ACT303 - Principles of Auditing: Ethical Dilemmas and Control Weakness

VerifiedAdded on 2023/06/14

|18

|3965

|500

Case Study

AI Summary

This case study delves into various aspects of auditing principles, focusing on ethical considerations and internal control deficiencies within different business scenarios. It addresses issues such as toxic waste disposal, hedging transaction errors, limitations in audit evidence, and threats to auditor independence. The analysis covers the importance of ethical conduct, robust internal controls, and adherence to auditing standards. Furthermore, it examines specific control deficiencies related to website ordering, courier services, sales order processing, credit and discount policies, and supplier statement reconciliation, providing recommendations for improvement. The study also identifies potential areas of material misstatement in asset accounts like cash balance and inventory, emphasizing the need for accurate financial reporting. Desklib offers a wide array of similar solved assignments and resources for students.

Running head: PRINCIPLES OF AUDITING

Principles of Auditing

Name of the Student:

Name of the University:

Author’s Note:

Principles of Auditing

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

PRINCIPLES OF AUDITING

Table of Contents

Part A...............................................................................................................................................2

Part A-1........................................................................................................................................2

Part A-2........................................................................................................................................2

Part A-3........................................................................................................................................3

Part A-4........................................................................................................................................3

Part B...............................................................................................................................................5

Part C.............................................................................................................................................10

Part C-1......................................................................................................................................10

Part C-2......................................................................................................................................12

Part D.............................................................................................................................................13

Reference.......................................................................................................................................16

PRINCIPLES OF AUDITING

Table of Contents

Part A...............................................................................................................................................2

Part A-1........................................................................................................................................2

Part A-2........................................................................................................................................2

Part A-3........................................................................................................................................3

Part A-4........................................................................................................................................3

Part B...............................................................................................................................................5

Part C.............................................................................................................................................10

Part C-1......................................................................................................................................10

Part C-2......................................................................................................................................12

Part D.............................................................................................................................................13

Reference.......................................................................................................................................16

2

PRINCIPLES OF AUDITING

Part A

Part A-1

As per the case study provided in the question, Pharmaceutical ltd is engaged in business

of chemical manufacturing. The ethical issues which the business is facing is regarding the

disposal of toxic wastes of the company. The company is under investigation for a spill of toxic

waste in a nearby river. The senior level employees of the business are trying to conceal the

matter.

As per Environmental Protection Agency (EPA), no organization is allowed to dispose

toxic wastes or chemical wastes in water sources as per the regulation of Water Management Act

(Powell 2014). The ethical consideration is that the company is trying to actively cover the spill

of hazardous waste in water source which could have serious environmental impacts and also

affect the health of humans. Such ethical factors and the case must be considered by the auditor

before accepting the engagement (Pitt 2014).

Part A-2

As per the case study provided, Pharmaceuticals ltd is engaged in the business of

importing pharmaceutical products from foreign countries. in order to cope up with the

fluctuation in prices of foreign currencies the company has engaged in hedging techniques.

However there exists certain errors in accounting for the hedge transactions.

The auditor needs to suggest to the management to develop a strong internal control for

the business so that the errors and mistakes can be avoided. The management needs to review the

transactions which are recorded for hedge transactions so that errors which occurs due to

inexperience or weak internal control can be avoided (Johnston et al. 2014).

PRINCIPLES OF AUDITING

Part A

Part A-1

As per the case study provided in the question, Pharmaceutical ltd is engaged in business

of chemical manufacturing. The ethical issues which the business is facing is regarding the

disposal of toxic wastes of the company. The company is under investigation for a spill of toxic

waste in a nearby river. The senior level employees of the business are trying to conceal the

matter.

As per Environmental Protection Agency (EPA), no organization is allowed to dispose

toxic wastes or chemical wastes in water sources as per the regulation of Water Management Act

(Powell 2014). The ethical consideration is that the company is trying to actively cover the spill

of hazardous waste in water source which could have serious environmental impacts and also

affect the health of humans. Such ethical factors and the case must be considered by the auditor

before accepting the engagement (Pitt 2014).

Part A-2

As per the case study provided, Pharmaceuticals ltd is engaged in the business of

importing pharmaceutical products from foreign countries. in order to cope up with the

fluctuation in prices of foreign currencies the company has engaged in hedging techniques.

However there exists certain errors in accounting for the hedge transactions.

