CQUniversity ACCT20075 Auditing Report: Financial Statement Analysis

VerifiedAdded on 2022/11/26

|13

|2651

|325

Report

AI Summary

This report presents an in-depth analysis of auditing concepts and procedures applied to a chosen company, likely Macquarie Group, based on the provided content. It begins by defining materiality, its significance in auditing financial statements, and methods for its calculation. The report then performs an analytical review of the company's financial statements from 2016 to 2019, assessing key ratios like asset turnover, liquidity, and profitability. It identifies key risk areas, audit assertions at risk, and corresponding audit procedures. The report also analyzes the company's cash flow statements, highlighting major cash inflows and outflows. Finally, it discusses the type of audit opinion and the key audit matters, including exploration expenditure and site rehabilitation, concluding with a summary of the audit's findings and its overall sustainability and transparency.

AUDIT PROCEDURE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................3

Part-1.....................................................................................................................................................3

Requirement-1..................................................................................................................................3

Requirement-2......................................................................................................................................5

Section-2................................................................................................................................................5

Analytical review...............................................................................................................................5

Key risky areas, audit assertion for risk, and other audit procedure.................................................7

Sec-3......................................................................................................................................................8

Cash flow statements........................................................................................................................8

Type of audit opinion............................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Introduction...........................................................................................................................................3

Part-1.....................................................................................................................................................3

Requirement-1..................................................................................................................................3

Requirement-2......................................................................................................................................5

Section-2................................................................................................................................................5

Analytical review...............................................................................................................................5

Key risky areas, audit assertion for risk, and other audit procedure.................................................7

Sec-3......................................................................................................................................................8

Cash flow statements........................................................................................................................8

Type of audit opinion............................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Introduction

This report reveals the key understanding on the audit assertion and financial performance of

the company. The reporting brings out a discussion on understanding of materiality concept

in relation to financial statements of the organisation. This concept will help in examining the

auditing risk model of the Macquarie Group (Lakis, & Masiulevičius, 2017). In the initial

stage, this report has the description and significance of materiality in relation to audit of the

financial reports. Further, an analytical review of the Macquarie Group`s financial statements

are assessed. Further, cash flow statement of the Macquarie Group has been reviewed in

order to examine the maximum and minimum cash inflows and outflows of particular items

in the financial records (Barman, & Sengupta, 2017).

Part-1

Requirement-1

Description, nature, and significance of the materiality concept in relation to Audit of the financial

statements

Materiality depends on the size of the financial information. Materiality concept is well

known for the ability of the data to change the decisions of the user from the decision, which

was taken in the absence material data (Macquarie Group, 2017). The significance of material

concept regarding the set of financial reports have increased when the audit is being

conducted. Audit does not mean to monitor the whole information, which is given in the

financial statements, but it is also conducted on the basis of sample (Ussery et al., 2019). The

finding of sample has been from the total population which have higher importance and the

risk associated with it. This importance is determined by the calculating the materiality for

the financial reporting (Macquarie Group, 2018).

Different basis and consideration to compute the materiality

This report reveals the key understanding on the audit assertion and financial performance of

the company. The reporting brings out a discussion on understanding of materiality concept

in relation to financial statements of the organisation. This concept will help in examining the

auditing risk model of the Macquarie Group (Lakis, & Masiulevičius, 2017). In the initial

stage, this report has the description and significance of materiality in relation to audit of the

financial reports. Further, an analytical review of the Macquarie Group`s financial statements

are assessed. Further, cash flow statement of the Macquarie Group has been reviewed in

order to examine the maximum and minimum cash inflows and outflows of particular items

in the financial records (Barman, & Sengupta, 2017).

Part-1

Requirement-1

Description, nature, and significance of the materiality concept in relation to Audit of the financial

statements

Materiality depends on the size of the financial information. Materiality concept is well

known for the ability of the data to change the decisions of the user from the decision, which

was taken in the absence material data (Macquarie Group, 2017). The significance of material

concept regarding the set of financial reports have increased when the audit is being

conducted. Audit does not mean to monitor the whole information, which is given in the

financial statements, but it is also conducted on the basis of sample (Ussery et al., 2019). The

finding of sample has been from the total population which have higher importance and the

risk associated with it. This importance is determined by the calculating the materiality for

the financial reporting (Macquarie Group, 2018).

