ACFI 2208 - Performance Measurement in Organisations: Age UK

VerifiedAdded on 2023/06/09

|11

|2196

|114

Report

AI Summary

This report provides an analysis of Age UK's performance measurement within the context of sustainability accounting. It evaluates the financial performance of Age UK using ratio analysis, examining donor dependency, income utilization, and fundraising efficiency based on 2016 and 2017 financial data. The report also assesses non-financial performance by identifying and analyzing key performance indicators (KPIs) related to Age UK's social sustainability efforts, including donor growth rate, fundraising ROI, volunteer rates, outreach, advocacy, and risk management and governance. The analysis concludes that Age UK demonstrates adequate financial performance and effectively raises funds, while also employing relevant KPIs to gauge social performance.

Performance Measurement in Organisations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The present report is developed for gaining an analysis of the performance measurement

of non-profit organizations in the context of sustainability accounting and reporting. In this

context, the performance of a NGO, that is, Age UK, one of the largest charity of the UK

working for the welfare of old people is analyzed in the report. The financial performance of Age

UK is analyzed with the use of ratio evaluation by examining the financial results of the year

2016 and 2017 such as donor dependency, income utilization, raising donations and others. In

addition to this, the non-financial performance is analyzed by identification and examination of

the KPI’s of Age UK that helps in depicting their performance in the social area of sustainability.

Performance Measurement

Ratio Analysis of the AGE UK

Ratio analysis refers to the quantitative analysis of the financial information that is

presented in the financial statements. It is done to define the various kinds of relationship

between the financial items. In this section of the report, ratio analyse has been made of AGE

UK for year 2016 and 2017. As AGE UK is the Not for profit organization there is need to use

some specific ratios that helps make proper evaluation of performance measurement of this

organization. Detailed ratio analysis of AGE UK has been provided below:

