ACCT20074 Contemporary Accounting Theory: Practical Report

VerifiedAdded on 2023/03/31

|13

|4008

|282

Report

AI Summary

This report examines the conceptual framework for financial reporting and integrated reporting practices, with a focus on their development, benefits, and limitations. Part A reviews the history and development of the conceptual framework, discusses concerns from the Australian accounting profession and academics, and illustrates its application by Oil Search Limited. Part B compares Sustainability Reporting Guidelines and the International Integrated Reporting Framework, assesses the rigor and applicability of conventional accounting, and presents an index for evaluating integrated reports. It also compares the reporting practices of Oil Search Limited with those of Exxaro Resources Ltd, a South African company, against the developed index, highlighting the practical implications and differences in their approaches to integrated reporting. The report uses the annual reports of Oil Search Ltd. and Exxaro Resources Ltd. to highlight how these two topics find its use practically.

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

PART A.........................................................................................................................................................2

Review of the history and the development of the Conceptual Framework for Financial Reporting-.....2

Explanation of Australian accounting profession’s concerns regarding the Conceptual Framework-.....3

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework...........................................................................................................................3

Explanation of how the conceptual framework has been applied by Oil Search Limited........................4

PART B.........................................................................................................................................................5

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting Framework

.................................................................................................................................................................5

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports..................................................6

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as well as

integrated reports...................................................................................................................................6

Preparation of an index (a table or checklist) of various components (criteria) of an integrated report,

and discussion of whether and how the selected South African company has disclosed information

against each of those components (criteria)...........................................................................................7

Comparison of Australian company’s reporting practices with the index and the integrated reporting

practices in the selected South African company....................................................................................9

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

PART A.........................................................................................................................................................2

Review of the history and the development of the Conceptual Framework for Financial Reporting-.....2

Explanation of Australian accounting profession’s concerns regarding the Conceptual Framework-.....3

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework...........................................................................................................................3

Explanation of how the conceptual framework has been applied by Oil Search Limited........................4

PART B.........................................................................................................................................................5

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting Framework

.................................................................................................................................................................5

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports..................................................6

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as well as

integrated reports...................................................................................................................................6

Preparation of an index (a table or checklist) of various components (criteria) of an integrated report,

and discussion of whether and how the selected South African company has disclosed information

against each of those components (criteria)...........................................................................................7

Comparison of Australian company’s reporting practices with the index and the integrated reporting

practices in the selected South African company....................................................................................9

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

A conceptual framework is a multi-variation and background conceptual model. It can be

enforced where an overall effect is required in various categories of work. It is used to

differentiate thematically and to arrange theories. Robust theoretical frameworks catch

something actual and do so in a manner which can be easily recalled and implemented.

Integrated reporting (IR) in big business interaction is a "method which leads to interaction,

most noticeably an" embedded study "on creating value over period. An integrated report is a

descriptive interaction on how the approach, accountability, quality and perspective of an

organization translate to value creation over the short, medium and long term."

INTRODUCTION

This paper deals with discussion on conceptual framework and Integrated reporting on how

they work, what are their drawbacks and can they be useful. An Australian Company called Oil

Research Ltd. and a South African Company called Exxaro Resources Ltd. annual report has

been used to highlight how these two topics find its use practically.

PART A

Review of the history and the development of the Conceptual Framework for Financial

Reporting-

In several European nations, the main function of financial reporting has traditionally been

distinct from the role of financial market roles in certain nations. This is since there hasn't been

any such heavy dependence on openly elevated finance in Europe historically. Alternatively,

finance has often been given by a restricted number of investors (such as banking institutions)

who have been ready to explicitly state the concrete information they wished to obtain from

the entity because of their' proximity' to the organization (with these information becoming

integrated into' specific purpose financial reports').With the growing globalism of enterprises as

well as financial markets, moreover, the position of financial reporting conducted by large

businesses across all European nations has now been generally concentrated on financial data

regulations for financial markets, with the result that provisions have created over a significant

period of time in financial markets controlled economies (with a large number of competing

stocks).While financial accounting exercise can be traced many centuries, financial accounting

legislation usually started in the twentieth century in many other capital-market-dominated

nations (like the United States, the United Kingdom, Ireland, Australia and Canada). Mainly this

lack of transparency in the early stages could have been based on the fact that there was

A conceptual framework is a multi-variation and background conceptual model. It can be

enforced where an overall effect is required in various categories of work. It is used to

differentiate thematically and to arrange theories. Robust theoretical frameworks catch

something actual and do so in a manner which can be easily recalled and implemented.

Integrated reporting (IR) in big business interaction is a "method which leads to interaction,

most noticeably an" embedded study "on creating value over period. An integrated report is a

descriptive interaction on how the approach, accountability, quality and perspective of an

organization translate to value creation over the short, medium and long term."

INTRODUCTION

This paper deals with discussion on conceptual framework and Integrated reporting on how

they work, what are their drawbacks and can they be useful. An Australian Company called Oil

Research Ltd. and a South African Company called Exxaro Resources Ltd. annual report has

been used to highlight how these two topics find its use practically.

PART A

Review of the history and the development of the Conceptual Framework for Financial

Reporting-

In several European nations, the main function of financial reporting has traditionally been

distinct from the role of financial market roles in certain nations. This is since there hasn't been

any such heavy dependence on openly elevated finance in Europe historically. Alternatively,

finance has often been given by a restricted number of investors (such as banking institutions)

who have been ready to explicitly state the concrete information they wished to obtain from

the entity because of their' proximity' to the organization (with these information becoming

integrated into' specific purpose financial reports').With the growing globalism of enterprises as

well as financial markets, moreover, the position of financial reporting conducted by large

businesses across all European nations has now been generally concentrated on financial data

regulations for financial markets, with the result that provisions have created over a significant

period of time in financial markets controlled economies (with a large number of competing

stocks).While financial accounting exercise can be traced many centuries, financial accounting

legislation usually started in the twentieth century in many other capital-market-dominated

nations (like the United States, the United Kingdom, Ireland, Australia and Canada). Mainly this

lack of transparency in the early stages could have been based on the fact that there was

restricted segregation between the ownership and control of businesses and, as such, many

accounting structures were intended to provide the proprietor / supervisor with data. In several

nations, the degree of freedom among owners and management has doubled in the 20th

century.There was an enhanced propensity to legislate financial reporting declarations with

such an excessive estrangement.

Explanation of Australian accounting profession’s concerns regarding the Conceptual

Framework-

Dean and Clarke characterize several issues pertaining to comprehending why this has been

troublesome to create conceptual frameworks at national scale. They recommend that present

conceptual framework initiatives have pursued to create an accounting structure predicated on

a law, instead of concentrating on ideas that transcend normal, daily trade.IASB's initial model

was released in 1989 and, in the meantime, has not been significantly modified. Calibration

notions are an area not enclosed by the present IASB. The Identification Rubric Falters to

offerany advice onthe Calibration Issue, which is basic to accounting. Gerboth references from

Popper:“ In science, we must be cautious that perhaps the statements we make should never

depend on the meaning of our terms. Even if the examples show, we never try to walk or target

any reasoning on any data from the logic. That's why we have so little difficulty with our

aspects. We're not overburdening them. We are ascribing as little weight as feasible to them”

One of the goals of the theoretical framework is to direct the administrator's regular practice.

