ACCT209 Corporate Accounting - Consolidated Financial Statements Case

VerifiedAdded on 2023/06/07

|7

|885

|56

Case Study

AI Summary

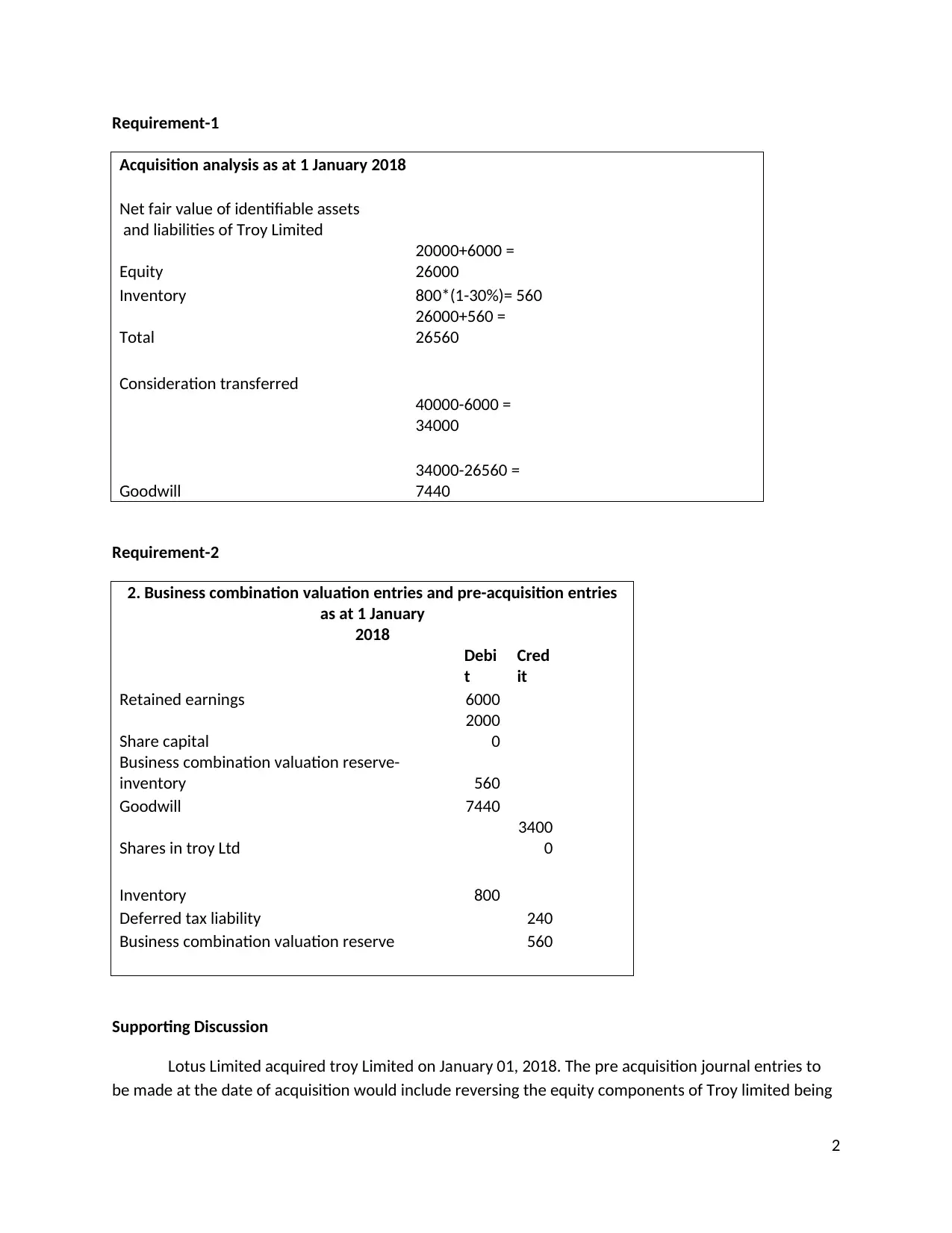

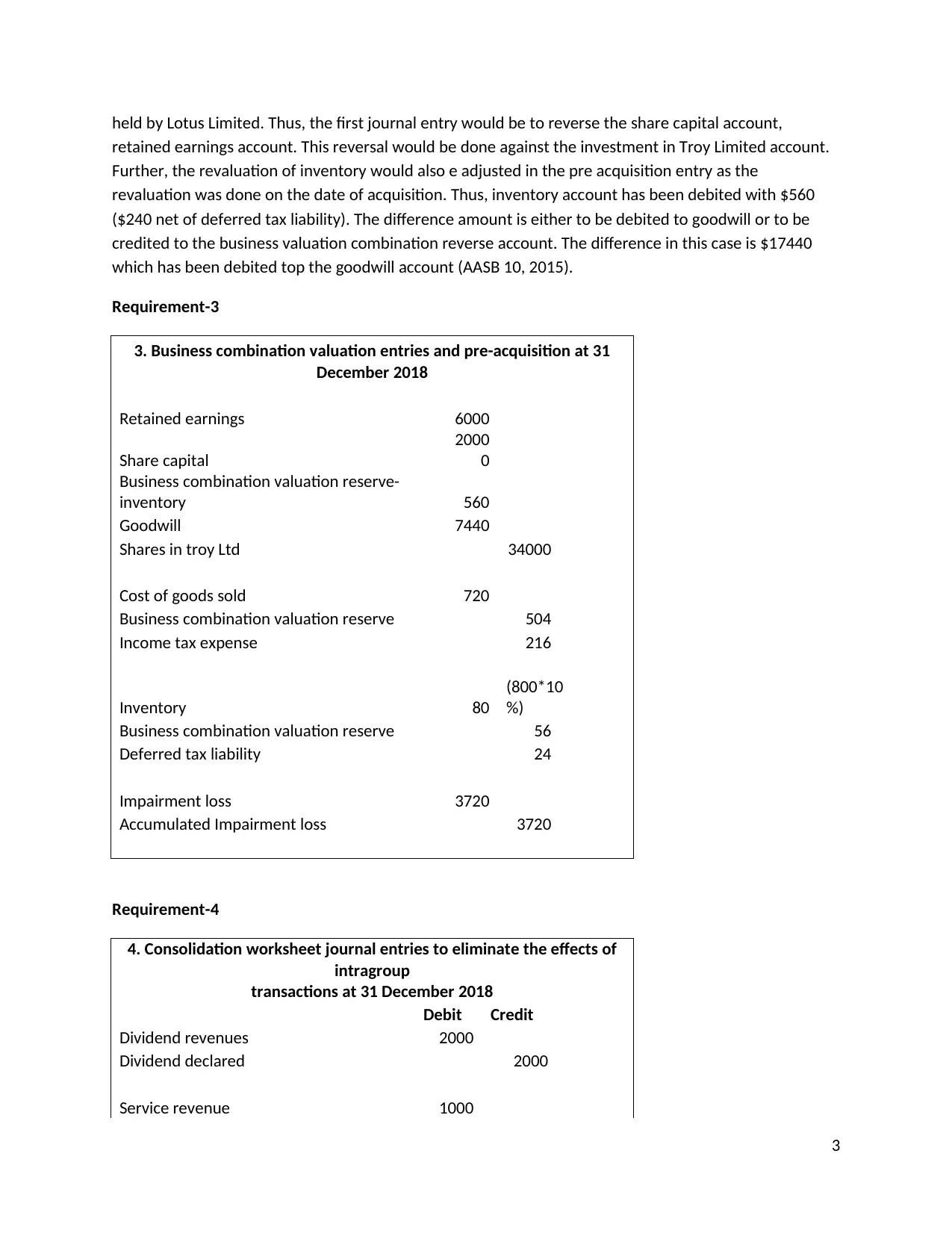

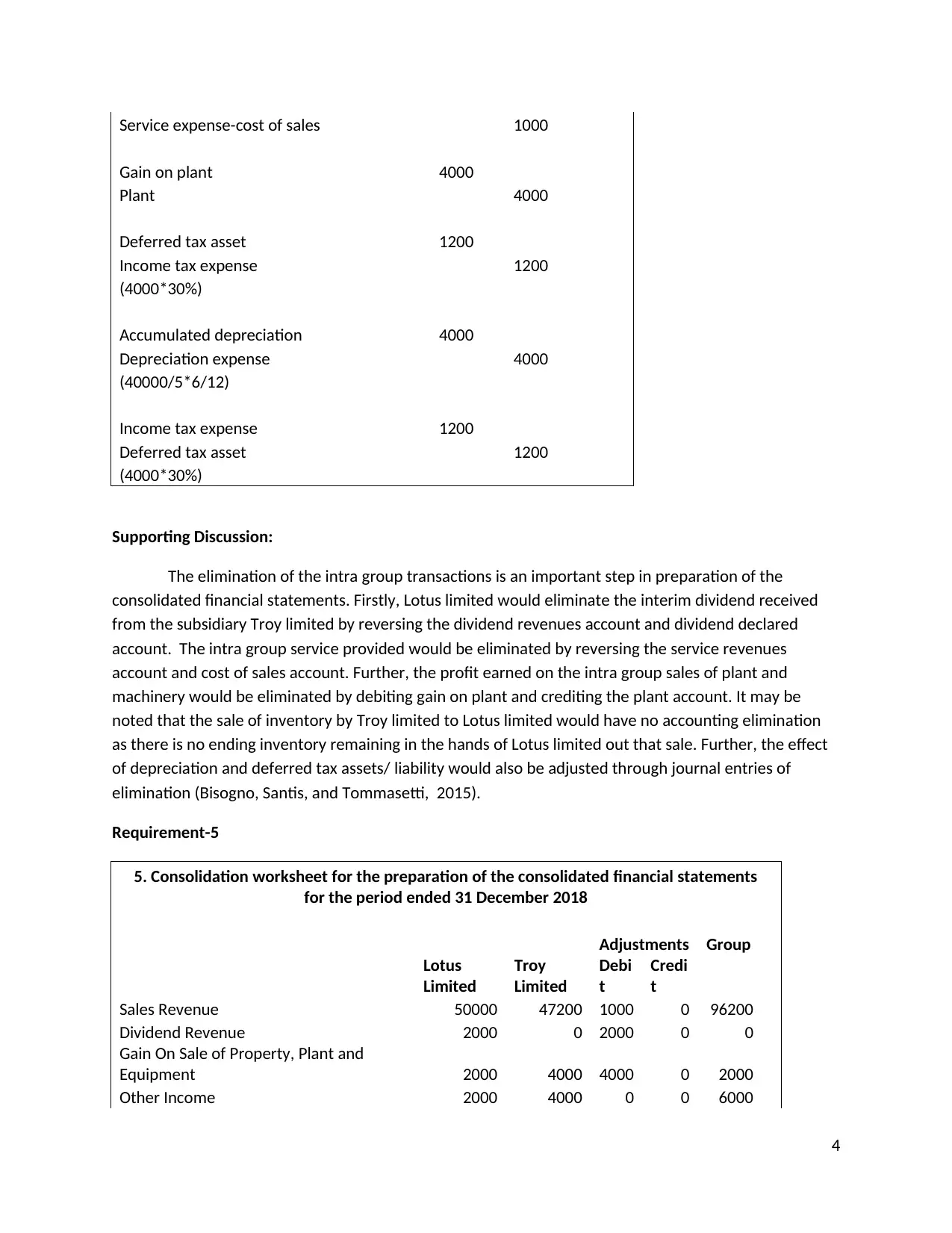

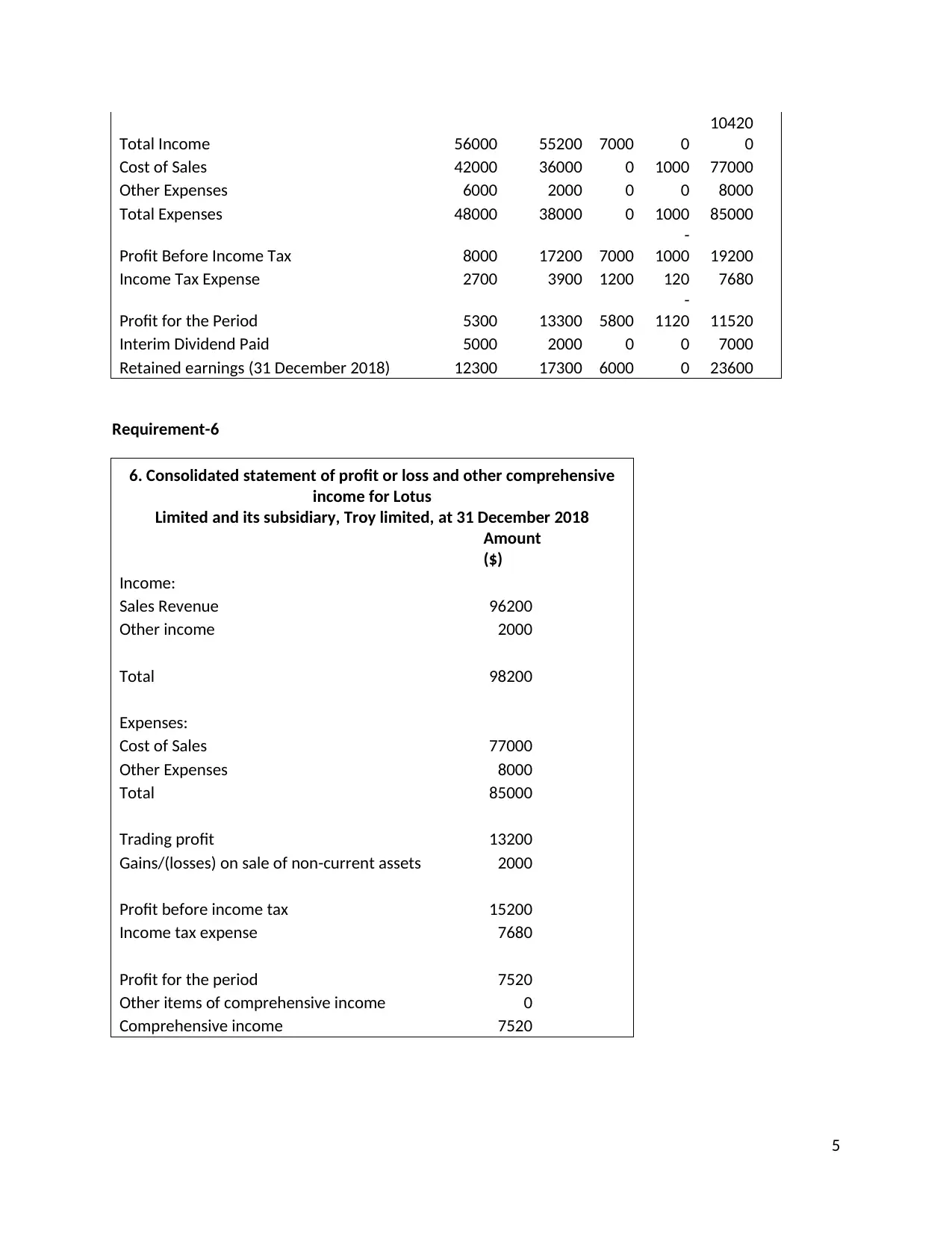

This assignment presents a case study involving Lotus Limited and its subsidiary, Troy Limited, focusing on the preparation of consolidated financial statements. The analysis includes an acquisition analysis as of January 1, 2018, business combination valuation entries, pre-acquisition entries, and consolidation worksheet journal entries for eliminating intra-group transactions as of December 31, 2018. Key aspects covered are the calculation of goodwill, the elimination of dividend revenues, service revenues, and gains on plant sales between the companies. The assignment culminates in the preparation of a consolidated statement of profit or loss and other comprehensive income for the period ended December 31, 2018, adhering to accounting standards such as AASB 10. The case study provides detailed financial information and additional context, requiring a thorough understanding of corporate accounting principles and consolidation techniques.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.