ACT305 Corporate Accounting: AASB 10 & Consolidated Reporting

VerifiedAdded on 2023/06/04

|12

|2248

|460

Report

AI Summary

This report provides a comprehensive analysis of AASB 10, focusing on its application to consolidated financial statements and investment decisions. It examines various scenarios, including investments in subsidiaries, loans converted to equity, and jointly controlled entities. The report addresses the requirements for consolidation, non-controlling interests, and goodwill impairment. It also delves into specific accounting treatments for intercompany transactions, such as inventory adjustments, profit on sale of plant, and management fees. The analysis is supported by journal entries and acquisition analyses, offering a practical understanding of AASB 10's impact on financial reporting. This student contributed document is available on Desklib, where students can find various study resources.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Answer to Question 1:.....................................................................................................................2

Requirement a:.............................................................................................................................2

Requirement b:.............................................................................................................................3

Answer to Question 2:.....................................................................................................................4

Answer to Question 3......................................................................................................................5

Acquisition Analysis:...................................................................................................................5

Consolidation Worksheet Entries:...............................................................................................5

Answer to Question 4:.....................................................................................................................6

Introduction..................................................................................................................................6

Part a............................................................................................................................................7

Part B...........................................................................................................................................7

Part c............................................................................................................................................8

Part D...........................................................................................................................................8

Conclusion...................................................................................................................................9

Reference & Bibliography:............................................................................................................10

Answer to Question 1:.....................................................................................................................2

Requirement a:.............................................................................................................................2

Requirement b:.............................................................................................................................3

Answer to Question 2:.....................................................................................................................4

Answer to Question 3......................................................................................................................5

Acquisition Analysis:...................................................................................................................5

Consolidation Worksheet Entries:...............................................................................................5

Answer to Question 4:.....................................................................................................................6

Introduction..................................................................................................................................6

Part a............................................................................................................................................7

Part B...........................................................................................................................................7

Part c............................................................................................................................................8

Part D...........................................................................................................................................8

Conclusion...................................................................................................................................9

Reference & Bibliography:............................................................................................................10

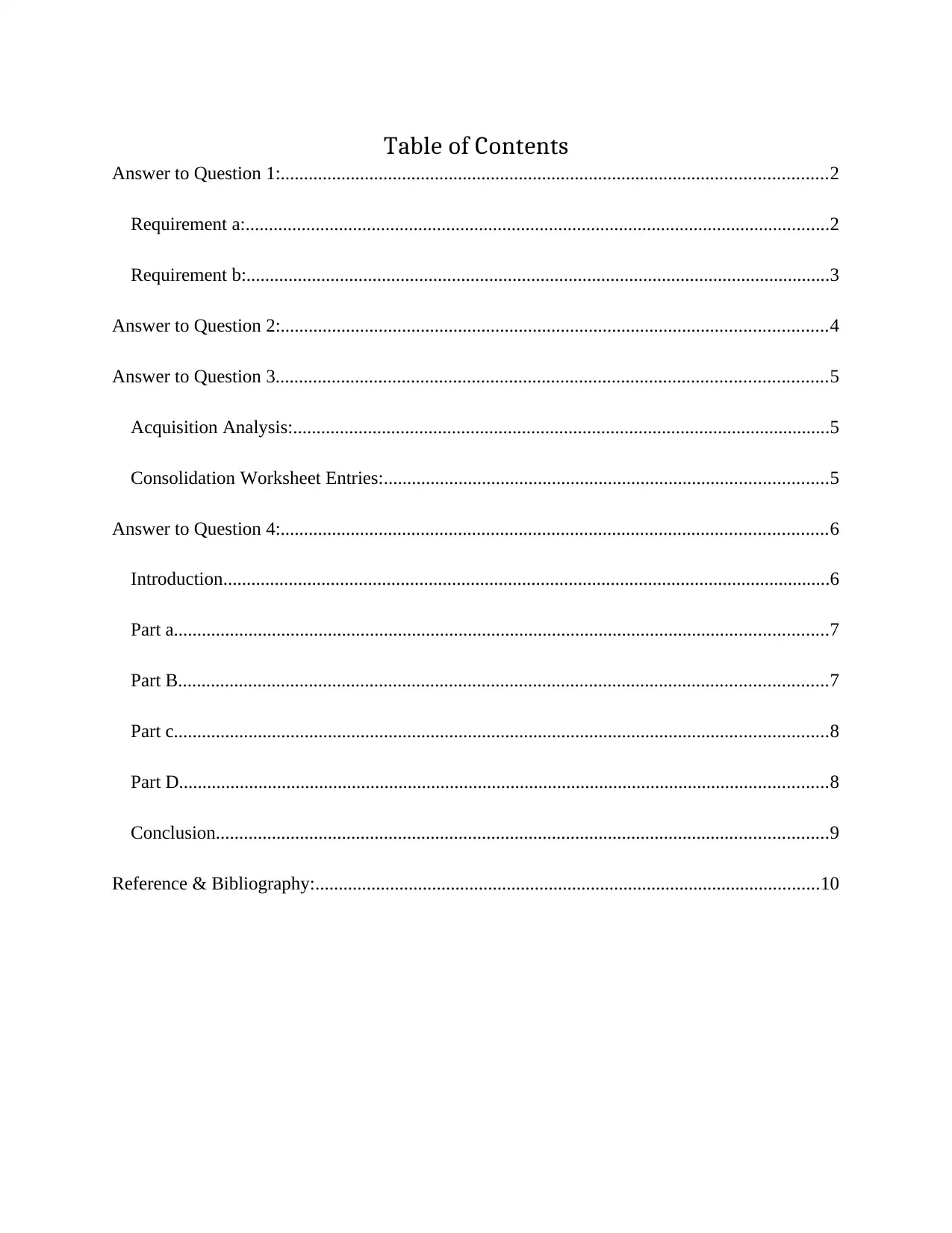

Answer to Question 1:

Requirement a:

Dr. Cr.

