ACCT20077: Cash Flow Analysis of Harvey Norman and JB HiFi

VerifiedAdded on 2020/02/18

|11

|2834

|48

Report

AI Summary

This report provides a comprehensive analysis of the cash flow statements of Harvey Norman Holdings and JB HiFi for the year 2016. The analysis includes an examination of the methods used by each company to prepare their cash flow statements, specifically focusing on the direct method employed by both. The report delves into the operating, investing, and financing activities of each company, highlighting key cash flows and trends. Furthermore, it calculates and interprets several financial ratios, including working capital ratio, cash flow adequacy ratio, debt to total asset ratio, debt coverage ratio, and cash flow to sales ratio, to assess the financial health and performance of both companies. The findings are supported by data extracted from the annual reports of the respective companies. The report concludes with recommendations based on the financial analysis, offering insights into the companies' cash management and overall financial positions.

ACCT20077: Practical and written assessment

Page 1 of 12

Page 1 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Part 1: Method used by each company for preparing the cash flow statements........................3

Part 2: Analysis of the cash flow statements of both the companies.........................................4

Comment on the cash flow statement of the Harvey Norman Holding Limited....................4

Working Capital Ratio............................................................................................................5

Cash Flow Adequacy Ratio....................................................................................................5

Debt to Total Asset Ratio.......................................................................................................6

Debt Coverage Ratio..............................................................................................................6

Cash Flow to Sales Ratio........................................................................................................7

Comment on the cash flow statement of the JB HiFi.............................................................7

Cash Flow Adequacy Ratio....................................................................................................8

Debt to Total Asset Ratio.......................................................................................................9

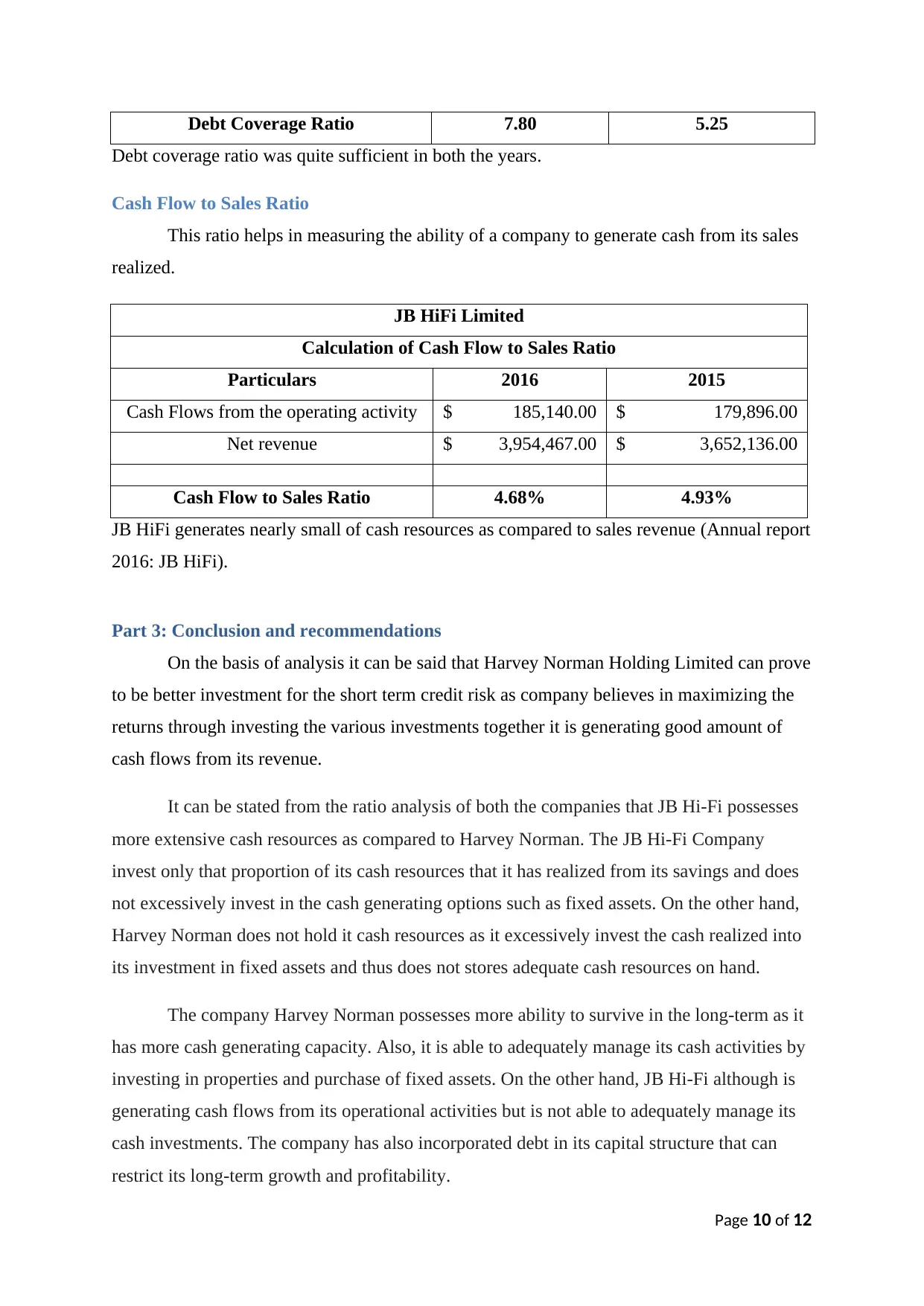

Debt Coverage Ratio..............................................................................................................9

Cash Flow to Sales Ratio......................................................................................................10

Part 3: Conclusion and recommendations................................................................................10

References................................................................................................................................12

Page 2 of 12

Introduction................................................................................................................................3

Part 1: Method used by each company for preparing the cash flow statements........................3

Part 2: Analysis of the cash flow statements of both the companies.........................................4

Comment on the cash flow statement of the Harvey Norman Holding Limited....................4

Working Capital Ratio............................................................................................................5

Cash Flow Adequacy Ratio....................................................................................................5

Debt to Total Asset Ratio.......................................................................................................6

Debt Coverage Ratio..............................................................................................................6

Cash Flow to Sales Ratio........................................................................................................7

Comment on the cash flow statement of the JB HiFi.............................................................7

Cash Flow Adequacy Ratio....................................................................................................8

Debt to Total Asset Ratio.......................................................................................................9

Debt Coverage Ratio..............................................................................................................9

Cash Flow to Sales Ratio......................................................................................................10

Part 3: Conclusion and recommendations................................................................................10

References................................................................................................................................12

Page 2 of 12

Introduction

Financial statements are the most important of the annual report and users of the

annual report uses financial statements to predict the financial performance of the company.