The auditor needs to suggest to the management to develop a strong internal control for

the business so that the errors and mistakes can be avoided. The management needs to review the

transactions which are recorded for hedge transactions so that errors which occurs due to

inexperience or weak internal control can be avoided (Johnston et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

PRINCIPLES OF AUDITING

Part A-3

As per the case study, the auditor Billings and Associates are to conduct an audit for a

new manufacturer whose financial statements have never been audited before. The auditor is

unable to acquire any sufficient appropriate audit evidences for account receivables as there is no

documentations.

The provisions of ASA 705, which deals with Modification of Audit Opinion in an

independent auditor’s report. The standard states that the auditor must issues a modified audit

opinion when there is material misstatement in the financial statement and when the auditor is

unable to collect appropriate audit evidences due to limitation on the part of the management

(Carson, Fargher and Zhang 2016). As provided in the case, the auditor is having problem in

obtaining sufficient appropriate evidences for account receivable for which proper

documentation is not maintained by the business, therefore this can be taken as a limitation on

the part of management. The auditor can therefore issue a modified report and moreover, the

engagement was for the audit which was provided by the auditor prior to commencement of

business. Therefore, on the request the engagement cannot be changed on a review engagement

even if the company is not subjected to audit (Habib 2013).

Part A-4

1. As per the case provided, Hail Pty ltd is engaged has prepared the financial statements of

the company which has been approved by the auditor of the company. However, the

company admits that it might not have calculated the amount of impairment cost

(Paugam and Ramond 2015). As the company is asking the auditor as to how to record

the impairments accurately, the auditor is providing non-audit services to the client which

can be pose a threat to the principle of independence of the auditor.

PRINCIPLES OF AUDITING

Part A-3

As per the case study, the auditor Billings and Associates are to conduct an audit for a

new manufacturer whose financial statements have never been audited before. The auditor is

unable to acquire any sufficient appropriate audit evidences for account receivables as there is no

documentations.

The provisions of ASA 705, which deals with Modification of Audit Opinion in an

independent auditor’s report. The standard states that the auditor must issues a modified audit

opinion when there is material misstatement in the financial statement and when the auditor is

unable to collect appropriate audit evidences due to limitation on the part of the management

(Carson, Fargher and Zhang 2016). As provided in the case, the auditor is having problem in

obtaining sufficient appropriate evidences for account receivable for which proper

documentation is not maintained by the business, therefore this can be taken as a limitation on

the part of management. The auditor can therefore issue a modified report and moreover, the

engagement was for the audit which was provided by the auditor prior to commencement of

business. Therefore, on the request the engagement cannot be changed on a review engagement

even if the company is not subjected to audit (Habib 2013).

Part A-4

1. As per the case provided, Hail Pty ltd is engaged has prepared the financial statements of

the company which has been approved by the auditor of the company. However, the

company admits that it might not have calculated the amount of impairment cost

(Paugam and Ramond 2015). As the company is asking the auditor as to how to record

the impairments accurately, the auditor is providing non-audit services to the client which

can be pose a threat to the principle of independence of the auditor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PRINCIPLES OF AUDITING

The safeguards which can be suggested so that the independence principle is not violated

is that the auditor should not be providing non-audit services to the client business for which

the auditor is conducting audit.

2. In the given case, Time travel ltd provides travel services to its customers and also acts as

a travelling agent for the auditors of the company. In times of crisis the company has

asked the auditor to recommend the name of the business to other auditors. In the

situation the case reveals conflict of interest on the part of the auditor and this will be

affecting the independence of the auditor (Kouakou, Boiral and Gendron 2013).

The measure which can be suggested in order to protect the independence

principle of the auditor is that the auditor should not take services from the clients so that

no situation of conflict of interest takes place.

3. In the given case, the auditor has taken up an audit engagement for a new business. A

major part of the shareholdings is being hold by wife of the partner of the audit firm. The

basic threat which is associated with the audit of such a company is related to the

principle of member of the audit firms or the family members of the partners of the audit

firm are not allowed to hold shares or any financial interest in the client. The threat is

identified to affect the independence of the auditor of the company (Fiolleau et al. 2013).

In such a situation the audit firm’s partner should be allowed to conduct the audit

of the financial report of the business and the business also use the techniques of audit

firm rotations.

4. In the case given in the question the auditor of the company is facing a problem where

the company is unable to pay the fees of the auditor. This will be resulting in

overdependence of the auditor on the fees which is to be given by the client.

PRINCIPLES OF AUDITING

The safeguards which can be suggested so that the independence principle is not violated

is that the auditor should not be providing non-audit services to the client business for which

the auditor is conducting audit.

