ACCT6003 - Financial Accounting Processes: Company Case Study

VerifiedAdded on 2023/06/10

|13

|1257

|125

Practical Assignment

AI Summary

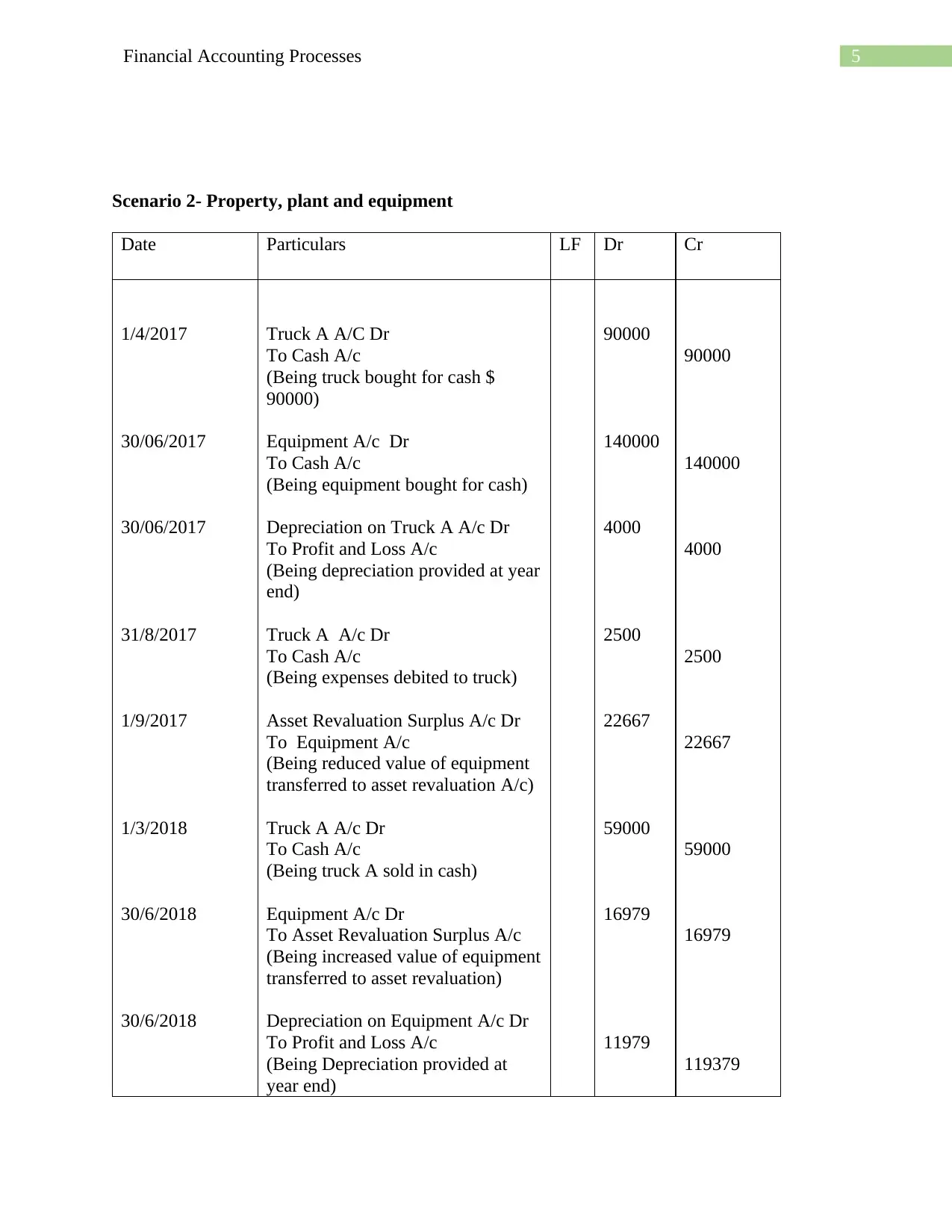

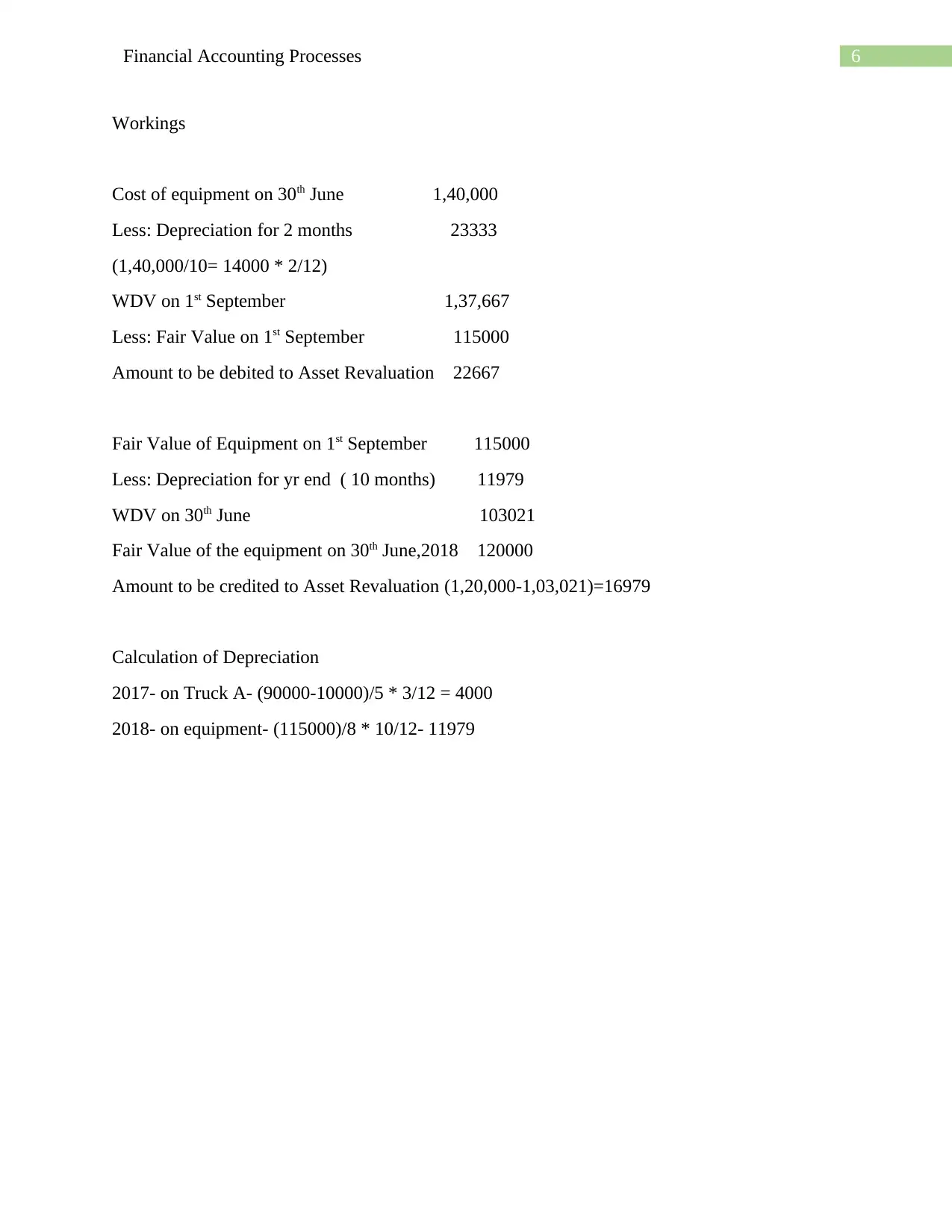

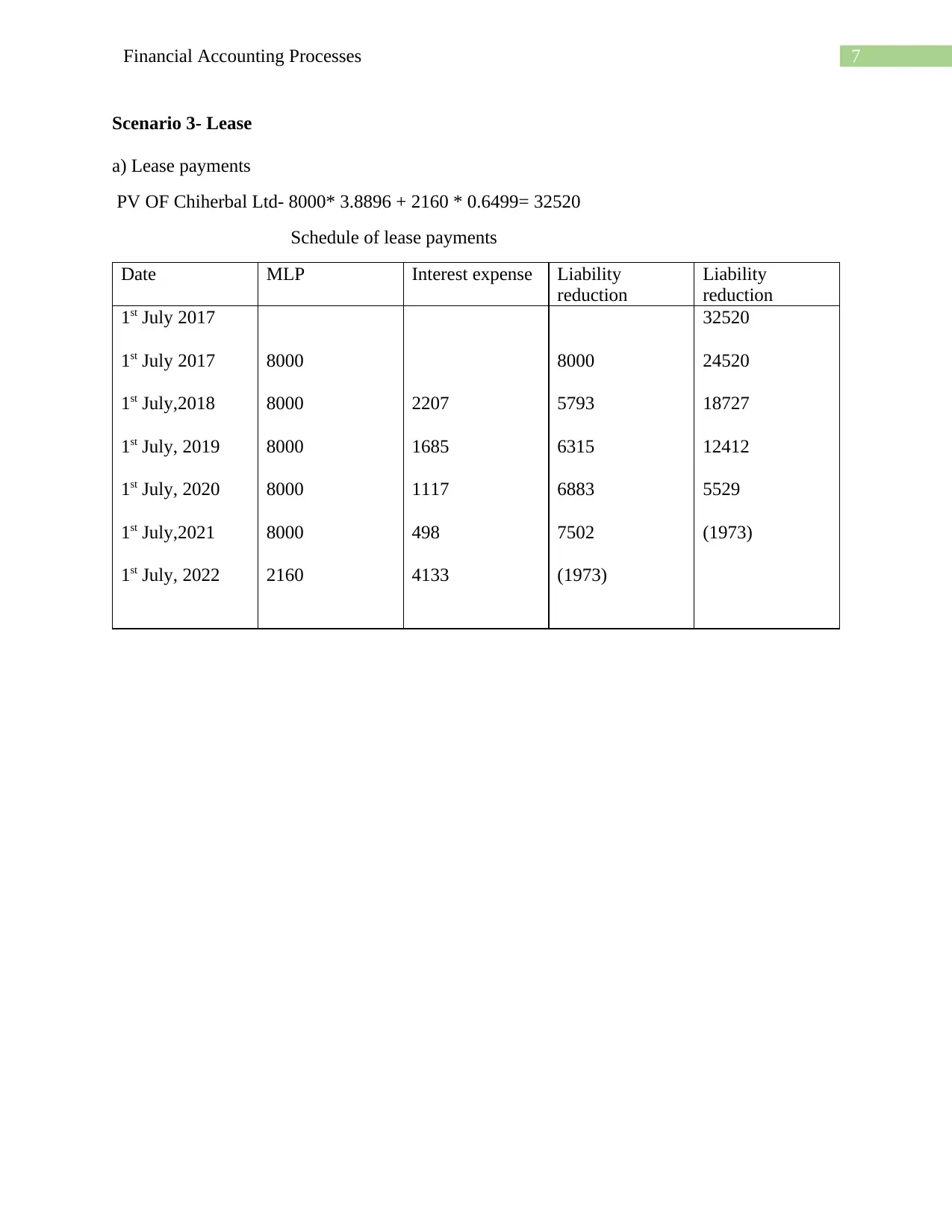

