ACCT20075 Auditing & Ethics: Materiality, Analytical Review, Audit

VerifiedAdded on 2023/03/23

|13

|2844

|31

Report

AI Summary

This report provides a detailed analysis of auditing and ethics, focusing on the application of materiality concepts in financial statement audits. It includes a quantitative estimate for materiality based on Boral Ltd's financial data for the year ended June 30, 2018, and discusses the rationale behind choosing a specific materiality level. Significant items for audit consideration, such as impairment of goodwill and contingencies, are identified along with recommended audit procedures. The report also presents a preliminary analytical review, examining profitability, liquidity, and leverage ratios to highlight areas of audit risk and suggests accounts for further review, including revenues and cash balances. Finally, it reviews the cash flow statement, raising concerns about the company's going concern assumption and outlining necessary audit procedures. This document is available on Desklib, a platform offering a wide range of study resources for students.

Running head: AUDITS AND ETHICS

Audits and ethics

Name of the student

Name of the university

Student ID

Author note

Audits and ethics

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITS AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality level...........................................................................................................................2

Quantitative estimate for materiality.......................................................................................3

Rational behind choosing the level of materiality...................................................................3

Significant items to be considered for audit................................................................................4

Section 2..........................................................................................................................................6

Section 3..........................................................................................................................................9

Review of cash flow statement....................................................................................................9

Review of audit report...............................................................................................................10

References......................................................................................................................................11

Table of Contents

Section 1..........................................................................................................................................2

Materiality level...........................................................................................................................2

Quantitative estimate for materiality.......................................................................................3

Rational behind choosing the level of materiality...................................................................3

Significant items to be considered for audit................................................................................4

Section 2..........................................................................................................................................6

Section 3..........................................................................................................................................9

Review of cash flow statement....................................................................................................9

Review of audit report...............................................................................................................10

References......................................................................................................................................11

2AUDITS AND ETHICS

Section 1

Materiality level

As basis for auditor’s opinion, auditing standards require the auditors for obtaining

reasonable assurances regarding whether as a whole the financial statement are free from the

material misstatements. Hence, the materiality concept is fundamental to audit that is applied by

the auditors at the stage of audit planning (Christensen, Glover & Wood, 2013). In accordance

with AUS 202 the main objective of carrying out audit for the financial statement is to express an

opinion on the same that will state whether the material aspects are taken care of in accordance

with the recognised framework for the financial reporting. Based on the level of materiality the

auditor determines the nature and timing of audit procedure and the extent of the same. Further,

the relationship between risk and the materiality level is taken into consideration while

determining the nature and timing of audit procedure and the extent of the same (Auasb.gov.au,

2019).

Planning materiality is the amount of misstatements that is set by the auditors at stage of

audit planning based on the materiality. It is used by the auditor for assessing whether

misstatements individually or in aggregate misstated materially in financial statements. To

ascertain the preliminary materiality assessment various factors are taken into consideration.

These factors are qualitative as well as quantitative information, reliability of the information

provided by the management and any other factor that may signify divergence from normal

activities (Coetzee & Lubbe, 2014). Materiality is calculated taking into consideration the

following bases –

Net profit – 5% to 10%

Section 1

Materiality level

As basis for auditor’s opinion, auditing standards require the auditors for obtaining

reasonable assurances regarding whether as a whole the financial statement are free from the

material misstatements. Hence, the materiality concept is fundamental to audit that is applied by

the auditors at the stage of audit planning (Christensen, Glover & Wood, 2013). In accordance

with AUS 202 the main objective of carrying out audit for the financial statement is to express an

opinion on the same that will state whether the material aspects are taken care of in accordance

with the recognised framework for the financial reporting. Based on the level of materiality the

auditor determines the nature and timing of audit procedure and the extent of the same. Further,

the relationship between risk and the materiality level is taken into consideration while

determining the nature and timing of audit procedure and the extent of the same (Auasb.gov.au,

2019).

