CQUniversity ACCT20075 Auditing and Ethics Report: FMG Analysis 2018

VerifiedAdded on 2023/01/20

|18

|3002

|20

Report

AI Summary

This report, prepared for CQUniversity's ACCT20075 course, analyzes the auditing and ethics of Fortescue Metals Group (FMG). It begins by establishing materiality, outlining audit procedures for significant events like contingent liabilities and capital commitments. The report then delves into ratio calculations, interpreting trends in profitability, liquidity, and solvency to identify key risk areas, such as decreasing profitability and cash management issues. Furthermore, it examines cash flow activities, highlighting the significant cash outflow in 2018, and assesses the company's going concern status. The report concludes with an overview of audit opinions based on the financial analysis conducted, offering a comprehensive view of FMG's financial health and compliance with auditing standards.

AUDITING AND ETHICS

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Section 1.....................................................................................................................................4

Materiality of financial statements.........................................................................................4

Outline of audit procedures for significant events.................................................................4

Section 2.....................................................................................................................................6

Ratio Calculation....................................................................................................................6

Analysis and interpretation.....................................................................................................6

Section 3.....................................................................................................................................9

Cash flow activities................................................................................................................9

Going concern......................................................................................................................10

Audit opinion........................................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

2

Introduction................................................................................................................................3

Section 1.....................................................................................................................................4

Materiality of financial statements.........................................................................................4

Outline of audit procedures for significant events.................................................................4

Section 2.....................................................................................................................................6

Ratio Calculation....................................................................................................................6

Analysis and interpretation.....................................................................................................6

Section 3.....................................................................................................................................9

Cash flow activities................................................................................................................9

Going concern......................................................................................................................10

Audit opinion........................................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

2

Introduction

There are legal foundations on the business organization to conduct audit under the

supervision of registered auditor at the end of every financial year with regard to financial

data provided in financial statements. Importance of auditing in a banking organization

increases as the general public and government organizations have a significant interest in the

performance of these organization (Cohen & Simnett, 2014). Mismanagement or fraud on

part of banking organization can impact the whole economy. In addition to that importance of

auditing also increases as it identifies risk management in internal control measures applied

by the organization. Therefore it can be said that with the help of identifying deficiencies,

management of the company can improve internal operations. Different aspects of auditing

and internal control will be discussed in this report by considering the business operations of

the Fortescue Metals Group.

3

There are legal foundations on the business organization to conduct audit under the

supervision of registered auditor at the end of every financial year with regard to financial

data provided in financial statements. Importance of auditing in a banking organization

increases as the general public and government organizations have a significant interest in the

performance of these organization (Cohen & Simnett, 2014). Mismanagement or fraud on

part of banking organization can impact the whole economy. In addition to that importance of

auditing also increases as it identifies risk management in internal control measures applied

by the organization. Therefore it can be said that with the help of identifying deficiencies,

management of the company can improve internal operations. Different aspects of auditing

and internal control will be discussed in this report by considering the business operations of

the Fortescue Metals Group.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 1

The materiality of financial statements

It is very important for an auditor to identify the level of materiality before starting the

process of audit. This type of materiality helps auditors to understand the level at which a

particular error omission can be considered as material in the decision-making process of

stakeholders. Audit materiality can be defined as a threshold limit up to which all the errors

and omissions are considered as not having any impact on the decision making the process of

stakeholder (Edgley, 2014).

There are various methods that can be used for calculation of audit materiality i.e. on the

basis of total assets, total revenue, total net profit, etc. In the case of Fortescue Metals Group,

audit materiality will be calculated on the basis of total revenue generated by the organization

in the last financial year i.e. 2018. Here total revenue is selected for calculation of materiality

rather than total assets or total profits (Cox, Dayanandan & Donker, 2014). This is due to the

fact that business organization is operating in a very competitive market and revenue

generated by business organization indicates the popularity of product and services in a

dynamic environment.

Audit materiality= Total sales* 0.5%

= $6,887 million* 0.5%

= $ 34.435 million

On the basis of this calculation, it can be said that if the total amount of errors and omissions

in auditing of this organization increases beyond $34.435 million then it should be considered

as material.