However, an administrative solipsism characterizes the current CF. For example; data

characteristics such as dependability are indicated in FASB Remark No 2, based on the success

of other attributes such as conceptual loyalty, objectivity, and veracity. These characteristics, in

turn, however, rely on other data qualities which are not empirically validated.

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework

The advantages of a moral framework involve creating notions in organized frames that make

financial accounting and reporting compatible and practical ; augmented functionality of

globally compatible norms through such accuracy ; economic accounting growth ; and improved

interaction as a whole (Sterling 1982). Creating standards with the assistance of a theoretical

framework is made easier and more price-effective as the fundamentals are already being

mentioned and formed (FASB 1980). These concepts can be introduced in cases where there

are no applicable accounting standards or other rules and where improprieties may occur as to

which initiatives to use in specific cases. Strategy from the theoretical framework already

formed will endure very little condemnation (Mosso 1998).

Though, on the drawback, the theoretical model can be too narrow in scope and its values with

its immense reliance on different parameters. Therefore, when generating financial reports, it

accounting structures were intended to provide the proprietor / supervisor with data. In several

nations, the degree of freedom among owners and management has doubled in the 20th

century.There was an enhanced propensity to legislate financial reporting declarations with

such an excessive estrangement.

Explanation of Australian accounting profession’s concerns regarding the Conceptual

Framework-

Dean and Clarke characterize several issues pertaining to comprehending why this has been

troublesome to create conceptual frameworks at national scale. They recommend that present

conceptual framework initiatives have pursued to create an accounting structure predicated on

a law, instead of concentrating on ideas that transcend normal, daily trade.IASB's initial model

was released in 1989 and, in the meantime, has not been significantly modified. Calibration

notions are an area not enclosed by the present IASB. The Identification Rubric Falters to

offerany advice onthe Calibration Issue, which is basic to accounting. Gerboth references from

Popper:“ In science, we must be cautious that perhaps the statements we make should never

depend on the meaning of our terms. Even if the examples show, we never try to walk or target

any reasoning on any data from the logic. That's why we have so little difficulty with our

aspects. We're not overburdening them. We are ascribing as little weight as feasible to them”

One of the goals of the theoretical framework is to direct the administrator's regular practice.

However, an administrative solipsism characterizes the current CF. For example; data

characteristics such as dependability are indicated in FASB Remark No 2, based on the success

of other attributes such as conceptual loyalty, objectivity, and veracity. These characteristics, in

turn, however, rely on other data qualities which are not empirically validated.

Discussion of academics’ concerns about the quality (potential benefits and limitations) of the

Conceptual Framework

The advantages of a moral framework involve creating notions in organized frames that make

financial accounting and reporting compatible and practical ; augmented functionality of

globally compatible norms through such accuracy ; economic accounting growth ; and improved

interaction as a whole (Sterling 1982). Creating standards with the assistance of a theoretical

framework is made easier and more price-effective as the fundamentals are already being

mentioned and formed (FASB 1980). These concepts can be introduced in cases where there

are no applicable accounting standards or other rules and where improprieties may occur as to

which initiatives to use in specific cases. Strategy from the theoretical framework already

formed will endure very little condemnation (Mosso 1998).

Though, on the drawback, the theoretical model can be too narrow in scope and its values with

its immense reliance on different parameters. Therefore, when generating financial reports, it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can be of little assistance and may lead to the formation of accounting standards that are

academically rigorous, conceptual and forgery-prone. In reality, these norms can also render

the clause of financial data very complicated for both financial report filers and users (Sterling

1982). Notions may be genuine and polished, but the effectiveness of financial statements

could be watered down with the technical complexity of knowledge. (BROMWICH, MACVE &

SUNDER, 2010)

Explanation of how the conceptual framework has been applied by Oil Search Limited.

On seeing the annual report of Oil Search Limited for the year 2017, we find that they

have strictly followed conceptual framework to present their financial statements. The

usual method for identifying elements in the financial statements is to determine- assets,

liabilities, income and expenses. For determining income we study the statements of

comprehensive income for the year ended on 31st December 2017 which turns out to be

A$ 302,580,000 whereas statement of financial position give us the other details which

includes assets and liabilities. The statements prepared by the company are in

accordance with International Financial Reporting Standards. They discuss about the

new Standards adopted as well as the ones which are still to implement. They have

prepared statement of changes in equity which shows a fall when compared to previous

year for parent company but rise for consolidated part. Cash flow statement has been

prepared which shows the cash and cash equivalents for the year end. Statement of

financial position gives us the idea about sum total of assets, liabilities as well as equities.

The comprehensive income gives us the detail of income or loss.

The Financial Statements of Oil Search Ltd. has been prepared in accordance with IFRS,

IFRIC interpretations and PNG Companies Act, 1997. They have been prepared under

historical cost convention. They adopted Amendments to IAS 7 Statement of cash flows

on 1st January, 2017. However there are few accounting standards which they have

decided to adopt from next financial year. Recognition of revenue is when risk and

rewards of ownership is transferred to the customer, consideration recovery is probable,

the associated costs and possible return of goods can be reliably estimated, there is no

continuing management involvement with the goods, and the amount of revenue can be

measured reliably. Borrowing costs get recognition in the statements of comprehensive

income in the period when they are incurred. Inventory costs are valued at the lower of

cost or net realizable value. The tax payable or receivable is based on taxable profit for

the year. Depreciation on plant and machinery is calculated on straight line basis.

Impairment of assets is strictly monitored.

All financial assets and financial liabilities are recognized at fair value of consideration

paid or received, net of transaction costs as appropriate and thus carried out at

amortized cost. They manage their capital with a view of going concern policy while

taking care of maximization of return for shareholders through optimization of debt and

equity balances. Credit risk management has been introduced at all the levels to mitigate

losses which arise due to failure of borrower to pay any kind of debt.Apart from this they

have also used Commodity Price risk management in order to avoid being limited by

exposure of fluctuating oil prices. Financial and Capital risk arises on a regular basis for

academically rigorous, conceptual and forgery-prone. In reality, these norms can also render

the clause of financial data very complicated for both financial report filers and users (Sterling

1982). Notions may be genuine and polished, but the effectiveness of financial statements

could be watered down with the technical complexity of knowledge. (BROMWICH, MACVE &

SUNDER, 2010)

Explanation of how the conceptual framework has been applied by Oil Search Limited.

