ACCT 2013 Cost Accounting: BlindsforShine Ltd Variance Analysis

VerifiedAdded on 2023/06/03

|9

|2051

|277

Case Study

AI Summary

This case study analyzes the budget and variances for BlindsforShine Ltd, a luxury blinds manufacturer, focusing on November 2018 performance. The analysis identifies variances exceeding 5%, explores potential causes such as market downturns and increased material/labor costs, and recommends corrective measures. Recommendations include innovative product changes, effective advertising, bulk purchasing of raw materials, and employee retention strategies. The report emphasizes the importance of accurate budgeting and monitoring to control expenses and achieve financial targets, ultimately aiming to improve the company's profitability and overall performance. The document provides students with a comprehensive case study solution, and Desklib offers a platform for accessing similar resources and study tools.

Running head: COST ACCOUNTING

Cost Accounting

Name of the Student:

Name of the University:

Author’s Note

Cost Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

COST ACCOUNTING

Executive Summary

The main purpose of this assessment is to analyze the budget which is prepared by the business

for the purpose of analyzing the variances of the business. The budget which is shown in Part B

is to be analyzed for the purpose of identifying the variances which is above 5% level. The

assessment recognizes the potential causes of such variances and also incorporate measures

which can be adopted by the business for the purpose of making improvement in the budgets.

The management of BlindsforShine Ltd can effectively exercise control over the revenue

generating activities of the business and also help the business in maintaining the costs of the

business of the business. On the basis of the variances which is calculated from the budget,

appropriate decisions are taken in order to improve the estimates of the business and ensure that

the business is able to achieve its targets.

COST ACCOUNTING

Executive Summary

The main purpose of this assessment is to analyze the budget which is prepared by the business

for the purpose of analyzing the variances of the business. The budget which is shown in Part B

is to be analyzed for the purpose of identifying the variances which is above 5% level. The

assessment recognizes the potential causes of such variances and also incorporate measures

which can be adopted by the business for the purpose of making improvement in the budgets.

The management of BlindsforShine Ltd can effectively exercise control over the revenue

generating activities of the business and also help the business in maintaining the costs of the

business of the business. On the basis of the variances which is calculated from the budget,

appropriate decisions are taken in order to improve the estimates of the business and ensure that

the business is able to achieve its targets.

2

COST ACCOUNTING

Table of Contents

Part A...............................................................................................................................................3

Budget Report..............................................................................................................................3

Part B...............................................................................................................................................4

Variance Analysis........................................................................................................................4

Recommendation for Variances..................................................................................................5

Reference.........................................................................................................................................8

COST ACCOUNTING

Table of Contents

Part A...............................................................................................................................................3

Budget Report..............................................................................................................................3

Part B...............................................................................................................................................4

Variance Analysis........................................................................................................................4

Recommendation for Variances..................................................................................................5

Reference.........................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

