ACCTG 221: Management Accounting - Cost Allocation & Regression Report

VerifiedAdded on 2023/06/14

|6

|1090

|77

Report

AI Summary

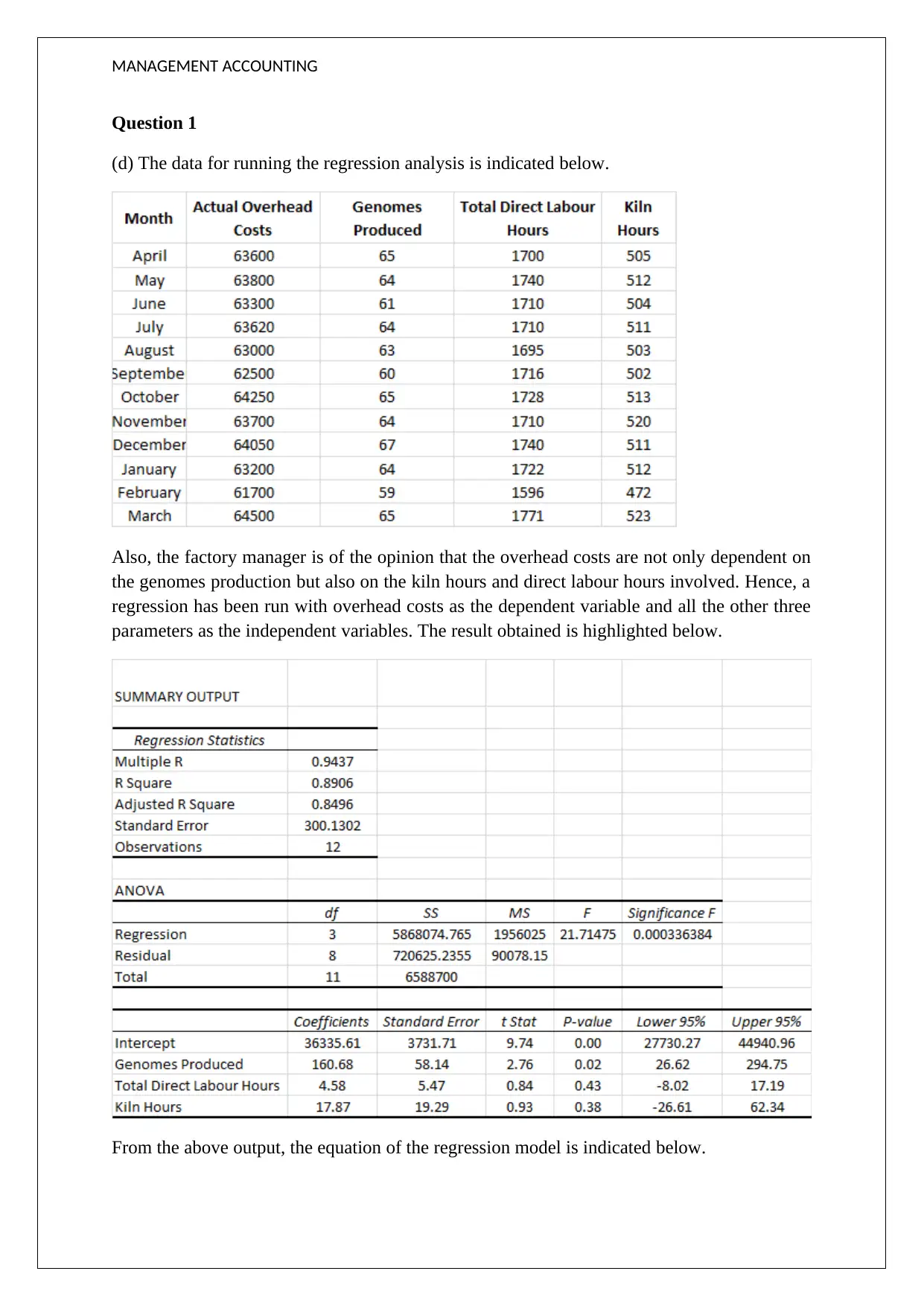

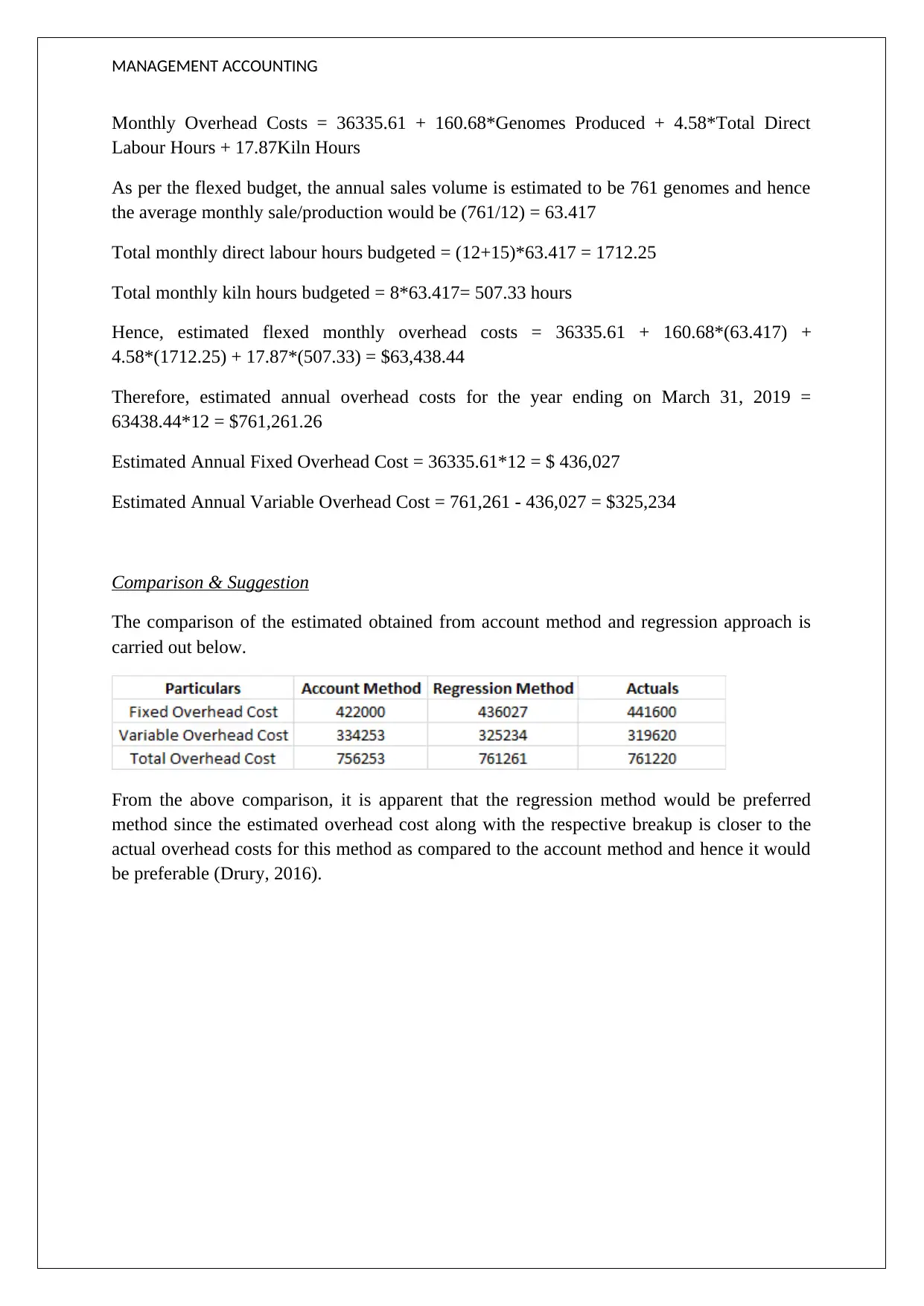

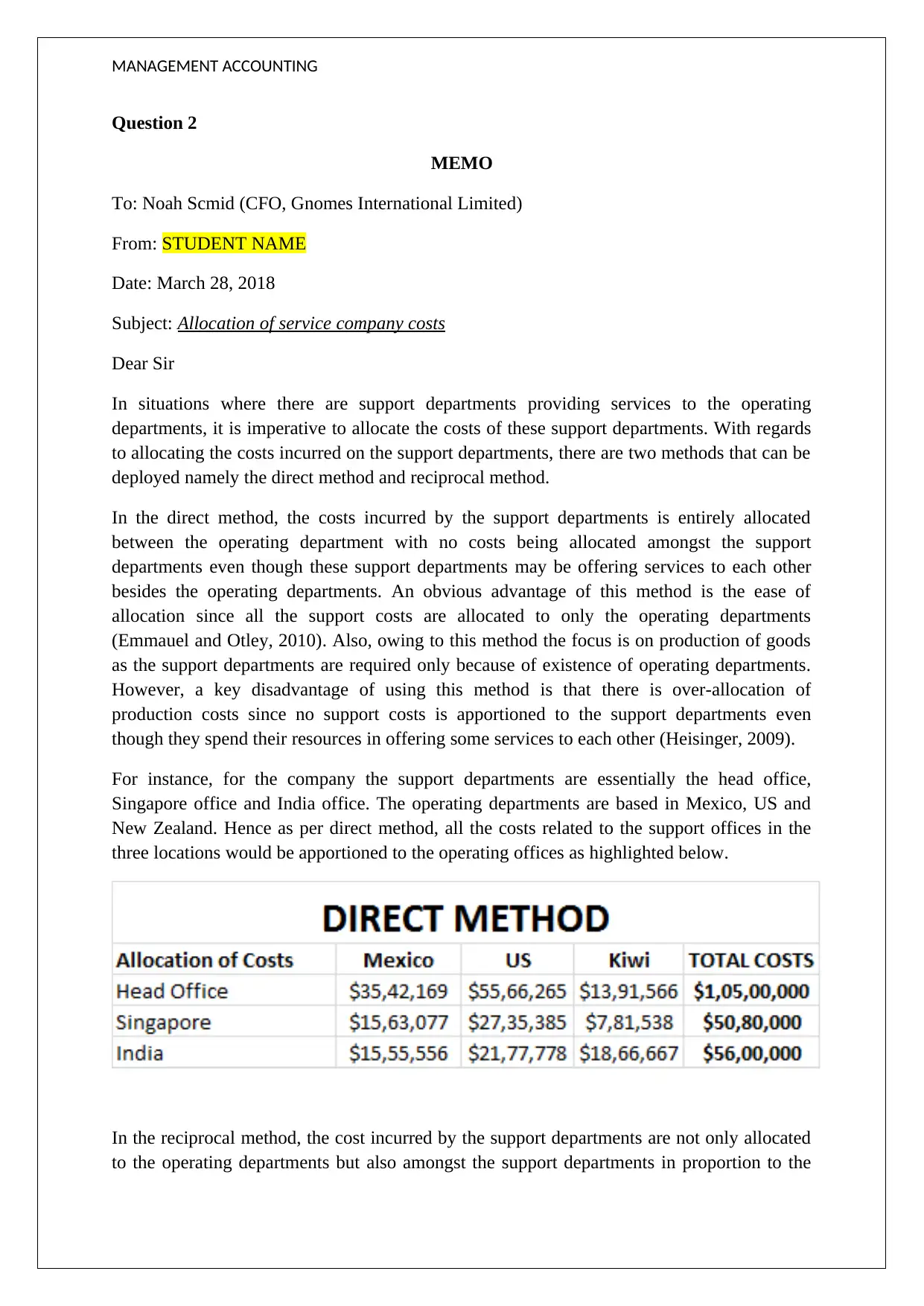

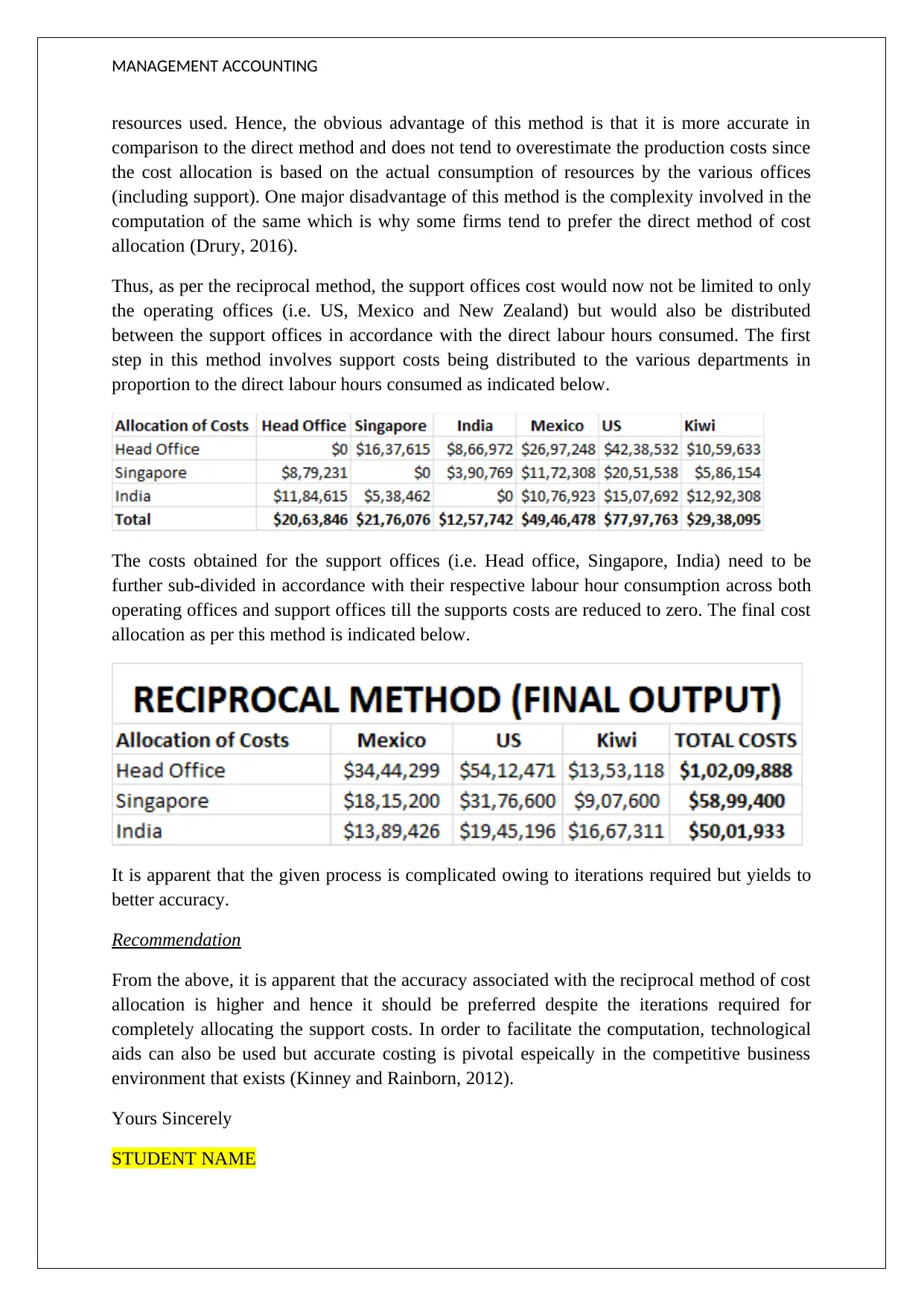

This report delves into management accounting, focusing on cost allocation methods and regression analysis. It compares the direct and reciprocal methods for allocating service company costs, highlighting the advantages and disadvantages of each. The report also utilizes regression analysis to estimate overhead costs based on genomes produced, direct labor hours, and kiln hours, comparing the results with the account method. Ultimately, the report recommends the reciprocal method for cost allocation due to its higher accuracy and suggests using technological aids to facilitate computation. This detailed analysis provides valuable insights into cost management strategies and their impact on financial accuracy. Desklib offers a wide range of solved assignments and past papers for students seeking additional resources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.