ACCT702 Advanced Financial Accounting: NZ IFRS 16 and the Warehouse

VerifiedAdded on 2023/04/20

|11

|1347

|294

Report

AI Summary

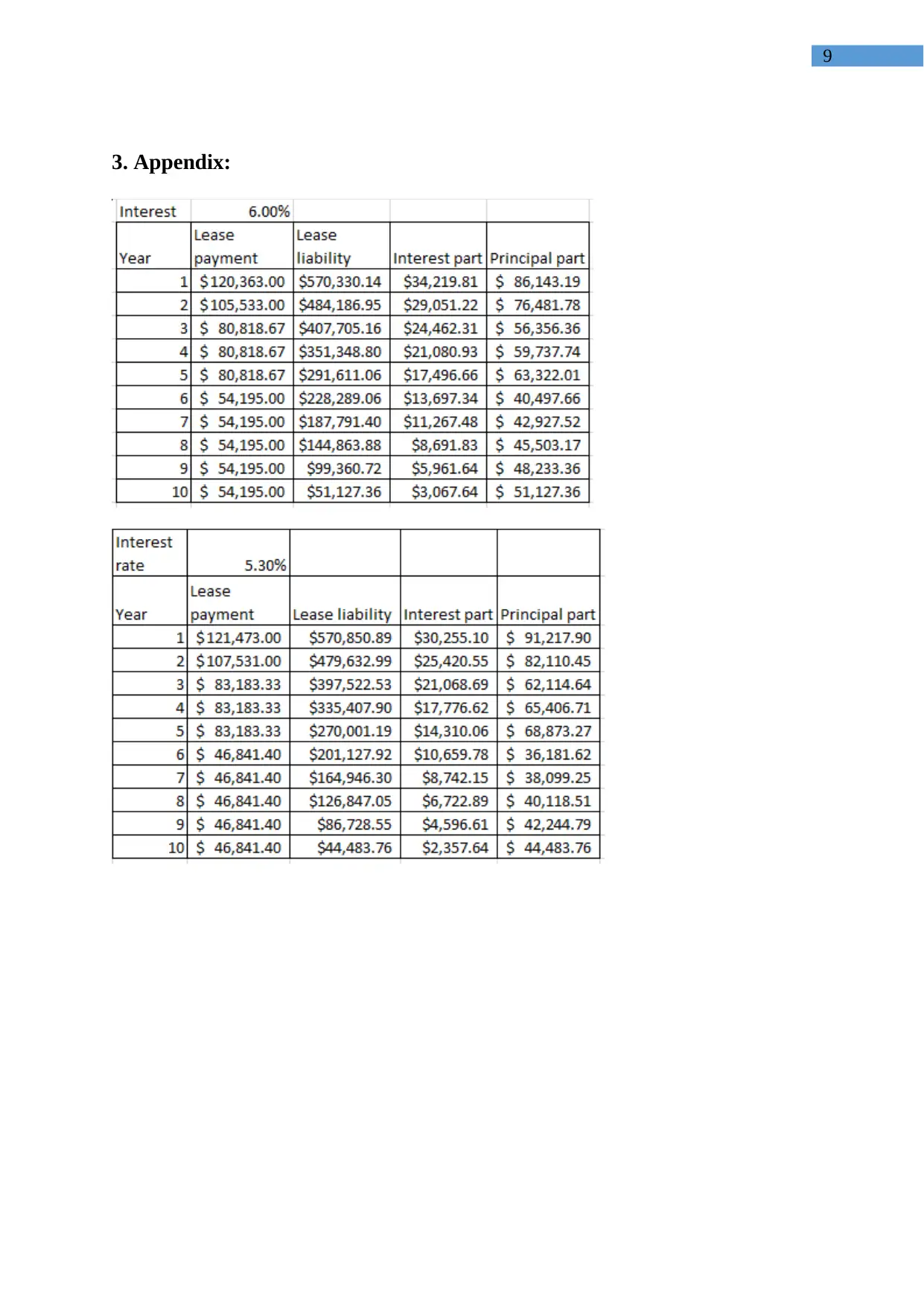

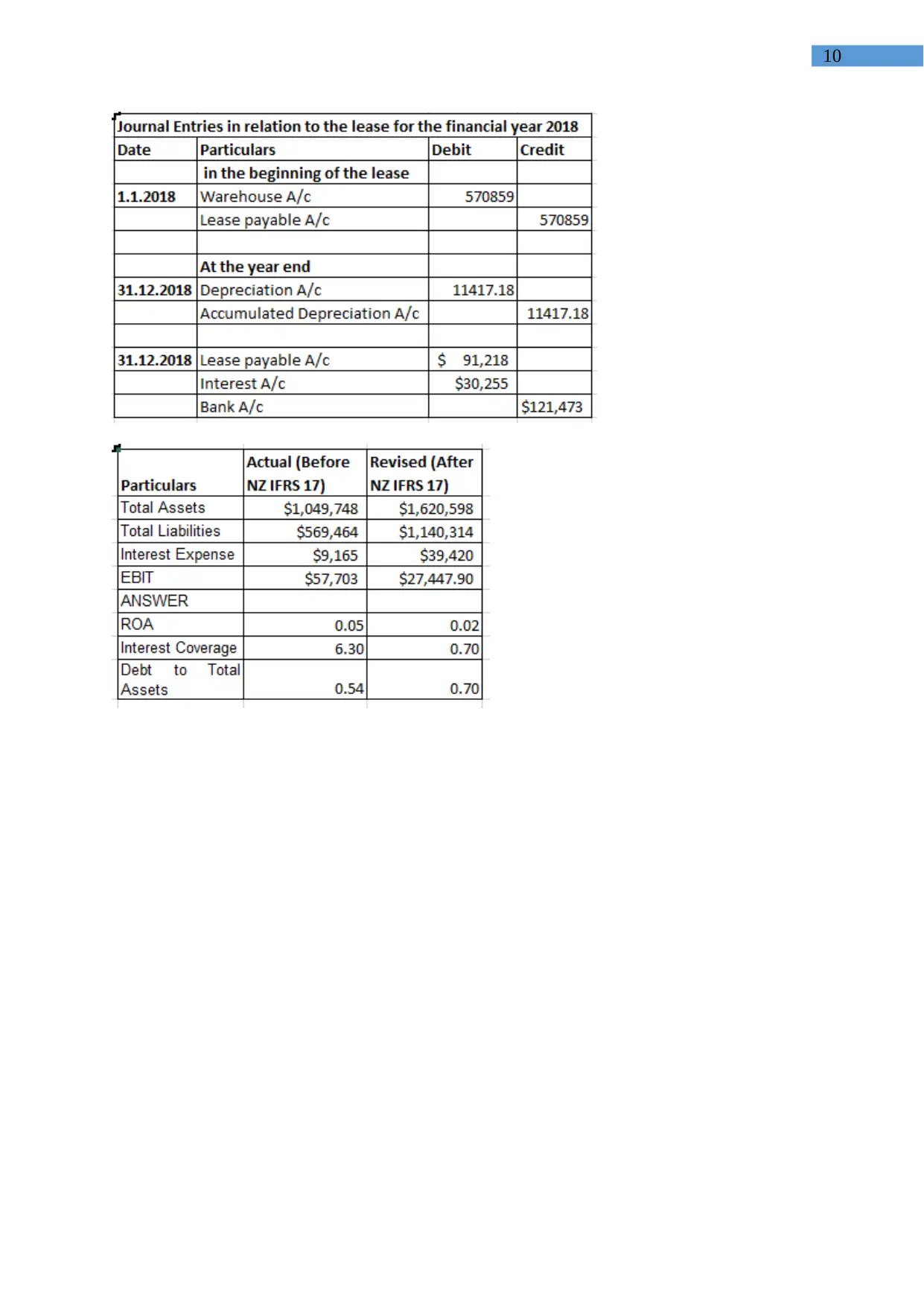

This report examines the effects of NZ IFRS 16 on a company's financial health, focusing on warehouse lease accounting. It details the implications of the new standard, including the capitalization of leases and the termination of old operating leases. The report includes journal entries and a recalculation of financial ratios, such as ROA, interest coverage, and debt to total assets, to demonstrate the impact of the new standard on financial statement analysis. The changes in these ratios are discussed in terms of their potential effect on investors' perceptions of the company's performance and financial stability. Ultimately, the report concludes that NZ IFRS 16 has significantly altered financial reporting and revealed weaknesses, emphasizing the need for retrospective adjustments to existing operating lease agreements.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.