2. In the given case, Time travel ltd provides travel services to its customers and also acts as

a travelling agent for the auditors of the company. In times of crisis the company has

asked the auditor to recommend the name of the business to other auditors. In the

situation the case reveals conflict of interest on the part of the auditor and this will be

affecting the independence of the auditor (Kouakou, Boiral and Gendron 2013).

The measure which can be suggested in order to protect the independence

principle of the auditor is that the auditor should not take services from the clients so that

no situation of conflict of interest takes place.

3. In the given case, the auditor has taken up an audit engagement for a new business. A

major part of the shareholdings is being hold by wife of the partner of the audit firm. The

basic threat which is associated with the audit of such a company is related to the

principle of member of the audit firms or the family members of the partners of the audit

firm are not allowed to hold shares or any financial interest in the client. The threat is

identified to affect the independence of the auditor of the company (Fiolleau et al. 2013).

In such a situation the audit firm’s partner should be allowed to conduct the audit

of the financial report of the business and the business also use the techniques of audit

firm rotations.

4. In the case given in the question the auditor of the company is facing a problem where

the company is unable to pay the fees of the auditor. This will be resulting in

overdependence of the auditor on the fees which is to be given by the client.

5

PRINCIPLES OF AUDITING

Overdependence on the fees of the company might provoke the auditor to improve the

opinion of the financial reports which might be in the favor of the company which affects

the independence principle of the auditor

The measure which can be suggested to the auditor is that the auditor should

apply for the fees as soon as possible as the auditor’s report will not be issued unless the

audit fees are given by the company.

