BAP53 Corporate Finance: Discount Rental Car Project Analysis

VerifiedAdded on 2023/04/21

|6

|964

|60

Project

AI Summary

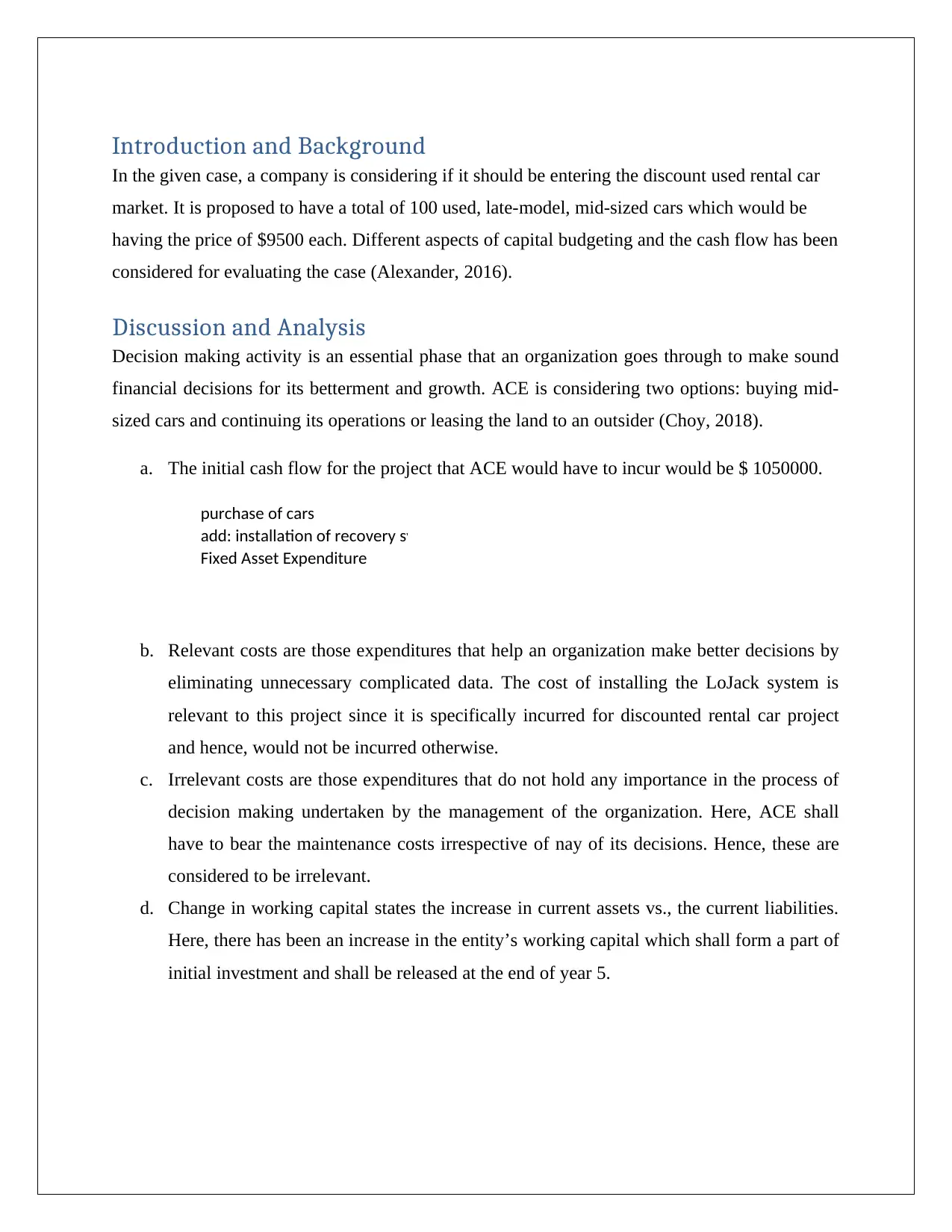

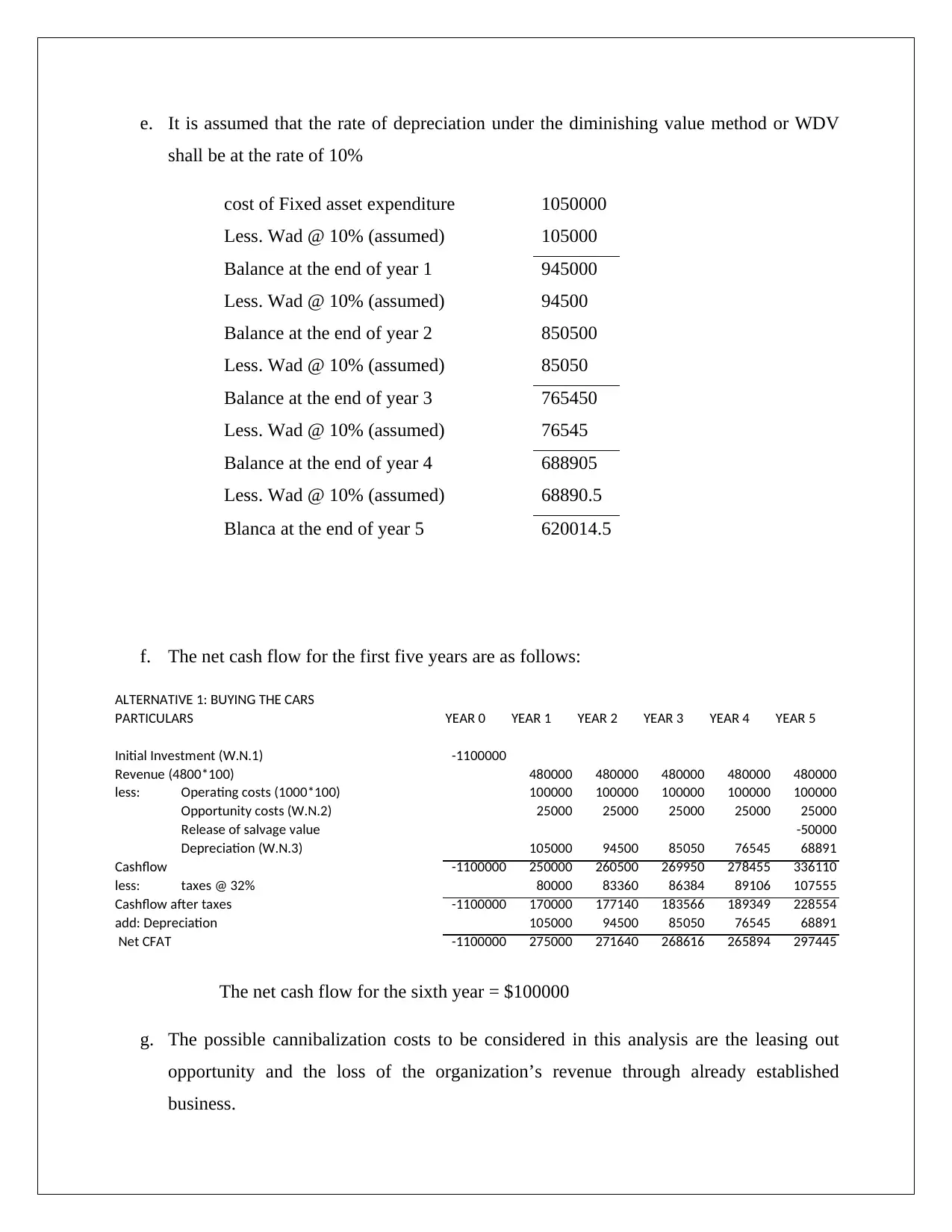

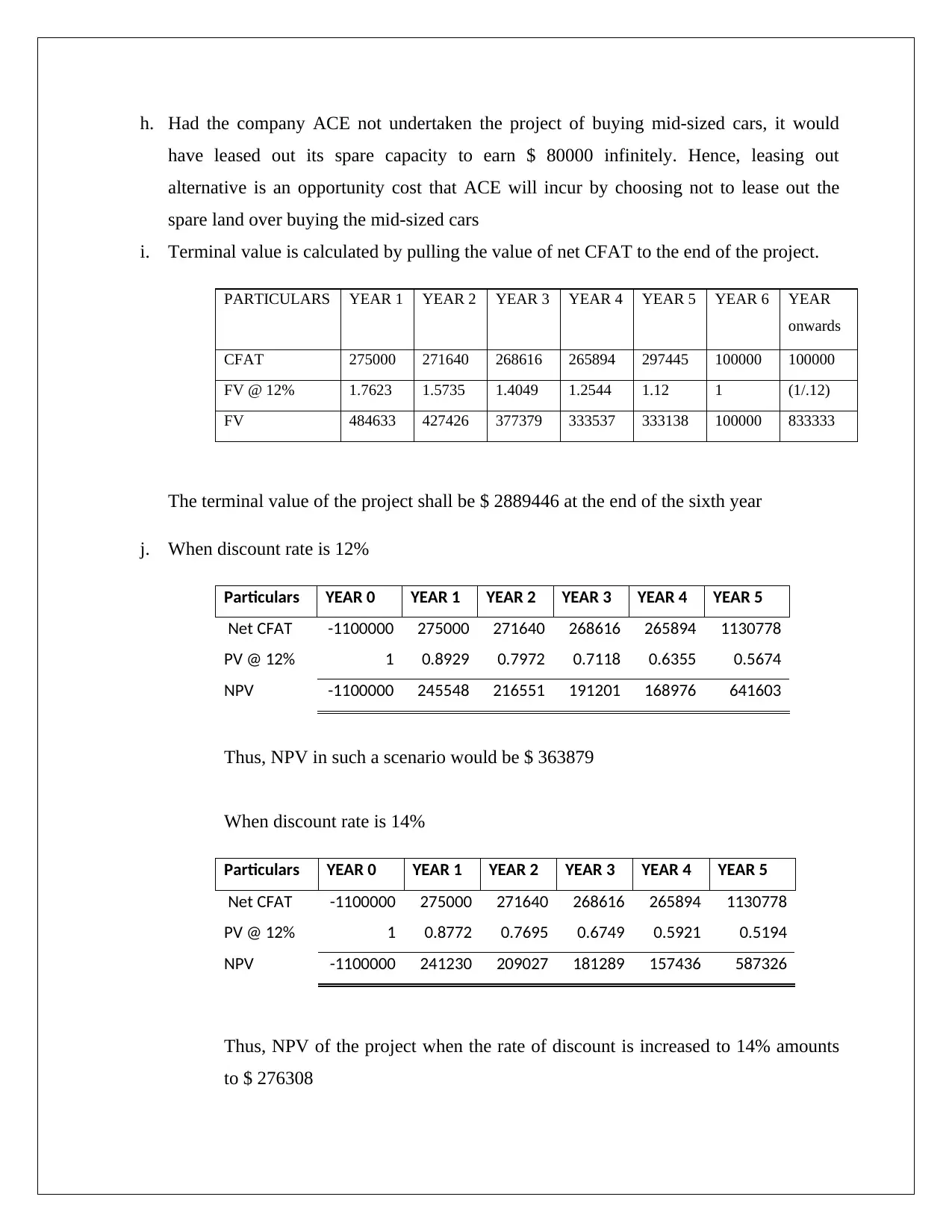

This assignment analyzes a corporate finance case study where Aus Car Exes (ACE) considers entering the discount used rental car market. The analysis includes the evaluation of initial cash flow, relevant and irrelevant costs, depreciation calculations using the diminishing value method, and net cash flow for five years. The assignment also addresses opportunity costs, terminal value calculations, and the impact of different discount rates (12% and 14%) on the project's net present value (NPV). The solution assesses the financial viability of the project, considering factors such as the purchase of cars, installation of recovery systems, revenue projections, operating costs, and tax implications. The assignment concludes with a comparison of NPV under different discount rates, providing insights into the project's potential profitability and financial decision-making.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.