Date Amount Amount

01-07-2017 Investment in Fry Ltd. Dr. $ 50,000.00

To, Cash at Bank $ 50,000.00

30-06-2018 Investment in Fry Ltd. Dr. $ 15,000.00

To, Share of Profit in Fry Ltd. $ 15,000.00

Cash at Bank Dr. $ 24,000.00

To, Investment in Fry Ltd. $ 24,000.00

30-06-2019 Investment in Fry Ltd. Dr. $ 13,500.00

To, Share of Profit in Fry Ltd. $ 13,500.00

Cash at Bank Dr. $ 4,500.00

To, Investment in Fry Ltd. $ 4,500.00

30-06-2020 Investment in Fry Ltd. Dr. $ 12,000.00

To, Share of Profit in Fry Ltd. $ 12,000.00

Cash at Bank Dr. $ 3,000.00

To, Investment in Fry Ltd. $ 3,000.00

In the books of Small Ltd.

Journal Entries

Particulars

Requirement a:

Dr. Cr.

Date Amount Amount

01-07-2017 Investment in Fry Ltd. Dr. $ 50,000.00

To, Cash at Bank $ 50,000.00

30-06-2018 Investment in Fry Ltd. Dr. $ 15,000.00

To, Share of Profit in Fry Ltd. $ 15,000.00

Cash at Bank Dr. $ 24,000.00

To, Investment in Fry Ltd. $ 24,000.00

30-06-2019 Investment in Fry Ltd. Dr. $ 13,500.00

To, Share of Profit in Fry Ltd. $ 13,500.00

Cash at Bank Dr. $ 4,500.00

To, Investment in Fry Ltd. $ 4,500.00

30-06-2020 Investment in Fry Ltd. Dr. $ 12,000.00

To, Share of Profit in Fry Ltd. $ 12,000.00

Cash at Bank Dr. $ 3,000.00

To, Investment in Fry Ltd. $ 3,000.00

In the books of Small Ltd.