COST ACCOUNTING

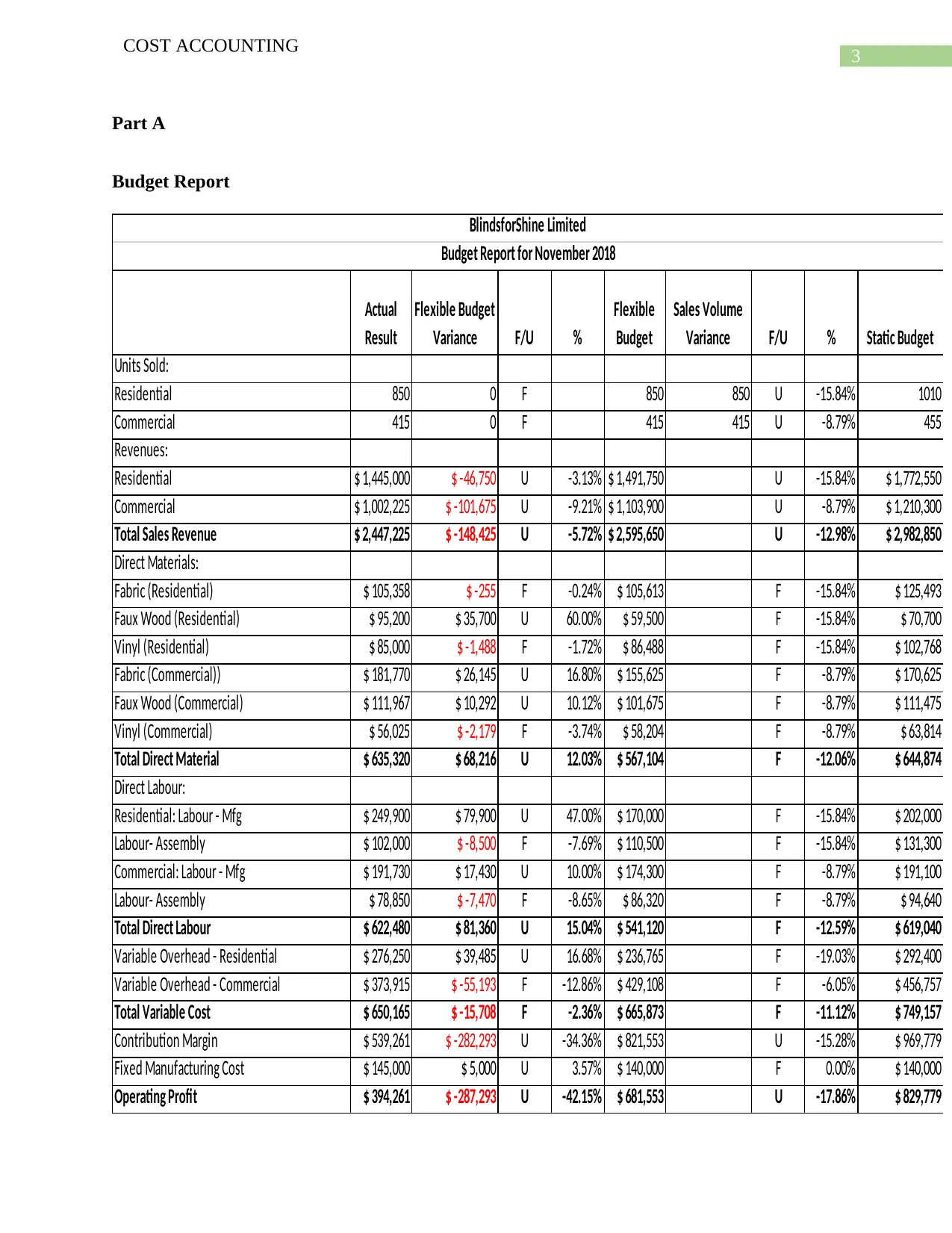

Part A

Budget Report

Actual

Result

Flexible Budget

Variance F/U %

Flexible

Budget

Sales Volume

Variance F/U % Static Budget

Units Sold:

Residential 850 0 F 850 850 U -15.84% 1010

Commercial 415 0 F 415 415 U -8.79% 455

Revenues:

Residential $ 1,445,000 $ -46,750 U -3.13% $ 1,491,750 U -15.84% $ 1,772,550

Commercial $ 1,002,225 $ -101,675 U -9.21% $ 1,103,900 U -8.79% $ 1,210,300

Total Sales Revenue $ 2,447,225 $ -148,425 U -5.72% $ 2,595,650 U -12.98% $ 2,982,850

Direct Materials:

Fabric (Residential) $ 105,358 $ -255 F -0.24% $ 105,613 F -15.84% $ 125,493

Faux Wood (Residential) $ 95,200 $ 35,700 U 60.00% $ 59,500 F -15.84% $ 70,700

Vinyl (Residential) $ 85,000 $ -1,488 F -1.72% $ 86,488 F -15.84% $ 102,768

Fabric (Commercial)) $ 181,770 $ 26,145 U 16.80% $ 155,625 F -8.79% $ 170,625

Faux Wood (Commercial) $ 111,967 $ 10,292 U 10.12% $ 101,675 F -8.79% $ 111,475

Vinyl (Commercial) $ 56,025 $ -2,179 F -3.74% $ 58,204 F -8.79% $ 63,814

Total Direct Material $ 635,320 $ 68,216 U 12.03% $ 567,104 F -12.06% $ 644,874

Direct Labour:

Residential: Labour - Mfg $ 249,900 $ 79,900 U 47.00% $ 170,000 F -15.84% $ 202,000

Labour- Assembly $ 102,000 $ -8,500 F -7.69% $ 110,500 F -15.84% $ 131,300

Commercial: Labour - Mfg $ 191,730 $ 17,430 U 10.00% $ 174,300 F -8.79% $ 191,100

Labour- Assembly $ 78,850 $ -7,470 F -8.65% $ 86,320 F -8.79% $ 94,640

Total Direct Labour $ 622,480 $ 81,360 U 15.04% $ 541,120 F -12.59% $ 619,040

Variable Overhead - Residential $ 276,250 $ 39,485 U 16.68% $ 236,765 F -19.03% $ 292,400

Variable Overhead - Commercial $ 373,915 $ -55,193 F -12.86% $ 429,108 F -6.05% $ 456,757

Total Variable Cost $ 650,165 $ -15,708 F -2.36% $ 665,873 F -11.12% $ 749,157

Contribution Margin $ 539,261 $ -282,293 U -34.36% $ 821,553 U -15.28% $ 969,779

Fixed Manufacturing Cost $ 145,000 $ 5,000 U 3.57% $ 140,000 F 0.00% $ 140,000

Operating Profit $ 394,261 $ -287,293 U -42.15% $ 681,553 U -17.86% $ 829,779

BlindsforShine Limited

Budget Report for November 2018

COST ACCOUNTING

Part A

Budget Report

Actual

Result

Flexible Budget

Variance F/U %

Flexible

Budget

Sales Volume

Variance F/U % Static Budget

Units Sold:

Residential 850 0 F 850 850 U -15.84% 1010

Commercial 415 0 F 415 415 U -8.79% 455

Revenues:

Residential $ 1,445,000 $ -46,750 U -3.13% $ 1,491,750 U -15.84% $ 1,772,550

Commercial $ 1,002,225 $ -101,675 U -9.21% $ 1,103,900 U -8.79% $ 1,210,300

Total Sales Revenue $ 2,447,225 $ -148,425 U -5.72% $ 2,595,650 U -12.98% $ 2,982,850

Direct Materials:

Fabric (Residential) $ 105,358 $ -255 F -0.24% $ 105,613 F -15.84% $ 125,493

Faux Wood (Residential) $ 95,200 $ 35,700 U 60.00% $ 59,500 F -15.84% $ 70,700

Vinyl (Residential) $ 85,000 $ -1,488 F -1.72% $ 86,488 F -15.84% $ 102,768

Fabric (Commercial)) $ 181,770 $ 26,145 U 16.80% $ 155,625 F -8.79% $ 170,625

Faux Wood (Commercial) $ 111,967 $ 10,292 U 10.12% $ 101,675 F -8.79% $ 111,475

Vinyl (Commercial) $ 56,025 $ -2,179 F -3.74% $ 58,204 F -8.79% $ 63,814

Total Direct Material $ 635,320 $ 68,216 U 12.03% $ 567,104 F -12.06% $ 644,874

Direct Labour:

Residential: Labour - Mfg $ 249,900 $ 79,900 U 47.00% $ 170,000 F -15.84% $ 202,000

Labour- Assembly $ 102,000 $ -8,500 F -7.69% $ 110,500 F -15.84% $ 131,300

Commercial: Labour - Mfg $ 191,730 $ 17,430 U 10.00% $ 174,300 F -8.79% $ 191,100

Labour- Assembly $ 78,850 $ -7,470 F -8.65% $ 86,320 F -8.79% $ 94,640

Total Direct Labour $ 622,480 $ 81,360 U 15.04% $ 541,120 F -12.59% $ 619,040

Variable Overhead - Residential $ 276,250 $ 39,485 U 16.68% $ 236,765 F -19.03% $ 292,400

