AC&DC Ltd. Financial Accounting Assignment Solution

VerifiedAdded on 2021/08/10

|28

|3540

|239

Homework Assignment

AI Summary

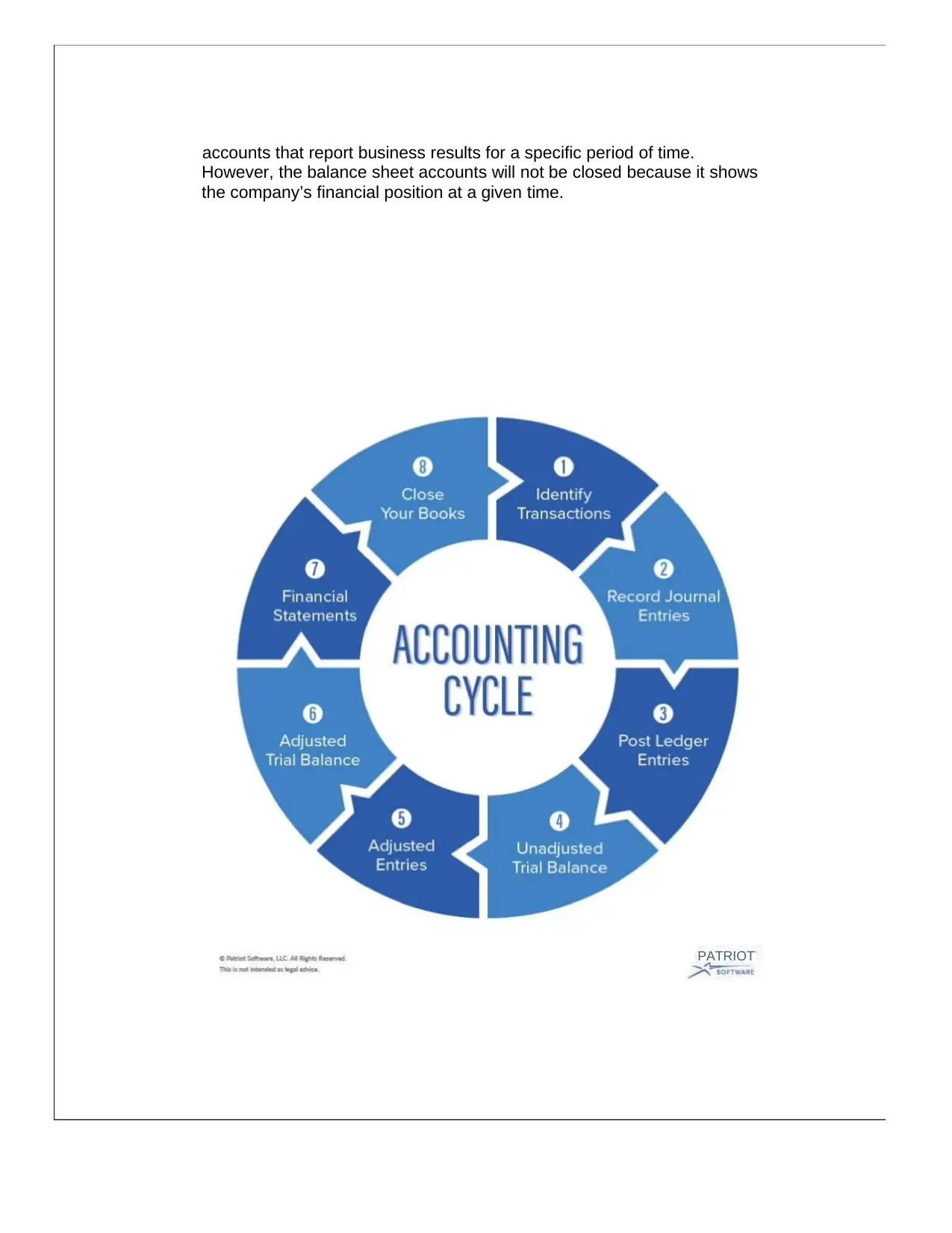

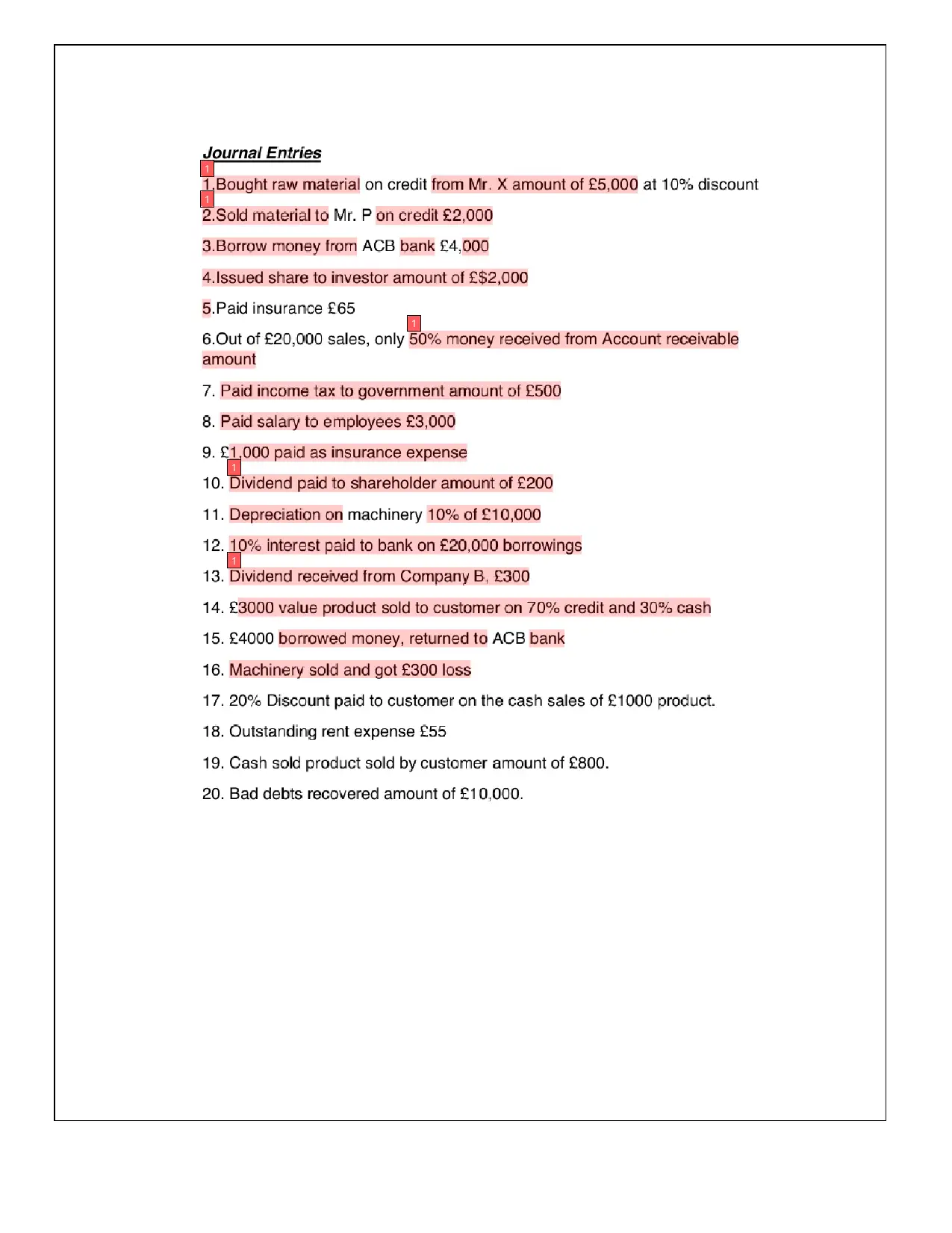