Journal Entries

Particulars

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

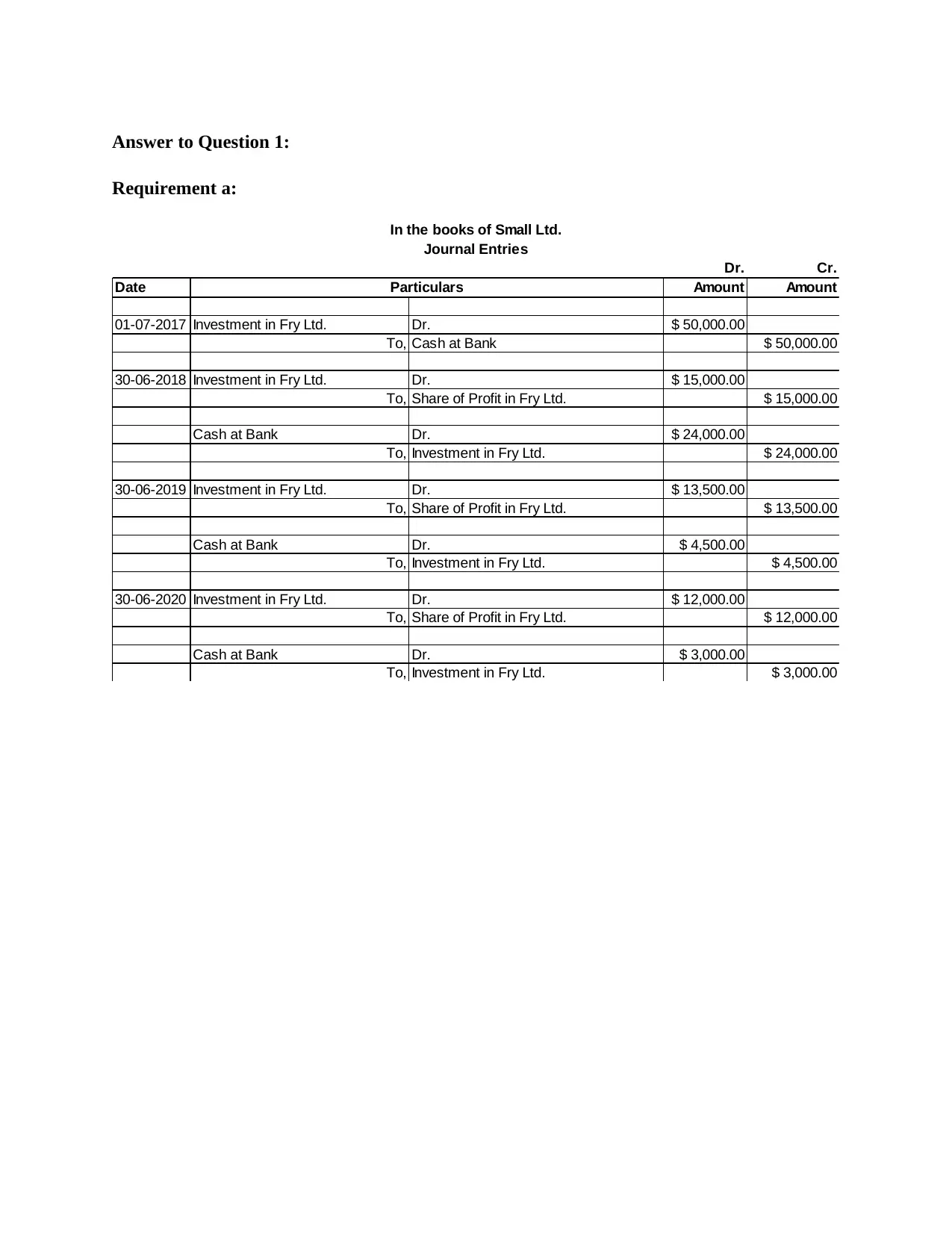

Requirement b:

Dr. Cr.

Date Amount Amount

01-07-2017 Investment in Fry Ltd. Dr. $ 50,000.00

To, Cash at Bank $ 50,000.00

30-06-2018 Equity Capital Dr. $ 9,000.00

Retained Profits (1/7/17) Dr. $ 36,000.00

Goodwill Dr. $ 5,000.00

To, Investment in Fry Ltd. $ 50,000.00

Equity Capital Dr. $ 21,000.00

Retained Profits (1/7/17) Dr. $ 84,000.00

To, NCI $ 1,05,000.00

Retained Profits (30/6/18) Dr. $ 35,000.00

To, NCI Share of Profit $ 35,000.00

Dividend Received Dr. $ 24,000.00

NCI Dr. $ 56,000.00

To, Dividend Paid $ 80,000.00

30-06-2019 Retained Profits (30/6/19) Dr. $ 31,500.00

To, NCI Share of Profit $ 31,500.00

Dividend Received Dr. $ 4,500.00

NCI Dr. $ 10,500.00

To, Dividend Paid $ 15,000.00

30-06-2020 Retained Profits (30/6/20) Dr. $ 28,000.00

To, NCI Share of Profit $ 28,000.00

Dividend Received Dr. $ 3,000.00

NCI Dr. $ 7,000.00

To, Dividend Paid $ 10,000.00

Particulars

In the books of Small Ltd.

Journal Entries

Dr. Cr.

Date Amount Amount

01-07-2017 Investment in Fry Ltd. Dr. $ 50,000.00

To, Cash at Bank $ 50,000.00

30-06-2018 Equity Capital Dr. $ 9,000.00

Retained Profits (1/7/17) Dr. $ 36,000.00

Goodwill Dr. $ 5,000.00

To, Investment in Fry Ltd. $ 50,000.00

Equity Capital Dr. $ 21,000.00

Retained Profits (1/7/17) Dr. $ 84,000.00

To, NCI $ 1,05,000.00

Retained Profits (30/6/18) Dr. $ 35,000.00

To, NCI Share of Profit $ 35,000.00

Dividend Received Dr. $ 24,000.00

NCI Dr. $ 56,000.00

To, Dividend Paid $ 80,000.00

30-06-2019 Retained Profits (30/6/19) Dr. $ 31,500.00

To, NCI Share of Profit $ 31,500.00

Dividend Received Dr. $ 4,500.00

NCI Dr. $ 10,500.00

To, Dividend Paid $ 15,000.00

30-06-2020 Retained Profits (30/6/20) Dr. $ 28,000.00

To, NCI Share of Profit $ 28,000.00

Dividend Received Dr. $ 3,000.00

NCI Dr. $ 7,000.00

To, Dividend Paid $ 10,000.00

Particulars

In the books of Small Ltd.

