CQUniversity ACCT20075 Auditing and Ethics Report: Assessment 2

VerifiedAdded on 2022/12/22

|18

|3032

|74

Report

AI Summary

This report, prepared for ACCT20075 Auditing and Ethics at CQUniversity, analyzes the financial statements of Boral Ltd for the year 2018. It begins by defining and assessing materiality, including quantitative and qualitative factors, and calculating planning materiality based on Boral Ltd's financial data. The report then examines significant audit items such as contingencies (bank guarantees) and provisions, outlining the necessary audit procedures for each. Furthermore, it conducts a preliminary analytical review, including key ratio computations (liquidity, leverage, and profitability ratios) to assess Boral's financial performance. The report also discusses audit procedures for cash and long-term loans and borrowings. The overall objective is to develop critical analysis skills in relation to materiality, analytical review, audit procedures and forming an opinion.

Running head: ACCT20075 AUDITING AND ETHICS

ACCT20075 auditing and ethics

Name of the student

Name of the university

Student ID

Author note

ACCT20075 auditing and ethics

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCT20075 AUDITING AND ETHICIS

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Level of materiality......................................................................................................................2

Items significant to audit.............................................................................................................4

Section 2..........................................................................................................................................6

Preliminary analytical review......................................................................................................6

Key ratio computation of Boral Ltd.............................................................................................7

Section 3........................................................................................................................................10

Cash flow statement...................................................................................................................10

Audit report................................................................................................................................10

Reference.......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Level of materiality......................................................................................................................2

Items significant to audit.............................................................................................................4

Section 2..........................................................................................................................................6

Preliminary analytical review......................................................................................................6

Key ratio computation of Boral Ltd.............................................................................................7

Section 3........................................................................................................................................10

Cash flow statement...................................................................................................................10

Audit report................................................................................................................................10

Reference.......................................................................................................................................12

2ACCT20075 AUDITING AND ETHICIS

Introduction

Audit materiality is considered as one of the major concepts for the auditors.

Misstatement that includes omissions are considered to be material if it is individually or in

aggregation are expected to persuade the user’s economic decision taken on the basis of financial

statements. However, the term materiality includes both qualitative and quantitative aspects

(Byrnes et al., 2015). On the other side, the procedure of analytical review is considered as one

of the procedure for substantive audit procedure. It is used for determining whether the

correlation among the financial data for determining whether the information provided in

financial statements are correct. The concept of analytical review presumes that the financial

relationships are stable over the period to period (Ruhnke, Pronobis & Michel, 2014)

Section 1

Level of materiality

AUS 202 – the objective and the general principles governs the audit of financial

statements. Primary objective of audit of the financial report is enabling them to express the

opinion concerning whether financial report in all material aspects has been prepared as per the

framework of identified financial reporting (Auasb.gov.au, 2019). The auditor shall consider the

materiality at the time of determining the timing, nature and the extent of the audit procedure and

analysing the impact of misstatement. A relationship is there between the level of the audit risk

and materiality that signifies that with higher risk material level becomes lower. Hence, in such

scenario the auditor considers this association between materiality and audit risk while

determining the extent, timing and nature of the audit procedure (Auasb.gov.au, 2019).

Introduction

Audit materiality is considered as one of the major concepts for the auditors.

Misstatement that includes omissions are considered to be material if it is individually or in

aggregation are expected to persuade the user’s economic decision taken on the basis of financial

statements. However, the term materiality includes both qualitative and quantitative aspects

(Byrnes et al., 2015). On the other side, the procedure of analytical review is considered as one

of the procedure for substantive audit procedure. It is used for determining whether the

correlation among the financial data for determining whether the information provided in

financial statements are correct. The concept of analytical review presumes that the financial

relationships are stable over the period to period (Ruhnke, Pronobis & Michel, 2014)