Outline of audit procedures for significant events

There are various events in business organization presented in notes to accounts that can have

a significant impact on financial performance and productivity of the business organization. It

is important to consider these events separately as they are not presented in financial

statements but still impacts business operations is significant. Following are some of these

events along with audit procedure that will help in identifying accuracy and impact on

business operations-

4

The materiality of financial statements

It is very important for an auditor to identify the level of materiality before starting the

process of audit. This type of materiality helps auditors to understand the level at which a

particular error omission can be considered as material in the decision-making process of

stakeholders. Audit materiality can be defined as a threshold limit up to which all the errors

and omissions are considered as not having any impact on the decision making the process of

stakeholder (Edgley, 2014).

There are various methods that can be used for calculation of audit materiality i.e. on the

basis of total assets, total revenue, total net profit, etc. In the case of Fortescue Metals Group,

audit materiality will be calculated on the basis of total revenue generated by the organization

in the last financial year i.e. 2018. Here total revenue is selected for calculation of materiality

rather than total assets or total profits (Cox, Dayanandan & Donker, 2014). This is due to the

fact that business organization is operating in a very competitive market and revenue

generated by business organization indicates the popularity of product and services in a

dynamic environment.

Audit materiality= Total sales* 0.5%

= $6,887 million* 0.5%

= $ 34.435 million

On the basis of this calculation, it can be said that if the total amount of errors and omissions

in auditing of this organization increases beyond $34.435 million then it should be considered

as material.

Outline of audit procedures for significant events

There are various events in business organization presented in notes to accounts that can have

a significant impact on financial performance and productivity of the business organization. It

is important to consider these events separately as they are not presented in financial

statements but still impacts business operations is significant. Following are some of these

events along with audit procedure that will help in identifying accuracy and impact on

business operations-

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contingent liabilities

These are the liabilities that have not impacted business operations in the latest financial year

under consideration but its impact in future can be significant (Cao, Chychyla & Stewart,

2015).

Fortescue has been operating in offices and other premises that are on lease and these leases

will expire in next one to three financial years. It is important for an organization to make

sure that business organization has fixed the place of operation at all the time as non-

availability of such premises can have a significant negative impact on a business

organization due to disturbance of day-to-day operations.

Auditor of the company should identify whether management of the company has made

sufficient arrangements to renew the lease agreement or arrange a new place for business

operations. In case of management has arranged for a place for business operation, the auditor

should evaluate whether the organization has prepared sufficiently to plans to make sure that

a transition of officers has no impact on day to day operations (Koren, Kosi & Valentincic,

2014).

Capital commitments- Management of the organization is in contractual liability for

construction of iron ore carriers worth $43 million in the next financial year i.e. 2019. This

type of capital expenditure will have a significant impact on the financial and liquidity

position of the company (Lewis, Neiberline & Steinhoff, 2014). Auditor of the organization is

required to identify whether sufficient sources of finance are arranged by a business

organization to make sure that such capital commitment will be met.

5

These are the liabilities that have not impacted business operations in the latest financial year

under consideration but its impact in future can be significant (Cao, Chychyla & Stewart,

2015).

Fortescue has been operating in offices and other premises that are on lease and these leases

will expire in next one to three financial years. It is important for an organization to make

sure that business organization has fixed the place of operation at all the time as non-

availability of such premises can have a significant negative impact on a business

organization due to disturbance of day-to-day operations.

Auditor of the company should identify whether management of the company has made

sufficient arrangements to renew the lease agreement or arrange a new place for business

operations. In case of management has arranged for a place for business operation, the auditor

should evaluate whether the organization has prepared sufficiently to plans to make sure that

a transition of officers has no impact on day to day operations (Koren, Kosi & Valentincic,

2014).

Capital commitments- Management of the organization is in contractual liability for

construction of iron ore carriers worth $43 million in the next financial year i.e. 2019. This

type of capital expenditure will have a significant impact on the financial and liquidity

position of the company (Lewis, Neiberline & Steinhoff, 2014). Auditor of the organization is

required to identify whether sufficient sources of finance are arranged by a business

organization to make sure that such capital commitment will be met.