Planning materiality is the amount of misstatements that is set by the auditors at stage of

audit planning based on the materiality. It is used by the auditor for assessing whether

misstatements individually or in aggregate misstated materially in financial statements. To

ascertain the preliminary materiality assessment various factors are taken into consideration.

These factors are qualitative as well as quantitative information, reliability of the information

provided by the management and any other factor that may signify divergence from normal

activities (Coetzee & Lubbe, 2014). Materiality is calculated taking into consideration the

following bases –

Net profit – 5% to 10%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITS AND ETHICS

Gross profit – 0.5% to 1%

Shareholder’s equity – 2% to 5%

Total asset – 1% to 2%

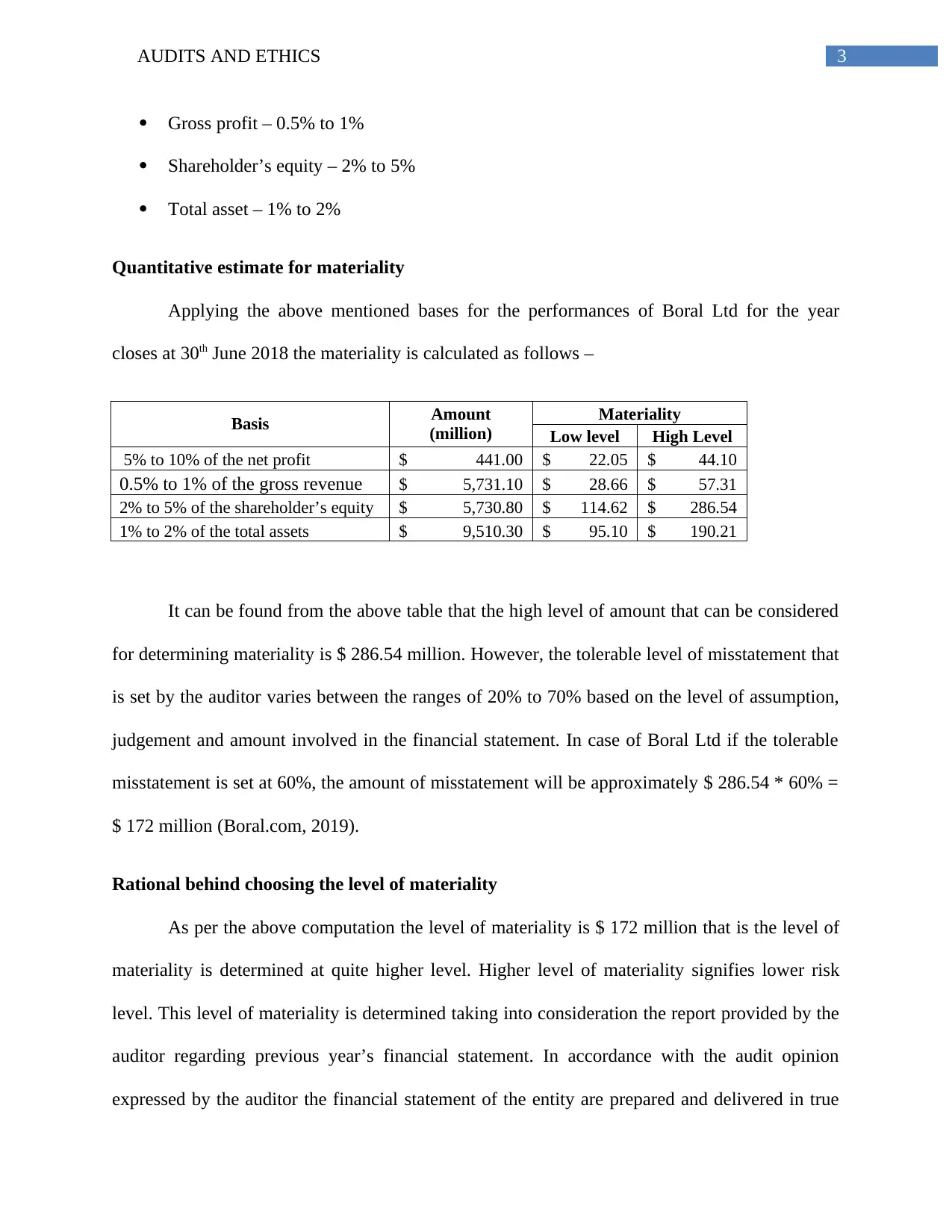

Quantitative estimate for materiality

Applying the above mentioned bases for the performances of Boral Ltd for the year