Section 1

Level of materiality

AUS 202 – the objective and the general principles governs the audit of financial

statements. Primary objective of audit of the financial report is enabling them to express the

opinion concerning whether financial report in all material aspects has been prepared as per the

framework of identified financial reporting (Auasb.gov.au, 2019). The auditor shall consider the

materiality at the time of determining the timing, nature and the extent of the audit procedure and

analysing the impact of misstatement. A relationship is there between the level of the audit risk

and materiality that signifies that with higher risk material level becomes lower. Hence, in such

scenario the auditor considers this association between materiality and audit risk while

determining the extent, timing and nature of the audit procedure (Auasb.gov.au, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCT20075 AUDITING AND ETHICIS

Preliminary estimate for the purpose of materiality at the financial statement level is

generally called as the planning materiality. It level is the optimum value by which auditors

believes that they statements could be misstated by the unknown or the known fraud or error and

still that will not have impact on the decisions taken by users of financial statements (Arens et

al., 2016). While establishing the preliminary assessment for the materiality, auditor shall take

into consideration the reliability of the management information, qualitative factors and any

other factors that may indicate the deviation from the normal activities. Generally, the materiality

is computed on the basis of following –

0.5% to 1% of the gross revenue

1% to 2% of the total assets

2% to 5% of the shareholder’s equity

5% to 10% of the net profit (Auasb.gov.au, 2019).

Considering the annual report of Boral Ltd for the year ended 2018, the materiality will

be computed as follows –

Basis Amount Materiality

Lowest Highest

0.5% to 1% of the gross revenue 5731.10 28.66 57.31

1% to 2% of the total assets 9510.30 95.10 190.21

2% to 5% of the shareholder’s equity 5730.80 114.62 286.54

5% to 10% of the net profit 441.00 22.05 44.10

From the above table the highest amount that is $ 286.54 million will be considered as

the benchmark of planning materiality. Maximum amount by which the material misstatement

can be tolerable is presumed to be 50% to 75% of the amount of material misstatement. Hence,

the level of tolerable misstatement will be assumed as $ 286.54 * 75% = $ 215 million

Preliminary estimate for the purpose of materiality at the financial statement level is

generally called as the planning materiality. It level is the optimum value by which auditors

believes that they statements could be misstated by the unknown or the known fraud or error and

still that will not have impact on the decisions taken by users of financial statements (Arens et

al., 2016). While establishing the preliminary assessment for the materiality, auditor shall take

into consideration the reliability of the management information, qualitative factors and any

other factors that may indicate the deviation from the normal activities. Generally, the materiality

is computed on the basis of following –

0.5% to 1% of the gross revenue

1% to 2% of the total assets

2% to 5% of the shareholder’s equity

5% to 10% of the net profit (Auasb.gov.au, 2019).

Considering the annual report of Boral Ltd for the year ended 2018, the materiality will

be computed as follows –

Basis Amount Materiality

Lowest Highest

0.5% to 1% of the gross revenue 5731.10 28.66 57.31

1% to 2% of the total assets 9510.30 95.10 190.21

2% to 5% of the shareholder’s equity 5730.80 114.62 286.54

5% to 10% of the net profit 441.00 22.05 44.10

From the above table the highest amount that is $ 286.54 million will be considered as

the benchmark of planning materiality. Maximum amount by which the material misstatement

can be tolerable is presumed to be 50% to 75% of the amount of material misstatement. Hence,

the level of tolerable misstatement will be assumed as $ 286.54 * 75% = $ 215 million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCT20075 AUDITING AND ETHICIS

approximately (Auasb.gov.au, 2019). This level is quite higher that signifies lower level of audit

risk and is selected based on the analysis of financial report of Boral Ltd for the year closed on

2018. As per the auditor’s report provided regarding the financial statements of the company, the

entity’s financial statements are providing true and fair view regarding its financial position as

well as the financial performances (Boral.com, 2019).

Items significant to audit

Analysing the annual report of Boral Ltd for the year closed on 2018 following items are

considered to have significance to audit –

Contingencies – Boral Ltd disclosed the contingent liabilities for the items for which probability

of future payments and receipts are not considered as remote. One such item is bank guarantee.