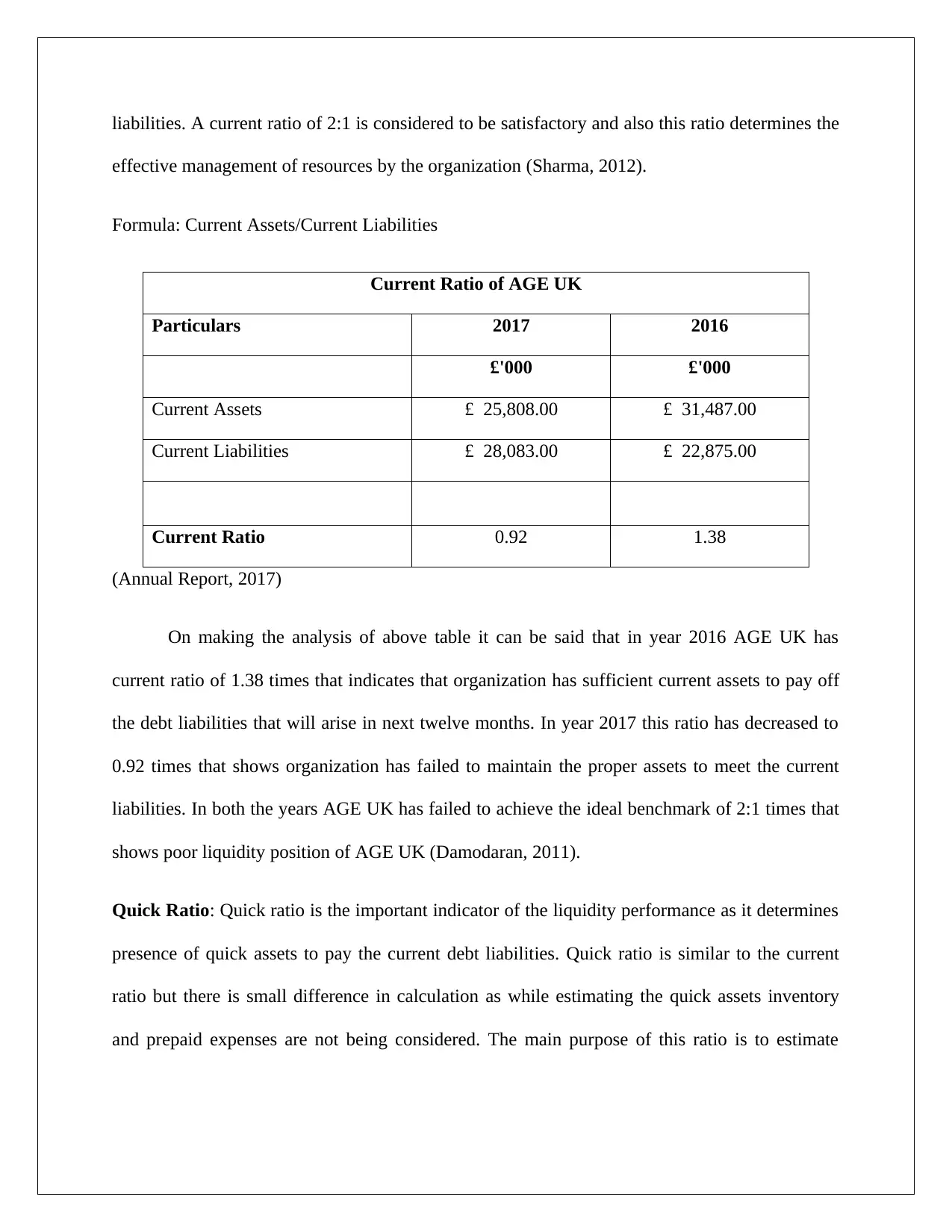

Current Ratio: This ratio is calculated to determine the ability of company to pay the short term

liabilities through use of current assets. Generally this ratio is used in profit making companies

but NPO uses this ratio to have knowledge that there are sufficient funds to pay off its immediate

debts that arises within 12 months. This ratio is calculated as current assets divided by current

The present report is developed for gaining an analysis of the performance measurement

of non-profit organizations in the context of sustainability accounting and reporting. In this

context, the performance of a NGO, that is, Age UK, one of the largest charity of the UK

working for the welfare of old people is analyzed in the report. The financial performance of Age

UK is analyzed with the use of ratio evaluation by examining the financial results of the year

2016 and 2017 such as donor dependency, income utilization, raising donations and others. In

addition to this, the non-financial performance is analyzed by identification and examination of

the KPI’s of Age UK that helps in depicting their performance in the social area of sustainability.

Performance Measurement

Ratio Analysis of the AGE UK

Ratio analysis refers to the quantitative analysis of the financial information that is

presented in the financial statements. It is done to define the various kinds of relationship

between the financial items. In this section of the report, ratio analyse has been made of AGE

UK for year 2016 and 2017. As AGE UK is the Not for profit organization there is need to use

some specific ratios that helps make proper evaluation of performance measurement of this

organization. Detailed ratio analysis of AGE UK has been provided below:

Current Ratio: This ratio is calculated to determine the ability of company to pay the short term

liabilities through use of current assets. Generally this ratio is used in profit making companies

but NPO uses this ratio to have knowledge that there are sufficient funds to pay off its immediate

debts that arises within 12 months. This ratio is calculated as current assets divided by current

liabilities. A current ratio of 2:1 is considered to be satisfactory and also this ratio determines the

effective management of resources by the organization (Sharma, 2012).

Formula: Current Assets/Current Liabilities

Current Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Current Assets £ 25,808.00 £ 31,487.00

Current Liabilities £ 28,083.00 £ 22,875.00

Current Ratio 0.92 1.38

(Annual Report, 2017)

On making the analysis of above table it can be said that in year 2016 AGE UK has

current ratio of 1.38 times that indicates that organization has sufficient current assets to pay off

the debt liabilities that will arise in next twelve months. In year 2017 this ratio has decreased to

0.92 times that shows organization has failed to maintain the proper assets to meet the current

liabilities. In both the years AGE UK has failed to achieve the ideal benchmark of 2:1 times that

shows poor liquidity position of AGE UK (Damodaran, 2011).

Quick Ratio: Quick ratio is the important indicator of the liquidity performance as it determines

presence of quick assets to pay the current debt liabilities. Quick ratio is similar to the current

ratio but there is small difference in calculation as while estimating the quick assets inventory

and prepaid expenses are not being considered. The main purpose of this ratio is to estimate

effective management of resources by the organization (Sharma, 2012).

Formula: Current Assets/Current Liabilities

Current Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Current Assets £ 25,808.00 £ 31,487.00

Current Liabilities £ 28,083.00 £ 22,875.00

Current Ratio 0.92 1.38

(Annual Report, 2017)

On making the analysis of above table it can be said that in year 2016 AGE UK has

current ratio of 1.38 times that indicates that organization has sufficient current assets to pay off

the debt liabilities that will arise in next twelve months. In year 2017 this ratio has decreased to

0.92 times that shows organization has failed to maintain the proper assets to meet the current

liabilities. In both the years AGE UK has failed to achieve the ideal benchmark of 2:1 times that

shows poor liquidity position of AGE UK (Damodaran, 2011).