Different basis and consideration to compute the materiality

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

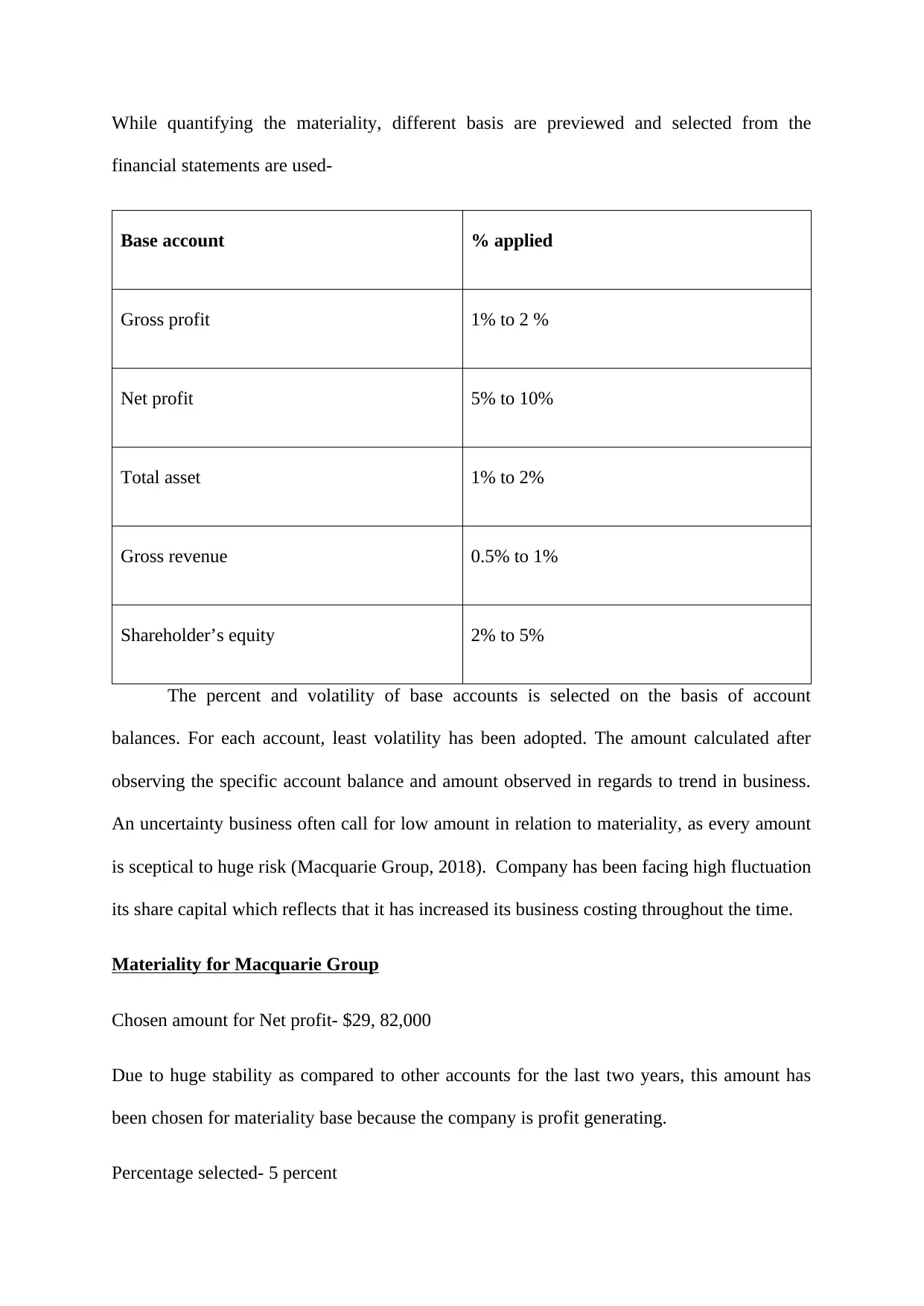

While quantifying the materiality, different basis are previewed and selected from the

financial statements are used-

Base account % applied

Gross profit 1% to 2 %

Net profit 5% to 10%

Total asset 1% to 2%

Gross revenue 0.5% to 1%

Shareholder’s equity 2% to 5%

The percent and volatility of base accounts is selected on the basis of account

balances. For each account, least volatility has been adopted. The amount calculated after

observing the specific account balance and amount observed in regards to trend in business.