Variable Overhead - Commercial $ 373,915 $ -55,193 F -12.86% $ 429,108 F -6.05% $ 456,757

Total Variable Cost $ 650,165 $ -15,708 F -2.36% $ 665,873 F -11.12% $ 749,157

Contribution Margin $ 539,261 $ -282,293 U -34.36% $ 821,553 U -15.28% $ 969,779

Fixed Manufacturing Cost $ 145,000 $ 5,000 U 3.57% $ 140,000 F 0.00% $ 140,000

Operating Profit $ 394,261 $ -287,293 U -42.15% $ 681,553 U -17.86% $ 829,779

BlindsforShine Limited

Budget Report for November 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

COST ACCOUNTING

Part B

Variance Analysis

The revenue which is earned by the business is mainly through sales of blinds which are

for both commercial and residential purpose. The sales unit which is estimated for the business is

shown to be 850 units and 415 units. The above table shows certain variances which are above

5% which needs to be considered by the management of the business for the purpose of taking

appropriate decisions regarding the same. The budgeted sales of commercial blinds areestimated

to be $ 1,103,900 for the year and the actual result which is achieved by the business is shown to

be $ 1,002,225 which creates a variance as shown in the budget above (Jansen & Zarges, 2014).

The main reason behind the same can be attributed to the downturn in the market of blinds which

has affected the sales of the business and thereby also has impacted. The variance percentage

which is computed is shown to be above 5% which shows that a major deviation from the

standard set has occurred which the management of the company needs to consider in the

decision-making process. The total sales revenue which was estimated by the management of

BlindsforShine ltd has also not meet with the actual results of the business

(Prieur & Tarantola, 2017). The management of the company has not been able

to maintain the sales of commercial blinds which is the main reason for the

fall of overall sales of the business in comparison to the budget established

by the business.

The management of the company has also incurred significant amount of expenses in

terms of direct material of Faux Wood (Residential) which is also shown to be unfavorable in

nature and the difference is shown to be $ 35,700. The variance can be caused due to due to

increase in the costs of the raw materials of the business more than the expectation of the

COST ACCOUNTING

Part B

Variance Analysis

The revenue which is earned by the business is mainly through sales of blinds which are

for both commercial and residential purpose. The sales unit which is estimated for the business is

shown to be 850 units and 415 units. The above table shows certain variances which are above

5% which needs to be considered by the management of the business for the purpose of taking

appropriate decisions regarding the same. The budgeted sales of commercial blinds areestimated

to be $ 1,103,900 for the year and the actual result which is achieved by the business is shown to

be $ 1,002,225 which creates a variance as shown in the budget above (Jansen & Zarges, 2014).

The main reason behind the same can be attributed to the downturn in the market of blinds which

has affected the sales of the business and thereby also has impacted. The variance percentage

which is computed is shown to be above 5% which shows that a major deviation from the

standard set has occurred which the management of the company needs to consider in the

decision-making process. The total sales revenue which was estimated by the management of

BlindsforShine ltd has also not meet with the actual results of the business

(Prieur & Tarantola, 2017). The management of the company has not been able

to maintain the sales of commercial blinds which is the main reason for the

fall of overall sales of the business in comparison to the budget established

by the business.

The management of the company has also incurred significant amount of expenses in

terms of direct material of Faux Wood (Residential) which is also shown to be unfavorable in

nature and the difference is shown to be $ 35,700. The variance can be caused due to due to

increase in the costs of the raw materials of the business more than the expectation of the

5

COST ACCOUNTING

management (Sunarni, 2013). The total direct material costs of the business is shown to have

unfavorable balance as the same is more than the budgeted expenses which was estimated by the

management of the company (Chapman, Kern & Laguecir, 2014). The direct labour costs of the

business is shown to be more than the estimation which was made by the business earlier which

is the reason for the variance. The reason for the variance might be the rise in costs of the labor

in the market and also the labour turnover can also be one of the reason for the rise in the costs of

direct labour of the business. The labour turnover rise affects the business as the same requires

business to recruit new employees and also train them to suit the processes of the business. The

variance for direct labour cost is also shown to be more than 5% which is material and therefore

must be considered by the management for the purpose of taking important decisions of the

business. The operating profit of the business is shown to be $ 681,583 as per budgeted estimate

and the actual result of the business is shown to be $ 394,261. The variance is computed to be of

$ 287,293 which shows that the business is not performing as well as the management

anticipates. The lower profit may be caused due to the fall in the sales of the business in

comparison to the budgeted expenses of the business and also the costs of direct material and

direct labour is much more than what was anticipated by the management.