On seeing the annual report of Oil Search Limited for the year 2017, we find that they

have strictly followed conceptual framework to present their financial statements. The

usual method for identifying elements in the financial statements is to determine- assets,

liabilities, income and expenses. For determining income we study the statements of

comprehensive income for the year ended on 31st December 2017 which turns out to be

A$ 302,580,000 whereas statement of financial position give us the other details which

includes assets and liabilities. The statements prepared by the company are in

accordance with International Financial Reporting Standards. They discuss about the

new Standards adopted as well as the ones which are still to implement. They have

prepared statement of changes in equity which shows a fall when compared to previous

year for parent company but rise for consolidated part. Cash flow statement has been

prepared which shows the cash and cash equivalents for the year end. Statement of

financial position gives us the idea about sum total of assets, liabilities as well as equities.

The comprehensive income gives us the detail of income or loss.

The Financial Statements of Oil Search Ltd. has been prepared in accordance with IFRS,

IFRIC interpretations and PNG Companies Act, 1997. They have been prepared under

historical cost convention. They adopted Amendments to IAS 7 Statement of cash flows

on 1st January, 2017. However there are few accounting standards which they have

decided to adopt from next financial year. Recognition of revenue is when risk and

rewards of ownership is transferred to the customer, consideration recovery is probable,

the associated costs and possible return of goods can be reliably estimated, there is no

continuing management involvement with the goods, and the amount of revenue can be

measured reliably. Borrowing costs get recognition in the statements of comprehensive

income in the period when they are incurred. Inventory costs are valued at the lower of

cost or net realizable value. The tax payable or receivable is based on taxable profit for

the year. Depreciation on plant and machinery is calculated on straight line basis.

Impairment of assets is strictly monitored.

All financial assets and financial liabilities are recognized at fair value of consideration

paid or received, net of transaction costs as appropriate and thus carried out at

amortized cost. They manage their capital with a view of going concern policy while

taking care of maximization of return for shareholders through optimization of debt and

equity balances. Credit risk management has been introduced at all the levels to mitigate

losses which arise due to failure of borrower to pay any kind of debt.Apart from this they

have also used Commodity Price risk management in order to avoid being limited by

exposure of fluctuating oil prices. Financial and Capital risk arises on a regular basis for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which respective management is available. Risk is borne only if the company is assured of

continuous cash inflow to meet future financial requirements. Share Plan has been

restricted in order to retain key management and valuable employees as well as to

compulsorily defer a portion of handful of participant’s short term incentive reward.

Performance rights plan is established as well since 2004 where chosen employees are

granted over ordinary shares of the company. The Organization's senior management

group evaluates the Organization's performance of the company and its sections mainly

in terms of pre-interest and tax income and capital spending on expansion and

assessment assets, oil and gas assets, and land, plant and equipment. The Faction

calculates the future costs of eliminating and preserving oil and gas production services,

wells, refineries and linked resources when the assets are set up. Administrators

frequently assesses decisions, forecasts and assumptions based on past experience and

other variables in implementing the Group's accounting initiatives, such as expectations

of future occurrences that may affect the Group. On the grounds of the most present set

of circumstances accessible to administrators, all decisions, projections and arguments

made are considered appropriate.

PART B

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework

The GRI Standards are the first worldwide sustainability reporting norms. They have a compact,

interconnected framework and offer the best worldwide reporting methods for a scope of

economic, social and environmental effects. Purpose of sustainable reporting is to provide all

the shareholders with a well-defined image of an entity’s performance in order to improve their

knowledge about the organization as well as their assessment capabilities whereas, integrated

reporting presents report in an integrated way on how an institute creates value over time

according to the business model. Guiding Principles of sustainability reporting are Obligation,

Identification, Openness, Integration, Consistency, Impartiality, Independence of private

entities, Accumulation accounting principle, Caution, Comparability, Understandability,

Vividness and Cleverness, and others. On the other side, integrated reporting concepts are

Tactical Emphasis and Upcoming Alignment, Data Interconnection, Stakeholder Relationships,

Subjectivity, Concision, Dependability and Comprehensiveness, Accuracy and Robustness. In

aspects of motive, both findings strive to satisfy the needs of separate users in order to improve

public sector oversight and accountability. (BUSCO, 2016) Their primary shareholders and the

material given, however, differ.Sustainability report and integrated report apply to a wide

variety of shareholders (financiers, residents, clients, workers, society, organizations, and so

continuous cash inflow to meet future financial requirements. Share Plan has been

restricted in order to retain key management and valuable employees as well as to

compulsorily defer a portion of handful of participant’s short term incentive reward.

Performance rights plan is established as well since 2004 where chosen employees are

granted over ordinary shares of the company. The Organization's senior management

group evaluates the Organization's performance of the company and its sections mainly

in terms of pre-interest and tax income and capital spending on expansion and

assessment assets, oil and gas assets, and land, plant and equipment. The Faction

calculates the future costs of eliminating and preserving oil and gas production services,

wells, refineries and linked resources when the assets are set up. Administrators

frequently assesses decisions, forecasts and assumptions based on past experience and

other variables in implementing the Group's accounting initiatives, such as expectations

of future occurrences that may affect the Group. On the grounds of the most present set

of circumstances accessible to administrators, all decisions, projections and arguments

made are considered appropriate.

PART B

Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework

The GRI Standards are the first worldwide sustainability reporting norms. They have a compact,

interconnected framework and offer the best worldwide reporting methods for a scope of

economic, social and environmental effects. Purpose of sustainable reporting is to provide all

the shareholders with a well-defined image of an entity’s performance in order to improve their

knowledge about the organization as well as their assessment capabilities whereas, integrated

reporting presents report in an integrated way on how an institute creates value over time

according to the business model. Guiding Principles of sustainability reporting are Obligation,

Identification, Openness, Integration, Consistency, Impartiality, Independence of private

entities, Accumulation accounting principle, Caution, Comparability, Understandability,

Vividness and Cleverness, and others. On the other side, integrated reporting concepts are

Tactical Emphasis and Upcoming Alignment, Data Interconnection, Stakeholder Relationships,

Subjectivity, Concision, Dependability and Comprehensiveness, Accuracy and Robustness. In

aspects of motive, both findings strive to satisfy the needs of separate users in order to improve

public sector oversight and accountability. (BUSCO, 2016) Their primary shareholders and the

material given, however, differ.Sustainability report and integrated report apply to a wide

variety of shareholders (financiers, residents, clients, workers, society, organizations, and so

on.) and publish financial and non-financial data in various ways: first as a separate report to

the financial statement, second as a single embedded report.

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports

Accountancy enables financial reports users to make better business decisions. However,

when setting policy, it is important to note the constraints of accounting and financial

reporting.

Accounting concepts like IFRS allow financial reports filers to use accounting measures that

truly reflect their institutions ' conditions.

While an extent of versatility is essential to portray a specific individual's accurate

information, the use of a multitude of accounting measures between separate entities

negatively affects the degree of standardization between financial statements.The use by

organizations working in different economic regions of different accounting structures (e.g.