The financial statements are mainly divided into four main parts namely, statement of

comprehensive income, statement of financial position, statement of change in equity and

statement of cash flows. Among them statement of cash flow the most important as it helps

in providing the actual cash flows take place in the company through the operating activity,

investing activity and financing activity.

In this report, cash flow statements of Harvey Norman Holdings and JB Hi Fi for year

2016 are analyzed to report on the cash position of the company. Financial ratios are also

calculated to support the findings.

Part 1: Method used by each company for preparing the cash flow statements

There are two methods to prepare the statement of cash flows, namely direct method

and indirect method. Mainly there is difference for preparing the cash flow from operating

activity. Cash flow from investing activity and financing are calculated in the similar manner

under both the options.

It has been analyzed from the annual report of the Harvey Norman Holdings that

company has implied direct method to prepare the statement of cash flows. The statement of

cash flows in annual report of Harvey Norman Holding Limited is presented on the page 65

and reconciliation of profit after income tax to net operating cash flows has been incorporated

in the notes to account in section 28 (b) on page 112 (Annual report 2016: Harvey Norman

Holding Limited). Under direct method for preparing the cash flow statement, it is important

to disclose the reconciliation statement under notes to accounts in order to facilitate the better

understanding of cash flows under the operating activity. On looking at the annual report of

the JB HiFi for the year 2016 it has been noted that this has also used direct method to

prepare the cash flow statement. The reconciliation of profit after income tax to net operating

cash flows has been incorporated in notes to accounts at note number 14 (Annual report

2016: JB HiFi).

Page 3 of 12

Financial statements are the most important of the annual report and users of the

annual report uses financial statements to predict the financial performance of the company.

The financial statements are mainly divided into four main parts namely, statement of

comprehensive income, statement of financial position, statement of change in equity and

statement of cash flows. Among them statement of cash flow the most important as it helps

in providing the actual cash flows take place in the company through the operating activity,

investing activity and financing activity.

In this report, cash flow statements of Harvey Norman Holdings and JB Hi Fi for year

2016 are analyzed to report on the cash position of the company. Financial ratios are also

calculated to support the findings.

Part 1: Method used by each company for preparing the cash flow statements

There are two methods to prepare the statement of cash flows, namely direct method

and indirect method. Mainly there is difference for preparing the cash flow from operating

activity. Cash flow from investing activity and financing are calculated in the similar manner

under both the options.

It has been analyzed from the annual report of the Harvey Norman Holdings that

company has implied direct method to prepare the statement of cash flows. The statement of

cash flows in annual report of Harvey Norman Holding Limited is presented on the page 65

and reconciliation of profit after income tax to net operating cash flows has been incorporated

in the notes to account in section 28 (b) on page 112 (Annual report 2016: Harvey Norman

Holding Limited). Under direct method for preparing the cash flow statement, it is important

to disclose the reconciliation statement under notes to accounts in order to facilitate the better

understanding of cash flows under the operating activity. On looking at the annual report of

the JB HiFi for the year 2016 it has been noted that this has also used direct method to

prepare the cash flow statement. The reconciliation of profit after income tax to net operating

cash flows has been incorporated in notes to accounts at note number 14 (Annual report

2016: JB HiFi).

Page 3 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

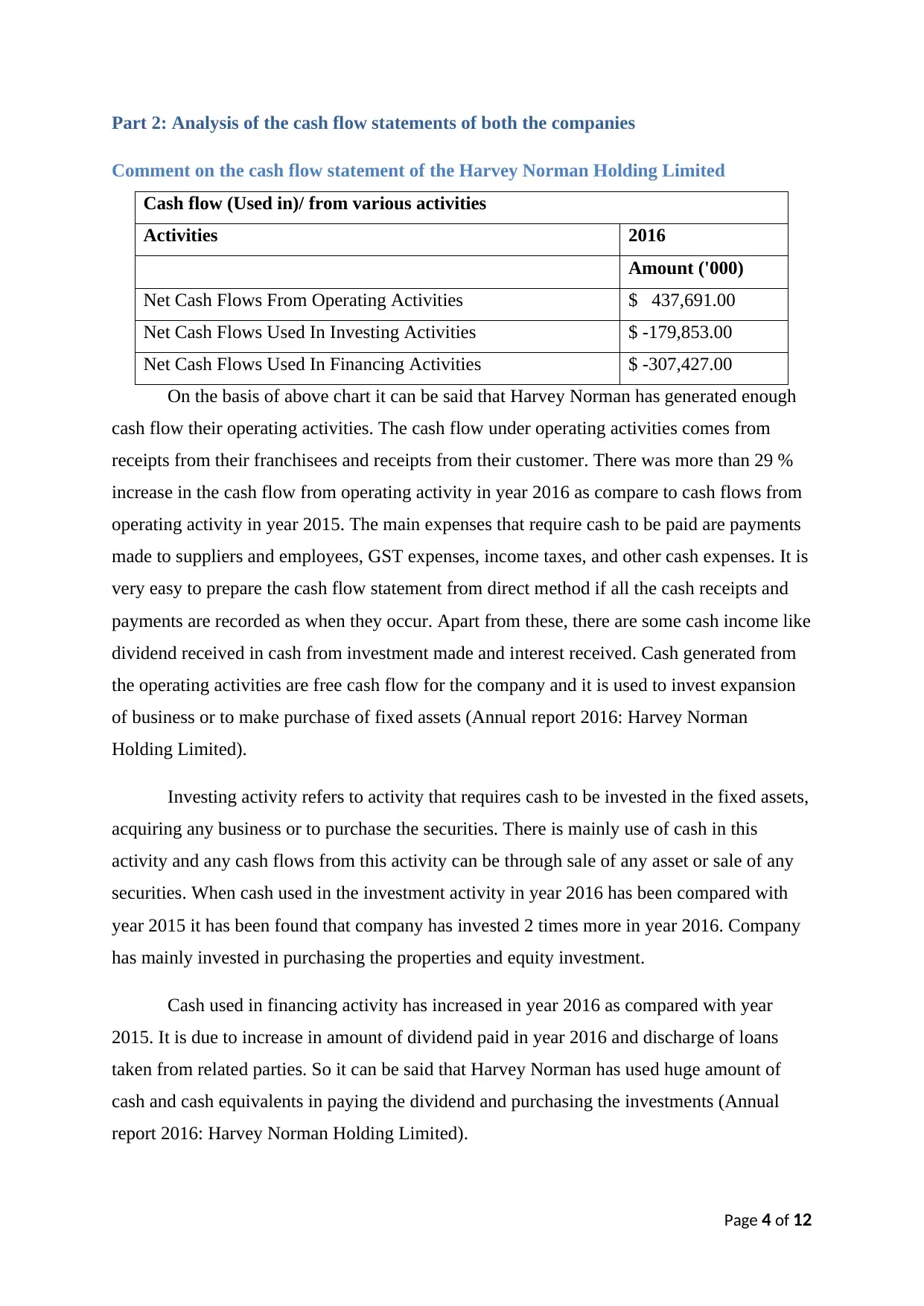

Part 2: Analysis of the cash flow statements of both the companies

Comment on the cash flow statement of the Harvey Norman Holding Limited

Cash flow (Used in)/ from various activities

Activities 2016

Amount ('000)