Recommendation for Variances

The variances of the budgets need to be considered by the management of the business

and in accordance to the materiality of the variance appropriate steps are to taken by the

management to rectify the situation as soon as possible. Variances represent lapses in the

performance standard of the business or faulty setting of the budget. Therefore, it is always a

necessity that the budget should be prepared with proper estimation and forecasting. The

variances which appear in the budget between the actual results and the budgeted estimates are

COST ACCOUNTING

management (Sunarni, 2013). The total direct material costs of the business is shown to have

unfavorable balance as the same is more than the budgeted expenses which was estimated by the

management of the company (Chapman, Kern & Laguecir, 2014). The direct labour costs of the

business is shown to be more than the estimation which was made by the business earlier which

is the reason for the variance. The reason for the variance might be the rise in costs of the labor

in the market and also the labour turnover can also be one of the reason for the rise in the costs of

direct labour of the business. The labour turnover rise affects the business as the same requires

business to recruit new employees and also train them to suit the processes of the business. The

variance for direct labour cost is also shown to be more than 5% which is material and therefore

must be considered by the management for the purpose of taking important decisions of the

business. The operating profit of the business is shown to be $ 681,583 as per budgeted estimate

and the actual result of the business is shown to be $ 394,261. The variance is computed to be of

$ 287,293 which shows that the business is not performing as well as the management

anticipates. The lower profit may be caused due to the fall in the sales of the business in

comparison to the budgeted expenses of the business and also the costs of direct material and

direct labour is much more than what was anticipated by the management.

Recommendation for Variances

The variances of the budgets need to be considered by the management of the business

and in accordance to the materiality of the variance appropriate steps are to taken by the

management to rectify the situation as soon as possible. Variances represent lapses in the

performance standard of the business or faulty setting of the budget. Therefore, it is always a

necessity that the budget should be prepared with proper estimation and forecasting. The

variances which appear in the budget between the actual results and the budgeted estimates are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

COST ACCOUNTING

important as the same are useful in maintain supervision and control over the activities of the

business. The corrective measures which can be taken by the management of BlindsforShine

ltd are discussed below in details:

There is a major variance in sales which is achieved by the business which may be due to

the downturn in the market and also due to competition in the market. The management

needs to make innovative changes in the products in order to stay ahead of the

competitors of the business and also incorporate an effective advertisement plan which

will then help the business to promote its products and make the people know about the

attributes of the products which is offered by the company. Effective promotion of the

product will increase the sales of the products and thereby the sales revenue of the

business.

The budget report also shows that the overall costs of materials are more than anticipated

by the business. This problem can be solved with the help of changing the purchase

pattern of raw materials for the business (Mbawuni & Anertey, 2014). The business can

purchase the raw materials in bulk and effectively store the same which will reduce the

material costs of the business and the management will be able to meet the necessary

budgeting estimates.

The direct labour costs of the business is also shown to be more than the estimates which

are considered by the business in the budgeting process. The reason for the variance may

be due to the increase in the labour rates in the market or due to high turnover ratio of

employees in the business (Fullerton, Kennedy & Widener, 2013). The management

needs to formulate a strategy through which the business is able to retain and motivate

the employees of the business. The employees of the business can be motivated by

COST ACCOUNTING

important as the same are useful in maintain supervision and control over the activities of the

business. The corrective measures which can be taken by the management of BlindsforShine

ltd are discussed below in details:

There is a major variance in sales which is achieved by the business which may be due to

the downturn in the market and also due to competition in the market. The management

needs to make innovative changes in the products in order to stay ahead of the

competitors of the business and also incorporate an effective advertisement plan which

will then help the business to promote its products and make the people know about the

attributes of the products which is offered by the company. Effective promotion of the

product will increase the sales of the products and thereby the sales revenue of the

business.