IFRS, US GAAP) also introduces similar issues when trying to compare their financial

statements. The issue is solved by the expanding use of IFRS and the method of integration

between prominent accounting bodies to reach a single set of international standards.In the

preparation of financial reports, accounting involves the use of calculations where accurate

amounts cannot be defined. Projections are extremely subjective and thus lack precision

since they entail the use of foresight by leadership to decide the values included in the

financial reports. Where projections are not premised on accurate and provable info,

accounting information may be less accurate. Using professional judgment by financial

reports filers is essential in implementing accounting initiatives in a way that is consistent

with a corporation's transactions' financial reality. However, disparities will always be

unavoidable in translating the accounting standards criteria and implementing them to

realistic situations. The higher the use of assessment engaged, the more debatable would

tend to be the annual reports.

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as

well as integrated reports

Several parallels can be noted among presenting on Corporate Social Responsibility (CSR) and

integrated reporting. Gray, Kouhy and Lavers (1995, p. 49) observed that CSR reporting is a) not

purposeful or governed, b) deemed to be related to stagnating instead of instant profits, and c)

linked to size of the company, sector, ownership country and many other inclinations. Looking

at the features of the "accredited investor" businesses in the Integrated Reporting Pilot

Program (IIRC, 2013b), we can believe that some organizational features common to CSR and

incorporated reporting may occur.The hypotheses of political and social economy are widely

the financial statement, second as a single embedded report.

Rigour (strengths & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports

Accountancy enables financial reports users to make better business decisions. However,

when setting policy, it is important to note the constraints of accounting and financial

reporting.

Accounting concepts like IFRS allow financial reports filers to use accounting measures that

truly reflect their institutions ' conditions.

While an extent of versatility is essential to portray a specific individual's accurate

information, the use of a multitude of accounting measures between separate entities

negatively affects the degree of standardization between financial statements.The use by

organizations working in different economic regions of different accounting structures (e.g.

IFRS, US GAAP) also introduces similar issues when trying to compare their financial

statements. The issue is solved by the expanding use of IFRS and the method of integration

between prominent accounting bodies to reach a single set of international standards.In the

preparation of financial reports, accounting involves the use of calculations where accurate

amounts cannot be defined. Projections are extremely subjective and thus lack precision

since they entail the use of foresight by leadership to decide the values included in the

financial reports. Where projections are not premised on accurate and provable info,

accounting information may be less accurate. Using professional judgment by financial

reports filers is essential in implementing accounting initiatives in a way that is consistent

with a corporation's transactions' financial reality. However, disparities will always be

unavoidable in translating the accounting standards criteria and implementing them to

realistic situations. The higher the use of assessment engaged, the more debatable would

tend to be the annual reports.

Applicability (usefulness or limitations) of the theories to explain contents of sustainability as

well as integrated reports

Several parallels can be noted among presenting on Corporate Social Responsibility (CSR) and

integrated reporting. Gray, Kouhy and Lavers (1995, p. 49) observed that CSR reporting is a) not

purposeful or governed, b) deemed to be related to stagnating instead of instant profits, and c)

linked to size of the company, sector, ownership country and many other inclinations. Looking

at the features of the "accredited investor" businesses in the Integrated Reporting Pilot

Program (IIRC, 2013b), we can believe that some organizational features common to CSR and

incorporated reporting may occur.The hypotheses of political and social economy are widely

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

used to demonstrate CSR methods and disclosure, the most prevalent is the hypothesis of

validity and the hypothesis of interested parties.The principles of shareholders concentrate on

the connection between the institution and its shareholders – individuals inspired or impacted

by the institution's operations.It is not a hierarchical organization which we discover in

embedded reporting, but rather one with disputes. In order to highlight the justifications for

this, we attempt to observe the constellation in which integrated reporting exists through the

genealogy of Integrated Value Added Statements, Value Reporting, the A4S Connected

Reporting Framework and the GRI Sustainability Reporting Index.

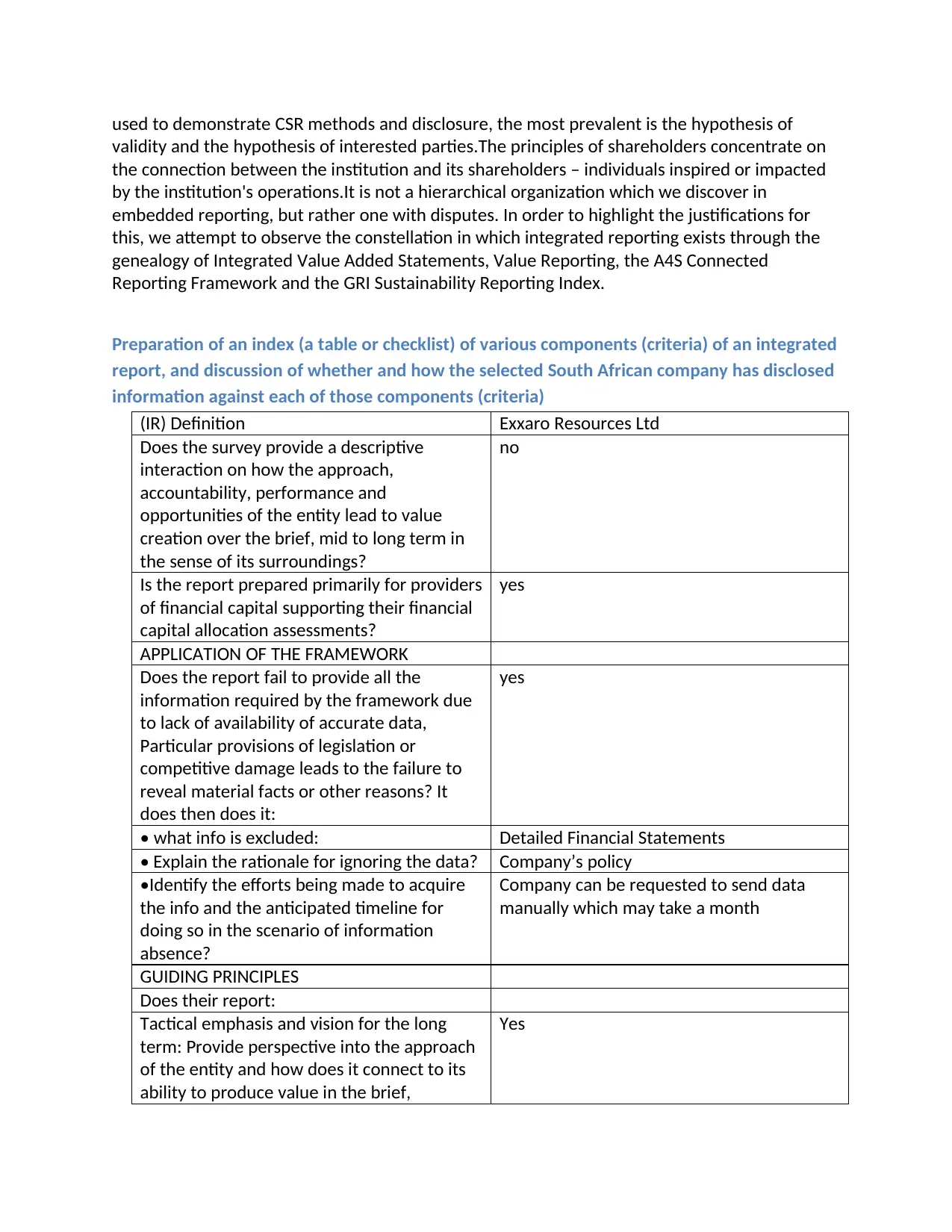

Preparation of an index (a table or checklist) of various components (criteria) of an integrated

report, and discussion of whether and how the selected South African company has disclosed

information against each of those components (criteria)