In case of this item the entity provided the bankers with letter of responsibility with regard to

accommodation delivered over the time by the banks to the controlled entities (Christensen,

Glover & Wood, 2013). Though the amount involved with this contingencies is lower that is $

38.3 million, as it required estimates and judgments, is considered to be significant item for the

purpose of audit. Audit procedures required for contingencies are as follows –

Evaluating the likelihood of the event – the auditor is required estimating the likelihood

of the fact that the event vent will take place. Likelihood can be reasonably possible,

probable or remote. Further, the auditor shall verify whether proper footnotes has been

provided by the company regarding contingent liabilities that is probable or reasonably

possible (Titera, 2013)

Looking at the probable events – auditors shall concentrate on the contingent liabilities

under the probable category as they are required to be treated specially as per accounting.

approximately (Auasb.gov.au, 2019). This level is quite higher that signifies lower level of audit

risk and is selected based on the analysis of financial report of Boral Ltd for the year closed on

2018. As per the auditor’s report provided regarding the financial statements of the company, the

entity’s financial statements are providing true and fair view regarding its financial position as

well as the financial performances (Boral.com, 2019).

Items significant to audit

Analysing the annual report of Boral Ltd for the year closed on 2018 following items are

considered to have significance to audit –

Contingencies – Boral Ltd disclosed the contingent liabilities for the items for which probability

of future payments and receipts are not considered as remote. One such item is bank guarantee.

In case of this item the entity provided the bankers with letter of responsibility with regard to

accommodation delivered over the time by the banks to the controlled entities (Christensen,

Glover & Wood, 2013). Though the amount involved with this contingencies is lower that is $

38.3 million, as it required estimates and judgments, is considered to be significant item for the

purpose of audit. Audit procedures required for contingencies are as follows –

Evaluating the likelihood of the event – the auditor is required estimating the likelihood

of the fact that the event vent will take place. Likelihood can be reasonably possible,

probable or remote. Further, the auditor shall verify whether proper footnotes has been

provided by the company regarding contingent liabilities that is probable or reasonably

possible (Titera, 2013)

Looking at the probable events – auditors shall concentrate on the contingent liabilities

under the probable category as they are required to be treated specially as per accounting.

5ACCT20075 AUDITING AND ETHICIS

If contingent liability is probable, however the amount cannot be estimated liability for

such item shall be disclosed trough disclosures and it requires no further action.

However, for the liabilities those can be estimated and are probable, requires specific

journal entry. In such case the auditor shall assure that the entity debited the same amount

and credited the liability account for any of the measurable and probable contingent

liability (Eilifsen & Messier, 2014)

Provisions – Boral Ltd recognizes the provision under the balance sheet if it has the present

obligation owing to any past event, reliable estimated can be made for the amount of obligation

and it is apparent that the outflow of economic benefits will be needed for settlement of the

obligation (Boral.com, 2019). Significant estimates, assumptions and judgments required by

Boral Ltd for recognising provision is regarding the future costs related to restructuring and

expected time period, likelihood for settling the insurance and customers claims and assessment

for profitability of the contracts. As recognition of provision requires higher level of estimates,

assumptions and judgments this item is regarded as significant for the audit (Coetzee & Lubbe,

2014). Audit procedures required for provisions are as follows –

Provisions made for all the contingencies and liabilities

The auditor must assure that the amount provided as provision is adequate

Auditor shall examine minutes of the meeting of board of directors regarding the required

provisions

It shall be verified that all the provisions are made through debiting profit and loss

statement

Auditor shall further verify that all provisions are disclosed properly under the financial

statements (Glover & Prawitt, 2014)

If contingent liability is probable, however the amount cannot be estimated liability for

such item shall be disclosed trough disclosures and it requires no further action.