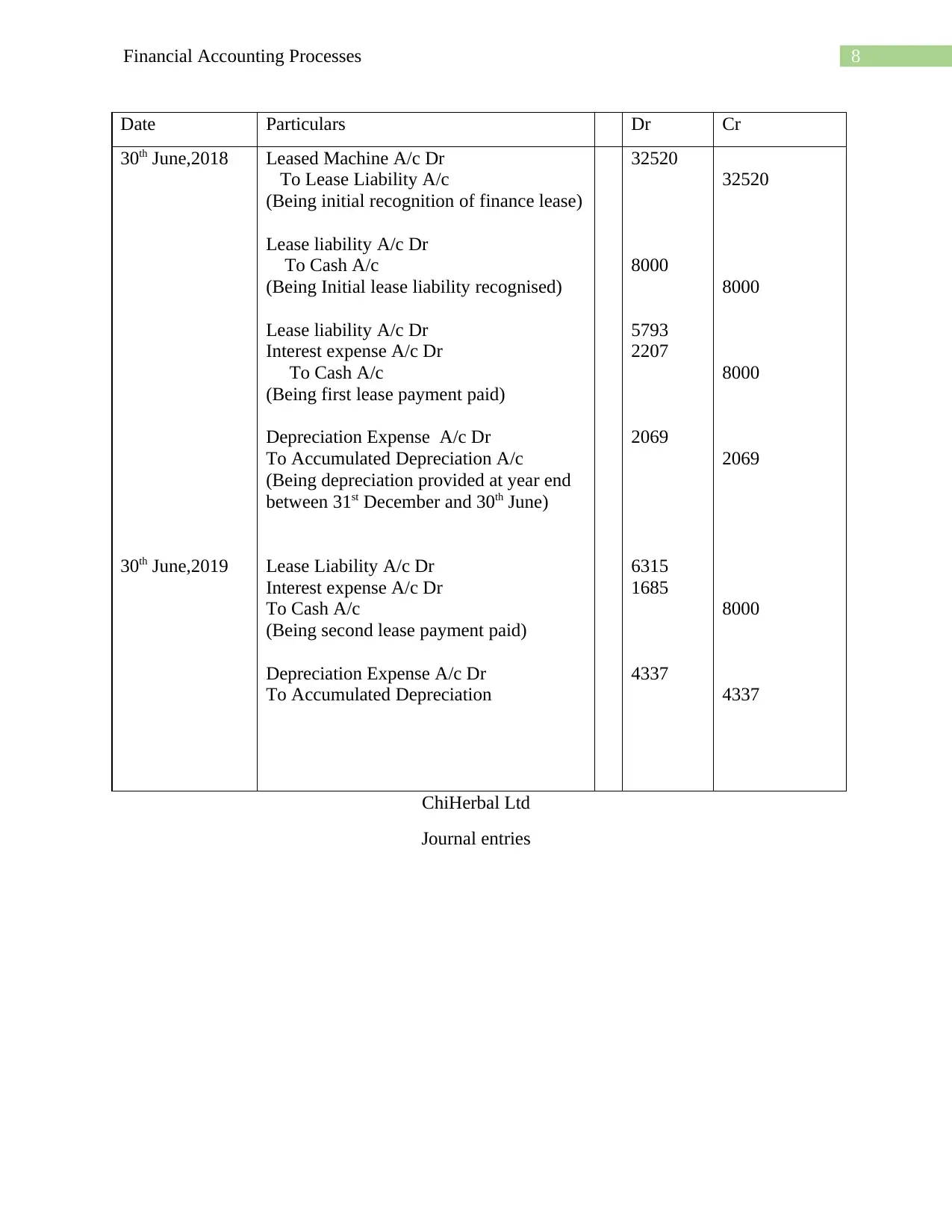

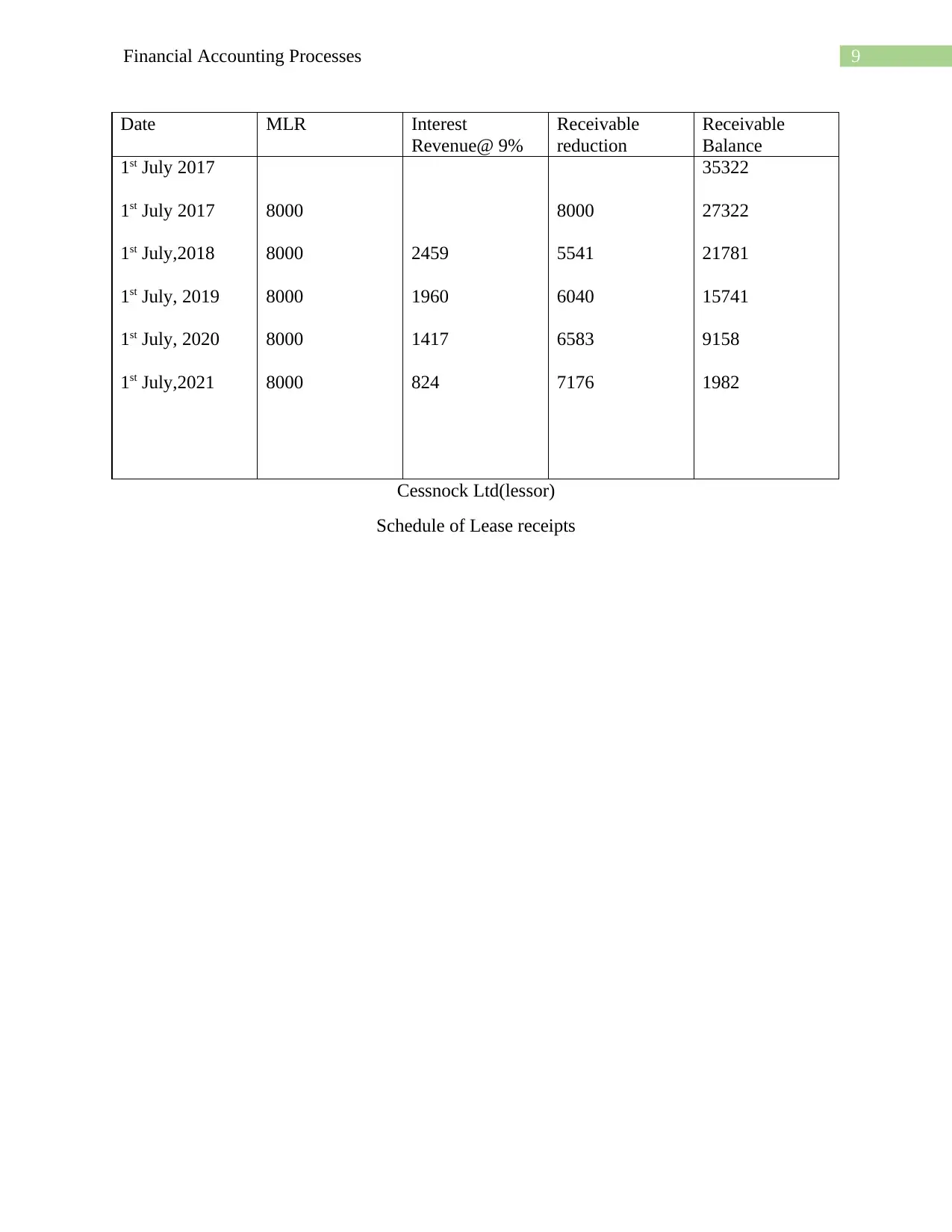

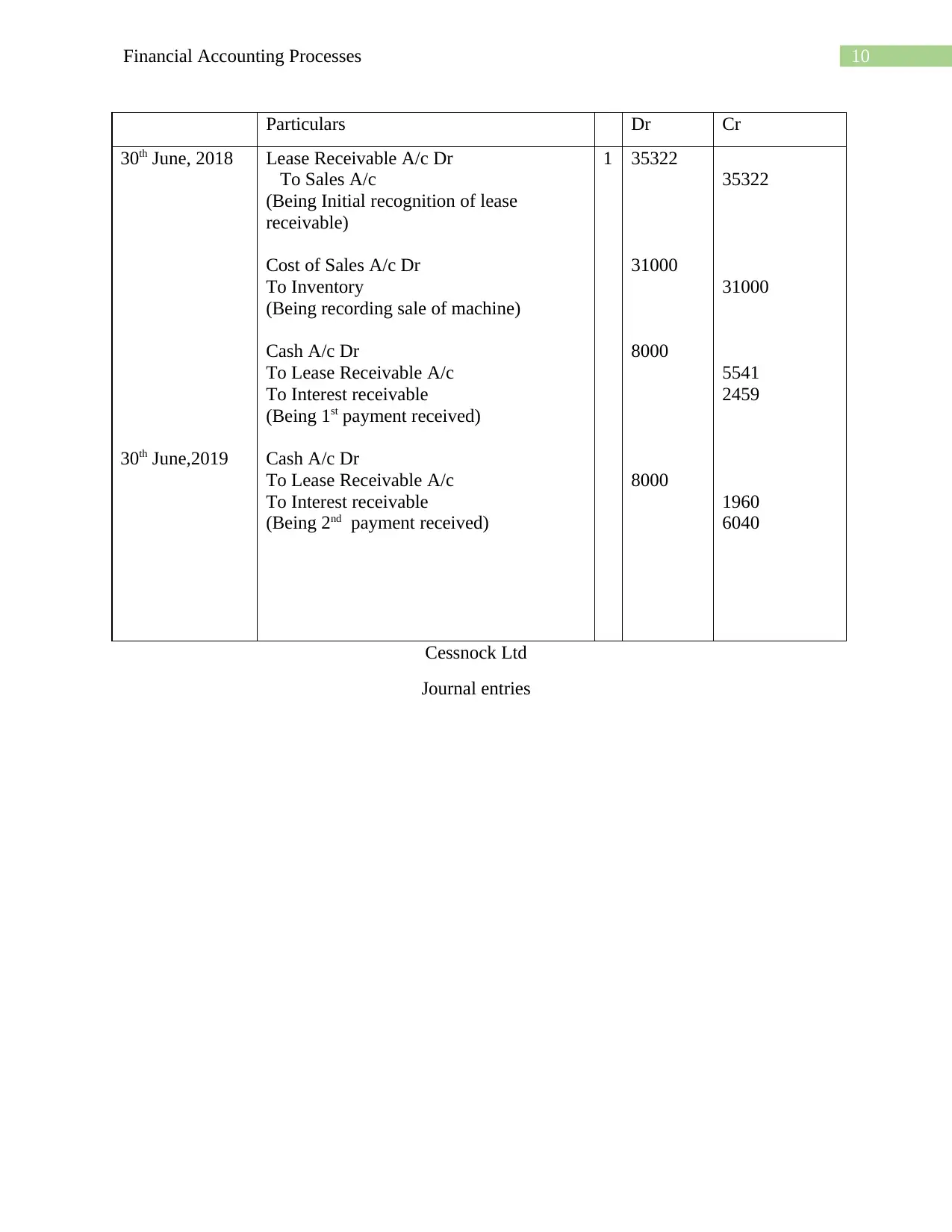

This assignment provides solutions to various financial accounting scenarios, including financing company operations through share issuance, accounting for property, plant, and equipment (PPE) with depreciation and revaluation, lease accounting under both lessee and lessor perspectives, and the treatment of intangible assets according to IAS 38. The share issuance scenario includes journal entries for application, allotment, calls, and forfeiture of shares. The PPE scenario demonstrates the accounting for asset purchases, depreciation, revaluation surpluses, and asset sales. The lease scenario covers the initial recognition, subsequent payments, and depreciation for the lessee, as well as the initial recognition and revenue recognition for the lessor. Finally, the treatment of software development costs as intangible assets is discussed with reference to IAS 38, emphasizing the capitalization of certain costs while expensing others. Desklib offers a range of study tools to help students understand accounting principles and practices.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.