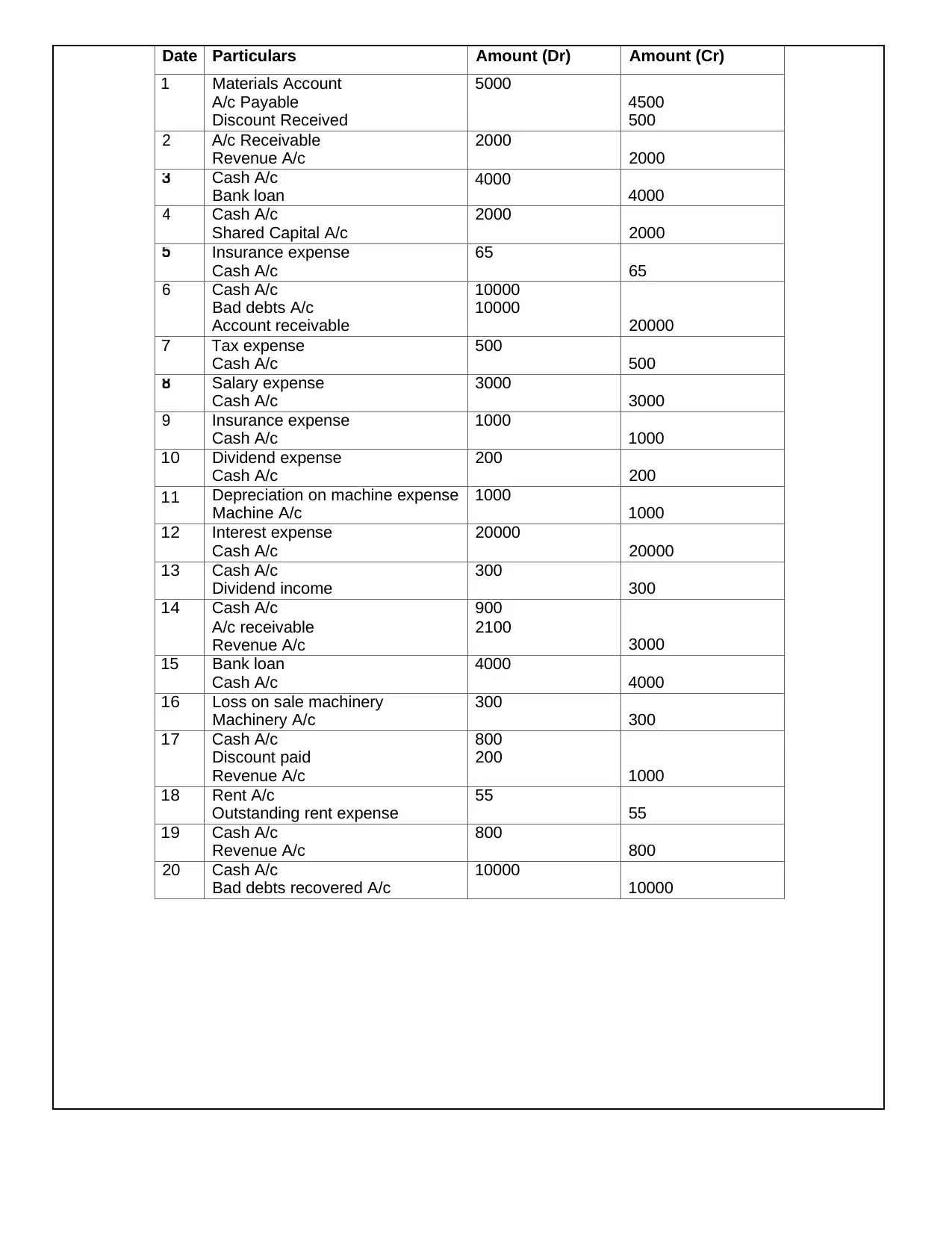

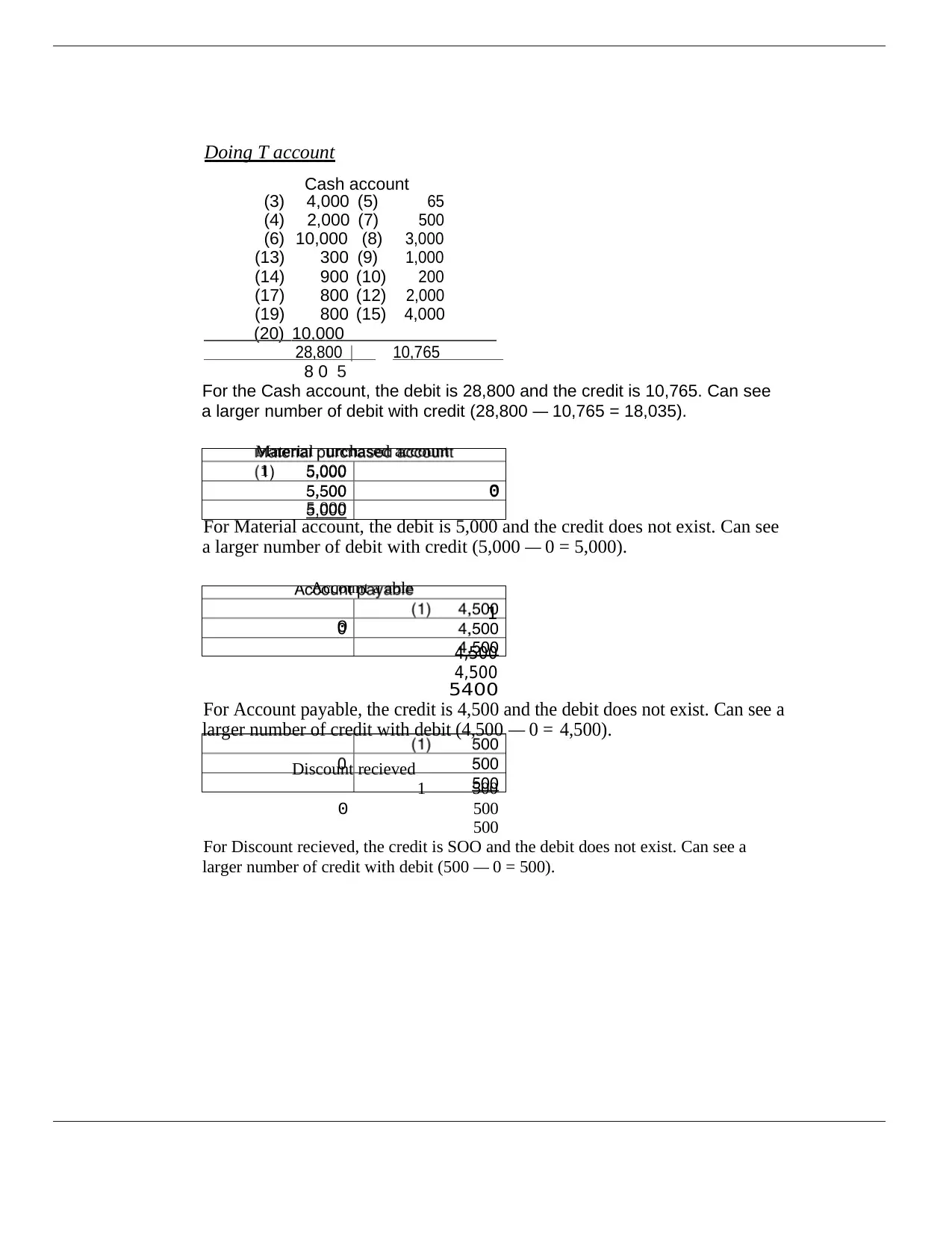

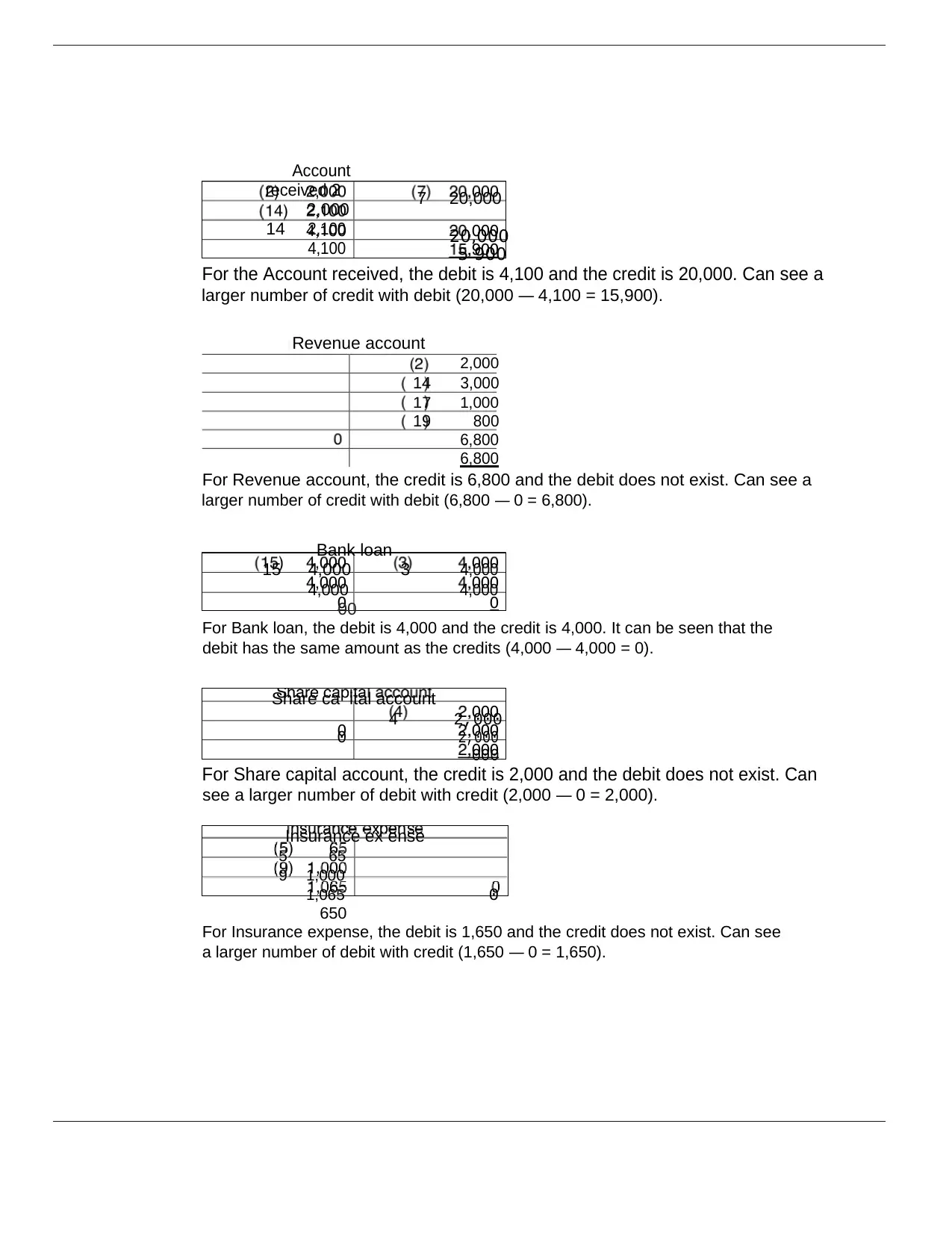

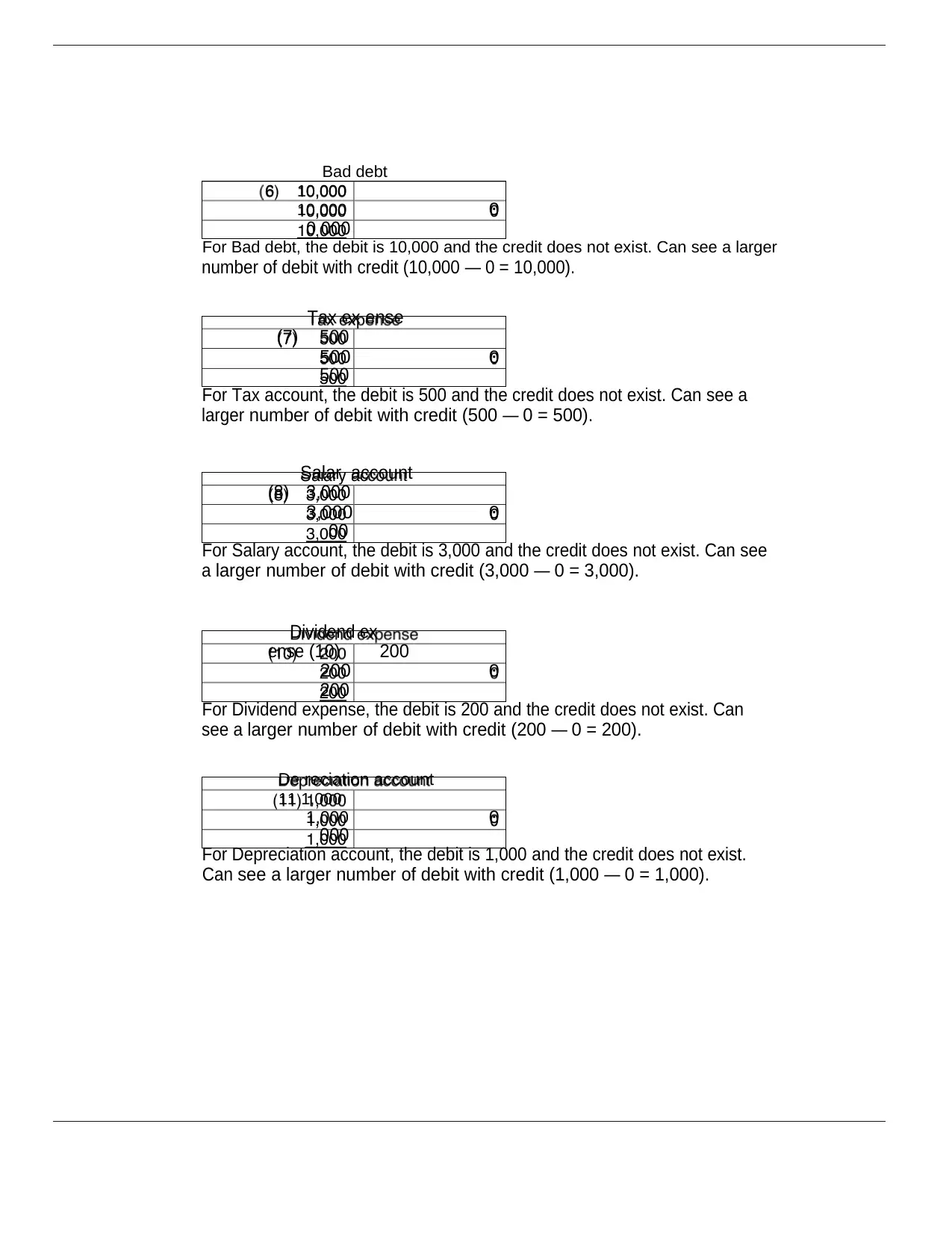

This assignment presents a comprehensive financial accounting solution for AC&DC Ltd. It begins with an explanation of the accounting cycle, detailing the steps from transactions and journal entries to the creation of financial statements. The solution includes a detailed journal, T-accounts, and a trial balance, showcasing the application of accounting principles. The assignment covers various transactions, including material purchases, revenue, expenses, and depreciation, illustrating how these are recorded and summarized. It also provides calculations for depreciation using both the straight-line and double-declining balance methods. Furthermore, the solution constructs an income statement and a balance sheet, providing a clear overview of AC&DC Ltd.'s financial performance and position. The document serves as a valuable resource for understanding financial accounting practices and the preparation of key financial reports.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.