However, for the liabilities those can be estimated and are probable, requires specific

journal entry. In such case the auditor shall assure that the entity debited the same amount

and credited the liability account for any of the measurable and probable contingent

liability (Eilifsen & Messier, 2014)

Provisions – Boral Ltd recognizes the provision under the balance sheet if it has the present

obligation owing to any past event, reliable estimated can be made for the amount of obligation

and it is apparent that the outflow of economic benefits will be needed for settlement of the

obligation (Boral.com, 2019). Significant estimates, assumptions and judgments required by

Boral Ltd for recognising provision is regarding the future costs related to restructuring and

expected time period, likelihood for settling the insurance and customers claims and assessment

for profitability of the contracts. As recognition of provision requires higher level of estimates,

assumptions and judgments this item is regarded as significant for the audit (Coetzee & Lubbe,

2014). Audit procedures required for provisions are as follows –

Provisions made for all the contingencies and liabilities

The auditor must assure that the amount provided as provision is adequate

Auditor shall examine minutes of the meeting of board of directors regarding the required

provisions

It shall be verified that all the provisions are made through debiting profit and loss

statement

Auditor shall further verify that all provisions are disclosed properly under the financial

statements (Glover & Prawitt, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCT20075 AUDITING AND ETHICIS

Section 2

Preliminary analytical review

Preliminary analytical review is performed for obtaining the understanding of business

and business environment. It helps in assessing risks of the material assessment for determining

the extent, timing and nature of audit. It is defined as both the analytical procedure and the

procedures of management inquiry that is applied under the audit’s planning stage. It is an

important part of audit procedure and consists of the analysis of the financial information that is

made by the study of reasonable relationship among non financial and financial data. Analytical

procedure can be carried out through different methods and one if such method is ratio analysis

(Wali, 2015).

Section 2

Preliminary analytical review

Preliminary analytical review is performed for obtaining the understanding of business

and business environment. It helps in assessing risks of the material assessment for determining

the extent, timing and nature of audit. It is defined as both the analytical procedure and the

procedures of management inquiry that is applied under the audit’s planning stage. It is an

important part of audit procedure and consists of the analysis of the financial information that is

made by the study of reasonable relationship among non financial and financial data. Analytical

procedure can be carried out through different methods and one if such method is ratio analysis

(Wali, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCT20075 AUDITING AND ETHICIS