An uncertainty business often call for low amount in relation to materiality, as every amount

is sceptical to huge risk (Macquarie Group, 2018). Company has been facing high fluctuation

its share capital which reflects that it has increased its business costing throughout the time.

Materiality for Macquarie Group

Chosen amount for Net profit- $29, 82,000

Due to huge stability as compared to other accounts for the last two years, this amount has

been chosen for materiality base because the company is profit generating.

Percentage selected- 5 percent

financial statements are used-

Base account % applied

Gross profit 1% to 2 %

Net profit 5% to 10%

Total asset 1% to 2%

Gross revenue 0.5% to 1%

Shareholder’s equity 2% to 5%

The percent and volatility of base accounts is selected on the basis of account

balances. For each account, least volatility has been adopted. The amount calculated after

observing the specific account balance and amount observed in regards to trend in business.

An uncertainty business often call for low amount in relation to materiality, as every amount

is sceptical to huge risk (Macquarie Group, 2018). Company has been facing high fluctuation

its share capital which reflects that it has increased its business costing throughout the time.

Materiality for Macquarie Group

Chosen amount for Net profit- $29, 82,000

Due to huge stability as compared to other accounts for the last two years, this amount has

been chosen for materiality base because the company is profit generating.

Percentage selected- 5 percent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Base amount- $20, 63,000

Materiality for Macquarie Group- $15, 60,000

It has been seen that the base amount has decreased in order to reach materiality for the audit

for the two reasons. This seems that risk is higher (Macquarie Group, 2016). The materiality

test is set with a view to assess the viability of the recorded financial details of the company.

Requirement-2

Significant drafts and notes

DRAFT OR NOTE AUDIT PROCEDURE

Contingent liabilities: From the

Financial reports, it is seen that the

value of contingent liabilities has

decreased by 20 percent (Macquarie

Group, 2016).

Monitoring the legal expenses closely

Review and examination of internal

revenue service reporting

Related party transactions:

From the annual reports, it is seen that

the transactions undertaken from the

account payable account has increased

in 2018 as compared to 2017

(Macquarie Group, 2018).

Getting the written confirmation

regarding the verification of relevant

parties to which the transactions have

been undertaken at arm`s length pricing

system.

Materiality for Macquarie Group- $15, 60,000

It has been seen that the base amount has decreased in order to reach materiality for the audit

for the two reasons. This seems that risk is higher (Macquarie Group, 2016). The materiality

test is set with a view to assess the viability of the recorded financial details of the company.

Requirement-2

Significant drafts and notes

DRAFT OR NOTE AUDIT PROCEDURE

Contingent liabilities: From the

Financial reports, it is seen that the

value of contingent liabilities has

decreased by 20 percent (Macquarie

Group, 2016).

Monitoring the legal expenses closely

Review and examination of internal

revenue service reporting

Related party transactions:

From the annual reports, it is seen that

the transactions undertaken from the

account payable account has increased

in 2018 as compared to 2017

(Macquarie Group, 2018).

Getting the written confirmation

regarding the verification of relevant

parties to which the transactions have

been undertaken at arm`s length pricing

system.