(IR) Definition Exxaro Resources Ltd

Does the survey provide a descriptive

interaction on how the approach,

accountability, performance and

opportunities of the entity lead to value

creation over the brief, mid to long term in

the sense of its surroundings?

no

Is the report prepared primarily for providers

of financial capital supporting their financial

capital allocation assessments?

yes

APPLICATION OF THE FRAMEWORK

Does the report fail to provide all the

information required by the framework due

to lack of availability of accurate data,

Particular provisions of legislation or

competitive damage leads to the failure to

reveal material facts or other reasons? It

does then does it:

yes

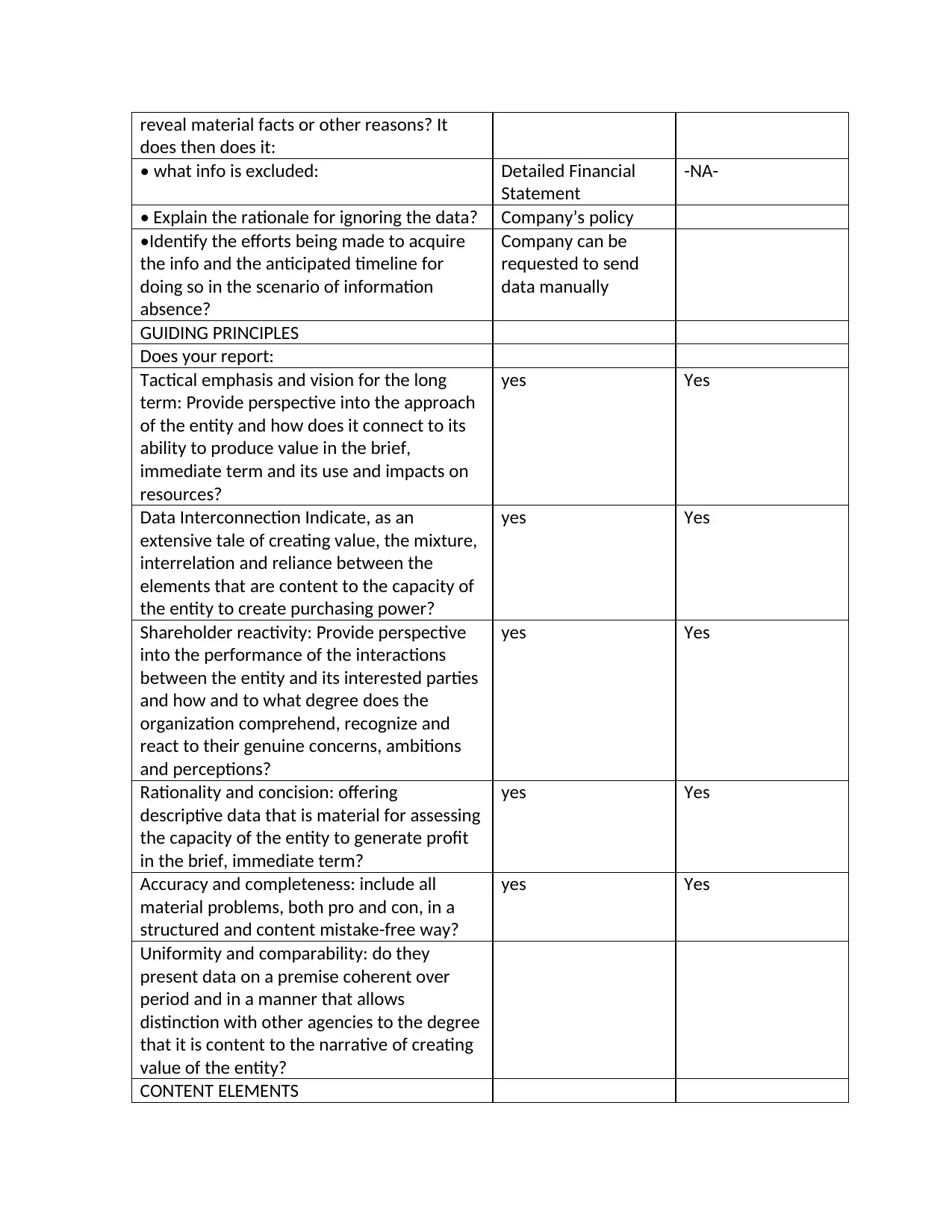

• what info is excluded: Detailed Financial Statements

• Explain the rationale for ignoring the data? Company’s policy

•Identify the efforts being made to acquire

the info and the anticipated timeline for

doing so in the scenario of information

absence?

Company can be requested to send data

manually which may take a month

GUIDING PRINCIPLES

Does their report:

Tactical emphasis and vision for the long

term: Provide perspective into the approach

of the entity and how does it connect to its

ability to produce value in the brief,

Yes

validity and the hypothesis of interested parties.The principles of shareholders concentrate on

the connection between the institution and its shareholders – individuals inspired or impacted

by the institution's operations.It is not a hierarchical organization which we discover in

embedded reporting, but rather one with disputes. In order to highlight the justifications for

this, we attempt to observe the constellation in which integrated reporting exists through the

genealogy of Integrated Value Added Statements, Value Reporting, the A4S Connected

Reporting Framework and the GRI Sustainability Reporting Index.

Preparation of an index (a table or checklist) of various components (criteria) of an integrated

report, and discussion of whether and how the selected South African company has disclosed

information against each of those components (criteria)

(IR) Definition Exxaro Resources Ltd

Does the survey provide a descriptive

interaction on how the approach,

accountability, performance and

opportunities of the entity lead to value

creation over the brief, mid to long term in

the sense of its surroundings?

no

Is the report prepared primarily for providers

of financial capital supporting their financial

capital allocation assessments?

yes

APPLICATION OF THE FRAMEWORK

Does the report fail to provide all the

information required by the framework due

to lack of availability of accurate data,

Particular provisions of legislation or

competitive damage leads to the failure to

reveal material facts or other reasons? It

does then does it:

yes

• what info is excluded: Detailed Financial Statements

• Explain the rationale for ignoring the data? Company’s policy

•Identify the efforts being made to acquire

the info and the anticipated timeline for

doing so in the scenario of information

absence?