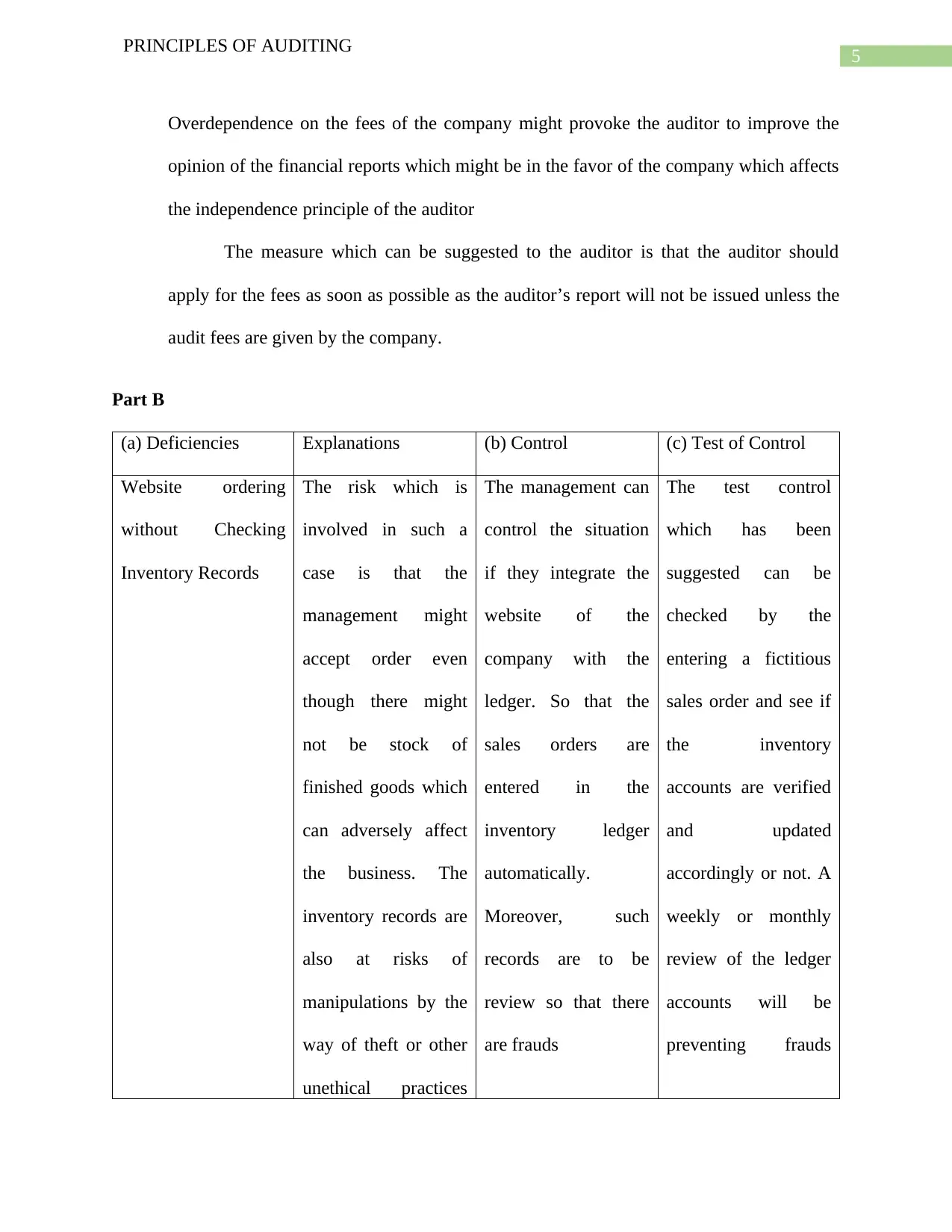

Part B

(a) Deficiencies Explanations (b) Control (c) Test of Control

Website ordering

without Checking

Inventory Records

The risk which is

involved in such a

case is that the

management might

accept order even

though there might

not be stock of

finished goods which

can adversely affect

the business. The

inventory records are

also at risks of

manipulations by the

way of theft or other

unethical practices

The management can

control the situation

if they integrate the

website of the

company with the

ledger. So that the

sales orders are

entered in the

inventory ledger

automatically.

Moreover, such

records are to be

review so that there

are frauds

The test control

which has been

suggested can be

checked by the

entering a fictitious

sales order and see if

the inventory

accounts are verified

and updated

accordingly or not. A

weekly or monthly

review of the ledger

accounts will be

preventing frauds

PRINCIPLES OF AUDITING

Overdependence on the fees of the company might provoke the auditor to improve the

opinion of the financial reports which might be in the favor of the company which affects

the independence principle of the auditor

The measure which can be suggested to the auditor is that the auditor should

apply for the fees as soon as possible as the auditor’s report will not be issued unless the

audit fees are given by the company.

Part B

(a) Deficiencies Explanations (b) Control (c) Test of Control

Website ordering

without Checking

Inventory Records

The risk which is

involved in such a

case is that the

management might

accept order even

though there might

not be stock of

finished goods which

can adversely affect

the business. The

inventory records are

also at risks of

manipulations by the

way of theft or other

unethical practices

The management can

control the situation

if they integrate the

website of the

company with the

ledger. So that the

sales orders are

entered in the

inventory ledger

automatically.