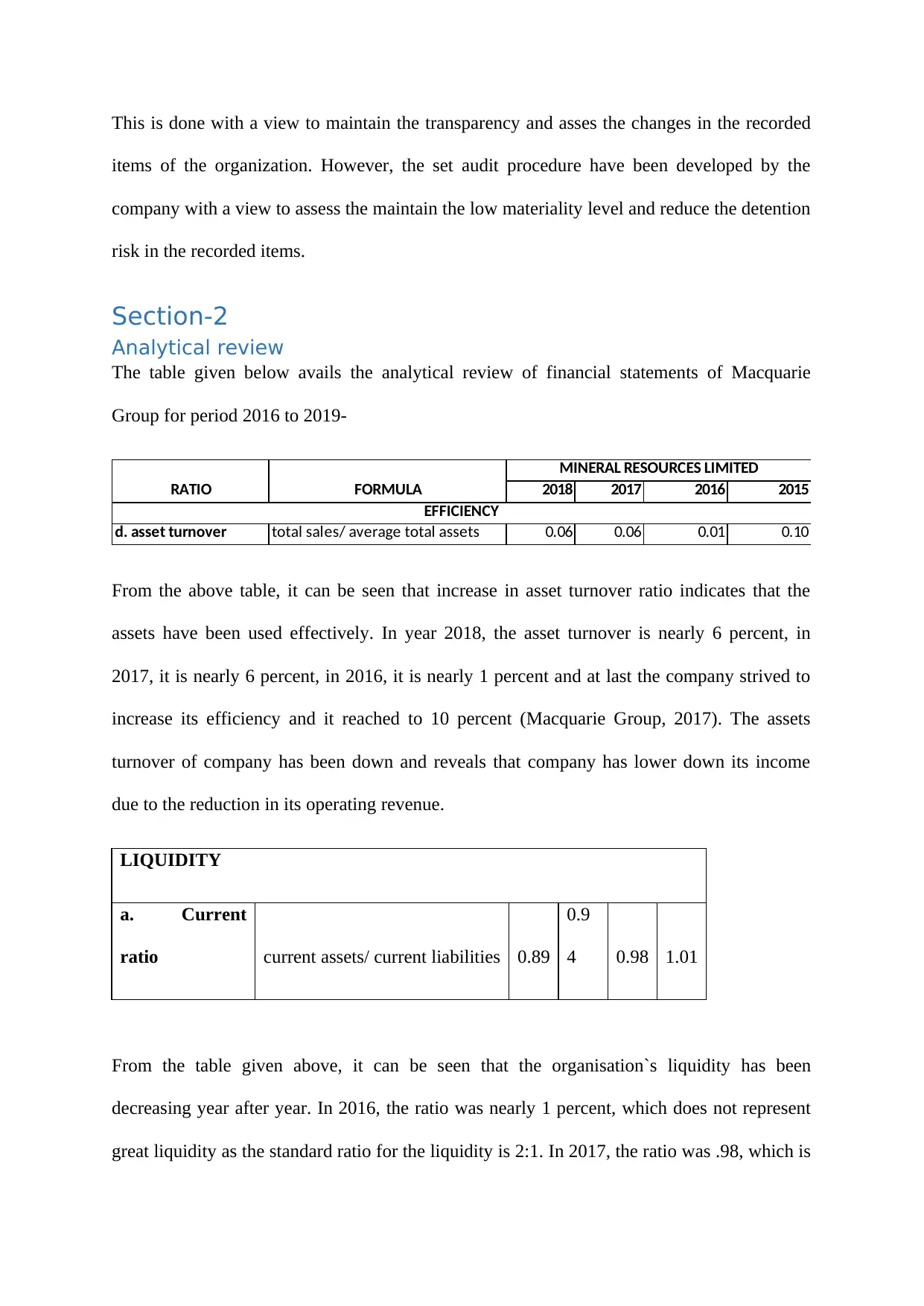

This is done with a view to maintain the transparency and asses the changes in the recorded

items of the organization. However, the set audit procedure have been developed by the

company with a view to assess the maintain the low materiality level and reduce the detention

risk in the recorded items.

Section-2

Analytical review

The table given below avails the analytical review of financial statements of Macquarie

Group for period 2016 to 2019-

2018 2017 2016 2015

d. asset turnover total sales/ average total assets 0.06 0.06 0.01 0.10

RATIO FORMULA

MINERAL RESOURCES LIMITED

EFFICIENCY

From the above table, it can be seen that increase in asset turnover ratio indicates that the

assets have been used effectively. In year 2018, the asset turnover is nearly 6 percent, in

2017, it is nearly 6 percent, in 2016, it is nearly 1 percent and at last the company strived to

increase its efficiency and it reached to 10 percent (Macquarie Group, 2017). The assets

turnover of company has been down and reveals that company has lower down its income

due to the reduction in its operating revenue.

LIQUIDITY

a. Current

ratio current assets/ current liabilities 0.89

0.9

4 0.98 1.01

From the table given above, it can be seen that the organisation`s liquidity has been

decreasing year after year. In 2016, the ratio was nearly 1 percent, which does not represent

great liquidity as the standard ratio for the liquidity is 2:1. In 2017, the ratio was .98, which is

items of the organization. However, the set audit procedure have been developed by the

company with a view to assess the maintain the low materiality level and reduce the detention

risk in the recorded items.