Company can be requested to send data

manually which may take a month

GUIDING PRINCIPLES

Does their report:

Tactical emphasis and vision for the long

term: Provide perspective into the approach

of the entity and how does it connect to its

ability to produce value in the brief,

Yes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

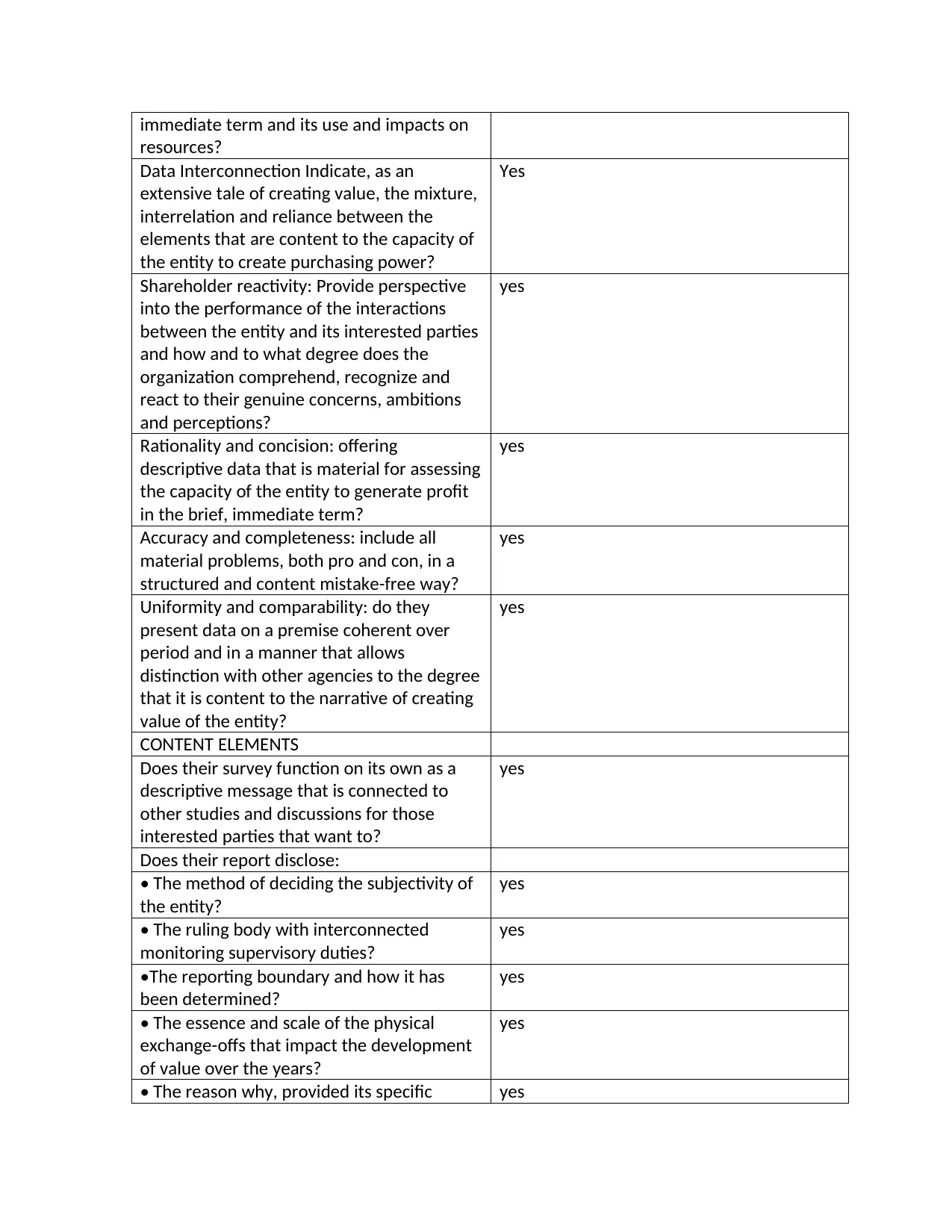

immediate term and its use and impacts on

resources?

Data Interconnection Indicate, as an

extensive tale of creating value, the mixture,

interrelation and reliance between the

elements that are content to the capacity of

the entity to create purchasing power?

Yes

Shareholder reactivity: Provide perspective

into the performance of the interactions

between the entity and its interested parties

and how and to what degree does the

organization comprehend, recognize and

react to their genuine concerns, ambitions

and perceptions?

yes

Rationality and concision: offering

descriptive data that is material for assessing

the capacity of the entity to generate profit

in the brief, immediate term?

yes

Accuracy and completeness: include all

material problems, both pro and con, in a

structured and content mistake-free way?

yes

Uniformity and comparability: do they

present data on a premise coherent over

period and in a manner that allows

distinction with other agencies to the degree

that it is content to the narrative of creating

value of the entity?

yes

CONTENT ELEMENTS

Does their survey function on its own as a

descriptive message that is connected to

other studies and discussions for those

interested parties that want to?

yes

Does their report disclose:

• The method of deciding the subjectivity of

the entity?

yes

• The ruling body with interconnected

monitoring supervisory duties?

yes

•The reporting boundary and how it has

been determined?

yes

• The essence and scale of the physical

exchange-offs that impact the development

of value over the years?

yes

• The reason why, provided its specific yes

resources?

Data Interconnection Indicate, as an

extensive tale of creating value, the mixture,

interrelation and reliance between the

elements that are content to the capacity of

the entity to create purchasing power?

Yes

Shareholder reactivity: Provide perspective

into the performance of the interactions

between the entity and its interested parties

and how and to what degree does the

organization comprehend, recognize and

react to their genuine concerns, ambitions

and perceptions?

yes

Rationality and concision: offering

descriptive data that is material for assessing

the capacity of the entity to generate profit

in the brief, immediate term?

yes

Accuracy and completeness: include all

material problems, both pro and con, in a

structured and content mistake-free way?

yes

Uniformity and comparability: do they

present data on a premise coherent over

period and in a manner that allows

distinction with other agencies to the degree

that it is content to the narrative of creating

value of the entity?

yes

CONTENT ELEMENTS

Does their survey function on its own as a

descriptive message that is connected to

other studies and discussions for those

interested parties that want to?

yes

Does their report disclose:

• The method of deciding the subjectivity of

the entity?

yes

• The ruling body with interconnected

monitoring supervisory duties?

yes

•The reporting boundary and how it has

been determined?

yes

• The essence and scale of the physical

exchange-offs that impact the development

of value over the years?

yes

• The reason why, provided its specific yes

situations, does the entity deem any of the

capitals recognized in this Structure to be

irrelevant, if so? Does your report answer

the questions?