5

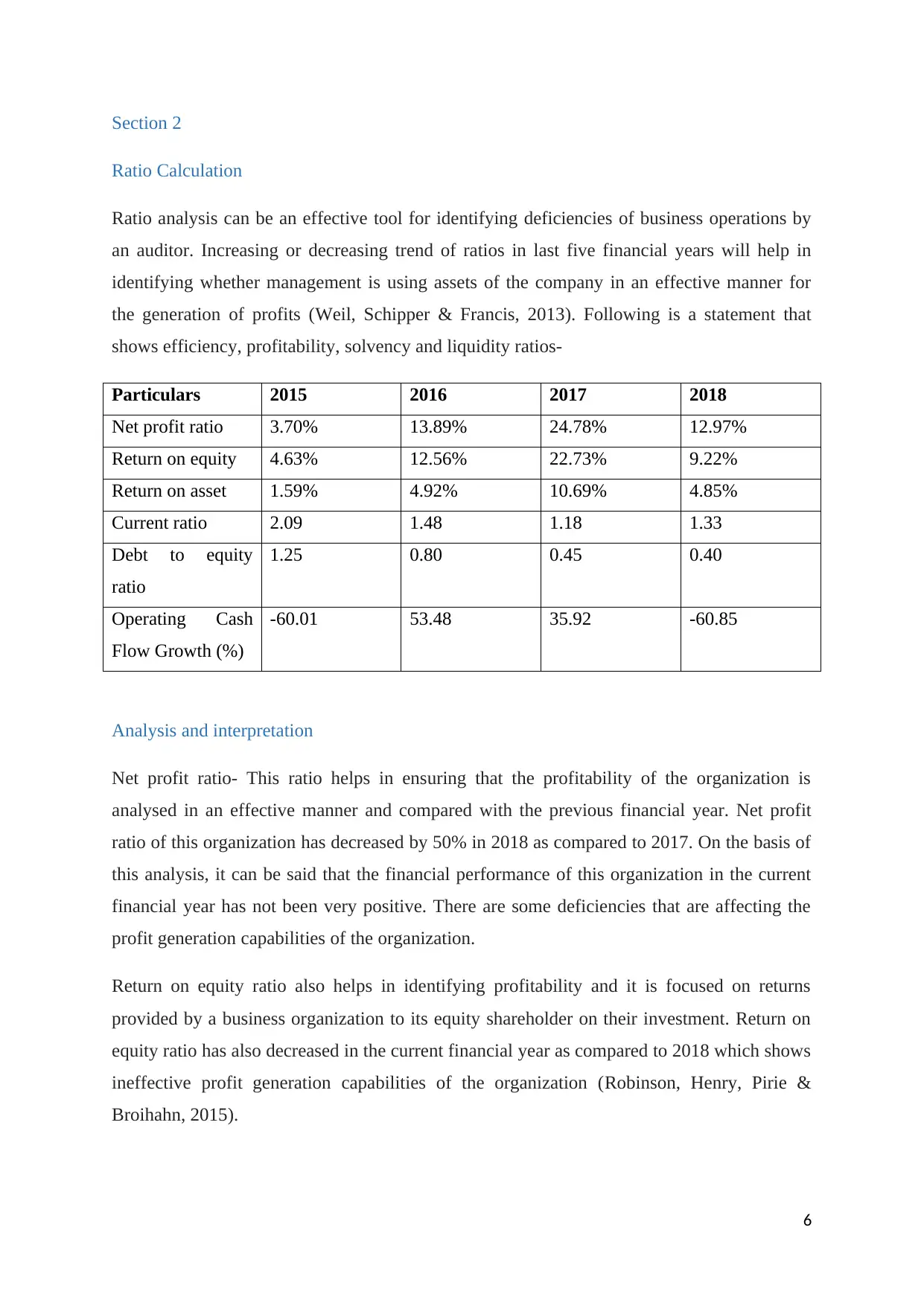

Section 2

Ratio Calculation

Ratio analysis can be an effective tool for identifying deficiencies of business operations by

an auditor. Increasing or decreasing trend of ratios in last five financial years will help in

identifying whether management is using assets of the company in an effective manner for

the generation of profits (Weil, Schipper & Francis, 2013). Following is a statement that

shows efficiency, profitability, solvency and liquidity ratios-

Particulars 2015 2016 2017 2018

Net profit ratio 3.70% 13.89% 24.78% 12.97%

Return on equity 4.63% 12.56% 22.73% 9.22%

Return on asset 1.59% 4.92% 10.69% 4.85%

Current ratio 2.09 1.48 1.18 1.33

Debt to equity

ratio

1.25 0.80 0.45 0.40

Operating Cash

Flow Growth (%)