Section-2

Analytical review

The table given below avails the analytical review of financial statements of Macquarie

Group for period 2016 to 2019-

2018 2017 2016 2015

d. asset turnover total sales/ average total assets 0.06 0.06 0.01 0.10

RATIO FORMULA

MINERAL RESOURCES LIMITED

EFFICIENCY

From the above table, it can be seen that increase in asset turnover ratio indicates that the

assets have been used effectively. In year 2018, the asset turnover is nearly 6 percent, in

2017, it is nearly 6 percent, in 2016, it is nearly 1 percent and at last the company strived to

increase its efficiency and it reached to 10 percent (Macquarie Group, 2017). The assets

turnover of company has been down and reveals that company has lower down its income

due to the reduction in its operating revenue.

LIQUIDITY

a. Current

ratio current assets/ current liabilities 0.89

0.9

4 0.98 1.01

From the table given above, it can be seen that the organisation`s liquidity has been

decreasing year after year. In 2016, the ratio was nearly 1 percent, which does not represent

great liquidity as the standard ratio for the liquidity is 2:1. In 2017, the ratio was .98, which is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

again lower as compared to 2016. In 2016, it again fell down to .94, which is much lower as

compared to standard ratio. Overall, it can be summed up that the organisation`s liquidity has

been getting worse (Macquarie Group, 2017). Company has increased its liquidity by

increasing its investment in its current assets.

PROFITABILITY

a. gross profit

margin

(gross profit/ total revenue)

* 100

100.00

%

100.00

%

100.00

%

100.00

%

c. return on equity

net income/ shareholder's

equity

231.75

%

294.72

%

223.99

%

194.24

%

d. return on assets

ratio net income/ total assets 1.47% 13.36% 1.21% 1.05%

From the table given above, it can be seen that the company obtains 100-percentage gross

profit as the COGS (cost of goods sold is zero). This shows that this ratio is not very much

relevant. It is important to note that this net income does not include any taxation but still the

organisation has been generating greater profits for the shareholders (Macquarie Group,

2018). It has also increased its purchasing cost by reducing its business efficiency in

managing the capital. Company has kept the downfall return on assets throughout the year

which reflects that it has faced downfall in it overall profitability (Macquarie Group, 2018).

a. debt ratio total debt/ total assets 0.33 0.37 0.38 0.44

b. debt to equity

ratio total debt/ total owner's equity) 51.66 6.33 69.82 81.32

compared to standard ratio. Overall, it can be summed up that the organisation`s liquidity has

been getting worse (Macquarie Group, 2017). Company has increased its liquidity by

increasing its investment in its current assets.

PROFITABILITY

a. gross profit

margin

(gross profit/ total revenue)

* 100

100.00

%

100.00

%

100.00

%

100.00

%

c. return on equity

net income/ shareholder's

equity

231.75

%

294.72

%

223.99

%

194.24

%

d. return on assets

ratio net income/ total assets 1.47% 13.36% 1.21% 1.05%

From the table given above, it can be seen that the company obtains 100-percentage gross

profit as the COGS (cost of goods sold is zero). This shows that this ratio is not very much

relevant. It is important to note that this net income does not include any taxation but still the

organisation has been generating greater profits for the shareholders (Macquarie Group,

2018). It has also increased its purchasing cost by reducing its business efficiency in

managing the capital. Company has kept the downfall return on assets throughout the year

which reflects that it has faced downfall in it overall profitability (Macquarie Group, 2018).

a. debt ratio total debt/ total assets 0.33 0.37 0.38 0.44

b. debt to equity

ratio total debt/ total owner's equity) 51.66 6.33 69.82 81.32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the given table, it is seen that the organisation does not have appropriate debt return as

it generates good sum of return nearly 30 to 40 percent in 2016-2019 (Macquarie Group,

2018).