Net Cash Flows From Operating Activities $ 437,691.00

Net Cash Flows Used In Investing Activities $ -179,853.00

Net Cash Flows Used In Financing Activities $ -307,427.00

On the basis of above chart it can be said that Harvey Norman has generated enough

cash flow their operating activities. The cash flow under operating activities comes from

receipts from their franchisees and receipts from their customer. There was more than 29 %

increase in the cash flow from operating activity in year 2016 as compare to cash flows from

operating activity in year 2015. The main expenses that require cash to be paid are payments

made to suppliers and employees, GST expenses, income taxes, and other cash expenses. It is

very easy to prepare the cash flow statement from direct method if all the cash receipts and

payments are recorded as when they occur. Apart from these, there are some cash income like

dividend received in cash from investment made and interest received. Cash generated from

the operating activities are free cash flow for the company and it is used to invest expansion

of business or to make purchase of fixed assets (Annual report 2016: Harvey Norman

Holding Limited).

Investing activity refers to activity that requires cash to be invested in the fixed assets,

acquiring any business or to purchase the securities. There is mainly use of cash in this

activity and any cash flows from this activity can be through sale of any asset or sale of any

securities. When cash used in the investment activity in year 2016 has been compared with

year 2015 it has been found that company has invested 2 times more in year 2016. Company

has mainly invested in purchasing the properties and equity investment.

Cash used in financing activity has increased in year 2016 as compared with year

2015. It is due to increase in amount of dividend paid in year 2016 and discharge of loans

taken from related parties. So it can be said that Harvey Norman has used huge amount of

cash and cash equivalents in paying the dividend and purchasing the investments (Annual

report 2016: Harvey Norman Holding Limited).

Page 4 of 12

Comment on the cash flow statement of the Harvey Norman Holding Limited

Cash flow (Used in)/ from various activities

Activities 2016

Amount ('000)

Net Cash Flows From Operating Activities $ 437,691.00

Net Cash Flows Used In Investing Activities $ -179,853.00

Net Cash Flows Used In Financing Activities $ -307,427.00

On the basis of above chart it can be said that Harvey Norman has generated enough

cash flow their operating activities. The cash flow under operating activities comes from

receipts from their franchisees and receipts from their customer. There was more than 29 %

increase in the cash flow from operating activity in year 2016 as compare to cash flows from

operating activity in year 2015. The main expenses that require cash to be paid are payments

made to suppliers and employees, GST expenses, income taxes, and other cash expenses. It is

very easy to prepare the cash flow statement from direct method if all the cash receipts and

payments are recorded as when they occur. Apart from these, there are some cash income like

dividend received in cash from investment made and interest received. Cash generated from

the operating activities are free cash flow for the company and it is used to invest expansion

of business or to make purchase of fixed assets (Annual report 2016: Harvey Norman

Holding Limited).

Investing activity refers to activity that requires cash to be invested in the fixed assets,

acquiring any business or to purchase the securities. There is mainly use of cash in this

activity and any cash flows from this activity can be through sale of any asset or sale of any

securities. When cash used in the investment activity in year 2016 has been compared with

year 2015 it has been found that company has invested 2 times more in year 2016. Company

has mainly invested in purchasing the properties and equity investment.

Cash used in financing activity has increased in year 2016 as compared with year

2015. It is due to increase in amount of dividend paid in year 2016 and discharge of loans

taken from related parties. So it can be said that Harvey Norman has used huge amount of

cash and cash equivalents in paying the dividend and purchasing the investments (Annual

report 2016: Harvey Norman Holding Limited).