-60.01 53.48 35.92 -60.85

Analysis and interpretation

Net profit ratio- This ratio helps in ensuring that the profitability of the organization is

analysed in an effective manner and compared with the previous financial year. Net profit

ratio of this organization has decreased by 50% in 2018 as compared to 2017. On the basis of

this analysis, it can be said that the financial performance of this organization in the current

financial year has not been very positive. There are some deficiencies that are affecting the

profit generation capabilities of the organization.

Return on equity ratio also helps in identifying profitability and it is focused on returns

provided by a business organization to its equity shareholder on their investment. Return on

equity ratio has also decreased in the current financial year as compared to 2018 which shows

ineffective profit generation capabilities of the organization (Robinson, Henry, Pirie &

Broihahn, 2015).

6

Ratio Calculation

Ratio analysis can be an effective tool for identifying deficiencies of business operations by

an auditor. Increasing or decreasing trend of ratios in last five financial years will help in

identifying whether management is using assets of the company in an effective manner for

the generation of profits (Weil, Schipper & Francis, 2013). Following is a statement that

shows efficiency, profitability, solvency and liquidity ratios-

Particulars 2015 2016 2017 2018

Net profit ratio 3.70% 13.89% 24.78% 12.97%

Return on equity 4.63% 12.56% 22.73% 9.22%

Return on asset 1.59% 4.92% 10.69% 4.85%

Current ratio 2.09 1.48 1.18 1.33

Debt to equity

ratio

1.25 0.80 0.45 0.40

Operating Cash

Flow Growth (%)

-60.01 53.48 35.92 -60.85

Analysis and interpretation

Net profit ratio- This ratio helps in ensuring that the profitability of the organization is

analysed in an effective manner and compared with the previous financial year. Net profit

ratio of this organization has decreased by 50% in 2018 as compared to 2017. On the basis of

this analysis, it can be said that the financial performance of this organization in the current

financial year has not been very positive. There are some deficiencies that are affecting the

profit generation capabilities of the organization.

Return on equity ratio also helps in identifying profitability and it is focused on returns

provided by a business organization to its equity shareholder on their investment. Return on

equity ratio has also decreased in the current financial year as compared to 2018 which shows

ineffective profit generation capabilities of the organization (Robinson, Henry, Pirie &

Broihahn, 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identification of capabilities of using total assets for generation of profit by using effective

and efficient management practices can be identified with the help of return on total asset

ratio. On the basis of calculation done in the above section, it can be said that the return on

asset ratio of the organization has also decreased by more than 50% during 2018. This is due

to the fact that management has not been able to generate effective profits in 2018.

The current ratio helps in identifying the liquidity position of the company in the market by

comparing total current assets and current liabilities. It can be said that management of the

company has sufficient current assets for payment of current liabilities in 2018 as the current

ratio is more than 1 (Brigham, Ehrhardt, Nason & Gessaroli, 2016). The liquidity position of

a business organization with a current ratio of 1 is considered to be average as the optimum

current ratio is 2:1 which was achieved by this organization in 2015.

Debt equity ratio- debt-equity ratio shows the efficiency of capital structure in a particular

organization. Debt to equity ratio of Fortescue Metals Group is decreasing on a constant basis

from 2015 to 2018. It has decreased from 1.25 in 2015 0.40 in 2018 which shows that

business organization is becoming more equity intrinsic which will result in mismanagement

due to interference from different stakeholders (Edwards, 2013).

Operating cash flow growth ratio helps in identifying the efficiency of the cash management

practices undertaken by a business organization. A business organization is considered to be

effective and efficient if the total of cash generated from the operational activity is increasing

on a yearly basis. This has not been the case for Fortescue Metals Group as the real growth

rate of operating cash flow is decreasing (Easton & Sommers, 2018). In the financial year,

2018 total cash generated from operating activities has decreased by 60.85%. It clearly shows

that management of the financial position and standing of the organization is not very

effective in the market.