closes at 30th June 2018 the materiality is calculated as follows –

Basis Amount

(million)

Materiality

Low level High Level

5% to 10% of the net profit $ 441.00 $ 22.05 $ 44.10

0.5% to 1% of the gross revenue $ 5,731.10 $ 28.66 $ 57.31

2% to 5% of the shareholder’s equity $ 5,730.80 $ 114.62 $ 286.54

1% to 2% of the total assets $ 9,510.30 $ 95.10 $ 190.21

It can be found from the above table that the high level of amount that can be considered

for determining materiality is $ 286.54 million. However, the tolerable level of misstatement that

is set by the auditor varies between the ranges of 20% to 70% based on the level of assumption,

judgement and amount involved in the financial statement. In case of Boral Ltd if the tolerable

misstatement is set at 60%, the amount of misstatement will be approximately $ 286.54 * 60% =

$ 172 million (Boral.com, 2019).

Rational behind choosing the level of materiality

As per the above computation the level of materiality is $ 172 million that is the level of

materiality is determined at quite higher level. Higher level of materiality signifies lower risk

level. This level of materiality is determined taking into consideration the report provided by the

auditor regarding previous year’s financial statement. In accordance with the audit opinion

expressed by the auditor the financial statement of the entity are prepared and delivered in true

Gross profit – 0.5% to 1%

Shareholder’s equity – 2% to 5%

Total asset – 1% to 2%

Quantitative estimate for materiality

Applying the above mentioned bases for the performances of Boral Ltd for the year

closes at 30th June 2018 the materiality is calculated as follows –

Basis Amount

(million)

Materiality

Low level High Level

5% to 10% of the net profit $ 441.00 $ 22.05 $ 44.10

0.5% to 1% of the gross revenue $ 5,731.10 $ 28.66 $ 57.31

2% to 5% of the shareholder’s equity $ 5,730.80 $ 114.62 $ 286.54

1% to 2% of the total assets $ 9,510.30 $ 95.10 $ 190.21

It can be found from the above table that the high level of amount that can be considered

for determining materiality is $ 286.54 million. However, the tolerable level of misstatement that

is set by the auditor varies between the ranges of 20% to 70% based on the level of assumption,

judgement and amount involved in the financial statement. In case of Boral Ltd if the tolerable

misstatement is set at 60%, the amount of misstatement will be approximately $ 286.54 * 60% =

$ 172 million (Boral.com, 2019).

Rational behind choosing the level of materiality

As per the above computation the level of materiality is $ 172 million that is the level of

materiality is determined at quite higher level. Higher level of materiality signifies lower risk

level. This level of materiality is determined taking into consideration the report provided by the

auditor regarding previous year’s financial statement. In accordance with the audit opinion

expressed by the auditor the financial statement of the entity are prepared and delivered in true

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITS AND ETHICS

and fair manner and is representing true and fair view of the financial performance as well as

position of the company.

Significant items to be considered for audit

Going through Boral Ltd’ financial statement included in the annual report for the year

ended 2018 it can be identified that some of the items of the included in the financial statement

require management’s judgments and assumption. These items are impairment and contingencies

and will have significance to audit (Leung et al., 2014).