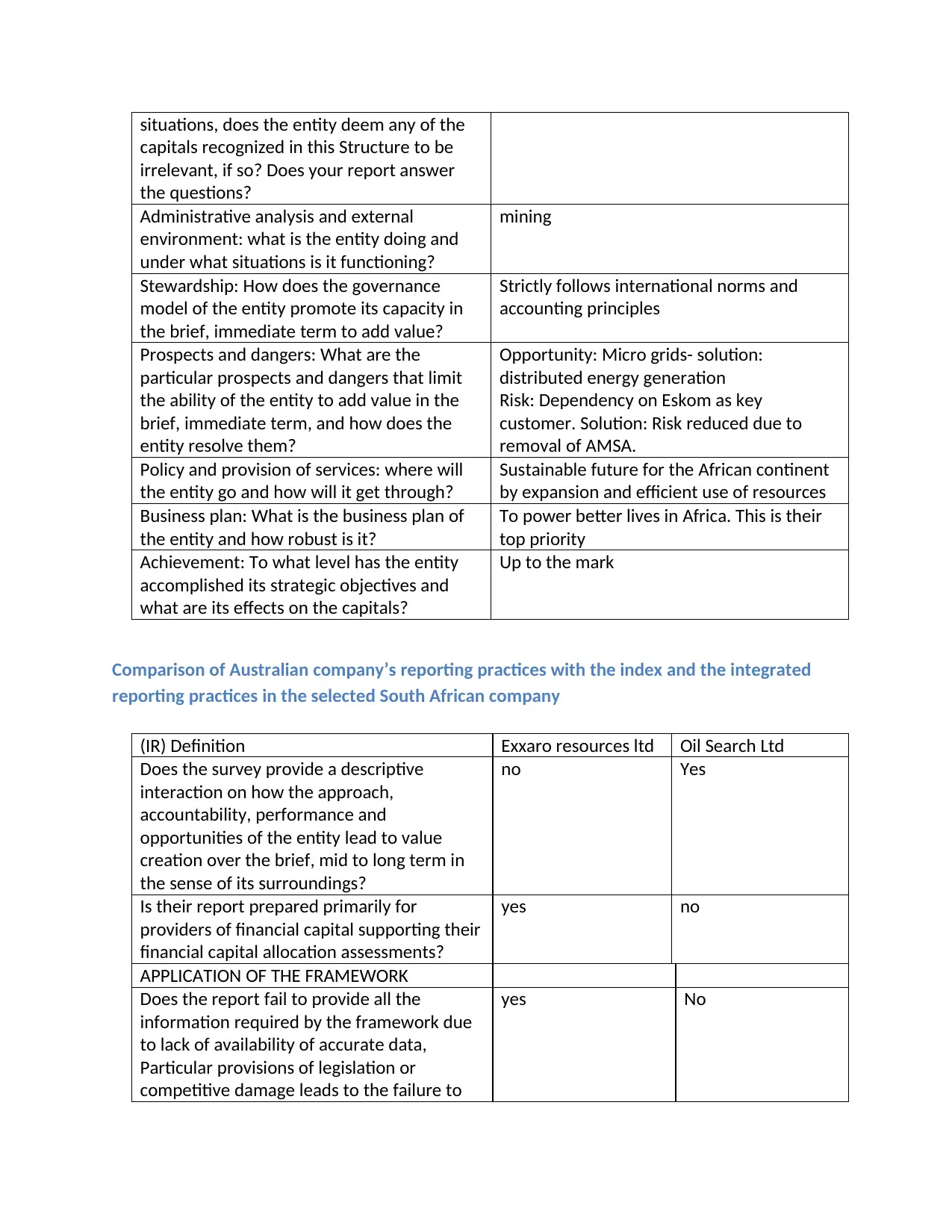

Administrative analysis and external

environment: what is the entity doing and

under what situations is it functioning?

mining

Stewardship: How does the governance

model of the entity promote its capacity in

the brief, immediate term to add value?

Strictly follows international norms and

accounting principles

Prospects and dangers: What are the

particular prospects and dangers that limit

the ability of the entity to add value in the

brief, immediate term, and how does the

entity resolve them?

Opportunity: Micro grids- solution:

distributed energy generation

Risk: Dependency on Eskom as key

customer. Solution: Risk reduced due to

removal of AMSA.

Policy and provision of services: where will

the entity go and how will it get through?

Sustainable future for the African continent

by expansion and efficient use of resources

Business plan: What is the business plan of

the entity and how robust is it?

To power better lives in Africa. This is their

top priority

Achievement: To what level has the entity

accomplished its strategic objectives and

what are its effects on the capitals?

Up to the mark

Comparison of Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African company

(IR) Definition Exxaro resources ltd Oil Search Ltd

Does the survey provide a descriptive

interaction on how the approach,

accountability, performance and

opportunities of the entity lead to value

creation over the brief, mid to long term in

the sense of its surroundings?

no Yes

Is their report prepared primarily for

providers of financial capital supporting their

financial capital allocation assessments?

yes no

APPLICATION OF THE FRAMEWORK

Does the report fail to provide all the

information required by the framework due

to lack of availability of accurate data,

Particular provisions of legislation or

competitive damage leads to the failure to

yes No

capitals recognized in this Structure to be

irrelevant, if so? Does your report answer

the questions?

Administrative analysis and external

environment: what is the entity doing and

under what situations is it functioning?

mining

Stewardship: How does the governance

model of the entity promote its capacity in

the brief, immediate term to add value?

Strictly follows international norms and

accounting principles

Prospects and dangers: What are the

particular prospects and dangers that limit

the ability of the entity to add value in the

brief, immediate term, and how does the

entity resolve them?

Opportunity: Micro grids- solution:

distributed energy generation

Risk: Dependency on Eskom as key

customer. Solution: Risk reduced due to

removal of AMSA.

Policy and provision of services: where will

the entity go and how will it get through?

Sustainable future for the African continent

by expansion and efficient use of resources

Business plan: What is the business plan of

the entity and how robust is it?

To power better lives in Africa. This is their

top priority

Achievement: To what level has the entity

accomplished its strategic objectives and

what are its effects on the capitals?

Up to the mark

Comparison of Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African company

(IR) Definition Exxaro resources ltd Oil Search Ltd

Does the survey provide a descriptive

interaction on how the approach,

accountability, performance and

opportunities of the entity lead to value

creation over the brief, mid to long term in

the sense of its surroundings?

no Yes

Is their report prepared primarily for

providers of financial capital supporting their

financial capital allocation assessments?

yes no

APPLICATION OF THE FRAMEWORK

Does the report fail to provide all the

information required by the framework due

to lack of availability of accurate data,

Particular provisions of legislation or

competitive damage leads to the failure to

yes No

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reveal material facts or other reasons? It

does then does it:

• what info is excluded: Detailed Financial

Statement

-NA-

• Explain the rationale for ignoring the data? Company’s policy

•Identify the efforts being made to acquire

the info and the anticipated timeline for

doing so in the scenario of information

absence?

Company can be

requested to send

data manually

GUIDING PRINCIPLES

Does your report:

Tactical emphasis and vision for the long

term: Provide perspective into the approach

of the entity and how does it connect to its

ability to produce value in the brief,

immediate term and its use and impacts on

resources?

yes Yes

Data Interconnection Indicate, as an

extensive tale of creating value, the mixture,

interrelation and reliance between the

elements that are content to the capacity of

the entity to create purchasing power?

yes Yes

Shareholder reactivity: Provide perspective

into the performance of the interactions

between the entity and its interested parties

and how and to what degree does the

organization comprehend, recognize and

react to their genuine concerns, ambitions

and perceptions?

yes Yes

Rationality and concision: offering

descriptive data that is material for assessing

the capacity of the entity to generate profit

in the brief, immediate term?

yes Yes

Accuracy and completeness: include all

material problems, both pro and con, in a

structured and content mistake-free way?

yes Yes

Uniformity and comparability: do they

present data on a premise coherent over

period and in a manner that allows

distinction with other agencies to the degree

that it is content to the narrative of creating

value of the entity?