On an overall analysis, it can be said that the profitability of the organization is the main root

cause for the current financial position of Fortescue Metals Group. Internal and external

analysis should be conducted by the auditor of the company. If the profitability of other

organizations operating in this industry is also decreased as compared to 2017 when it can be

said that there are market factors that affecting profitability (Brooks and Mukherjee, 2013).

On the other hand if operating profitability of other organization in stronger than there is a

deficiency in internal management practices of Fortescue Metals Group.

7

and efficient management practices can be identified with the help of return on total asset

ratio. On the basis of calculation done in the above section, it can be said that the return on

asset ratio of the organization has also decreased by more than 50% during 2018. This is due

to the fact that management has not been able to generate effective profits in 2018.

The current ratio helps in identifying the liquidity position of the company in the market by

comparing total current assets and current liabilities. It can be said that management of the

company has sufficient current assets for payment of current liabilities in 2018 as the current

ratio is more than 1 (Brigham, Ehrhardt, Nason & Gessaroli, 2016). The liquidity position of

a business organization with a current ratio of 1 is considered to be average as the optimum

current ratio is 2:1 which was achieved by this organization in 2015.

Debt equity ratio- debt-equity ratio shows the efficiency of capital structure in a particular

organization. Debt to equity ratio of Fortescue Metals Group is decreasing on a constant basis

from 2015 to 2018. It has decreased from 1.25 in 2015 0.40 in 2018 which shows that

business organization is becoming more equity intrinsic which will result in mismanagement

due to interference from different stakeholders (Edwards, 2013).

Operating cash flow growth ratio helps in identifying the efficiency of the cash management

practices undertaken by a business organization. A business organization is considered to be

effective and efficient if the total of cash generated from the operational activity is increasing

on a yearly basis. This has not been the case for Fortescue Metals Group as the real growth

rate of operating cash flow is decreasing (Easton & Sommers, 2018). In the financial year,

2018 total cash generated from operating activities has decreased by 60.85%. It clearly shows

that management of the financial position and standing of the organization is not very

effective in the market.

On an overall analysis, it can be said that the profitability of the organization is the main root

cause for the current financial position of Fortescue Metals Group. Internal and external

analysis should be conducted by the auditor of the company. If the profitability of other

organizations operating in this industry is also decreased as compared to 2017 when it can be

said that there are market factors that affecting profitability (Brooks and Mukherjee, 2013).

On the other hand if operating profitability of other organization in stronger than there is a

deficiency in internal management practices of Fortescue Metals Group.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Key risk areas

Decreasing profitability- overall profitability is decreasing on a regular basis therefore

management operation can be considered as key risk area in this scenarios. Auditor is

required to communicate with management regarding the basic deficiencies in the

management operations that are resulting in this decreased profitability.

Cash management- Cash is always very vulnerable to fraud, error or mistake and in given

scenario cash flow from operations are fluctuating significantly over the previous 5 years,

therefore cash is also a key area that required auditor’s attention. Auditor is required to

evaluate the policies that are used by management to manage cash and whether these policies

are actually followed by the management or not.

Section 3

Cash flow activities

Total cash outflow of Fortescue Metals Group in the year 2018 has been $961 million as

compared to total cash inflow of $259 million in the year 2017. It clearly shows that cash

management practices in the year 2018 have not been very effective as compared to 2017. In

addition to the two main problems of this organization is cash flow from operating activities

at it has decreased by 63% in 2018.

The main contributor that resulted in a cash outflow of $961 million in the year 2018 has

been cash outflow from financing activities. Total cash outflow from financing activities in

2018 is $1626 million. Primary activities in cash flow from financing activities are repayment

of borrowings and financial lease, the dividend paid, finance cost paid and purchase of shares

by employees share trust (Bhandari & Iyer, 2013). The outflow of this organization in 2018

has increased significantly due to the repayment of borrowing and financial analysis and this

type of business activities does not occur yearly basis but the management of the company

should focus on cash flow from operating activity. It is important that cash flow from

operating activities increases over the period of time.