Impairment – goodwill and other intangible assets with indefinite useful life are annually tested

for the purpose of impairment and for other assets it is tested while any indication exists for

impairment. Impairment is reported in the income statement if the carrying of the item is more

than its recoverable value. However, the management require forming significant judgments,

assumptions and estimates to determine whether carrying value of the non-financial asset has

indication of impairment. It involves forecasting the cash flow for future period, discount rate to

be applied to the cash flows and expected growth rate for long term. Such judgments and

estimates can be changed with the change in operational and economic conditions. Hence, the

actual cash flow may vary with the forecasts and that may have impact on the recognition of the

impairment charges (Boral.com, 2019). Audit procedures to be carried out for evaluating

impairment charges are as follows –

Review the fixed asset and ensure that AASB 136 is complied with while charging

impairment for any particular asset. Further, the auditor must review the processes and

procedures used by the management for assessing the impairments

and fair manner and is representing true and fair view of the financial performance as well as

position of the company.

Significant items to be considered for audit

Going through Boral Ltd’ financial statement included in the annual report for the year

ended 2018 it can be identified that some of the items of the included in the financial statement

require management’s judgments and assumption. These items are impairment and contingencies

and will have significance to audit (Leung et al., 2014).

Impairment – goodwill and other intangible assets with indefinite useful life are annually tested

for the purpose of impairment and for other assets it is tested while any indication exists for

impairment. Impairment is reported in the income statement if the carrying of the item is more

than its recoverable value. However, the management require forming significant judgments,

assumptions and estimates to determine whether carrying value of the non-financial asset has

indication of impairment. It involves forecasting the cash flow for future period, discount rate to

be applied to the cash flows and expected growth rate for long term. Such judgments and

estimates can be changed with the change in operational and economic conditions. Hence, the

actual cash flow may vary with the forecasts and that may have impact on the recognition of the

impairment charges (Boral.com, 2019). Audit procedures to be carried out for evaluating

impairment charges are as follows –

Review the fixed asset and ensure that AASB 136 is complied with while charging

impairment for any particular asset. Further, the auditor must review the processes and

procedures used by the management for assessing the impairments

5AUDITS AND ETHICS

Comparing the cash flows forecasted with the forecasts approved by the board and

considering the impact of past event on the forecasts.

Contingencies – contingent liabilities are disclosed in the note of the financial statements only

for those items for which the possibility for future receipts and future payments are negligible.

Contingency disclosed by the company is for bank guarantee. The entity delivered a letter of

responsibility for the accommodation provided by bank to the controlled companies of Boral Ltd

from time to time. However, the amount recorded as contingency for bank guarantee is only $

38.3 million, as the item requires significant judgments and assumption of the management it is

regarded to have significance to audit (Boral.com, 2019). Audit procedures to be carried out for

evaluating contingencies are as follows –

Materiality of the transaction – disclosing of contingencies are dependent upon the fact

that whether the liability will have material impact on the financial statement of the

entity. Auditor shall determine the threshold for materiality before analysing individual

liabilities. If the liability is lower than the limit it is considered to have insignificant

impact on financial statement (Byrnes et al., 2015).

Probability of occurrence – probability of the event shall be estimated for determining its

impact on financial statement of the entity. Levels of probability are remote, probable and

reasonably probable, however only the probable and reasonably probable items shall be

disclosed as contingencies.

Journal entries for the probable events – while the contingency is probable, the entity

shall provide the same in the general ledger. For instance, pending lawsuit shall be

recorded as debit to the legal expenses and credit to the accrued liabilities. However, if

Comparing the cash flows forecasted with the forecasts approved by the board and

considering the impact of past event on the forecasts.

Contingencies – contingent liabilities are disclosed in the note of the financial statements only

for those items for which the possibility for future receipts and future payments are negligible.

Contingency disclosed by the company is for bank guarantee. The entity delivered a letter of

responsibility for the accommodation provided by bank to the controlled companies of Boral Ltd

from time to time. However, the amount recorded as contingency for bank guarantee is only $

38.3 million, as the item requires significant judgments and assumption of the management it is

regarded to have significance to audit (Boral.com, 2019). Audit procedures to be carried out for

evaluating contingencies are as follows –

Materiality of the transaction – disclosing of contingencies are dependent upon the fact

that whether the liability will have material impact on the financial statement of the

entity. Auditor shall determine the threshold for materiality before analysing individual

liabilities. If the liability is lower than the limit it is considered to have insignificant

impact on financial statement (Byrnes et al., 2015).