Quick Ratio: Quick ratio is the important indicator of the liquidity performance as it determines

presence of quick assets to pay the current debt liabilities. Quick ratio is similar to the current

ratio but there is small difference in calculation as while estimating the quick assets inventory

and prepaid expenses are not being considered. The main purpose of this ratio is to estimate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

availability of most liquidated assets to finance the debt liabilities. The formula of quick ratio is

quick assets divided by current liabilities.

Formula: Quick Assets/Current Liabilities

Quick Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Current Assets £ 25,808.00 £ 31,487.00

Stock £ 566.00 £ 534.00

Quick Assets £ 25,242.00 £ 30,953.00

Current Liabilities £ 28,083.00 £ 22,875.00

Quick Ratio 0.90 1.35

(Annual Report, 2017)

Quick ratio of AGE UK was 1.35 times in year 2016 and it was decreased to 0.90 times

in year 2017 that indicates poor liquidity performance organization in year 2017.

Debt Ratio (Pension Included): Debt ratio is important leverage ratio that it indicates

percentage of assets used to pay all the liabilities that has been reported in balance sheet. It is

calculated as total liabilities divided by the total assets (Sharma, 2012).

Formula: Total Liabilities/Total Assets

Debt Ratio of AGE UK

Particulars 2017 2016

quick assets divided by current liabilities.

Formula: Quick Assets/Current Liabilities

Quick Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Current Assets £ 25,808.00 £ 31,487.00

Stock £ 566.00 £ 534.00

Quick Assets £ 25,242.00 £ 30,953.00

Current Liabilities £ 28,083.00 £ 22,875.00

Quick Ratio 0.90 1.35

(Annual Report, 2017)

Quick ratio of AGE UK was 1.35 times in year 2016 and it was decreased to 0.90 times

in year 2017 that indicates poor liquidity performance organization in year 2017.

Debt Ratio (Pension Included): Debt ratio is important leverage ratio that it indicates

percentage of assets used to pay all the liabilities that has been reported in balance sheet. It is

calculated as total liabilities divided by the total assets (Sharma, 2012).

Formula: Total Liabilities/Total Assets

Debt Ratio of AGE UK

Particulars 2017 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£'000 £'000