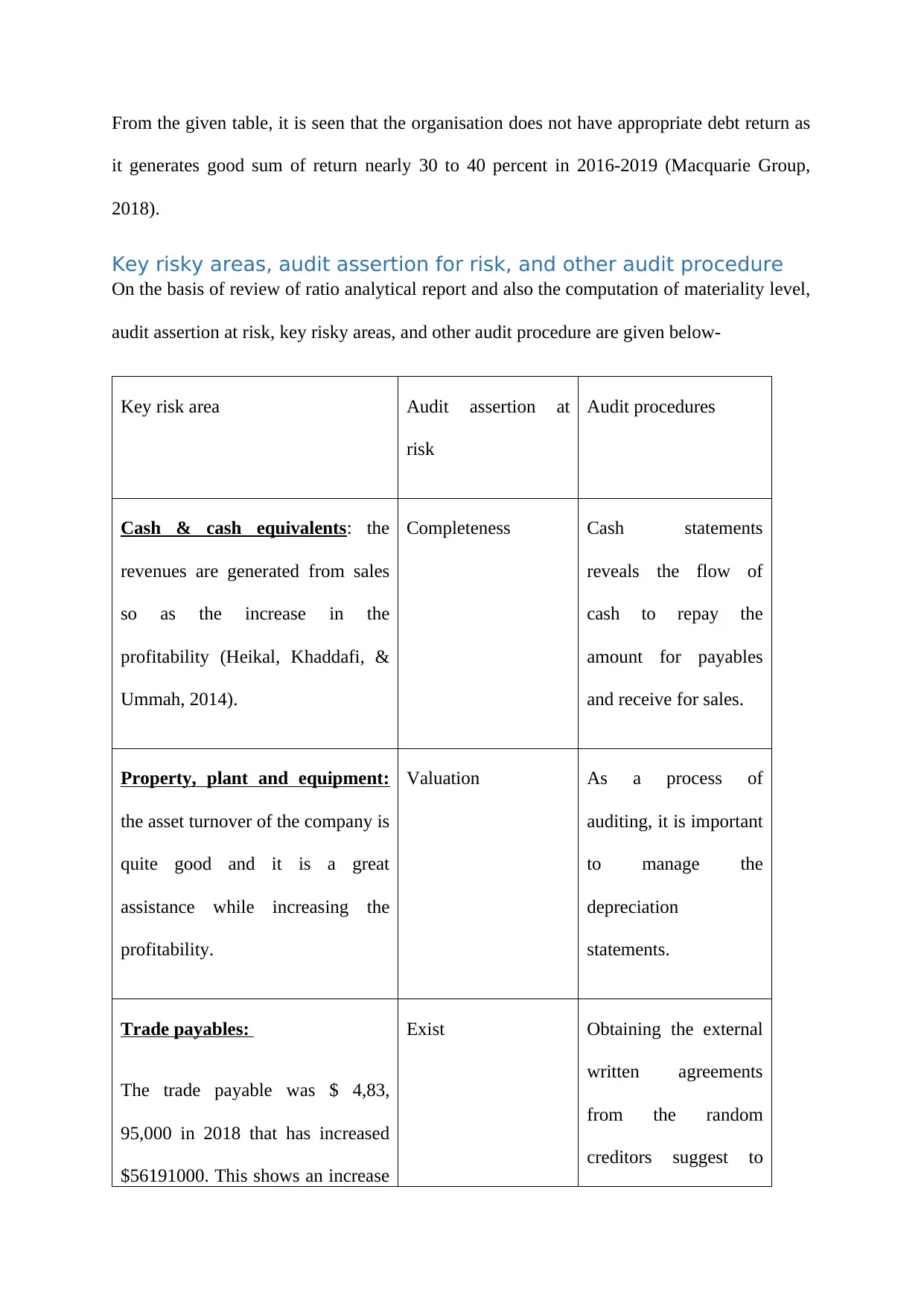

Key risky areas, audit assertion for risk, and other audit procedure

On the basis of review of ratio analytical report and also the computation of materiality level,

audit assertion at risk, key risky areas, and other audit procedure are given below-

Key risk area Audit assertion at

risk

Audit procedures

Cash & cash equivalents: the

revenues are generated from sales

so as the increase in the

profitability (Heikal, Khaddafi, &

Ummah, 2014).

Completeness Cash statements

reveals the flow of

cash to repay the

amount for payables

and receive for sales.

Property, plant and equipment:

the asset turnover of the company is

quite good and it is a great

assistance while increasing the

profitability.

Valuation As a process of

auditing, it is important

to manage the

depreciation

statements.

Trade payables:

The trade payable was $ 4,83,

95,000 in 2018 that has increased

$56191000. This shows an increase

Exist Obtaining the external

written agreements

from the random

creditors suggest to

it generates good sum of return nearly 30 to 40 percent in 2016-2019 (Macquarie Group,

2018).

Key risky areas, audit assertion for risk, and other audit procedure

On the basis of review of ratio analytical report and also the computation of materiality level,

audit assertion at risk, key risky areas, and other audit procedure are given below-

Key risk area Audit assertion at

risk

Audit procedures

Cash & cash equivalents: the

revenues are generated from sales

so as the increase in the

profitability (Heikal, Khaddafi, &

Ummah, 2014).