Page 4 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

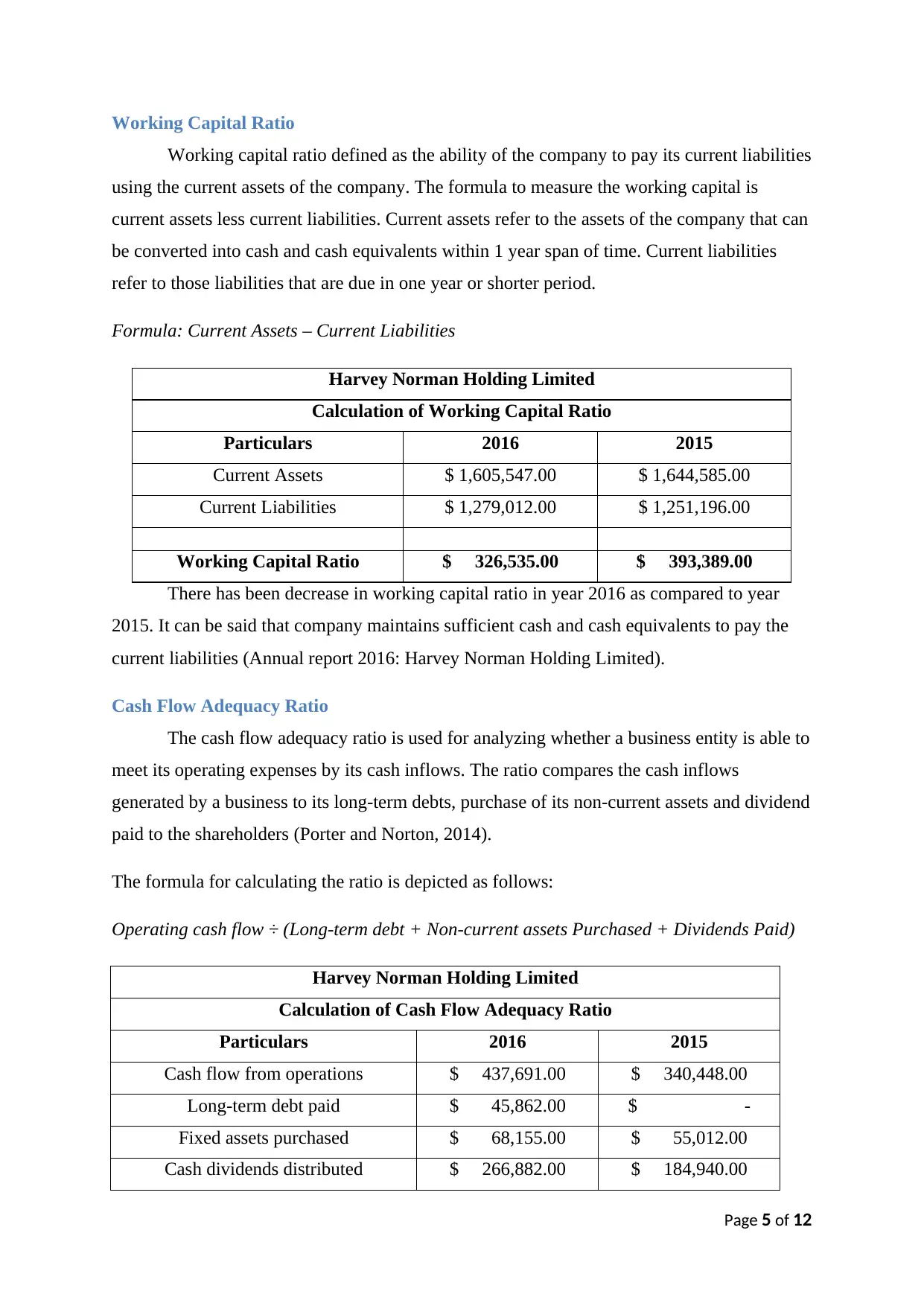

Working Capital Ratio

Working capital ratio defined as the ability of the company to pay its current liabilities

using the current assets of the company. The formula to measure the working capital is

current assets less current liabilities. Current assets refer to the assets of the company that can

be converted into cash and cash equivalents within 1 year span of time. Current liabilities

refer to those liabilities that are due in one year or shorter period.

Formula: Current Assets – Current Liabilities

Harvey Norman Holding Limited

Calculation of Working Capital Ratio

Particulars 2016 2015

Current Assets $ 1,605,547.00 $ 1,644,585.00

Current Liabilities $ 1,279,012.00 $ 1,251,196.00

Working Capital Ratio $ 326,535.00 $ 393,389.00

There has been decrease in working capital ratio in year 2016 as compared to year

2015. It can be said that company maintains sufficient cash and cash equivalents to pay the

current liabilities (Annual report 2016: Harvey Norman Holding Limited).

Cash Flow Adequacy Ratio

The cash flow adequacy ratio is used for analyzing whether a business entity is able to

meet its operating expenses by its cash inflows. The ratio compares the cash inflows

generated by a business to its long-term debts, purchase of its non-current assets and dividend

paid to the shareholders (Porter and Norton, 2014).

The formula for calculating the ratio is depicted as follows:

Operating cash flow ÷ (Long-term debt + Non-current assets Purchased + Dividends Paid)

Harvey Norman Holding Limited

Calculation of Cash Flow Adequacy Ratio

Particulars 2016 2015

Cash flow from operations $ 437,691.00 $ 340,448.00

Long-term debt paid $ 45,862.00 $ -

Fixed assets purchased $ 68,155.00 $ 55,012.00

Cash dividends distributed $ 266,882.00 $ 184,940.00

Page 5 of 12

Working capital ratio defined as the ability of the company to pay its current liabilities

using the current assets of the company. The formula to measure the working capital is

current assets less current liabilities. Current assets refer to the assets of the company that can

be converted into cash and cash equivalents within 1 year span of time. Current liabilities

refer to those liabilities that are due in one year or shorter period.

Formula: Current Assets – Current Liabilities

Harvey Norman Holding Limited

Calculation of Working Capital Ratio

Particulars 2016 2015

Current Assets $ 1,605,547.00 $ 1,644,585.00

Current Liabilities $ 1,279,012.00 $ 1,251,196.00

Working Capital Ratio $ 326,535.00 $ 393,389.00

There has been decrease in working capital ratio in year 2016 as compared to year

2015. It can be said that company maintains sufficient cash and cash equivalents to pay the

current liabilities (Annual report 2016: Harvey Norman Holding Limited).

Cash Flow Adequacy Ratio

The cash flow adequacy ratio is used for analyzing whether a business entity is able to

meet its operating expenses by its cash inflows. The ratio compares the cash inflows

generated by a business to its long-term debts, purchase of its non-current assets and dividend

paid to the shareholders (Porter and Norton, 2014).

The formula for calculating the ratio is depicted as follows:

Operating cash flow ÷ (Long-term debt + Non-current assets Purchased + Dividends Paid)