8

Decreasing profitability- overall profitability is decreasing on a regular basis therefore

management operation can be considered as key risk area in this scenarios. Auditor is

required to communicate with management regarding the basic deficiencies in the

management operations that are resulting in this decreased profitability.

Cash management- Cash is always very vulnerable to fraud, error or mistake and in given

scenario cash flow from operations are fluctuating significantly over the previous 5 years,

therefore cash is also a key area that required auditor’s attention. Auditor is required to

evaluate the policies that are used by management to manage cash and whether these policies

are actually followed by the management or not.

Section 3

Cash flow activities

Total cash outflow of Fortescue Metals Group in the year 2018 has been $961 million as

compared to total cash inflow of $259 million in the year 2017. It clearly shows that cash

management practices in the year 2018 have not been very effective as compared to 2017. In

addition to the two main problems of this organization is cash flow from operating activities

at it has decreased by 63% in 2018.

The main contributor that resulted in a cash outflow of $961 million in the year 2018 has

been cash outflow from financing activities. Total cash outflow from financing activities in

2018 is $1626 million. Primary activities in cash flow from financing activities are repayment

of borrowings and financial lease, the dividend paid, finance cost paid and purchase of shares

by employees share trust (Bhandari & Iyer, 2013). The outflow of this organization in 2018

has increased significantly due to the repayment of borrowing and financial analysis and this

type of business activities does not occur yearly basis but the management of the company

should focus on cash flow from operating activity. It is important that cash flow from

operating activities increases over the period of time.

8

Other than financing activities following are some of the critical cash receipts and cash

payments are undertaken by the business organization in 2018-

Payments-

Purchase of property plant equipment

Purchase of financial assets

Payment made to suppliers and employees

Interest paid

Income Tax Paid

Receipts-

Cash generated from operations

Cash received from customers in exchange of products and services

Proceeds from disposal of fixed assets i.e. plant and machinery (Kroes & Manikas, 2014)

There were no non cash financial and investing activities in the financial year ending 2018 in

accordance with the financial accounts and noted to accounts issues by management.

Going concern

Cash flow activities of the organization it can be said that business operation is undertaken by

the Organization on a regular basis irrespective of the fact that it has decreased in the current

financial year. On the basis of frequent business activities, it can be said that there are no

probable chances of dissolution of this organization in the near future, therefore, there is no

risk of going concern for Fortescue Metals Group.

Following are the procedures that will help in identifying Going Concern risk in a particular

business organization-

Non-payment to of interest and principal amount on borrowings and loans from

financial institutions for a long period of time.

Decrease in total revenue of a business organization at a significant rate.

Constant selling of fixed asset, plants, and machinery to generate cash inflows.

9

payments are undertaken by the business organization in 2018-

Payments-

Purchase of property plant equipment

Purchase of financial assets

Payment made to suppliers and employees

Interest paid

Income Tax Paid

Receipts-

Cash generated from operations

Cash received from customers in exchange of products and services

Proceeds from disposal of fixed assets i.e. plant and machinery (Kroes & Manikas, 2014)

There were no non cash financial and investing activities in the financial year ending 2018 in

accordance with the financial accounts and noted to accounts issues by management.

Going concern

Cash flow activities of the organization it can be said that business operation is undertaken by

the Organization on a regular basis irrespective of the fact that it has decreased in the current

financial year. On the basis of frequent business activities, it can be said that there are no

probable chances of dissolution of this organization in the near future, therefore, there is no

risk of going concern for Fortescue Metals Group.

Following are the procedures that will help in identifying Going Concern risk in a particular

business organization-

Non-payment to of interest and principal amount on borrowings and loans from

financial institutions for a long period of time.

Decrease in total revenue of a business organization at a significant rate.

Constant selling of fixed asset, plants, and machinery to generate cash inflows.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

An increasing amount of debt component in the organization's capital structure

(William Jr, Glover & Prawitt, 2016). Increase in stock turnover ratios and non-

payment of salary and commission to employees.

Audit opinion

Audit opinion can be defined as the opening provided by the statutory auditor on financial

statements are prepared by a business organization. It is important that the audit opinion

provided by the auditor is unbiased. All the principles of the code of ethics and professional

behaviour should be followed while providing opinion on financial statements.