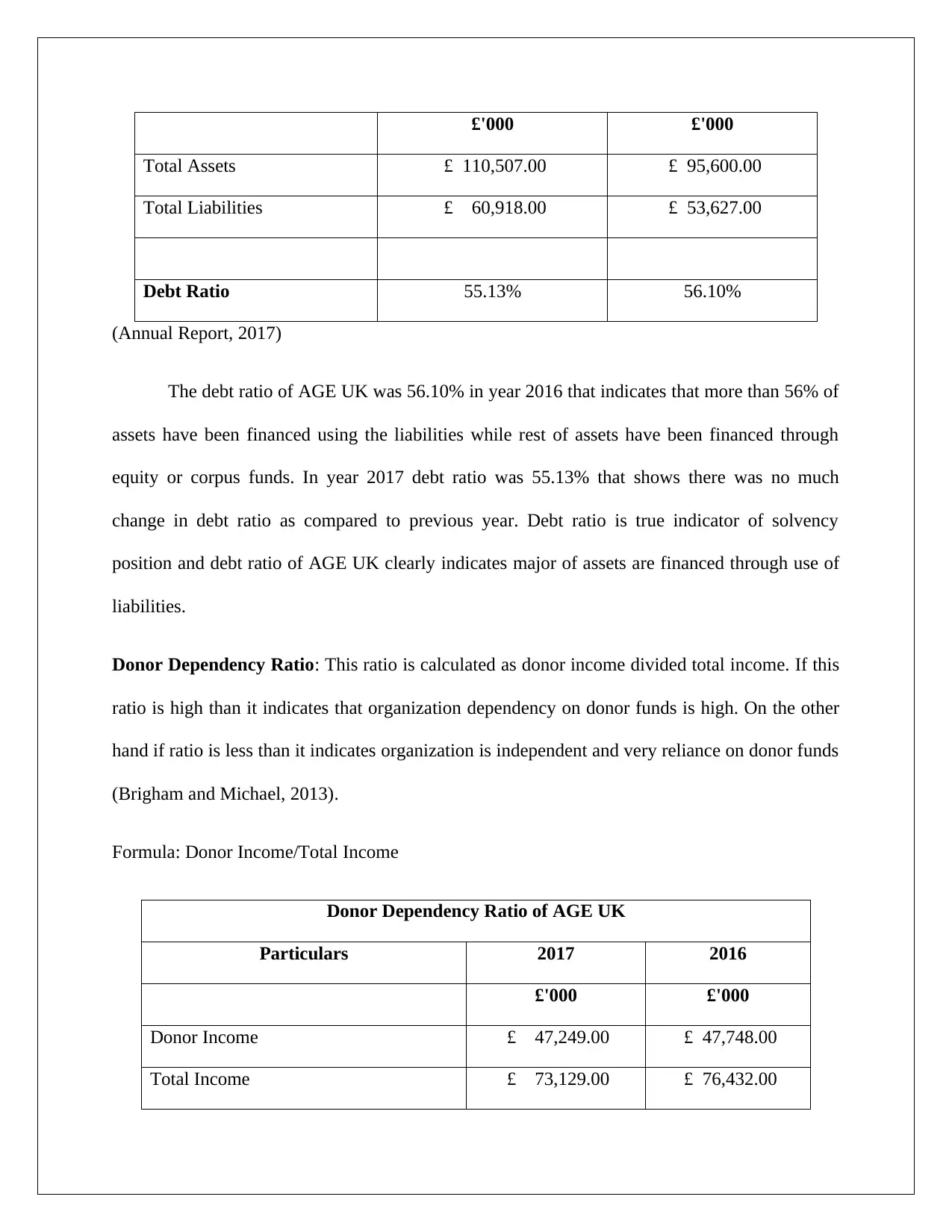

Total Assets £ 110,507.00 £ 95,600.00

Total Liabilities £ 60,918.00 £ 53,627.00

Debt Ratio 55.13% 56.10%

(Annual Report, 2017)

The debt ratio of AGE UK was 56.10% in year 2016 that indicates that more than 56% of

assets have been financed using the liabilities while rest of assets have been financed through

equity or corpus funds. In year 2017 debt ratio was 55.13% that shows there was no much

change in debt ratio as compared to previous year. Debt ratio is true indicator of solvency

position and debt ratio of AGE UK clearly indicates major of assets are financed through use of

liabilities.