Journal Entries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

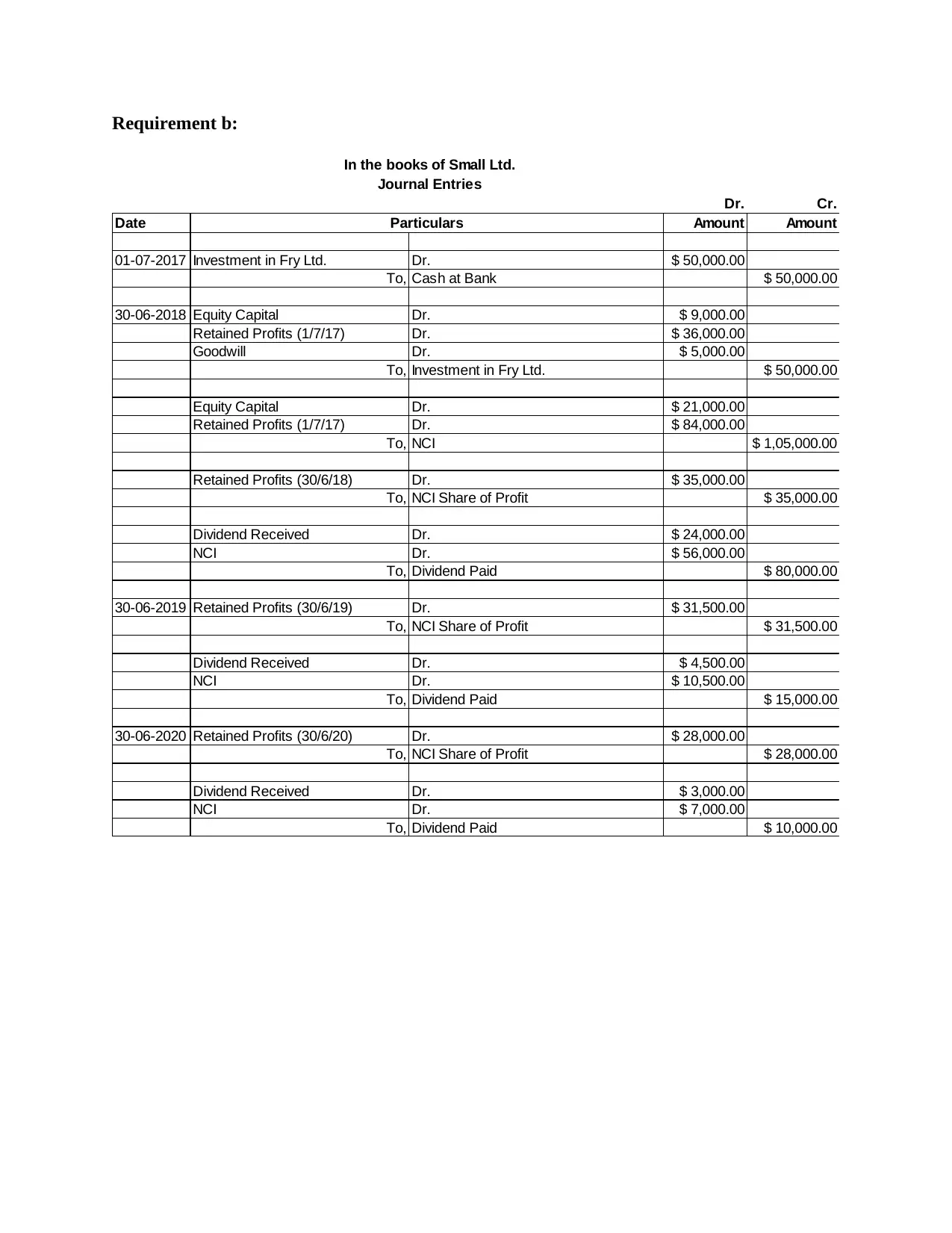

Answer to Question 2:

Creditors's Payment Priority on Liquidation Ranking

Receiver's Cost when realising secured assets 1

Liquidator's Expenses 2

Secured Creditors 3

Staff Wages Payable 4

Staff Leave Entitlements 5

Tax Payable 6

Local Government Rates 7

Unsecured Bank Overdraft 8

Unsecured Trade Payables 9

Executive Directors' Wages Payable 10

Executive Directors' Leave Entitlements 11

Dividend Payable 12

Particulars

Secured Land &

Buildings Other Assets Total Balance

Receipts from Sale $ 75,00,000.00 $ 67,50,000.00 $ 1,42,50,000.00

Receiver's Cost when realising secured assets $ -1,50,000.00 $ -1,50,000.00

Liquidator's Expenses $ -6,00,000.00 $ -6,00,000.00

Secured Creditors $ -67,50,000.00 $ -22,50,000.00 $ -90,00,000.00

Staff Wages Payable $ -9,00,000.00 $ -9,00,000.00

Staff Leave Entitlements $ -1,50,000.00 $ -1,50,000.00

Tax Payable $ -10,50,000.00 $ -10,50,000.00

Local Government Rates $ -3,00,000.00 $ -3,00,000.00

Unsecured Bank Overdraft $ -7,50,000.00 $ -7,50,000.00

Unsecured Trade Payables $ -13,50,000.00 $ -24,00,000.00

Executive Directors' Wages Payable $ -4,50,000.00

Executive Directors' Leave Entitlements $ -1,50,000.00

Dividend Payable $ -4,50,000.00

BALANCE $ 0.00 $ 0.00 $ -21,00,000.00

SALE PROCEEDS FROM

Creditors's Payment Priority on Liquidation Ranking

Receiver's Cost when realising secured assets 1

Liquidator's Expenses 2

Secured Creditors 3

Staff Wages Payable 4

Staff Leave Entitlements 5

Tax Payable 6

Local Government Rates 7

Unsecured Bank Overdraft 8

Unsecured Trade Payables 9

Executive Directors' Wages Payable 10

Executive Directors' Leave Entitlements 11

Dividend Payable 12

Particulars

Secured Land &

Buildings Other Assets Total Balance

Receipts from Sale $ 75,00,000.00 $ 67,50,000.00 $ 1,42,50,000.00

Receiver's Cost when realising secured assets $ -1,50,000.00 $ -1,50,000.00

Liquidator's Expenses $ -6,00,000.00 $ -6,00,000.00

Secured Creditors $ -67,50,000.00 $ -22,50,000.00 $ -90,00,000.00

Staff Wages Payable $ -9,00,000.00 $ -9,00,000.00

Staff Leave Entitlements $ -1,50,000.00 $ -1,50,000.00

Tax Payable $ -10,50,000.00 $ -10,50,000.00

Local Government Rates $ -3,00,000.00 $ -3,00,000.00

Unsecured Bank Overdraft $ -7,50,000.00 $ -7,50,000.00

Unsecured Trade Payables $ -13,50,000.00 $ -24,00,000.00

Executive Directors' Wages Payable $ -4,50,000.00

Executive Directors' Leave Entitlements $ -1,50,000.00

Dividend Payable $ -4,50,000.00

BALANCE $ 0.00 $ 0.00 $ -21,00,000.00

SALE PROCEEDS FROM

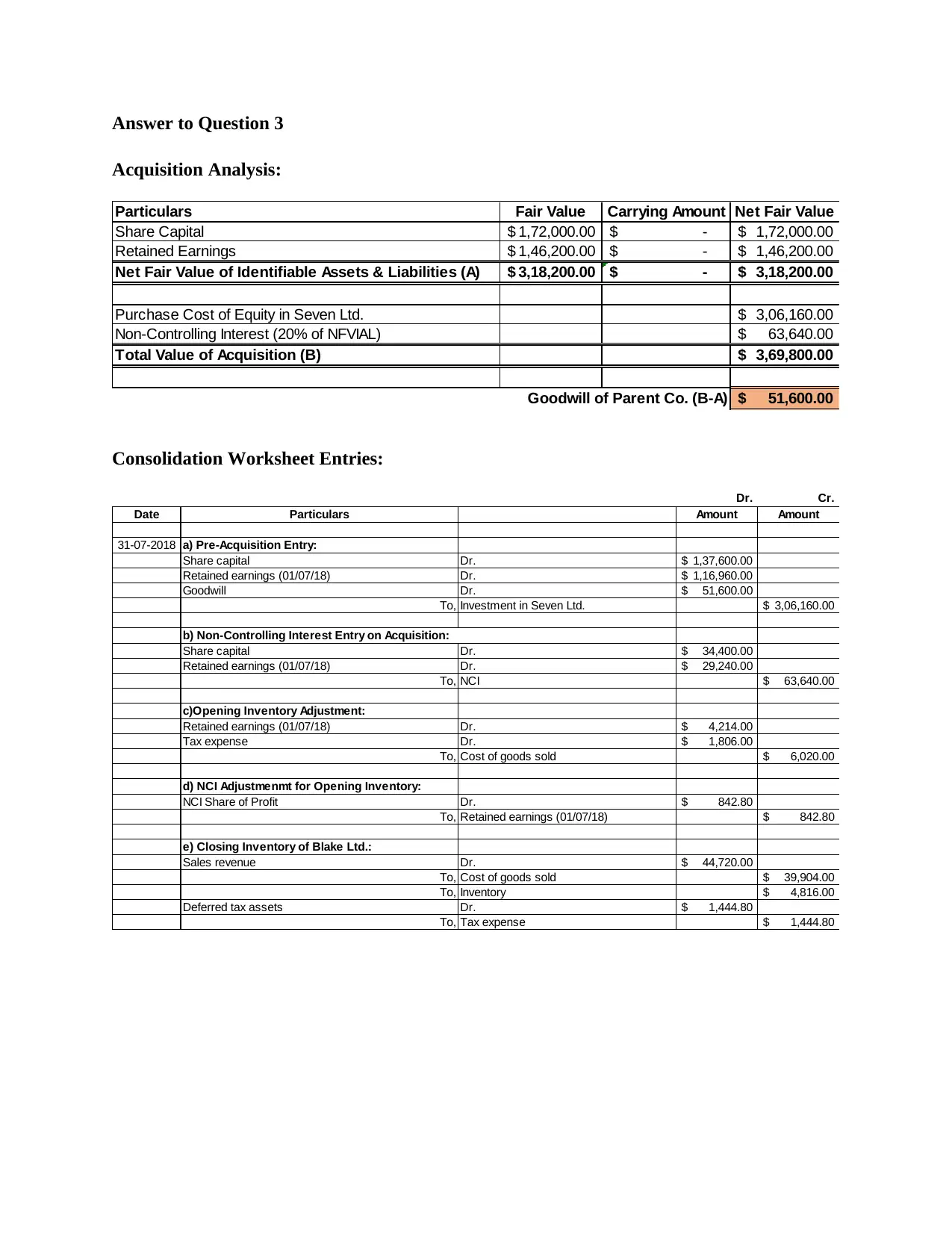

Answer to Question 3

Acquisition Analysis:

Particulars Fair Value Carrying Amount Net Fair Value

Share Capital 1,72,000.00$ -$ 1,72,000.00$

Retained Earnings 1,46,200.00$ -$ 1,46,200.00$

Net Fair Value of Identifiable Assets & Liabilities (A) 3,18,200.00$ -$ 3,18,200.00$

Purchase Cost of Equity in Seven Ltd. 3,06,160.00$

Non-Controlling Interest (20% of NFVIAL) 63,640.00$

Total Value of Acquisition (B) 3,69,800.00$

51,600.00$Goodwill of Parent Co. (B-A)

Consolidation Worksheet Entries:

Dr. Cr.