Moreover, such

records are to be

review so that there

are frauds

The test control

which has been

suggested can be

checked by the

entering a fictitious

sales order and see if

the inventory

accounts are verified

and updated

accordingly or not. A

weekly or monthly

review of the ledger

accounts will be

preventing frauds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

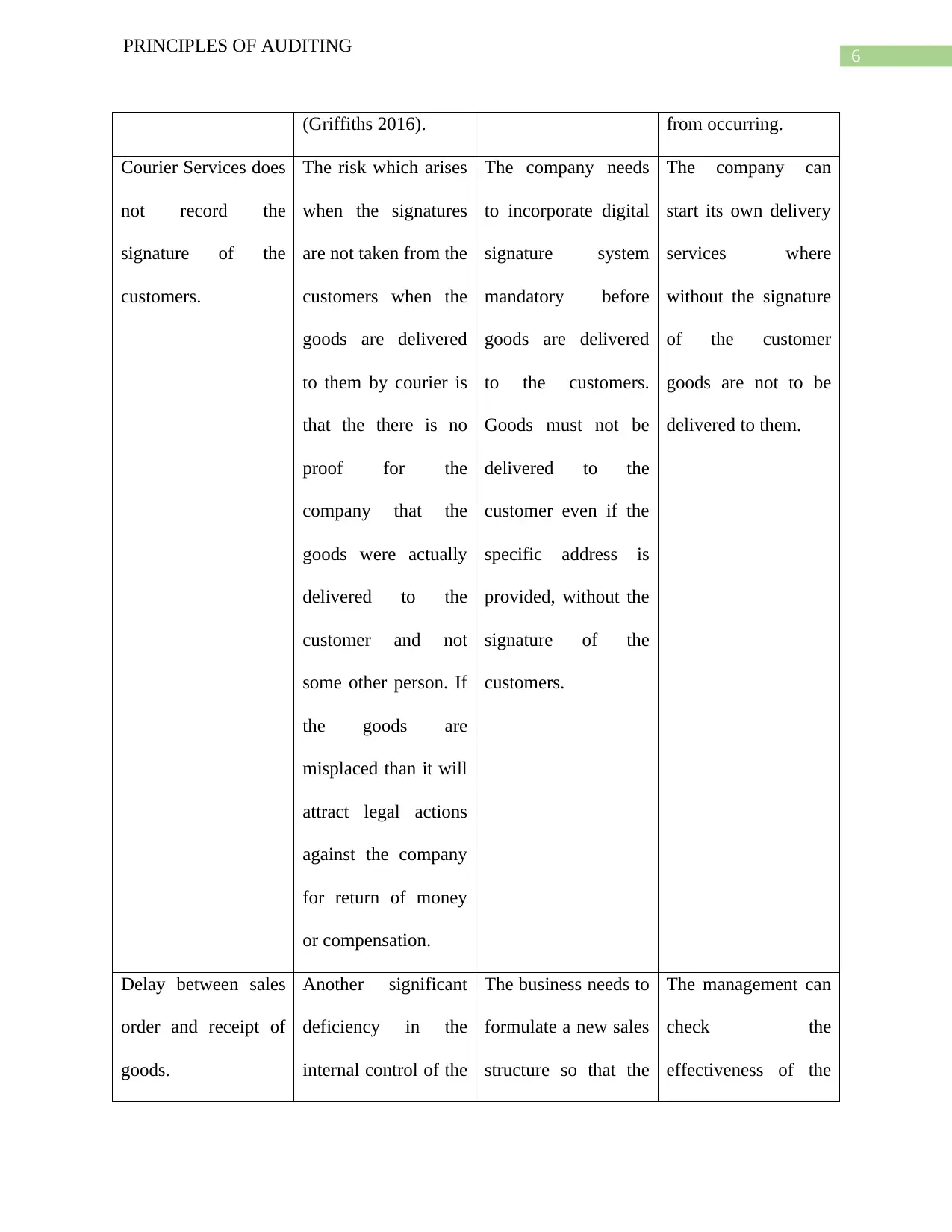

PRINCIPLES OF AUDITING

(Griffiths 2016). from occurring.

Courier Services does

not record the

signature of the

customers.

The risk which arises

when the signatures

are not taken from the

customers when the

goods are delivered

to them by courier is

that the there is no

proof for the

company that the

goods were actually

delivered to the

customer and not

some other person. If

the goods are

misplaced than it will

attract legal actions

against the company

for return of money

or compensation.

The company needs

to incorporate digital

signature system

mandatory before

goods are delivered

to the customers.

Goods must not be

delivered to the

customer even if the

specific address is

provided, without the

signature of the

customers.

The company can

start its own delivery

services where

without the signature

of the customer

goods are not to be

delivered to them.

Delay between sales

order and receipt of

goods.

Another significant

deficiency in the

internal control of the

The business needs to

formulate a new sales

structure so that the

The management can

check the

effectiveness of the

PRINCIPLES OF AUDITING

(Griffiths 2016). from occurring.

Courier Services does

not record the

signature of the

customers.

The risk which arises

when the signatures

are not taken from the

customers when the

goods are delivered

to them by courier is

that the there is no

proof for the

company that the

goods were actually

delivered to the

customer and not

some other person. If

the goods are

misplaced than it will

attract legal actions

against the company

for return of money

or compensation.

The company needs

to incorporate digital

signature system

mandatory before

goods are delivered

to the customers.

Goods must not be

delivered to the

customer even if the

specific address is

provided, without the

signature of the

customers.

The company can

start its own delivery

services where

without the signature

of the customer

goods are not to be

delivered to them.

Delay between sales

order and receipt of

goods.

Another significant

deficiency in the

internal control of the

The business needs to

formulate a new sales

structure so that the

The management can

check the

effectiveness of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

PRINCIPLES OF AUDITING

business is the delay

between the sales

order and the actual

goods received by the

customers (Feng et

al. 2014). This

suggest that the sales

and delivery structure

of the business is

weak.

business the gaps in

order received and

delivery of the goods

is removed. The

company also needs

to start its delivery

services which can

help in reducing such

a gap. The new sales

structure will ensure

that the recording of

sales and dispatching

of goods so that it can

be received by

customers.

new sales and

delivery structure by

analyzing the sales

and receiving

feedbacks of the

customers as to

whether they are

satisfied or not.

Allowing of Sales

credit and discounts.