Probability of occurrence – probability of the event shall be estimated for determining its

impact on financial statement of the entity. Levels of probability are remote, probable and

reasonably probable, however only the probable and reasonably probable items shall be

disclosed as contingencies.

Journal entries for the probable events – while the contingency is probable, the entity

shall provide the same in the general ledger. For instance, pending lawsuit shall be

recorded as debit to the legal expenses and credit to the accrued liabilities. However, if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITS AND ETHICS

the amount cannot be estimated it shall be mentioned in the disclosure that the amount

cannot be estimated.

Section 2

Preliminary analytical review is defined as procedure of management’s inquiry as well as

analytical procedure that are applied at the audit planning stage. Within the standard of risk

assessment he auditor shall perform the risk assessment procedure including the analytical

procedure as well as the management’s inquiry. The procedure of risk assessment further

includes performing inspection as well as observation procedure that is focussed on the gaining

understanding of internal control procedure of the organisation. Hence, the preliminary analytical

review procedure involves significant component of the procedure for risk assessment. One of

the procedures for preliminary analytical review is conducting ratio analysis to identify the areas

of significant changes (Christensen et al., 2016).

the amount cannot be estimated it shall be mentioned in the disclosure that the amount

cannot be estimated.

Section 2

Preliminary analytical review is defined as procedure of management’s inquiry as well as

analytical procedure that are applied at the audit planning stage. Within the standard of risk

assessment he auditor shall perform the risk assessment procedure including the analytical

procedure as well as the management’s inquiry. The procedure of risk assessment further

includes performing inspection as well as observation procedure that is focussed on the gaining

understanding of internal control procedure of the organisation. Hence, the preliminary analytical

review procedure involves significant component of the procedure for risk assessment. One of

the procedures for preliminary analytical review is conducting ratio analysis to identify the areas

of significant changes (Christensen et al., 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITS AND ETHICS