Auditor for the year 2018 has been undertaken by PricewaterhouseCoopers which is one of

the most reputed to audit firms in the world. Auditor of this organization has stated that true

and fair view of the financial position of the organization is depicted in financial statements

(Knechel and Salterio, 2016). There are no additional paragraphs or sections included by the

auditor in relation to audit issues.

10

(William Jr, Glover & Prawitt, 2016). Increase in stock turnover ratios and non-

payment of salary and commission to employees.

Audit opinion

Audit opinion can be defined as the opening provided by the statutory auditor on financial

statements are prepared by a business organization. It is important that the audit opinion

provided by the auditor is unbiased. All the principles of the code of ethics and professional

behaviour should be followed while providing opinion on financial statements.

Auditor for the year 2018 has been undertaken by PricewaterhouseCoopers which is one of

the most reputed to audit firms in the world. Auditor of this organization has stated that true

and fair view of the financial position of the organization is depicted in financial statements

(Knechel and Salterio, 2016). There are no additional paragraphs or sections included by the

auditor in relation to audit issues.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

An overall analysis it can be concluded that the financial position of this organization has not

been very effective in 2018 where is the financial position was better in the year 2017.

Different aspects of auditing are considered before making this conclusion such as cash flow

analysis, going concern analysis, ratio analysis, etc. in addition to that audit opinion provided

by the auditor of the organization is also considered while evaluating the financial position of

the company.

11

An overall analysis it can be concluded that the financial position of this organization has not

been very effective in 2018 where is the financial position was better in the year 2017.

Different aspects of auditing are considered before making this conclusion such as cash flow

analysis, going concern analysis, ratio analysis, etc. in addition to that audit opinion provided

by the auditor of the organization is also considered while evaluating the financial position of

the company.

11

References

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Brigham, E. F., Ehrhardt, M. C., Nason, R. R., & Gessaroli, J. (2016). Financial Managment:

Theory and Practice, Canadian Edition. Nelson Education.

Brooks, R., & Mukherjee, A. K. (2013). Financial management: core concepts. Pearson.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research

agenda. Auditing: A Journal of Practice & Theory, 34(1), 59-74.

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks:

A Canadian perspective. International Journal of Disclosure and Governance, 11(3),

284-298.

Easton, M., & Sommers, Z. (2018). Financial Statement Analysis & Valuation, 5e.

Edgley, C. (2014). A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), 255-271.

Edwards, J. R. (2013). A History of Financial Accounting (RLE Accounting). Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Koren, J., Kosi, U., & Valentincic, A. (2014). Does Financial Statement Audit Reduce the

Cost of Debt of Private Firms? Available at SSRN 2373987.

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of

Production Economics, 148, 37-50.

Lewis, A. C., Neiberline, C., & Steinhoff, J. C. (2014). DIGITAL AUDITING: Modernizing

the Government Financial Statement Audit Approach. Journal of Government

financial management, 63(1).

12

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Brigham, E. F., Ehrhardt, M. C., Nason, R. R., & Gessaroli, J. (2016). Financial Managment:

Theory and Practice, Canadian Edition. Nelson Education.

Brooks, R., & Mukherjee, A. K. (2013). Financial management: core concepts. Pearson.

Cao, M., Chychyla, R., & Stewart, T. (2015). Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), 423-429.

Cohen, J. R., & Simnett, R. (2014). CSR and assurance services: A research

agenda. Auditing: A Journal of Practice & Theory, 34(1), 59-74.

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks:

A Canadian perspective. International Journal of Disclosure and Governance, 11(3),

284-298.

Easton, M., & Sommers, Z. (2018). Financial Statement Analysis & Valuation, 5e.

Edgley, C. (2014). A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), 255-271.

Edwards, J. R. (2013). A History of Financial Accounting (RLE Accounting). Routledge.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Koren, J., Kosi, U., & Valentincic, A. (2014). Does Financial Statement Audit Reduce the

Cost of Debt of Private Firms? Available at SSRN 2373987.

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of

Production Economics, 148, 37-50.

Lewis, A. C., Neiberline, C., & Steinhoff, J. C. (2014). DIGITAL AUDITING: Modernizing

the Government Financial Statement Audit Approach. Journal of Government

financial management, 63(1).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.