Harvey Norman Holding Limited

Calculation of Cash Flow Adequacy Ratio

Particulars 2016 2015

Cash flow from operations $ 437,691.00 $ 340,448.00

Long-term debt paid $ 45,862.00 $ -

Fixed assets purchased $ 68,155.00 $ 55,012.00

Cash dividends distributed $ 266,882.00 $ 184,940.00

Page 5 of 12

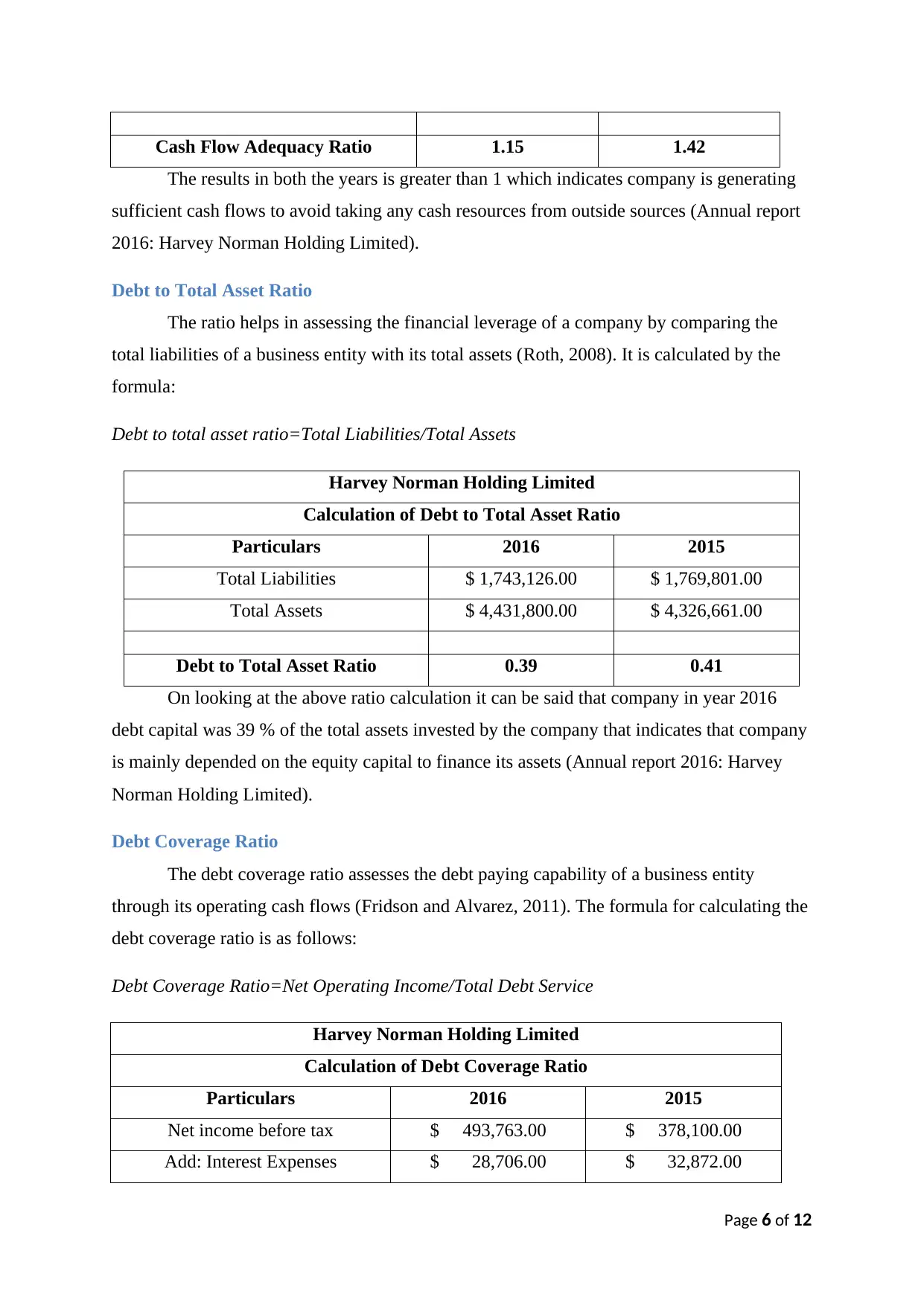

Cash Flow Adequacy Ratio 1.15 1.42

The results in both the years is greater than 1 which indicates company is generating

sufficient cash flows to avoid taking any cash resources from outside sources (Annual report

2016: Harvey Norman Holding Limited).

Debt to Total Asset Ratio

The ratio helps in assessing the financial leverage of a company by comparing the

total liabilities of a business entity with its total assets (Roth, 2008). It is calculated by the

formula:

Debt to total asset ratio=Total Liabilities/Total Assets

Harvey Norman Holding Limited

Calculation of Debt to Total Asset Ratio

Particulars 2016 2015

Total Liabilities $ 1,743,126.00 $ 1,769,801.00

Total Assets $ 4,431,800.00 $ 4,326,661.00

Debt to Total Asset Ratio 0.39 0.41

On looking at the above ratio calculation it can be said that company in year 2016

debt capital was 39 % of the total assets invested by the company that indicates that company

is mainly depended on the equity capital to finance its assets (Annual report 2016: Harvey

Norman Holding Limited).

Debt Coverage Ratio

The debt coverage ratio assesses the debt paying capability of a business entity

through its operating cash flows (Fridson and Alvarez, 2011). The formula for calculating the

debt coverage ratio is as follows:

Debt Coverage Ratio=Net Operating Income/Total Debt Service

Harvey Norman Holding Limited

Calculation of Debt Coverage Ratio

Particulars 2016 2015

Net income before tax $ 493,763.00 $ 378,100.00

Add: Interest Expenses $ 28,706.00 $ 32,872.00

Page 6 of 12

The results in both the years is greater than 1 which indicates company is generating

sufficient cash flows to avoid taking any cash resources from outside sources (Annual report

2016: Harvey Norman Holding Limited).

Debt to Total Asset Ratio

The ratio helps in assessing the financial leverage of a company by comparing the

total liabilities of a business entity with its total assets (Roth, 2008). It is calculated by the

formula:

Debt to total asset ratio=Total Liabilities/Total Assets

Harvey Norman Holding Limited

Calculation of Debt to Total Asset Ratio

Particulars 2016 2015

Total Liabilities $ 1,743,126.00 $ 1,769,801.00

Total Assets $ 4,431,800.00 $ 4,326,661.00

Debt to Total Asset Ratio 0.39 0.41

On looking at the above ratio calculation it can be said that company in year 2016

debt capital was 39 % of the total assets invested by the company that indicates that company

is mainly depended on the equity capital to finance its assets (Annual report 2016: Harvey

Norman Holding Limited).

Debt Coverage Ratio

The debt coverage ratio assesses the debt paying capability of a business entity

through its operating cash flows (Fridson and Alvarez, 2011). The formula for calculating the

debt coverage ratio is as follows:

Debt Coverage Ratio=Net Operating Income/Total Debt Service

Harvey Norman Holding Limited

Calculation of Debt Coverage Ratio

Particulars 2016 2015

Net income before tax $ 493,763.00 $ 378,100.00

Add: Interest Expenses $ 28,706.00 $ 32,872.00

Page 6 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

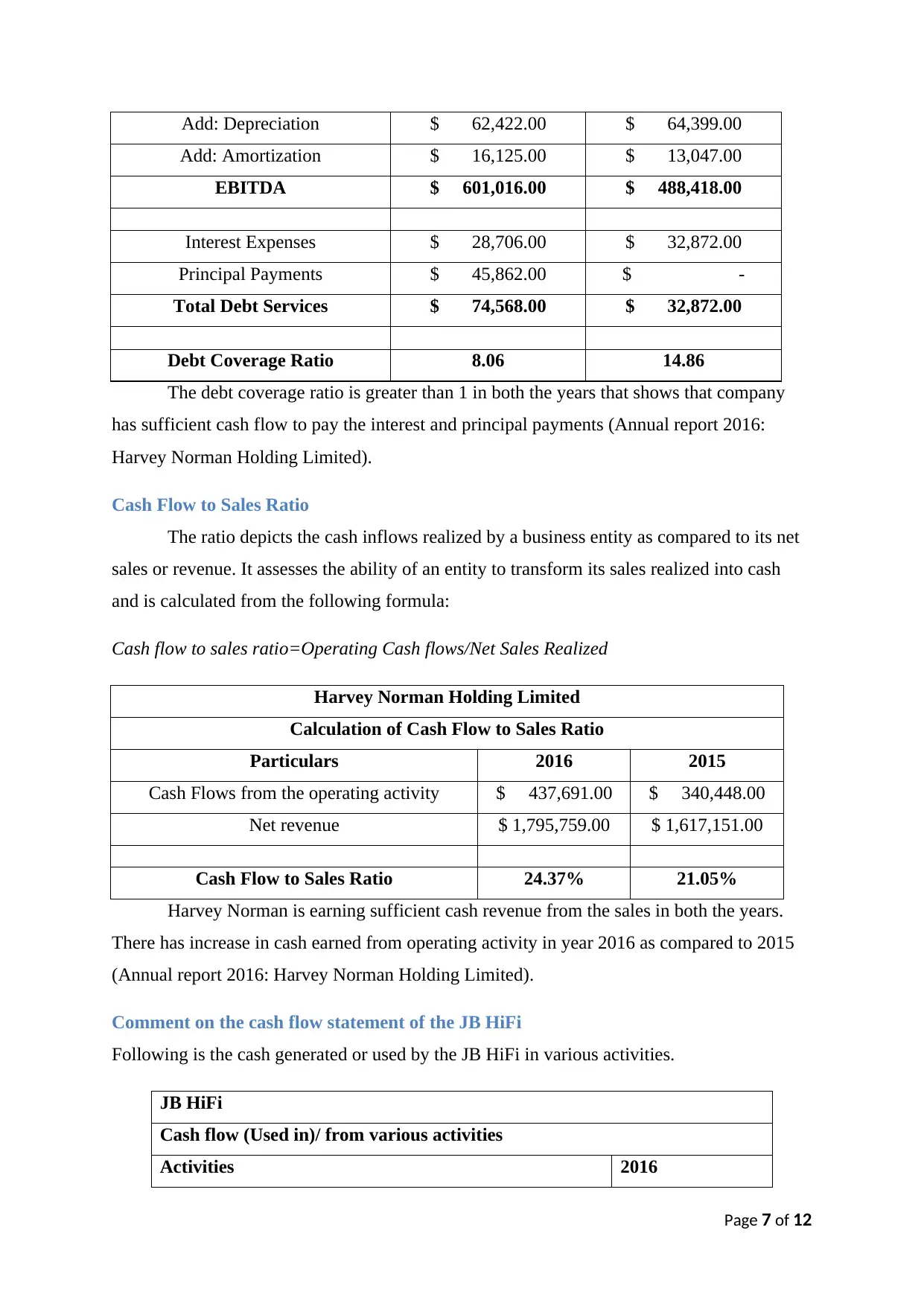

Add: Depreciation $ 62,422.00 $ 64,399.00

Add: Amortization $ 16,125.00 $ 13,047.00

EBITDA $ 601,016.00 $ 488,418.00

Interest Expenses $ 28,706.00 $ 32,872.00

Principal Payments $ 45,862.00 $ -

Total Debt Services $ 74,568.00 $ 32,872.00

Debt Coverage Ratio 8.06 14.86

The debt coverage ratio is greater than 1 in both the years that shows that company

has sufficient cash flow to pay the interest and principal payments (Annual report 2016:

Harvey Norman Holding Limited).

Cash Flow to Sales Ratio

The ratio depicts the cash inflows realized by a business entity as compared to its net

sales or revenue. It assesses the ability of an entity to transform its sales realized into cash

and is calculated from the following formula:

Cash flow to sales ratio=Operating Cash flows/Net Sales Realized

Harvey Norman Holding Limited

Calculation of Cash Flow to Sales Ratio

Particulars 2016 2015

Cash Flows from the operating activity $ 437,691.00 $ 340,448.00

Net revenue $ 1,795,759.00 $ 1,617,151.00

Cash Flow to Sales Ratio 24.37% 21.05%

Harvey Norman is earning sufficient cash revenue from the sales in both the years.

There has increase in cash earned from operating activity in year 2016 as compared to 2015

(Annual report 2016: Harvey Norman Holding Limited).

Comment on the cash flow statement of the JB HiFi

Following is the cash generated or used by the JB HiFi in various activities.

JB HiFi

Cash flow (Used in)/ from various activities

Activities 2016

Page 7 of 12

Add: Amortization $ 16,125.00 $ 13,047.00

EBITDA $ 601,016.00 $ 488,418.00

Interest Expenses $ 28,706.00 $ 32,872.00

Principal Payments $ 45,862.00 $ -

Total Debt Services $ 74,568.00 $ 32,872.00

Debt Coverage Ratio 8.06 14.86

The debt coverage ratio is greater than 1 in both the years that shows that company

has sufficient cash flow to pay the interest and principal payments (Annual report 2016:

Harvey Norman Holding Limited).

Cash Flow to Sales Ratio

The ratio depicts the cash inflows realized by a business entity as compared to its net

sales or revenue. It assesses the ability of an entity to transform its sales realized into cash

and is calculated from the following formula:

Cash flow to sales ratio=Operating Cash flows/Net Sales Realized

Harvey Norman Holding Limited

Calculation of Cash Flow to Sales Ratio

Particulars 2016 2015

Cash Flows from the operating activity $ 437,691.00 $ 340,448.00

Net revenue $ 1,795,759.00 $ 1,617,151.00

Cash Flow to Sales Ratio 24.37% 21.05%

Harvey Norman is earning sufficient cash revenue from the sales in both the years.

There has increase in cash earned from operating activity in year 2016 as compared to 2015

(Annual report 2016: Harvey Norman Holding Limited).

Comment on the cash flow statement of the JB HiFi

Following is the cash generated or used by the JB HiFi in various activities.

JB HiFi

Cash flow (Used in)/ from various activities

Activities 2016

Page 7 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amount ('000)

Net Cash Flows From Operating Activities $ 185,140.00

Net Cash Flows Used In Investing Activities $ -52,001.00

Net Cash Flows Used In Financing Activities $ -130,565.00

JB HiFi receives the cash mainly from the receipts from the customer and its main

expenditure includes payments to the suppliers and employees. Other expenditures that

company has to bear are income taxes and finance cost. JB HiFi has invested $ 52,343,000 in

purchasing the plant and equipments. There was no more expenditure in the financing

activity. In financing activity, it has been seen that JB HiFi has used cash to pay for the

dividend and to repay the borrowings. Some of the cash has also been used to buy back the

equity shares from the open market (Annual report 2016: JB HiFi).

Working Capital Ratio

The ratio depicts the proportion of current assets of a company to its current liabilities

and is calculated with the formula: Working capital ratio=Current assets/Current liabilities

(Fabozzi, 2008).