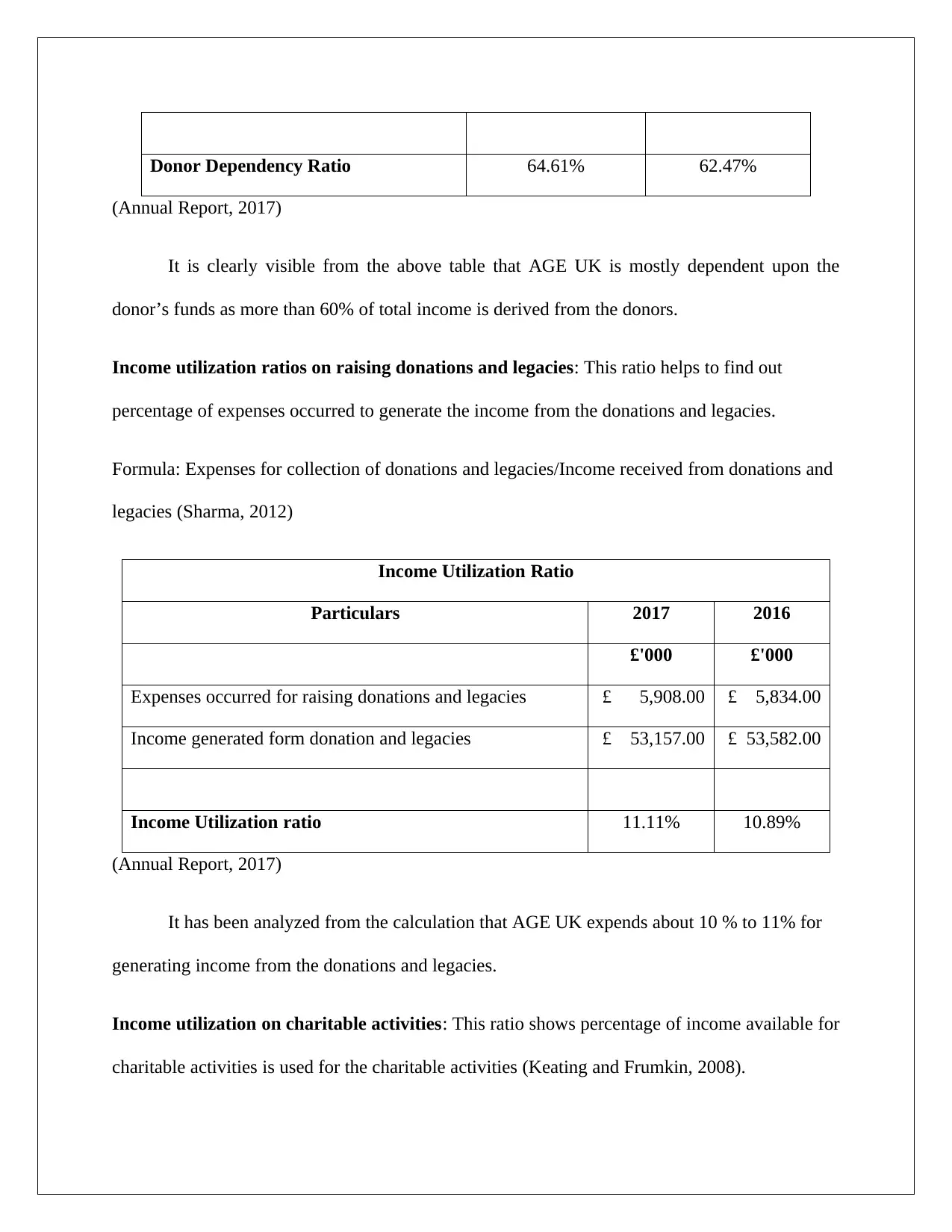

Donor Dependency Ratio: This ratio is calculated as donor income divided total income. If this

ratio is high than it indicates that organization dependency on donor funds is high. On the other

hand if ratio is less than it indicates organization is independent and very reliance on donor funds

(Brigham and Michael, 2013).

Formula: Donor Income/Total Income

Donor Dependency Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Donor Income £ 47,249.00 £ 47,748.00

Total Income £ 73,129.00 £ 76,432.00

Total Assets £ 110,507.00 £ 95,600.00

Total Liabilities £ 60,918.00 £ 53,627.00

Debt Ratio 55.13% 56.10%

(Annual Report, 2017)

The debt ratio of AGE UK was 56.10% in year 2016 that indicates that more than 56% of

assets have been financed using the liabilities while rest of assets have been financed through

equity or corpus funds. In year 2017 debt ratio was 55.13% that shows there was no much

change in debt ratio as compared to previous year. Debt ratio is true indicator of solvency

position and debt ratio of AGE UK clearly indicates major of assets are financed through use of

liabilities.

Donor Dependency Ratio: This ratio is calculated as donor income divided total income. If this

ratio is high than it indicates that organization dependency on donor funds is high. On the other

hand if ratio is less than it indicates organization is independent and very reliance on donor funds

(Brigham and Michael, 2013).

Formula: Donor Income/Total Income

Donor Dependency Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

Donor Income £ 47,249.00 £ 47,748.00

Total Income £ 73,129.00 £ 76,432.00

Donor Dependency Ratio 64.61% 62.47%

(Annual Report, 2017)

It is clearly visible from the above table that AGE UK is mostly dependent upon the

donor’s funds as more than 60% of total income is derived from the donors.

Income utilization ratios on raising donations and legacies: This ratio helps to find out

percentage of expenses occurred to generate the income from the donations and legacies.

Formula: Expenses for collection of donations and legacies/Income received from donations and

legacies (Sharma, 2012)

Income Utilization Ratio

Particulars 2017 2016

£'000 £'000

Expenses occurred for raising donations and legacies £ 5,908.00 £ 5,834.00

Income generated form donation and legacies £ 53,157.00 £ 53,582.00

Income Utilization ratio 11.11% 10.89%

(Annual Report, 2017)

It has been analyzed from the calculation that AGE UK expends about 10 % to 11% for

generating income from the donations and legacies.