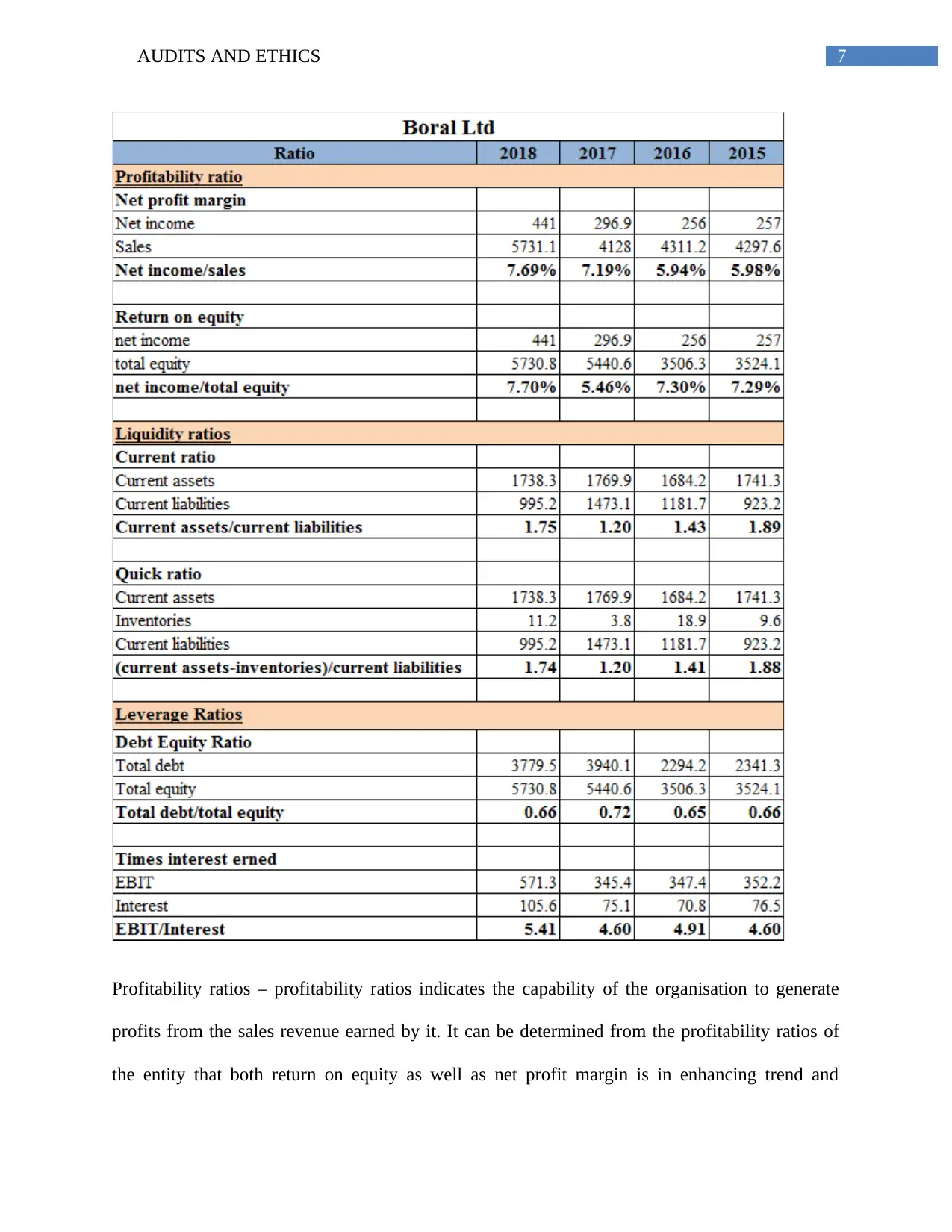

Profitability ratios – profitability ratios indicates the capability of the organisation to generate

profits from the sales revenue earned by it. It can be determined from the profitability ratios of

the entity that both return on equity as well as net profit margin is in enhancing trend and

Profitability ratios – profitability ratios indicates the capability of the organisation to generate

profits from the sales revenue earned by it. It can be determined from the profitability ratios of

the entity that both return on equity as well as net profit margin is in enhancing trend and

8AUDITS AND ETHICS

increased from 7.29% to 7.70% and 5.98% to 7.69% respectively over the time period of last 4

years. Audit risk involved with increasing trend of profit is inflation of revenues (Lai, Melloni &

Stacchezzini, 2017).

Liquidity ratios – liquidity ratios determine the ability of the entity to meet its short term

liabilities upon becoming due. It can be determined from the liquidity ratios of the entity that

both quick assets as well current ratios are in reducing trend and increased from 1.88 to 1.74 and

1.89 to 1.75 respectively over the time period of last 4 years. Audit risk involved with reducing

trend of liquidity ratios is deflation of cash and other assets (Christensen et al., 2016).

Leverage ratios – it signifies the gearing position of the entity though focussing on the proportion

of equity and borrowing in its capital structure. It can be determined from the leverage ratios of

the entity that the debt equity ratio of the company remained at same level that is at 0.6 over the

past 4 year and the times interest earned increased from 4.60 times to 5.41 times (Knechel &

Salterio, 2016).

Going through the trend of the ratios calculated above it can be stated that the following

accounts shall be selected for analytical review –

Revenues – revenues of the entity for the past 4 years are in improving trend and

increased from $ 4297.6 million to $ 5731.1 million. Assertions involved with sales

revenues are – (i) accuracy that is all the sales transactions are recorded at full amount

and without any error (ii) cut-off that is the recorded transaction for sales belongs to the

period for which the statement is prepared (Kharisova & Kozlova, 2014). Audit

procedure to be followed for assertion are (i) accuracy – reconcile the recorded balance

increased from 7.29% to 7.70% and 5.98% to 7.69% respectively over the time period of last 4

years. Audit risk involved with increasing trend of profit is inflation of revenues (Lai, Melloni &

Stacchezzini, 2017).