JB HiFi Limited

Calculation of Working Capital Ratio

Particulars 2016 2015

Current Assets $ 702,518.00 $ 616,901.00

Current Liabilities $ 446,833.00 $ 380,336.00

Working Capital Ratio $ 255,685.00 $ 236,565.00

The results show that JB HiFi has enough working capital in both the years.

Cash Flow Adequacy Ratio

This ratio helps in analyzing the cash sufficiency of a business entity by measuring its

efficiency of meeting its current liabilities with the cash flows generated.

JB HiFi Limited

Calculation of Cash Flow Adequacy Ratio

Particulars 2016 2015

Cash flow from operations $ 185,140.00 $ 179,896.00

Long-term debt paid $ 30,000.00 $ 40,113.00

Page 8 of 12

Net Cash Flows From Operating Activities $ 185,140.00

Net Cash Flows Used In Investing Activities $ -52,001.00

Net Cash Flows Used In Financing Activities $ -130,565.00

JB HiFi receives the cash mainly from the receipts from the customer and its main

expenditure includes payments to the suppliers and employees. Other expenditures that

company has to bear are income taxes and finance cost. JB HiFi has invested $ 52,343,000 in

purchasing the plant and equipments. There was no more expenditure in the financing

activity. In financing activity, it has been seen that JB HiFi has used cash to pay for the

dividend and to repay the borrowings. Some of the cash has also been used to buy back the

equity shares from the open market (Annual report 2016: JB HiFi).

Working Capital Ratio

The ratio depicts the proportion of current assets of a company to its current liabilities

and is calculated with the formula: Working capital ratio=Current assets/Current liabilities

(Fabozzi, 2008).

JB HiFi Limited

Calculation of Working Capital Ratio

Particulars 2016 2015

Current Assets $ 702,518.00 $ 616,901.00

Current Liabilities $ 446,833.00 $ 380,336.00

Working Capital Ratio $ 255,685.00 $ 236,565.00

The results show that JB HiFi has enough working capital in both the years.

Cash Flow Adequacy Ratio

This ratio helps in analyzing the cash sufficiency of a business entity by measuring its

efficiency of meeting its current liabilities with the cash flows generated.

JB HiFi Limited

Calculation of Cash Flow Adequacy Ratio

Particulars 2016 2015

Cash flow from operations $ 185,140.00 $ 179,896.00

Long-term debt paid $ 30,000.00 $ 40,113.00

Page 8 of 12

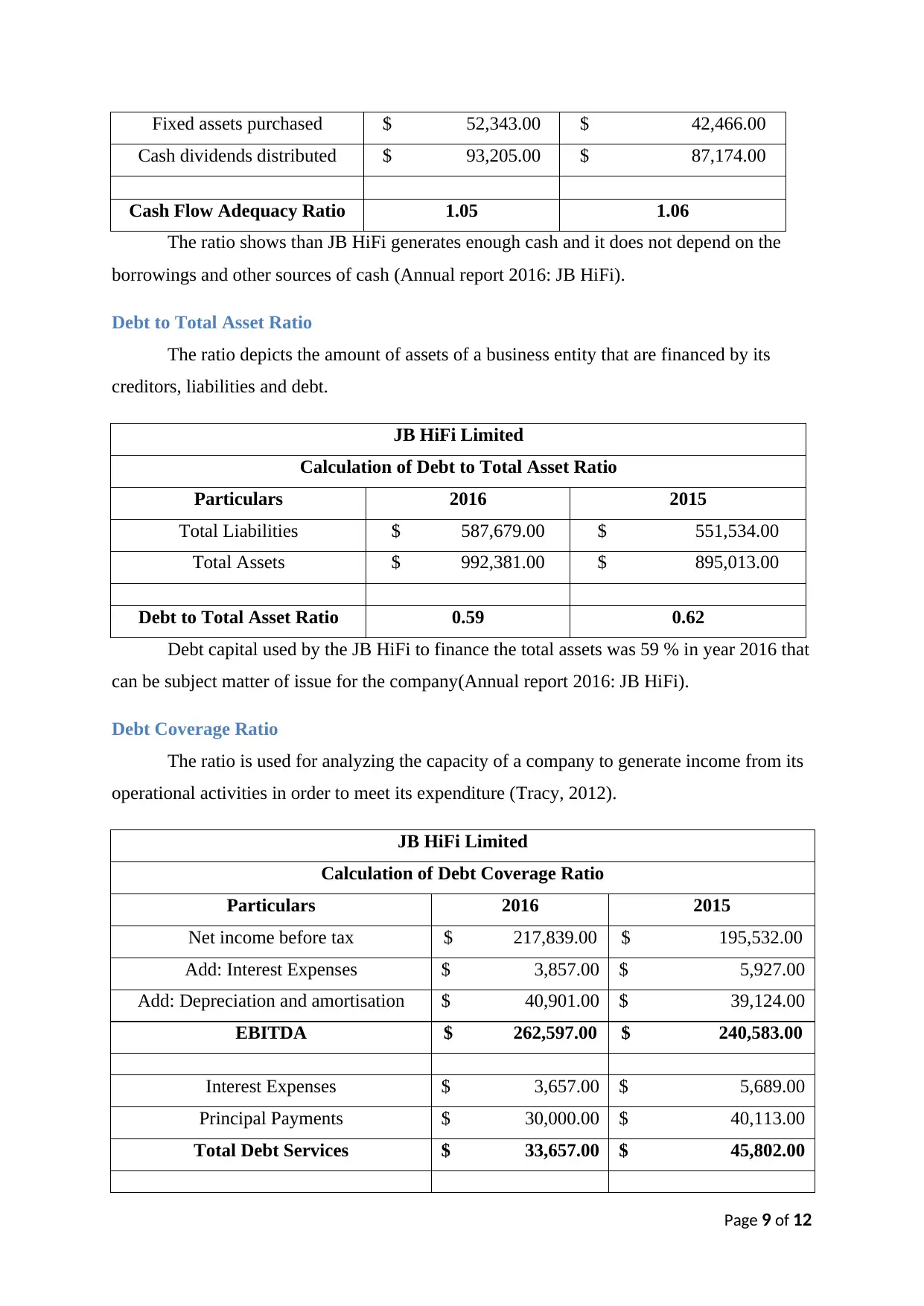

Fixed assets purchased $ 52,343.00 $ 42,466.00

Cash dividends distributed $ 93,205.00 $ 87,174.00

Cash Flow Adequacy Ratio 1.05 1.06

The ratio shows than JB HiFi generates enough cash and it does not depend on the

borrowings and other sources of cash (Annual report 2016: JB HiFi).

Debt to Total Asset Ratio

The ratio depicts the amount of assets of a business entity that are financed by its

creditors, liabilities and debt.