Completeness Cash statements

reveals the flow of

cash to repay the

amount for payables

and receive for sales.

Property, plant and equipment:

the asset turnover of the company is

quite good and it is a great

assistance while increasing the

profitability.

Valuation As a process of

auditing, it is important

to manage the

depreciation

statements.

Trade payables:

The trade payable was $ 4,83,

95,000 in 2018 that has increased

$56191000. This shows an increase

Exist Obtaining the external

written agreements

from the random

creditors suggest to

in creditor`s ratio Noreen, Brewer,

& Garrison, 2014).

balance that has been

asked for the

organisation (Ruhnke,

Pronobis, & Michel,

2018).

However, this audit risk could also be measured by using the audit model which reveals the

inherent risk, detention risk and control risk in the business process (Macquarie Group,

2018).

Sec-3

Cash flow statements

Majority of the cash flows- $12823000 in 2016 was the maximum cash from operations

generated. This shows that company has strengthen its business operation and having high

cash inflow from its operation activities.

Majority of cash outlets- $3,133,000 in 2017 as the investment in the investing activities are

reported more. The majority of the cash outlet is identified from the investing activities

which reflects that company has invested high amount of cash in its investing activities

(Macquarie Group, 2018).

Crucial cash receipts-

Interest receivables

Investment disposable

Disposing of plant, equipment, and property

Cash payments-

& Garrison, 2014).

balance that has been

asked for the

organisation (Ruhnke,

Pronobis, & Michel,

2018).

However, this audit risk could also be measured by using the audit model which reveals the

inherent risk, detention risk and control risk in the business process (Macquarie Group,

2018).

Sec-3

Cash flow statements

Majority of the cash flows- $12823000 in 2016 was the maximum cash from operations

generated. This shows that company has strengthen its business operation and having high

cash inflow from its operation activities.

Majority of cash outlets- $3,133,000 in 2017 as the investment in the investing activities are

reported more. The majority of the cash outlet is identified from the investing activities

which reflects that company has invested high amount of cash in its investing activities

(Macquarie Group, 2018).

Crucial cash receipts-

Interest receivables

Investment disposable

Disposing of plant, equipment, and property

Cash payments-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Payment to account payables- It is the amount which need to be paid by company to its credit

suppliers. However, it has increased by 20% since last three years (Macquarie Group, 2018).

Payment to the income tax department- It is the amount of tax which needs to be paid by the

company to the government (Macquarie Group, 2018).

Payment to the employees- It is the amount of money which is paid by company to its

employees. However, it has increased by 27% since last three years.

Purchasing of investment- It is related to the investment made by company to increase its

return on capital employed.

Borrowings repayment – It helps company to lower down its cost of capital but at the same

time it increases its business costing.

Type of audit opinion

The audit of this group is carried out by. The opinions laid down in regards to the financial

statements remain unmodified. A succinct reflection of the audit reporting has been presented

fair and true in regards to the financial statements of the company (Eilifsen, Hamilton, &

Messier Jr, 2017). The audit opinion is based on the set structure and developed audit risk

model which reflects that company has faced inherent, detention and control risk in its

recorded financial statements. However, as per the auditor opinion, company has complied

with the all the applicable accounting standards and maintained non-qualified audit report for

its financial statements (Macquarie Group, 2018). The audit opinion reveals that company has

less volatility in its business process and having high sustainability in the recorded business

process. This reveals that company has maintained high transparency in its books of account

and kept the true and fair view of the recorded assets. Nonetheless, company has faced issue

in complying with the IAS 138 due to the high impairment loss in its business process.

Additional information for the key audit matters

suppliers. However, it has increased by 20% since last three years (Macquarie Group, 2018).

Payment to the income tax department- It is the amount of tax which needs to be paid by the

company to the government (Macquarie Group, 2018).

Payment to the employees- It is the amount of money which is paid by company to its

employees. However, it has increased by 27% since last three years.

Purchasing of investment- It is related to the investment made by company to increase its

return on capital employed.

Borrowings repayment – It helps company to lower down its cost of capital but at the same

time it increases its business costing.

