, the relevance of operationalized applying various accounting elements denotes

corroborative and prescient framework. As discussed earlier in this paper, accountants will

critically evaluate the quality of financial earnings instead of accounting reporting and its quality.

This aspect is restrained due to the fact that it ignores non-financial information and future

financial-connected data that is accessible by shareholders. In order to enhance the quality,

extend, extensive and prescient analysis of the National Aust. Bank (NAB) financial statement is

required.

Financial Accounting 12

Part B: Integrated/sustainability reporting

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are applicable in the

business world today. The role of businesses in the society today is gradually increasing, as

compared its initial obligation of evaluating its profitability or recording its finances. The

Sustainability Reporting Guideline presents the relevant standards applicable to the help

companies to enhance competitive advantage. International Integrated Reporting Framework

improves the corporation’s reputation; thus, the profitability of the firm can be evaluated based

on global norms and laws (Aasb.gov.au., 2019). The reporting necessitates investors to build the

relationship with both the accounting and non-accounting data analysts to be able to effectively

evaluate potential risks. Numerous organizations have energetically begun to get readily

integrated reports in different configurations and each report has been shaped as per the

requirements of business properties. Moreover, integrated announcing standards and rules have

been distributed by the Worldwide Integrated Detailing Board, so as to give direction to report

regulators.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strengths

The conventional accounting, centred on the CF provides a firm foundation for formulating

future financial statement standards, which enhance the sustainability status of specific

companies. The strength evident in this framework is to permit the introduction of accounting

Part B: Integrated/sustainability reporting

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are applicable in the

business world today. The role of businesses in the society today is gradually increasing, as

compared its initial obligation of evaluating its profitability or recording its finances. The

Sustainability Reporting Guideline presents the relevant standards applicable to the help

companies to enhance competitive advantage. International Integrated Reporting Framework

improves the corporation’s reputation; thus, the profitability of the firm can be evaluated based

on global norms and laws (Aasb.gov.au., 2019). The reporting necessitates investors to build the

relationship with both the accounting and non-accounting data analysts to be able to effectively

evaluate potential risks. Numerous organizations have energetically begun to get readily

integrated reports in different configurations and each report has been shaped as per the

requirements of business properties. Moreover, integrated announcing standards and rules have

been distributed by the Worldwide Integrated Detailing Board, so as to give direction to report

regulators.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strengths

The conventional accounting, centred on the CF provides a firm foundation for formulating

future financial statement standards, which enhance the sustainability status of specific

companies. The strength evident in this framework is to permit the introduction of accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.