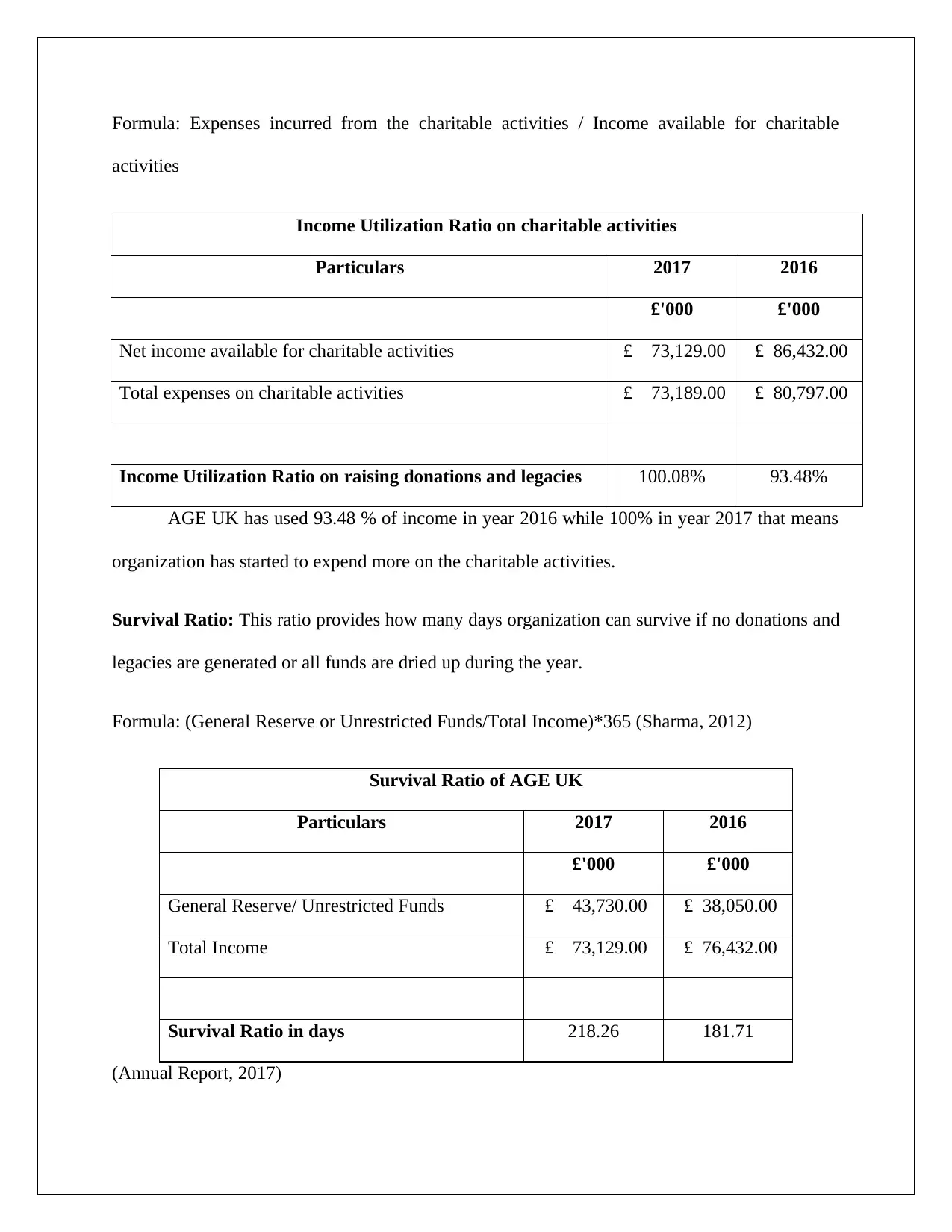

Income utilization on charitable activities: This ratio shows percentage of income available for

charitable activities is used for the charitable activities (Keating and Frumkin, 2008).

(Annual Report, 2017)

It is clearly visible from the above table that AGE UK is mostly dependent upon the

donor’s funds as more than 60% of total income is derived from the donors.

Income utilization ratios on raising donations and legacies: This ratio helps to find out

percentage of expenses occurred to generate the income from the donations and legacies.

Formula: Expenses for collection of donations and legacies/Income received from donations and

legacies (Sharma, 2012)

Income Utilization Ratio

Particulars 2017 2016

£'000 £'000

Expenses occurred for raising donations and legacies £ 5,908.00 £ 5,834.00

Income generated form donation and legacies £ 53,157.00 £ 53,582.00

Income Utilization ratio 11.11% 10.89%

(Annual Report, 2017)

It has been analyzed from the calculation that AGE UK expends about 10 % to 11% for

generating income from the donations and legacies.

Income utilization on charitable activities: This ratio shows percentage of income available for

charitable activities is used for the charitable activities (Keating and Frumkin, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formula: Expenses incurred from the charitable activities / Income available for charitable

activities

Income Utilization Ratio on charitable activities

Particulars 2017 2016

£'000 £'000

Net income available for charitable activities £ 73,129.00 £ 86,432.00

Total expenses on charitable activities £ 73,189.00 £ 80,797.00

Income Utilization Ratio on raising donations and legacies 100.08% 93.48%

AGE UK has used 93.48 % of income in year 2016 while 100% in year 2017 that means

organization has started to expend more on the charitable activities.

Survival Ratio: This ratio provides how many days organization can survive if no donations and

legacies are generated or all funds are dried up during the year.

Formula: (General Reserve or Unrestricted Funds/Total Income)*365 (Sharma, 2012)

Survival Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

General Reserve/ Unrestricted Funds £ 43,730.00 £ 38,050.00

Total Income £ 73,129.00 £ 76,432.00

Survival Ratio in days 218.26 181.71

(Annual Report, 2017)

activities

Income Utilization Ratio on charitable activities

Particulars 2017 2016

£'000 £'000

Net income available for charitable activities £ 73,129.00 £ 86,432.00

Total expenses on charitable activities £ 73,189.00 £ 80,797.00

Income Utilization Ratio on raising donations and legacies 100.08% 93.48%

AGE UK has used 93.48 % of income in year 2016 while 100% in year 2017 that means

organization has started to expend more on the charitable activities.