Date Particulars Amount Amount

31-07-2018 a) Pre-Acquisition Entry:

Share capital Dr. 1,37,600.00$

Retained earnings (01/07/18) Dr. 1,16,960.00$

Goodwill Dr. 51,600.00$

To, Investment in Seven Ltd. 3,06,160.00$

Share capital Dr. 34,400.00$

Retained earnings (01/07/18) Dr. 29,240.00$

To, NCI 63,640.00$

c)Opening Inventory Adjustment:

Retained earnings (01/07/18) Dr. 4,214.00$

Tax expense Dr. 1,806.00$

To, Cost of goods sold 6,020.00$

d) NCI Adjustmenmt for Opening Inventory:

NCI Share of Profit Dr. 842.80$

To, Retained earnings (01/07/18) 842.80$

e) Closing Inventory of Blake Ltd.:

Sales revenue Dr. 44,720.00$

To, Cost of goods sold 39,904.00$

To, Inventory 4,816.00$

Deferred tax assets Dr. 1,444.80$

To, Tax expense 1,444.80$

b) Non-Controlling Interest Entry on Acquisition:

Acquisition Analysis:

Particulars Fair Value Carrying Amount Net Fair Value

Share Capital 1,72,000.00$ -$ 1,72,000.00$

Retained Earnings 1,46,200.00$ -$ 1,46,200.00$

Net Fair Value of Identifiable Assets & Liabilities (A) 3,18,200.00$ -$ 3,18,200.00$

Purchase Cost of Equity in Seven Ltd. 3,06,160.00$

Non-Controlling Interest (20% of NFVIAL) 63,640.00$

Total Value of Acquisition (B) 3,69,800.00$

51,600.00$Goodwill of Parent Co. (B-A)

Consolidation Worksheet Entries:

Dr. Cr.

Date Particulars Amount Amount

31-07-2018 a) Pre-Acquisition Entry:

Share capital Dr. 1,37,600.00$

Retained earnings (01/07/18) Dr. 1,16,960.00$

Goodwill Dr. 51,600.00$

To, Investment in Seven Ltd. 3,06,160.00$

Share capital Dr. 34,400.00$

Retained earnings (01/07/18) Dr. 29,240.00$

To, NCI 63,640.00$

c)Opening Inventory Adjustment:

Retained earnings (01/07/18) Dr. 4,214.00$

Tax expense Dr. 1,806.00$

To, Cost of goods sold 6,020.00$

d) NCI Adjustmenmt for Opening Inventory:

NCI Share of Profit Dr. 842.80$

To, Retained earnings (01/07/18) 842.80$

e) Closing Inventory of Blake Ltd.:

Sales revenue Dr. 44,720.00$

To, Cost of goods sold 39,904.00$

To, Inventory 4,816.00$

Deferred tax assets Dr. 1,444.80$

To, Tax expense 1,444.80$

b) Non-Controlling Interest Entry on Acquisition:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