Liquidity ratios – liquidity ratios determine the ability of the entity to meet its short term

liabilities upon becoming due. It can be determined from the liquidity ratios of the entity that

both quick assets as well current ratios are in reducing trend and increased from 1.88 to 1.74 and

1.89 to 1.75 respectively over the time period of last 4 years. Audit risk involved with reducing

trend of liquidity ratios is deflation of cash and other assets (Christensen et al., 2016).

Leverage ratios – it signifies the gearing position of the entity though focussing on the proportion

of equity and borrowing in its capital structure. It can be determined from the leverage ratios of

the entity that the debt equity ratio of the company remained at same level that is at 0.6 over the

past 4 year and the times interest earned increased from 4.60 times to 5.41 times (Knechel &

Salterio, 2016).

Going through the trend of the ratios calculated above it can be stated that the following

accounts shall be selected for analytical review –

Revenues – revenues of the entity for the past 4 years are in improving trend and

increased from $ 4297.6 million to $ 5731.1 million. Assertions involved with sales

revenues are – (i) accuracy that is all the sales transactions are recorded at full amount

and without any error (ii) cut-off that is the recorded transaction for sales belongs to the

period for which the statement is prepared (Kharisova & Kozlova, 2014). Audit

procedure to be followed for assertion are (i) accuracy – reconcile the recorded balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITS AND ETHICS

with sales register (ii) cut – off – verifying the balances of cash and account receivable

(Glover & Prawitt, 2014).

Cash – cash and cash equivalent balance has significantly reduced from $ 237.8 million

to $ 74.3 million over the past 2 years. Assertions involved with cash balances are – (i)

existence that is all the cash transactions are recorded at full amount and without any

error (ii) completeness that is all the cash transactions have been recorded at the time of

statement preparation. Audit procedure to be followed for assertion are (i) existence –

reconciling the cash balance with bank balance randomly (ii) completeness – cash books

and cash registers shall be matched with the reported cash balance (Eilifsen & Messier,

2014)

Section 3

Review of cash flow statement

Major amount of cash inflow provided by operational activities and the amount is $ 578

million

Major amount of cash outflows was towards financing activities and the amount is $

398.2 million (Boral.com, 2019).

Primary source of cash receipt is cash received from the customers and the amount was $

6,209 million and major amount of payments amounting to $ 5399.1 million that is made

to the suppliers.

During the year closed on 30th June 2018 the entity did not report any non-cash investing

as well as financing activities (Boral.com, 2019).

with sales register (ii) cut – off – verifying the balances of cash and account receivable

(Glover & Prawitt, 2014).

Cash – cash and cash equivalent balance has significantly reduced from $ 237.8 million

to $ 74.3 million over the past 2 years. Assertions involved with cash balances are – (i)

existence that is all the cash transactions are recorded at full amount and without any

error (ii) completeness that is all the cash transactions have been recorded at the time of

statement preparation. Audit procedure to be followed for assertion are (i) existence –

reconciling the cash balance with bank balance randomly (ii) completeness – cash books

and cash registers shall be matched with the reported cash balance (Eilifsen & Messier,

2014)

Section 3

Review of cash flow statement

Major amount of cash inflow provided by operational activities and the amount is $ 578

million

Major amount of cash outflows was towards financing activities and the amount is $

398.2 million (Boral.com, 2019).

Primary source of cash receipt is cash received from the customers and the amount was $

6,209 million and major amount of payments amounting to $ 5399.1 million that is made

to the suppliers.