The sales credits are

set by the sales ledger

clerk and also the

sales discounts are

allowed by the sales

team member which

might not be

appropriate. The

The credit policy and

the discounting

policy of the

company should be

set by the top-level

management which

includes the sales

manager or the sales

The credit policy and

discounting policy as

set by the senior level

management will be

more effective. This

can be checked by

analyzing the

departmental meeting

PRINCIPLES OF AUDITING

business is the delay

between the sales

order and the actual

goods received by the

customers (Feng et

al. 2014). This

suggest that the sales

and delivery structure

of the business is

weak.

business the gaps in

order received and

delivery of the goods

is removed. The

company also needs

to start its delivery

services which can

help in reducing such

a gap. The new sales

structure will ensure

that the recording of

sales and dispatching

of goods so that it can

be received by

customers.

new sales and

delivery structure by

analyzing the sales

and receiving

feedbacks of the

customers as to

whether they are

satisfied or not.

Allowing of Sales

credit and discounts.

The sales credits are

set by the sales ledger

clerk and also the

sales discounts are

allowed by the sales

team member which

might not be

appropriate. The

The credit policy and

the discounting

policy of the

company should be

set by the top-level

management which

includes the sales

manager or the sales

The credit policy and

discounting policy as

set by the senior level

management will be

more effective. This

can be checked by

analyzing the

departmental meeting

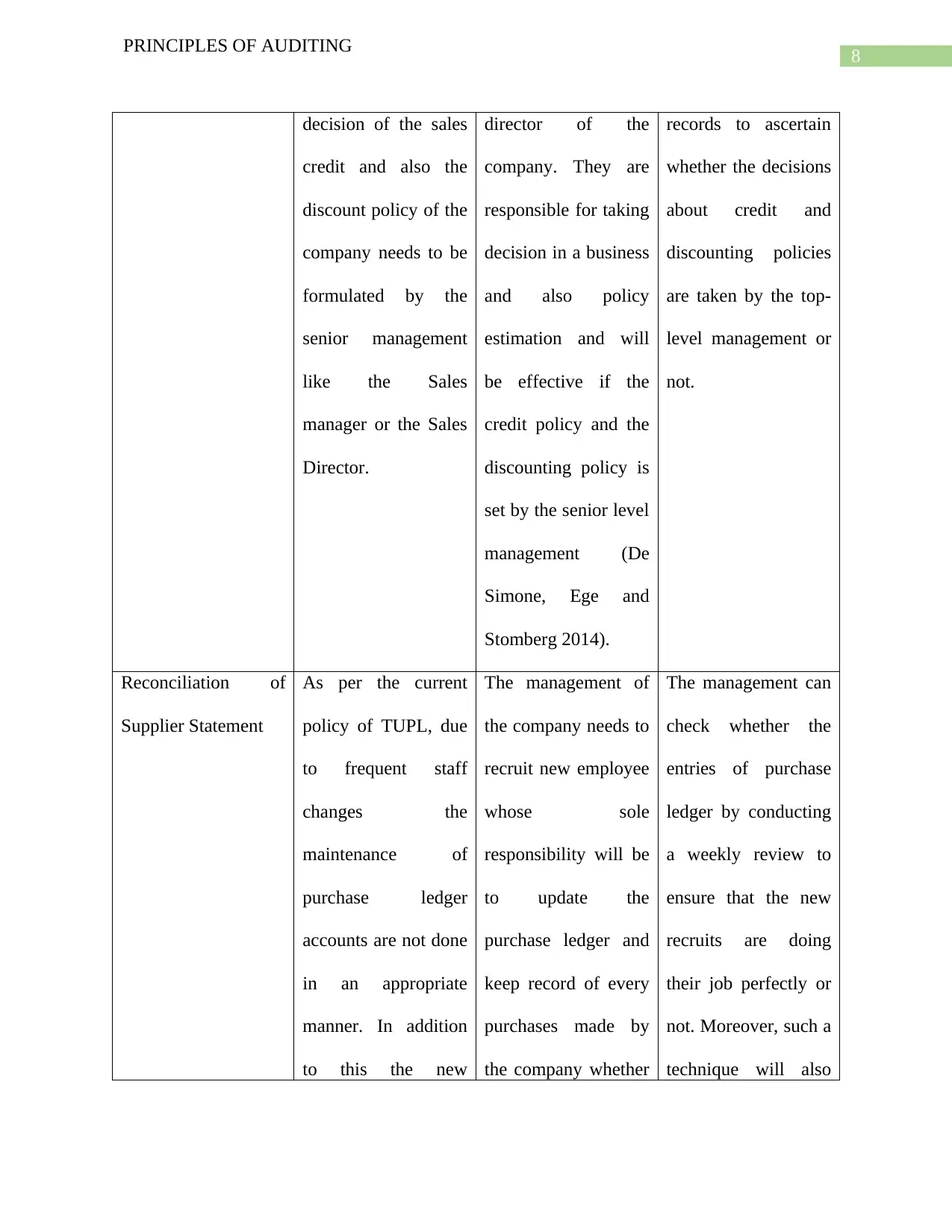

8

PRINCIPLES OF AUDITING

decision of the sales

credit and also the

discount policy of the

company needs to be

formulated by the

senior management

like the Sales

manager or the Sales

Director.

director of the

company. They are

responsible for taking

decision in a business

and also policy

estimation and will

be effective if the

credit policy and the

discounting policy is

set by the senior level

management (De

Simone, Ege and

Stomberg 2014).

records to ascertain

whether the decisions

about credit and

discounting policies

are taken by the top-

level management or

not.

Reconciliation of

Supplier Statement

As per the current

policy of TUPL, due

to frequent staff

changes the

maintenance of

purchase ledger

accounts are not done

in an appropriate

manner. In addition

to this the new

The management of

the company needs to

recruit new employee

whose sole

responsibility will be

to update the

purchase ledger and

keep record of every

purchases made by

the company whether

The management can

check whether the

entries of purchase

ledger by conducting

a weekly review to

ensure that the new

recruits are doing

their job perfectly or

not. Moreover, such a

technique will also

PRINCIPLES OF AUDITING

decision of the sales

credit and also the

discount policy of the

company needs to be

formulated by the

senior management

like the Sales

manager or the Sales

Director.

director of the

company. They are

responsible for taking

decision in a business

and also policy

estimation and will

be effective if the

credit policy and the

discounting policy is

set by the senior level

management (De

Simone, Ege and

Stomberg 2014).

records to ascertain

whether the decisions

about credit and

discounting policies

are taken by the top-

level management or

not.

Reconciliation of

Supplier Statement

As per the current

policy of TUPL, due

to frequent staff

changes the

maintenance of

purchase ledger

accounts are not done

in an appropriate