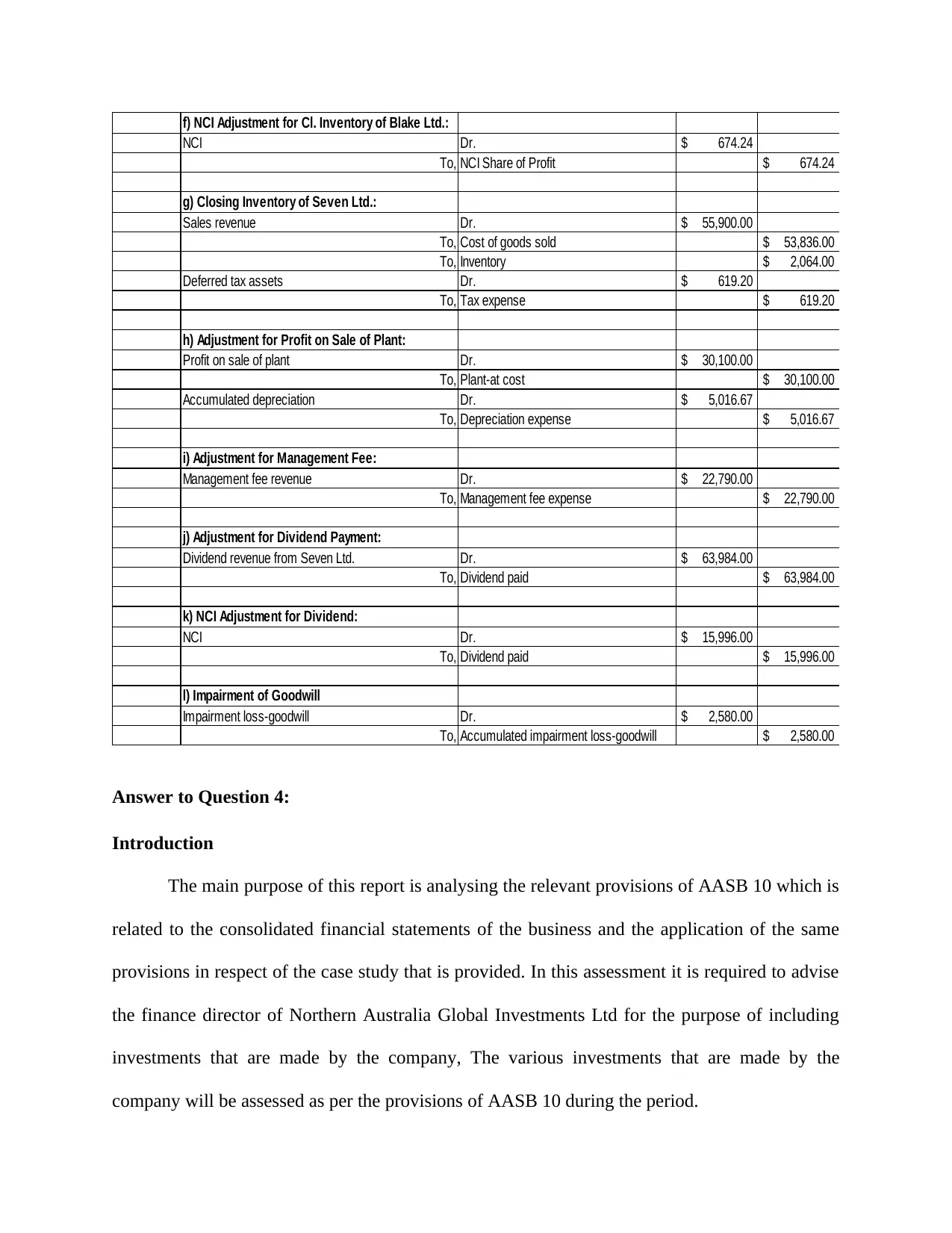

f) NCI Adjustment for Cl. Inventory of Blake Ltd.:

NCI Dr. 674.24$

To, NCI Share of Profit 674.24$

g) Closing Inventory of Seven Ltd.:

Sales revenue Dr. 55,900.00$

To, Cost of goods sold 53,836.00$

To, Inventory 2,064.00$

Deferred tax assets Dr. 619.20$

To, Tax expense 619.20$

h) Adjustment for Profit on Sale of Plant:

Profit on sale of plant Dr. 30,100.00$

To, Plant-at cost 30,100.00$

Accumulated depreciation Dr. 5,016.67$

To, Depreciation expense 5,016.67$

i) Adjustment for Management Fee:

Management fee revenue Dr. 22,790.00$

To, Management fee expense 22,790.00$

j) Adjustment for Dividend Payment:

Dividend revenue from Seven Ltd. Dr. 63,984.00$

To, Dividend paid 63,984.00$

k) NCI Adjustment for Dividend:

NCI Dr. 15,996.00$

To, Dividend paid 15,996.00$

l) Impairment of Goodwill

Impairment loss-goodwill Dr. 2,580.00$

To, Accumulated impairment loss-goodwill 2,580.00$

Answer to Question 4:

Introduction

The main purpose of this report is analysing the relevant provisions of AASB 10 which is

related to the consolidated financial statements of the business and the application of the same

provisions in respect of the case study that is provided. In this assessment it is required to advise

the finance director of Northern Australia Global Investments Ltd for the purpose of including

investments that are made by the company, The various investments that are made by the

company will be assessed as per the provisions of AASB 10 during the period.

NCI Dr. 674.24$

To, NCI Share of Profit 674.24$

g) Closing Inventory of Seven Ltd.:

Sales revenue Dr. 55,900.00$

To, Cost of goods sold 53,836.00$

To, Inventory 2,064.00$

Deferred tax assets Dr. 619.20$

To, Tax expense 619.20$

h) Adjustment for Profit on Sale of Plant:

Profit on sale of plant Dr. 30,100.00$

To, Plant-at cost 30,100.00$

Accumulated depreciation Dr. 5,016.67$

To, Depreciation expense 5,016.67$

i) Adjustment for Management Fee:

Management fee revenue Dr. 22,790.00$

To, Management fee expense 22,790.00$

j) Adjustment for Dividend Payment:

Dividend revenue from Seven Ltd. Dr. 63,984.00$

To, Dividend paid 63,984.00$

k) NCI Adjustment for Dividend:

NCI Dr. 15,996.00$

To, Dividend paid 15,996.00$

l) Impairment of Goodwill

Impairment loss-goodwill Dr. 2,580.00$

To, Accumulated impairment loss-goodwill 2,580.00$

Answer to Question 4:

Introduction

The main purpose of this report is analysing the relevant provisions of AASB 10 which is

related to the consolidated financial statements of the business and the application of the same

provisions in respect of the case study that is provided. In this assessment it is required to advise

the finance director of Northern Australia Global Investments Ltd for the purpose of including

investments that are made by the company, The various investments that are made by the

company will be assessed as per the provisions of AASB 10 during the period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part a

As per the case study , NAGIL ltd has provided a loan to Struggle Ltd which was

converted to equity as the latter company was unable to repay the liability. This provided the

company a holding of 70% in the business of Struggle Ltd. According to the provisions of Para 5

of AASB 10, an investor needs to determine whether the same is a parent company on the basis

of control, as per the business which have over the investee. As per para 7, control over a

business is established when all the requisite conditions are met . These conditions include the

power over the investee, exposure or rights to variable returns from the involvement in the

business , the power to affect the returns which are made by the investee(Aasb.gov.au. 2018).