Type of audit opinion

The audit of this group is carried out by. The opinions laid down in regards to the financial

statements remain unmodified. A succinct reflection of the audit reporting has been presented

fair and true in regards to the financial statements of the company (Eilifsen, Hamilton, &

Messier Jr, 2017). The audit opinion is based on the set structure and developed audit risk

model which reflects that company has faced inherent, detention and control risk in its

recorded financial statements. However, as per the auditor opinion, company has complied

with the all the applicable accounting standards and maintained non-qualified audit report for

its financial statements (Macquarie Group, 2018). The audit opinion reveals that company has

less volatility in its business process and having high sustainability in the recorded business

process. This reveals that company has maintained high transparency in its books of account

and kept the true and fair view of the recorded assets. Nonetheless, company has faced issue

in complying with the IAS 138 due to the high impairment loss in its business process.

Additional information for the key audit matters

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The auditors often include an additional paragraph as seen in the audit reports identified that

the auditors laid down its rights in their independent report for the auditors. There were some

issues, which was identified by the auditors during the audit such as per the requirement and

judgement of the auditors. It is seen that no separate opinion has been expressed for them

(Eilifsen, Hamilton, & Messier Jr, 2017). The issues are-

Exploration expenditure- greater is the volume of the judgement in relation to impairment

indicators, recoverable accounts, amortisation charges, and the impairment risk which can

make the account as the key audit matter with significant audit (Eilifsen, Hamilton, &

Messier Jr, 2017).

Sit rehabilitation- it has been seen that a significant judgement, complexity, uncertainty of the

estimations, and high-attached materiality has created the account for the audit matters

(Eilifsen, Hamilton, & Messier Jr, 2017).

Conclusion

This report has concluded that auditors have fairly conducted their process with

extreme authenticity. The auditors have also included additional set of information when

auditing the financial statements of the Macquarie Group. The matching concept shows the

reconciling of the cash statements in order to monitor the authenticity of the sales

transactions. At the end, it can be said that the organisation has stable risk for audit and it is

sustainable in the end.

the auditors laid down its rights in their independent report for the auditors. There were some

issues, which was identified by the auditors during the audit such as per the requirement and

judgement of the auditors. It is seen that no separate opinion has been expressed for them

(Eilifsen, Hamilton, & Messier Jr, 2017). The issues are-

Exploration expenditure- greater is the volume of the judgement in relation to impairment

indicators, recoverable accounts, amortisation charges, and the impairment risk which can

make the account as the key audit matter with significant audit (Eilifsen, Hamilton, &

Messier Jr, 2017).

Sit rehabilitation- it has been seen that a significant judgement, complexity, uncertainty of the

estimations, and high-attached materiality has created the account for the audit matters

(Eilifsen, Hamilton, & Messier Jr, 2017).

Conclusion

This report has concluded that auditors have fairly conducted their process with

extreme authenticity. The auditors have also included additional set of information when

auditing the financial statements of the Macquarie Group. The matching concept shows the

reconciling of the cash statements in order to monitor the authenticity of the sales

transactions. At the end, it can be said that the organisation has stable risk for audit and it is

sustainable in the end.

References

Barman, A. N., & Sengupta, P. P. (2017). DETERMINANTS OF PROFITABILITY IN

INDIAN TELECOM INDUSTRY USING FINANCIAL RATIO

ANALYSIS. International Journal of Research in Management & Social Science, 25.

Eilifsen, A., Hamilton, E. L., & Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis

Disclosures on Investors’ Judgments and Decisions. 4(12), 101.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lakis, V., & Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR

USERS OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Macquarie Group, (2016). Annual report, 2016. Retrieved from:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/

results/2016/Macquarie-Group-FY16-Annual-Report.pdf?v=2

Macquarie Group, (2017). Annual report, 2017. Retrieved from:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/

results/2017/Macquarie-Group-FY17-Annual-Report.pdf?v=2

Barman, A. N., & Sengupta, P. P. (2017). DETERMINANTS OF PROFITABILITY IN

INDIAN TELECOM INDUSTRY USING FINANCIAL RATIO

ANALYSIS. International Journal of Research in Management & Social Science, 25.

Eilifsen, A., Hamilton, E. L., & Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis

Disclosures on Investors’ Judgments and Decisions. 4(12), 101.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lakis, V., & Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR

USERS OF FINANCIAL STATEMENTS. Journal of Management, 2(31).

Macquarie Group, (2016). Annual report, 2016. Retrieved from:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/

results/2016/Macquarie-Group-FY16-Annual-Report.pdf?v=2

Macquarie Group, (2017). Annual report, 2017. Retrieved from:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/

results/2017/Macquarie-Group-FY17-Annual-Report.pdf?v=2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.