Survival Ratio: This ratio provides how many days organization can survive if no donations and

legacies are generated or all funds are dried up during the year.

Formula: (General Reserve or Unrestricted Funds/Total Income)*365 (Sharma, 2012)

Survival Ratio of AGE UK

Particulars 2017 2016

£'000 £'000

General Reserve/ Unrestricted Funds £ 43,730.00 £ 38,050.00

Total Income £ 73,129.00 £ 76,432.00

Survival Ratio in days 218.26 181.71

(Annual Report, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per the ratio organization can survive for 218 days in year 2017 if no funds will be

generated during the year.

Non Performance Measurement

Theoretical discussion about social sustainability

Social sustainability can be defined as identification and managing the business impacts,

that is, positive and negative, on people successfully. Businesses need to develop the process and

structures efficiently so that they are able to meet the varying needs and requirements of

communities at present and also in future generations. It involves gaining an in-depth

understanding of the impact of business corporations on society at large. The business practices

and procedures should be developed in a way so that they are able to produce maximum impact

on the society and minimizing its negative effects. The business can improve their social

sustainability performance by integrating a social perspective into their governance, systems,

processes, practices and operations. The social performance can be enhanced by maintaining

positive relations with employees, community and customers.

Social sustainability performance can be improved by businesses through maximizing its

economic and environmental performance. Environmental sustainability involves reducing the

business activities that negatively impacts the environment and thus maximizing the societal

growth. On the other hand, the economic performance involves maximizing its profitability

through adoption of adequate governance and risk management policies. The increasing

profitability of business will help in promoting social performance by producing maximizing

profits for the communities (Carbo, 2017).

Analysis of the social sustainability KPIs of the charity

generated during the year.

Non Performance Measurement

Theoretical discussion about social sustainability

Social sustainability can be defined as identification and managing the business impacts,

that is, positive and negative, on people successfully. Businesses need to develop the process and

structures efficiently so that they are able to meet the varying needs and requirements of

communities at present and also in future generations. It involves gaining an in-depth

understanding of the impact of business corporations on society at large. The business practices

and procedures should be developed in a way so that they are able to produce maximum impact

on the society and minimizing its negative effects. The business can improve their social

sustainability performance by integrating a social perspective into their governance, systems,

processes, practices and operations. The social performance can be enhanced by maintaining

positive relations with employees, community and customers.

Social sustainability performance can be improved by businesses through maximizing its

economic and environmental performance. Environmental sustainability involves reducing the

business activities that negatively impacts the environment and thus maximizing the societal

growth. On the other hand, the economic performance involves maximizing its profitability

through adoption of adequate governance and risk management policies. The increasing

profitability of business will help in promoting social performance by producing maximizing

profits for the communities (Carbo, 2017).

Analysis of the social sustainability KPIs of the charity

KPI’s (Key Performance Indicator) can be regarded as quantifiable measures that are

used for evaluating the success of a business organization. The non-profit organizations such as

Age UK places emphasize on measuring revenue and donation metrics while developing the

KPI’s. The KPI’s of Age UK are identified and analyzed as follows:

Growth rate of Donor: The rate of growth of donor as a KPI of the NGO to gain an

analysis of the funds donated by the donors to the organization. The financial reports of

the NGO provide a measurement of the donation rate by comparing the present year

donation figure with that of the previous year. This will help in developing an analysis of

the trust and confidence developed by the NGO among the society.

Returns Realized from Raising Funds: Measuring ROI (Return on Investment) of all the

resources that are used in raising funds is also an effective KPI of the NGO. It involves

taking into account the time incurred on raising funds, developing mission and marketing

strategies for gaining charities. The greater the ROI the larger is the charity realized by

the NGO for promoting social welfare.

Rate of Volunteer: The KPI helps in measuring the number of volunteers the NGO has

used for raising funds. Volunteers play an important role in promoting the growth and

development of the NGO by ensuring that its services are effectively implemented

(Annual Report, 2017).

Outreach and Advocacy: This KPI helps in providing a measurement of the community

events that are organized by the NGO. Also, it provides a measurement of the training

providing to the advocates and the attendance rates of people within the community

events organized by NGO.

used for evaluating the success of a business organization. The non-profit organizations such as

Age UK places emphasize on measuring revenue and donation metrics while developing the

KPI’s. The KPI’s of Age UK are identified and analyzed as follows:

Growth rate of Donor: The rate of growth of donor as a KPI of the NGO to gain an

analysis of the funds donated by the donors to the organization. The financial reports of

the NGO provide a measurement of the donation rate by comparing the present year

donation figure with that of the previous year. This will help in developing an analysis of

the trust and confidence developed by the NGO among the society.