manner. In addition

to this the new

The management of

the company needs to

recruit new employee

whose sole

responsibility will be

to update the

purchase ledger and

keep record of every

purchases made by

the company whether

The management can

check whether the

entries of purchase

ledger by conducting

a weekly review to

ensure that the new

recruits are doing

their job perfectly or

not. Moreover, such a

technique will also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

PRINCIPLES OF AUDITING

supplier’s details are

not even added to the

purchase ledger. The

risk which arises due

to this is that, the

details of the

potential suppliers

who have provided

the business with

credit purchases

might get lost and it

will be difficult to

keep track of the total

purchases. This will

in turn affect the

financial statements

of the company as it

will show purchases

with an inaccurate

amount.

in cash or credit. In

addition to this a

weekly review of the

purchase ledger will

result in scrutiny of

the ledger accounts

and ensure that the

entries are accurately

recorded.

ensure that the

transactions in the

purchase ledger are

effectively recorded

and make the work of

the auditor easier in

such areas.

PRINCIPLES OF AUDITING

supplier’s details are

not even added to the

purchase ledger. The

risk which arises due

to this is that, the

details of the

potential suppliers

who have provided

the business with

credit purchases

might get lost and it

will be difficult to

keep track of the total

purchases. This will

in turn affect the

financial statements

of the company as it

will show purchases

with an inaccurate

amount.

in cash or credit. In

addition to this a

weekly review of the

purchase ledger will

result in scrutiny of

the ledger accounts

and ensure that the

entries are accurately

recorded.

ensure that the

transactions in the

purchase ledger are

effectively recorded

and make the work of

the auditor easier in

such areas.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

PRINCIPLES OF AUDITING

Part C

Part C-1

a. As per the case study, Unique Furniture Manufacturing Pty ltd is engaged in the

manufacturing of grandfather clocks. The two assets accounts which are under the risks

of being materially misstatement are:

i. Cash Balance: The cash balance of the business is under the risk of being materially

misstated. As the prices of labour is increasing and also the business imports timber

which is the main raw material for the business in manufacturing has a high cost, the cash

balance might be overstated so that a favorable cash balance is shown. The import of the

timber requires foreign currency which is increasing therefore the cost of imports are also

increasing. The reduction gross margin and the net margin of the company is evidence

that the cost of the company is high and the overall sales of the company are more or less

same (Lobo and Zhao 2013). Hence, the management might want to show a favorable

cash balance in order to give the shareholders hope that the liquidity position of the

company is still secure (Brunnermeier, Gorton and Krishnamurthy 2013).

ii. Inventory Account: As the company follows Sales or Return basis for recording sales

transactions. The inventory account of the business is at risk of being materially misstated

(Knechel and Salterio 2016). The management might accidently or knowingly record the

inventory stock of the company as sales of the business as under the method when the

prices of the finished goods are received then it is considered as sales of the business

otherwise it is kept as stock. The inventory balance might be overstated or understated as

the case may be.