CONTENT ELEMENTS

does then does it:

• what info is excluded: Detailed Financial

Statement

-NA-

• Explain the rationale for ignoring the data? Company’s policy

•Identify the efforts being made to acquire

the info and the anticipated timeline for

doing so in the scenario of information

absence?

Company can be

requested to send

data manually

GUIDING PRINCIPLES

Does your report:

Tactical emphasis and vision for the long

term: Provide perspective into the approach

of the entity and how does it connect to its

ability to produce value in the brief,

immediate term and its use and impacts on

resources?

yes Yes

Data Interconnection Indicate, as an

extensive tale of creating value, the mixture,

interrelation and reliance between the

elements that are content to the capacity of

the entity to create purchasing power?

yes Yes

Shareholder reactivity: Provide perspective

into the performance of the interactions

between the entity and its interested parties

and how and to what degree does the

organization comprehend, recognize and

react to their genuine concerns, ambitions

and perceptions?

yes Yes

Rationality and concision: offering

descriptive data that is material for assessing

the capacity of the entity to generate profit

in the brief, immediate term?

yes Yes

Accuracy and completeness: include all

material problems, both pro and con, in a

structured and content mistake-free way?

yes Yes

Uniformity and comparability: do they

present data on a premise coherent over

period and in a manner that allows

distinction with other agencies to the degree

that it is content to the narrative of creating

value of the entity?

CONTENT ELEMENTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Does their survey function on its own as a

descriptive message that is connected to

other studies and discussions for those

interested parties that want to?

yes Yes

Does their report disclose:

• The organization’s materiality

determination process?

yes Yes

• The governance body with oversight

responsibilities for integrated reporting?

yes Yes

• The reporting boundary and how it has

been determined?

yes Yes

• The nature and magnitude of the

material trade-offs that influence value

creation over time?

yes Yes

• The reason why, provided its specific

situations, does the entity deem any of the

capitals recognized in this Structure to be

irrelevant, if so? Does your report answer

the questions?

yes Yes

Administrative analysis and external

environment: what is the entity doing and

under what situations is it functioning?

mining Oil and Gas

exploration

Stewardship: How does the governance

model of the entity promote its capacity in

the brief, immediate term to add value?

Strictly follows

international norms

and accounting

principles

Strictly follows

international norms

and accounting

principles

Prospects and dangers: What are the

particular prospects and dangers that limit

the ability of the entity to add value in the

brief, immediate term, and how does the

entity resolve them?

Opportunity: Micro

grids- solution:

distributed energy

generation

Risk: Dependency on

Eskom as key

customer. Solution:

Risk reduced due to

removal of AMSA.

Opportunity-

untouched natural

resources. Solution-

Continuous

exploration

Policy and distribution of resources: where

will the entity go and how will it get there?

Sustainable future

for the African

continent by

expansion and

efficient use of

resources

Sustainable future

for the Australian

continent by

expansion and

efficient use of

resources

Business plan: What is the business plan of

the entity and how robust is it?

To power better

lives in Africa. This is

Sustainable Future

descriptive message that is connected to

other studies and discussions for those

interested parties that want to?

yes Yes

Does their report disclose:

• The organization’s materiality

determination process?

yes Yes

• The governance body with oversight

responsibilities for integrated reporting?

yes Yes

• The reporting boundary and how it has

been determined?

yes Yes

• The nature and magnitude of the

material trade-offs that influence value

creation over time?

yes Yes

• The reason why, provided its specific

situations, does the entity deem any of the

capitals recognized in this Structure to be

irrelevant, if so? Does your report answer

the questions?

yes Yes

Administrative analysis and external

environment: what is the entity doing and

under what situations is it functioning?

mining Oil and Gas

exploration

Stewardship: How does the governance

model of the entity promote its capacity in

the brief, immediate term to add value?

Strictly follows

international norms

and accounting

principles

Strictly follows

international norms

and accounting

principles

Prospects and dangers: What are the

particular prospects and dangers that limit

the ability of the entity to add value in the

brief, immediate term, and how does the

entity resolve them?

Opportunity: Micro

grids- solution:

distributed energy

generation

Risk: Dependency on

Eskom as key

customer. Solution:

Risk reduced due to

removal of AMSA.

Opportunity-

untouched natural

resources. Solution-

Continuous

exploration

Policy and distribution of resources: where

will the entity go and how will it get there?

Sustainable future

for the African

continent by

expansion and

efficient use of

resources

Sustainable future

for the Australian

continent by

expansion and

efficient use of

resources

Business plan: What is the business plan of

the entity and how robust is it?

To power better

lives in Africa. This is

Sustainable Future

their top priority

Achievement: To what level has the entity

accomplished its strategic objectives and

what are its effects on the capitals?

Up to the mark Up to the mark

CONCLUSION

This paper discusses about use of integrated reporting and conceptual framework and how

they are used to determine functioning of Company. It also gives the reader of financial

statements a clear idea if there is something important missing or intentionally being hidden

with intentions to manipulate the parties which utilize the reports.

REFERENCES

Accounting standards. (2019). Retrieved from

https://www.aasb.gov.au/Pronouncements/Current-standards.aspx

BUSCO, C. (2016). INTEGRATED REPORTING.:SPRINGER INTERNATIONAL PU.

BROMWICH, M., MACVE, R., & SUNDER, S. (2010). Hicksian Income in the Conceptual

Framework. Abacus, 46(3), 348-376. doi: 10.1111/j.1467-6281.2010.00322.x

Deegan, C. (n.d.). Financial Accounting Theory.

FASB Home. (2019). Retrieved from https://www.fasb.org/home

Achievement: To what level has the entity

accomplished its strategic objectives and

what are its effects on the capitals?

Up to the mark Up to the mark

CONCLUSION

This paper discusses about use of integrated reporting and conceptual framework and how

they are used to determine functioning of Company. It also gives the reader of financial

statements a clear idea if there is something important missing or intentionally being hidden

with intentions to manipulate the parties which utilize the reports.

REFERENCES

Accounting standards. (2019). Retrieved from

https://www.aasb.gov.au/Pronouncements/Current-standards.aspx

BUSCO, C. (2016). INTEGRATED REPORTING.:SPRINGER INTERNATIONAL PU.

BROMWICH, M., MACVE, R., & SUNDER, S. (2010). Hicksian Income in the Conceptual

Framework. Abacus, 46(3), 348-376. doi: 10.1111/j.1467-6281.2010.00322.x

Deegan, C. (n.d.). Financial Accounting Theory.

FASB Home. (2019). Retrieved from https://www.fasb.org/home

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.