The budget report also shows that the overall costs of materials are more than anticipated

by the business. This problem can be solved with the help of changing the purchase

pattern of raw materials for the business (Mbawuni & Anertey, 2014). The business can

purchase the raw materials in bulk and effectively store the same which will reduce the

material costs of the business and the management will be able to meet the necessary

budgeting estimates.

The direct labour costs of the business is also shown to be more than the estimates which

are considered by the business in the budgeting process. The reason for the variance may

be due to the increase in the labour rates in the market or due to high turnover ratio of

employees in the business (Fullerton, Kennedy & Widener, 2013). The management

needs to formulate a strategy through which the business is able to retain and motivate

the employees of the business. The employees of the business can be motivated by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

COST ACCOUNTING

providing them with better facilities, pay and working environment. This will reduce the

unnecessary training costs of new employees and also the costs which are committed by

inexperienced employees and thereby reduce the overall direct labour costs of the

business.

The management needs to incorporate a proper plan for monitoring and supervising the

activities of the business in order to control the expenses of the business also supervise

the various activities which are undertaken by the business during the period. The

activities of the business are to be supervised so that the employees are not engaged in

any unproductive activity. This plan will itself reduce the overall costs of the business

and also ensure that the various estimates which are set in the budget are meet when

actual results are revealed.

COST ACCOUNTING

providing them with better facilities, pay and working environment. This will reduce the

unnecessary training costs of new employees and also the costs which are committed by

inexperienced employees and thereby reduce the overall direct labour costs of the

business.

The management needs to incorporate a proper plan for monitoring and supervising the

activities of the business in order to control the expenses of the business also supervise

the various activities which are undertaken by the business during the period. The

activities of the business are to be supervised so that the employees are not engaged in

any unproductive activity. This plan will itself reduce the overall costs of the business

and also ensure that the various estimates which are set in the budget are meet when

actual results are revealed.

8

COST ACCOUNTING

Reference

Chapman, C., Kern, A., & Laguecir, A. (2014). Costing practices in healthcare. Accounting

Horizons, 28(2), 353-364.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2013). Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), 50-71.

Jansen, T., & Zarges, C. (2014). Performance analysis of randomised search heuristics operating

with a fixed budget. Theoretical Computer Science, 545, 39-58.

Mbawuni, J., & Anertey, A. R. (2014). Exploring management accounting practices in emerging

telecommunication market in Ghana. Accounting and Finance Research, 3(4), 71.

Prieur, C., & Tarantola, S. (2017). Variance-based sensitivity analysis: Theory and estimation

algorithms. Handbook of Uncertainty Quantification, 1217-1239.

Sunarni, C. W. (2013). Management accounting practices and the role of management

accountant: Evidence from manufacturing companies throughout Yogyakarta,

Indonesia. Review of Integrative Business and Economics Research, 2(2), 616-626.

COST ACCOUNTING

Reference

Chapman, C., Kern, A., & Laguecir, A. (2014). Costing practices in healthcare. Accounting

Horizons, 28(2), 353-364.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2013). Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), 50-71.

Jansen, T., & Zarges, C. (2014). Performance analysis of randomised search heuristics operating

with a fixed budget. Theoretical Computer Science, 545, 39-58.

Mbawuni, J., & Anertey, A. R. (2014). Exploring management accounting practices in emerging

telecommunication market in Ghana. Accounting and Finance Research, 3(4), 71.

Prieur, C., & Tarantola, S. (2017). Variance-based sensitivity analysis: Theory and estimation

algorithms. Handbook of Uncertainty Quantification, 1217-1239.

Sunarni, C. W. (2013). Management accounting practices and the role of management

accountant: Evidence from manufacturing companies throughout Yogyakarta,

Indonesia. Review of Integrative Business and Economics Research, 2(2), 616-626.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.