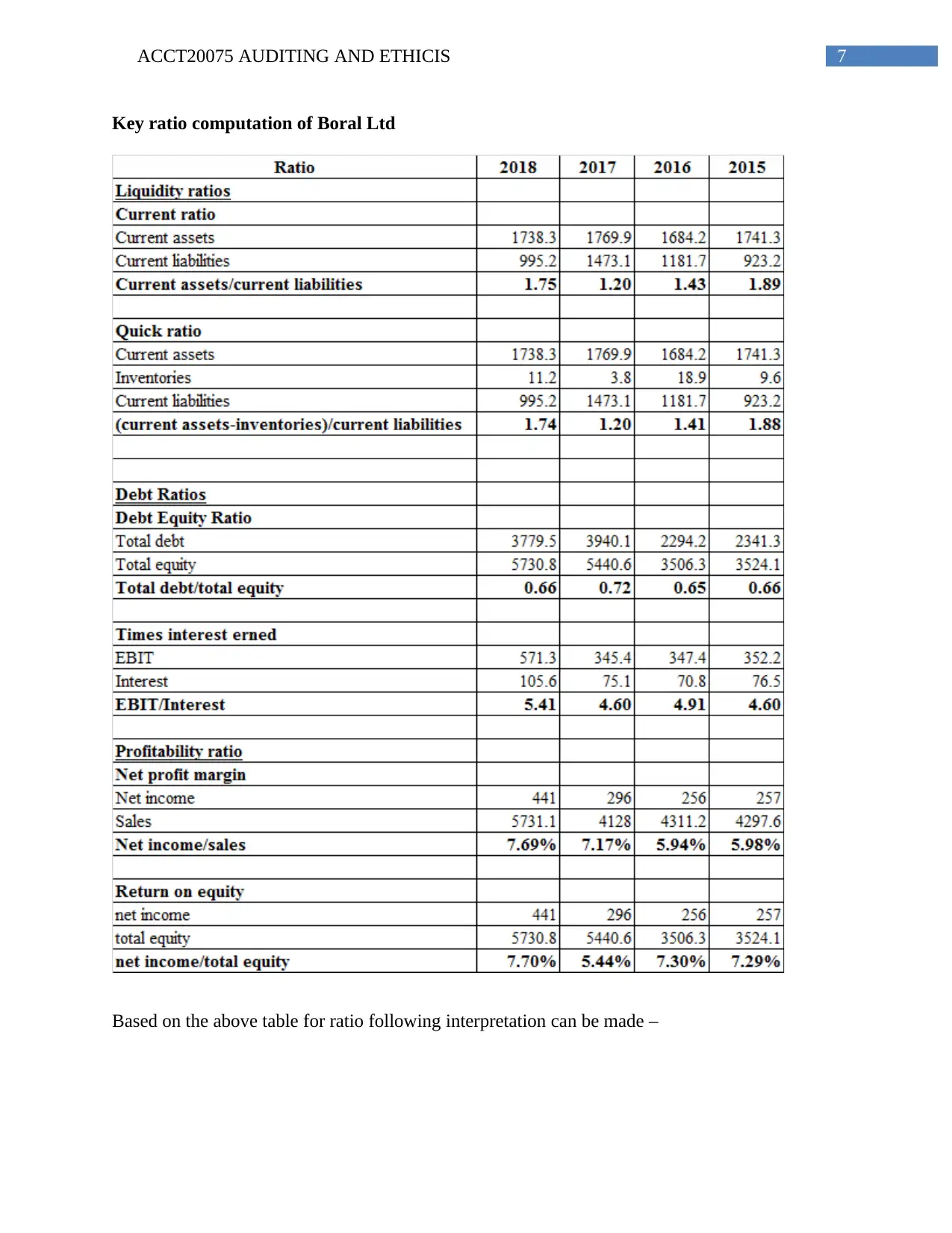

Key ratio computation of Boral Ltd

Based on the above table for ratio following interpretation can be made –

Key ratio computation of Boral Ltd

Based on the above table for ratio following interpretation can be made –

8ACCT20075 AUDITING AND ETHICIS

Liquidity ratio – it signifies the ability of the entity for meeting its short term obligation with the

available current assets. 2 widely used ratios for measuring the liquidity position of the entity

are current ratio and quick ratio. Analysing the current ratio that measures the current assets

against the current liabilities is signifying that the current ratio of the entity till 2017 was in

reducing trend and reduced to 1.20 times from 1.89 times in 2015 (Boral.com, 2019). However,

the entity was able to enhance its liquidity position in 2018 and the same is increased to 1.75

times. Analysing the quick ratio that does not consider the assets those are not readility

convertible into cash till 2017 was in reducing trend and reduced to 1.20 times from 1.88 times

in 2015. However, the entity was able to enhance its liquidity position in 2018 and the current

ratio is increased to 1.74 times in 2018 (Boral.com, 2019).

Leverage ratio – it signifies the leverage position of the entity that is the proportion of capital

structure financed through debt and financed through equity. Higher debt indicates that the entity

is highly leveraged and is exposed to interest risk. Analysing the debt ratio of Boral Ltd it can be

identified that the debt ratio of the entity till 2017 was in upward trend and increased to 0.72

from 0.66 in 2015 (Boral.com, 2019). However, the entity was able to enhance its leverage

position in 2018 and the same is reduced to 0.66 in 2018. If the times interest earned is

considered it can be identified that the ability of the company to meet its interest expenses is

reduced over the years from 2016 to 2017, however, it is enhanced to 5.41 times by the end of

the year 2018 (Boral.com, 2019).