During the year closed on 30th June 2018 the entity did not report any non-cash investing

as well as financing activities (Boral.com, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITS AND ETHICS

Going concern – it can be verified from the cash flow statement of the entity for the year ended

2018 that the cash used for financing activities amounted to $ 344.6 million whereas in 2017 the

cash inflow amounted to $ 3107 million from the same activity. Further, the cash and cash

equivalent balance has significantly reduced from $ 237.8 million to $ 74.3 million over the past

2 years (Boral.com, 2019). These facts will raise significant issue in going concern assumption.

Audit procedure that required to be followed for the same is 1st of all the reason behind this

major variation over the last 2 years shall be verified with the management. Further, the cash

books shall be reconciled with bank balance randomly and cash books and cash registers shall be

matched with the reported cash balance (William, Glover & Prawitt, 2016).

Review of audit report

Audit for the year 2018 has been carried out by KPMG and they expressed unmodified

opinion. As per the auditor’ opinion the financial statement of the entity are prepared and

delivered in true and fair manner and is representing true and fair view of the financial

performance as well as position of the company (Boral.com, 2019).

Additional issues mentioned by the auditor as key audit matters are –

Availability as well as recoverability of US tax loss assets Carrying value for goodwill of North America PPA (purchase price allocation) accounting associated to acquisition of Headwaters Carrying value of investment made in Meridian bank JV and USG Boral JV (Boral.com,

2019).

Going concern – it can be verified from the cash flow statement of the entity for the year ended

2018 that the cash used for financing activities amounted to $ 344.6 million whereas in 2017 the

cash inflow amounted to $ 3107 million from the same activity. Further, the cash and cash

equivalent balance has significantly reduced from $ 237.8 million to $ 74.3 million over the past

2 years (Boral.com, 2019). These facts will raise significant issue in going concern assumption.

Audit procedure that required to be followed for the same is 1st of all the reason behind this

major variation over the last 2 years shall be verified with the management. Further, the cash

books shall be reconciled with bank balance randomly and cash books and cash registers shall be

matched with the reported cash balance (William, Glover & Prawitt, 2016).

Review of audit report

Audit for the year 2018 has been carried out by KPMG and they expressed unmodified

opinion. As per the auditor’ opinion the financial statement of the entity are prepared and

delivered in true and fair manner and is representing true and fair view of the financial

performance as well as position of the company (Boral.com, 2019).

Additional issues mentioned by the auditor as key audit matters are –

Availability as well as recoverability of US tax loss assets Carrying value for goodwill of North America PPA (purchase price allocation) accounting associated to acquisition of Headwaters Carrying value of investment made in Meridian bank JV and USG Boral JV (Boral.com,

2019).

11AUDITS AND ETHICS

References

Auasb.gov.au. (2019). Retrieved 9 May 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/AUS_306.pdf

Boral.com. (2019). Retrieved 9 May 2019, from

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. &

Vasarhelyi, M., (2015). Evolution of auditing: From the traditional approach to the future

audit. Audit Analytics, 71.

Christensen, B. E., Glover, S. M., Omer, T. C., & Shelley, M. K. (2016). Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), 1648-1684.

Christensen, B.E., Glover, S.M. & Wood, D.A., (2013). Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Coetzee, P. & Lubbe, D., (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Eilifsen, A. & Messier Jr, W.F., (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. & Prawitt, D.F., (2014). Enhancing auditor professional skepticism: The

professional skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

References

Auasb.gov.au. (2019). Retrieved 9 May 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/AUS_306.pdf

Boral.com. (2019). Retrieved 9 May 2019, from

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. &

Vasarhelyi, M., (2015). Evolution of auditing: From the traditional approach to the future

audit. Audit Analytics, 71.

Christensen, B. E., Glover, S. M., Omer, T. C., & Shelley, M. K. (2016). Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), 1648-1684.

Christensen, B.E., Glover, S.M. & Wood, D.A., (2013). Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Coetzee, P. & Lubbe, D., (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Eilifsen, A. & Messier Jr, W.F., (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. & Prawitt, D.F., (2014). Enhancing auditor professional skepticism: The

professional skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.