PRINCIPLES OF AUDITING

Part C

Part C-1

a. As per the case study, Unique Furniture Manufacturing Pty ltd is engaged in the

manufacturing of grandfather clocks. The two assets accounts which are under the risks

of being materially misstatement are:

i. Cash Balance: The cash balance of the business is under the risk of being materially

misstated. As the prices of labour is increasing and also the business imports timber

which is the main raw material for the business in manufacturing has a high cost, the cash

balance might be overstated so that a favorable cash balance is shown. The import of the

timber requires foreign currency which is increasing therefore the cost of imports are also

increasing. The reduction gross margin and the net margin of the company is evidence

that the cost of the company is high and the overall sales of the company are more or less

same (Lobo and Zhao 2013). Hence, the management might want to show a favorable

cash balance in order to give the shareholders hope that the liquidity position of the

company is still secure (Brunnermeier, Gorton and Krishnamurthy 2013).

ii. Inventory Account: As the company follows Sales or Return basis for recording sales

transactions. The inventory account of the business is at risk of being materially misstated

(Knechel and Salterio 2016). The management might accidently or knowingly record the

inventory stock of the company as sales of the business as under the method when the

prices of the finished goods are received then it is considered as sales of the business

otherwise it is kept as stock. The inventory balance might be overstated or understated as

the case may be.

11

PRINCIPLES OF AUDITING

b. The prior period figures of sales and inventory might be materially misstated as the

company follows Sales or Return basis under which sales is only to be recorded when the

price for the same is received (Johnstone, Gramling and Rittenberg 2013). There is a

chance that due to inexperience of the accountant potential inventory under this method

might be recorded as sales of the business.

c. The three factors which can bring in the going concern concept of the management under

question are given below:

i. The net profit margin and gross profit margin of the business suggest that the

company is not able to make much profits as the company is incurring high costs.

Moreover, as mentioned in the case study the management of the company is unable

to recover amount of cost from the customers which is a factor which contributes to

the low profits of the business.

ii. The increasing cost of materials of the business which the management imports. The

foreign exchange prices of the imports are increasing which is also contributing to the

high cost of companies.

iii. The availability of cheap labour is also a difficult for the business and the cost of

skilled labour is very high and also contributes to the cost of the company.

d. The audit planning process will be carried out considering all the factors which affect the

cost of the company. In addition to this, the auditor needs to have a clear understanding

of the Sales or Return basis policies which the business follows and ensure that such a

basis is constantly applied for measuring the sales transaction of the business (King,

Oracle International Corp 2014). The auditor also needs to plan for the valuation process

PRINCIPLES OF AUDITING

b. The prior period figures of sales and inventory might be materially misstated as the

company follows Sales or Return basis under which sales is only to be recorded when the

price for the same is received (Johnstone, Gramling and Rittenberg 2013). There is a

chance that due to inexperience of the accountant potential inventory under this method

might be recorded as sales of the business.

c. The three factors which can bring in the going concern concept of the management under

question are given below:

i. The net profit margin and gross profit margin of the business suggest that the

company is not able to make much profits as the company is incurring high costs.

Moreover, as mentioned in the case study the management of the company is unable

to recover amount of cost from the customers which is a factor which contributes to

the low profits of the business.

ii. The increasing cost of materials of the business which the management imports. The

foreign exchange prices of the imports are increasing which is also contributing to the

high cost of companies.

iii. The availability of cheap labour is also a difficult for the business and the cost of

skilled labour is very high and also contributes to the cost of the company.

d. The audit planning process will be carried out considering all the factors which affect the

cost of the company. In addition to this, the auditor needs to have a clear understanding

of the Sales or Return basis policies which the business follows and ensure that such a

basis is constantly applied for measuring the sales transaction of the business (King,

Oracle International Corp 2014). The auditor also needs to plan for the valuation process

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.