Profitability ratio – it reveals the ability of the entity to earn profits from the revenues earned by

it which in turn will enable it to provide return to the shareholders on their holding. Analysing

the profitability position of the entity it can be acknowledged that the net profit margin of the

company that represents the company’s earning capability are in increasing trend and reached to

Liquidity ratio – it signifies the ability of the entity for meeting its short term obligation with the

available current assets. 2 widely used ratios for measuring the liquidity position of the entity

are current ratio and quick ratio. Analysing the current ratio that measures the current assets

against the current liabilities is signifying that the current ratio of the entity till 2017 was in

reducing trend and reduced to 1.20 times from 1.89 times in 2015 (Boral.com, 2019). However,

the entity was able to enhance its liquidity position in 2018 and the same is increased to 1.75

times. Analysing the quick ratio that does not consider the assets those are not readility

convertible into cash till 2017 was in reducing trend and reduced to 1.20 times from 1.88 times

in 2015. However, the entity was able to enhance its liquidity position in 2018 and the current

ratio is increased to 1.74 times in 2018 (Boral.com, 2019).

Leverage ratio – it signifies the leverage position of the entity that is the proportion of capital

structure financed through debt and financed through equity. Higher debt indicates that the entity

is highly leveraged and is exposed to interest risk. Analysing the debt ratio of Boral Ltd it can be

identified that the debt ratio of the entity till 2017 was in upward trend and increased to 0.72

from 0.66 in 2015 (Boral.com, 2019). However, the entity was able to enhance its leverage

position in 2018 and the same is reduced to 0.66 in 2018. If the times interest earned is

considered it can be identified that the ability of the company to meet its interest expenses is

reduced over the years from 2016 to 2017, however, it is enhanced to 5.41 times by the end of

the year 2018 (Boral.com, 2019).

Profitability ratio – it reveals the ability of the entity to earn profits from the revenues earned by

it which in turn will enable it to provide return to the shareholders on their holding. Analysing

the profitability position of the entity it can be acknowledged that the net profit margin of the

company that represents the company’s earning capability are in increasing trend and reached to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCT20075 AUDITING AND ETHICIS

7.69% in 2018 from 5.98% in 2015 (Boral.com, 2019). Return on equity tat signifies the ability

of the company to generate earnings through deploying the shareholder’s investment is in

enhancing trend and increased to 7.70% in 2018 from 7.29% in 2015 (Boral.com, 2019).

Considering the overall financial performance of the entity over the period from 2015 to

2019 some of the areas those are required to be reviewed analytically are as follows –

Cash – irrespective of the amount involved cash is considered as a material item b y its

nature. Key assertions involved with cash are – (i) completeness that is the risk that all

the cash related transactions has not been considered while preparing the accounts (ii)

existence that is the cash balance shown in the accounts is actually in existence on the

date on balance sheet. Audit procedure to be followed for cash is reconciling the cash

balance with the bank for the major cash transactions (Kharisova & Kozlova 2014)

Long term loans and borrowings – as it is the major item under liabilities it shall be

verified with special attention. Key assertions involved with cash are – (i) existence that

is the loans and borrowings shown in the accounts is the actual balance in existence on

the date on balance sheet (Leung et al., 2014) (ii) cut – off that is only the loans and

borrowings which are associated with the current period are recorded that is the loans

which are already repaid has not been included. Audit procedure to be followed for loans

and borrowings is to verify all the loans related documents with details of amount

borrowed, purpose of borrowings, whether authorisation taken for the same, rate of

interest, repayment schedule and lending institution (Legoria, Melendrez & Reynolds

2013)

7.69% in 2018 from 5.98% in 2015 (Boral.com, 2019). Return on equity tat signifies the ability

of the company to generate earnings through deploying the shareholder’s investment is in

enhancing trend and increased to 7.70% in 2018 from 7.29% in 2015 (Boral.com, 2019).