Returns Realized from Raising Funds: Measuring ROI (Return on Investment) of all the

resources that are used in raising funds is also an effective KPI of the NGO. It involves

taking into account the time incurred on raising funds, developing mission and marketing

strategies for gaining charities. The greater the ROI the larger is the charity realized by

the NGO for promoting social welfare.

Rate of Volunteer: The KPI helps in measuring the number of volunteers the NGO has

used for raising funds. Volunteers play an important role in promoting the growth and

development of the NGO by ensuring that its services are effectively implemented

(Annual Report, 2017).

Outreach and Advocacy: This KPI helps in providing a measurement of the community

events that are organized by the NGO. Also, it provides a measurement of the training

providing to the advocates and the attendance rates of people within the community

events organized by NGO.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk Management & Governance: The proper implementation of the risk management

and governance system is necessary for the continuing growth and development of a

NGO. It can be measured by assessing the programs used for mitigation of the emergency

conditions and effectiveness of the governance policies so that all the internal activities

are carried out in an efficient manner and the charity realized is used for societal welfare

(Epstein and Yuthas, 2017).

Conclusion

The report has concluded that Age UK financial performance is adequate and it is able to

effectively raise funds for promoting the growth and development of old age people as indicated

from the results of different ratio’s. Also, its non-financial performance has indicated that the

non-profit organization has developed effective KPI’s for gaining an analysis of its social

performance.

and governance system is necessary for the continuing growth and development of a

NGO. It can be measured by assessing the programs used for mitigation of the emergency

conditions and effectiveness of the governance policies so that all the internal activities

are carried out in an efficient manner and the charity realized is used for societal welfare

(Epstein and Yuthas, 2017).

Conclusion

The report has concluded that Age UK financial performance is adequate and it is able to

effectively raise funds for promoting the growth and development of old age people as indicated

from the results of different ratio’s. Also, its non-financial performance has indicated that the

non-profit organization has developed effective KPI’s for gaining an analysis of its social

performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

About AGE UK. 2018. [Online]. Available at: https://www.ageuk.org.uk/about-us/what-we-do/

[Accessed on: 14 August 2018].

Annual Report 2017. AGE UK. [Online]. Available at:

https://www.ageuk.org.uk/globalassets/age-uk/documents/annual-reports-and-reviews/

report_of_trustees_and_annual_accounts_2016_2017.pdf [Accessed on: 14 August 2018].

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Cengage

Learning.

Carbo, J. 2017. Social Sustainability for Business. Routledge.

Damodaran, A, 2011. Applied corporate finance. John Wiley & sons.

Epstein, M. and Yuthas, K. 2017. Measuring and Improving Social Impacts: A Guide for

Nonprofits, Companies and Impact Investors. Routledge.

Keating, E.K. and Frumkin, P. 2008. How to Assess Nonprofit Financial Performance. [Online].

Available at: https://nasaa-arts.org/wp-content/uploads/2017/03/Reading-5-Understanding-

Financial-Statements.pdf [Accessed on: 14 August 2018].

Sharma. P. 2012. Performance Measurement in NGOs. [Online]. Available at:

https://browneandmohan.files.wordpress.com/2012/12/pratibha-sharma-journal.pdf [Accessed

on: 14 August 2018].

About AGE UK. 2018. [Online]. Available at: https://www.ageuk.org.uk/about-us/what-we-do/

[Accessed on: 14 August 2018].

Annual Report 2017. AGE UK. [Online]. Available at:

https://www.ageuk.org.uk/globalassets/age-uk/documents/annual-reports-and-reviews/

report_of_trustees_and_annual_accounts_2016_2017.pdf [Accessed on: 14 August 2018].

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Cengage

Learning.

Carbo, J. 2017. Social Sustainability for Business. Routledge.

Damodaran, A, 2011. Applied corporate finance. John Wiley & sons.

Epstein, M. and Yuthas, K. 2017. Measuring and Improving Social Impacts: A Guide for

Nonprofits, Companies and Impact Investors. Routledge.

Keating, E.K. and Frumkin, P. 2008. How to Assess Nonprofit Financial Performance. [Online].

Available at: https://nasaa-arts.org/wp-content/uploads/2017/03/Reading-5-Understanding-

Financial-Statements.pdf [Accessed on: 14 August 2018].

Sharma. P. 2012. Performance Measurement in NGOs. [Online]. Available at:

https://browneandmohan.files.wordpress.com/2012/12/pratibha-sharma-journal.pdf [Accessed

on: 14 August 2018].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.