JB HiFi Limited

Calculation of Debt to Total Asset Ratio

Particulars 2016 2015

Total Liabilities $ 587,679.00 $ 551,534.00

Total Assets $ 992,381.00 $ 895,013.00

Debt to Total Asset Ratio 0.59 0.62

Debt capital used by the JB HiFi to finance the total assets was 59 % in year 2016 that

can be subject matter of issue for the company(Annual report 2016: JB HiFi).

Debt Coverage Ratio

The ratio is used for analyzing the capacity of a company to generate income from its

operational activities in order to meet its expenditure (Tracy, 2012).

JB HiFi Limited

Calculation of Debt Coverage Ratio

Particulars 2016 2015

Net income before tax $ 217,839.00 $ 195,532.00

Add: Interest Expenses $ 3,857.00 $ 5,927.00

Add: Depreciation and amortisation $ 40,901.00 $ 39,124.00

EBITDA $ 262,597.00 $ 240,583.00

Interest Expenses $ 3,657.00 $ 5,689.00

Principal Payments $ 30,000.00 $ 40,113.00

Total Debt Services $ 33,657.00 $ 45,802.00

Page 9 of 12

Cash dividends distributed $ 93,205.00 $ 87,174.00

Cash Flow Adequacy Ratio 1.05 1.06

The ratio shows than JB HiFi generates enough cash and it does not depend on the

borrowings and other sources of cash (Annual report 2016: JB HiFi).

Debt to Total Asset Ratio

The ratio depicts the amount of assets of a business entity that are financed by its

creditors, liabilities and debt.

JB HiFi Limited

Calculation of Debt to Total Asset Ratio

Particulars 2016 2015

Total Liabilities $ 587,679.00 $ 551,534.00

Total Assets $ 992,381.00 $ 895,013.00

Debt to Total Asset Ratio 0.59 0.62

Debt capital used by the JB HiFi to finance the total assets was 59 % in year 2016 that

can be subject matter of issue for the company(Annual report 2016: JB HiFi).

Debt Coverage Ratio

The ratio is used for analyzing the capacity of a company to generate income from its

operational activities in order to meet its expenditure (Tracy, 2012).

JB HiFi Limited

Calculation of Debt Coverage Ratio

Particulars 2016 2015

Net income before tax $ 217,839.00 $ 195,532.00

Add: Interest Expenses $ 3,857.00 $ 5,927.00

Add: Depreciation and amortisation $ 40,901.00 $ 39,124.00

EBITDA $ 262,597.00 $ 240,583.00

Interest Expenses $ 3,657.00 $ 5,689.00

Principal Payments $ 30,000.00 $ 40,113.00

Total Debt Services $ 33,657.00 $ 45,802.00

Page 9 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debt Coverage Ratio 7.80 5.25

Debt coverage ratio was quite sufficient in both the years.

Cash Flow to Sales Ratio

This ratio helps in measuring the ability of a company to generate cash from its sales

realized.

JB HiFi Limited

Calculation of Cash Flow to Sales Ratio

Particulars 2016 2015

Cash Flows from the operating activity $ 185,140.00 $ 179,896.00

Net revenue $ 3,954,467.00 $ 3,652,136.00

Cash Flow to Sales Ratio 4.68% 4.93%

JB HiFi generates nearly small of cash resources as compared to sales revenue (Annual report

2016: JB HiFi).

Part 3: Conclusion and recommendations

On the basis of analysis it can be said that Harvey Norman Holding Limited can prove

to be better investment for the short term credit risk as company believes in maximizing the

returns through investing the various investments together it is generating good amount of

cash flows from its revenue.

It can be stated from the ratio analysis of both the companies that JB Hi-Fi possesses

more extensive cash resources as compared to Harvey Norman. The JB Hi-Fi Company

invest only that proportion of its cash resources that it has realized from its savings and does

not excessively invest in the cash generating options such as fixed assets. On the other hand,

Harvey Norman does not hold it cash resources as it excessively invest the cash realized into

its investment in fixed assets and thus does not stores adequate cash resources on hand.

The company Harvey Norman possesses more ability to survive in the long-term as it

has more cash generating capacity. Also, it is able to adequately manage its cash activities by

investing in properties and purchase of fixed assets. On the other hand, JB Hi-Fi although is

generating cash flows from its operational activities but is not able to adequately manage its

cash investments. The company has also incorporated debt in its capital structure that can

restrict its long-term growth and profitability.

Page 10 of 12

Debt coverage ratio was quite sufficient in both the years.

Cash Flow to Sales Ratio

This ratio helps in measuring the ability of a company to generate cash from its sales

realized.

JB HiFi Limited

Calculation of Cash Flow to Sales Ratio

Particulars 2016 2015

Cash Flows from the operating activity $ 185,140.00 $ 179,896.00

Net revenue $ 3,954,467.00 $ 3,652,136.00

Cash Flow to Sales Ratio 4.68% 4.93%

JB HiFi generates nearly small of cash resources as compared to sales revenue (Annual report

2016: JB HiFi).

Part 3: Conclusion and recommendations

On the basis of analysis it can be said that Harvey Norman Holding Limited can prove

to be better investment for the short term credit risk as company believes in maximizing the

returns through investing the various investments together it is generating good amount of

cash flows from its revenue.

It can be stated from the ratio analysis of both the companies that JB Hi-Fi possesses

more extensive cash resources as compared to Harvey Norman. The JB Hi-Fi Company

invest only that proportion of its cash resources that it has realized from its savings and does

not excessively invest in the cash generating options such as fixed assets. On the other hand,

Harvey Norman does not hold it cash resources as it excessively invest the cash realized into

its investment in fixed assets and thus does not stores adequate cash resources on hand.

The company Harvey Norman possesses more ability to survive in the long-term as it

has more cash generating capacity. Also, it is able to adequately manage its cash activities by

investing in properties and purchase of fixed assets. On the other hand, JB Hi-Fi although is

generating cash flows from its operational activities but is not able to adequately manage its

cash investments. The company has also incorporated debt in its capital structure that can

restrict its long-term growth and profitability.

Page 10 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On comparing the cash to sales ratio for both the companies it has been found that

Harvey Norman Holding Limited has generated 24.37 % cash resources from its sales

revenue while JB HiFi has generated only 4.68% cash resources in year 2016. So, it can be

concluded that Harvey Norman is successfully utilising its resources to generate enough cash

from its revenue.

Page 11 of 12

Harvey Norman Holding Limited has generated 24.37 % cash resources from its sales

revenue while JB HiFi has generated only 4.68% cash resources in year 2016. So, it can be

concluded that Harvey Norman is successfully utilising its resources to generate enough cash

from its revenue.

Page 11 of 12

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.