Considering the overall financial performance of the entity over the period from 2015 to

2019 some of the areas those are required to be reviewed analytically are as follows –

Cash – irrespective of the amount involved cash is considered as a material item b y its

nature. Key assertions involved with cash are – (i) completeness that is the risk that all

the cash related transactions has not been considered while preparing the accounts (ii)

existence that is the cash balance shown in the accounts is actually in existence on the

date on balance sheet. Audit procedure to be followed for cash is reconciling the cash

balance with the bank for the major cash transactions (Kharisova & Kozlova 2014)

Long term loans and borrowings – as it is the major item under liabilities it shall be

verified with special attention. Key assertions involved with cash are – (i) existence that

is the loans and borrowings shown in the accounts is the actual balance in existence on

the date on balance sheet (Leung et al., 2014) (ii) cut – off that is only the loans and

borrowings which are associated with the current period are recorded that is the loans

which are already repaid has not been included. Audit procedure to be followed for loans

and borrowings is to verify all the loans related documents with details of amount

borrowed, purpose of borrowings, whether authorisation taken for the same, rate of

interest, repayment schedule and lending institution (Legoria, Melendrez & Reynolds

2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCT20075 AUDITING AND ETHICIS

Section 3

Cash flow statement

Cash flow from operations amounting to $ 578 million provided majority of the cash

inflows

Cash used by the financing activities amounting to $ 398.2 million had greatest outflows

Receipts from customers amounting to $ 6209 million were primary cash receipts and

payment to the suppliers and the employees amounting to $ 5399.1 was primary cash

payments during the year (Boral.com, 2019).

Non-cash financing and investing activity is Effects of exchange rate fluctuations on the

balances of cash and cash equivalents held in foreign currencies

From the cash flow statement it is identified that the cash provided by financing activities

was $ 3107 million that is reduced to $ - 344.6 million in 2018. Further, the reduction in

cash and cash equivalent from 237.8 million to 74.3 million is indicating the going

concern issue for the entity (Boral.com, 2019). The auditor procedure to be followed for

this is to verify the previous year’s receipts with this year’s particularly the source from

where the receipts have been significantly reduced in this year. Reasons of major

variation shall be asked to the management (Louwers et al., 2015).

Audit report

Auditor expressed unmodified opinion for the financial statements of the year with

mentioning some of the key audit matters as follows –

Carrying value of the North America goodwill regarding discount rate, calculation of

terminal value and growth rate for forecast

Section 3

Cash flow statement

Cash flow from operations amounting to $ 578 million provided majority of the cash

inflows

Cash used by the financing activities amounting to $ 398.2 million had greatest outflows

Receipts from customers amounting to $ 6209 million were primary cash receipts and

payment to the suppliers and the employees amounting to $ 5399.1 was primary cash

payments during the year (Boral.com, 2019).

Non-cash financing and investing activity is Effects of exchange rate fluctuations on the

balances of cash and cash equivalents held in foreign currencies

From the cash flow statement it is identified that the cash provided by financing activities

was $ 3107 million that is reduced to $ - 344.6 million in 2018. Further, the reduction in

cash and cash equivalent from 237.8 million to 74.3 million is indicating the going

concern issue for the entity (Boral.com, 2019). The auditor procedure to be followed for

this is to verify the previous year’s receipts with this year’s particularly the source from

where the receipts have been significantly reduced in this year. Reasons of major

variation shall be asked to the management (Louwers et al., 2015).

Audit report

Auditor expressed unmodified opinion for the financial statements of the year with

mentioning some of the key audit matters as follows –

Carrying value of the North America goodwill regarding discount rate, calculation of

terminal value and growth rate for forecast

11ACCT20075 AUDITING AND ETHICIS

Recoverability and availability of the US tax loss assets

Carrying value of investment in the USG Boral JV and Meridian bank JV

Accounting for purchase price allocation related to acquisition of Headwaters owing to

the pervasive impact of acquisition (Boral.com, 2019).

Recoverability and availability of the US tax loss assets

Carrying value of investment in the USG Boral JV and Meridian bank JV

Accounting for purchase price allocation related to acquisition of Headwaters owing to

the pervasive impact of acquisition (Boral.com, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.