In this case study NAGIL ltd is not actively involved in the day to day operations of the

company and also not in decisions of the business. Hence the management of the company

should not involve such investments in the consolidation of the business.

Part B

As per the case study, NAGIL has provided loan to Very Big Company ltd ( VBCL)

during the period. The management of NAGIL has not made an investment in the shares of

VBCL. The management of NAGIL has not made an investment in the shares of the company of

VBCL but has provided a loan . VBCL has not been able to meet the payment requirements of

the loan and therefore a bailout package is initiated . This has been done as the company cannot

make any payments unless the same is approved by NAGIL. This is not an investment in the

equity shares of the company. Hence the same cannot be coveted in AAASB 10 as NAGIL

cannot be considered as a parent company of VBCL. Therefore the management of NAGIL

should consider the same as loan for the purpose of business(Carlin 2014.).

As per the case study , NAGIL ltd has provided a loan to Struggle Ltd which was

converted to equity as the latter company was unable to repay the liability. This provided the

company a holding of 70% in the business of Struggle Ltd. According to the provisions of Para 5

of AASB 10, an investor needs to determine whether the same is a parent company on the basis

of control, as per the business which have over the investee. As per para 7, control over a

business is established when all the requisite conditions are met . These conditions include the

power over the investee, exposure or rights to variable returns from the involvement in the

business , the power to affect the returns which are made by the investee(Aasb.gov.au. 2018).

In this case study NAGIL ltd is not actively involved in the day to day operations of the

company and also not in decisions of the business. Hence the management of the company

should not involve such investments in the consolidation of the business.

Part B

As per the case study, NAGIL has provided loan to Very Big Company ltd ( VBCL)

during the period. The management of NAGIL has not made an investment in the shares of

VBCL. The management of NAGIL has not made an investment in the shares of the company of

VBCL but has provided a loan . VBCL has not been able to meet the payment requirements of

the loan and therefore a bailout package is initiated . This has been done as the company cannot

make any payments unless the same is approved by NAGIL. This is not an investment in the

equity shares of the company. Hence the same cannot be coveted in AAASB 10 as NAGIL

cannot be considered as a parent company of VBCL. Therefore the management of NAGIL

should consider the same as loan for the purpose of business(Carlin 2014.).

Part c

The case which is provided is related to the company of Medium Sized

Company( MSCL). Thus company is a subsidiary of both NAGIL and Sharp Players Ltd( SPL).

Both these companies hold an equal ownership in the business and also provides an equal source

of finance to the company. As per the provisions of AASB 10 ,the para 9 states that ij case an

investee is controlled by two investors together then the same cannot be controlled by any one

business. Hence both the companies needs to only account for the interest which it has in the

investee(Müller 2014).

In the case of MSCL, the management NAGIL needs to only consider the interest on

loans and the management fees which is to be paid in case the company is able to generate

profits for the period. In the case of losses, the management of MSCL only needs to incur

interest expenses and not the management fees to the business.

Part D

The case which is provided in the assessment shows that the management of NAGIL ltd

holds around 40 % of the holdings in the business of CrocsRUs and the other 60 percent is held

by the owners . the case provides that the management of the company is handled by NAGIL and

also how the major decisions are taken by the company as well. According to the provisions of

AASB 10, para 7 provides that in order for a business to have control of the investee. The

business should possess a power over the investee and should have variable rights on returns of

the business which is considered for an active role on the business(Howieson 2013).

The case which is provided is related to the company of Medium Sized

Company( MSCL). Thus company is a subsidiary of both NAGIL and Sharp Players Ltd( SPL).

Both these companies hold an equal ownership in the business and also provides an equal source

of finance to the company. As per the provisions of AASB 10 ,the para 9 states that ij case an

investee is controlled by two investors together then the same cannot be controlled by any one

business. Hence both the companies needs to only account for the interest which it has in the

investee(Müller 2014).

In the case of MSCL, the management NAGIL needs to only consider the interest on

loans and the management fees which is to be paid in case the company is able to generate

profits for the period. In the case of losses, the management of MSCL only needs to incur

interest expenses and not the management fees to the business.

Part D

The case which is provided in the assessment shows that the management of NAGIL ltd

holds around 40 % of the holdings in the business of CrocsRUs and the other 60 percent is held

by the owners . the case provides that the management of the company is handled by NAGIL and

also how the major decisions are taken by the company as well. According to the provisions of

AASB 10, para 7 provides that in order for a business to have control of the investee. The

business should possess a power over the investee and should have variable rights on returns of

the business which is considered for an active role on the business(Howieson 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the case of CrocsRUs the management of NAGIL has the control over the buiness and

also takes the major decisions and therefore they need to consolidate those investments in the

balance sheet.

Conclusion

The above discussion shows the various investment and loans that are provided to

different businesses during this period. The assessment shows the application of the provisions of

AASB 10 in order to determine whether the finance director should incorporate the transactions

in the consolidated financial statements of the businesses. The assessment effectively deals with

the reporting requirements of investment made in other businesses.

also takes the major decisions and therefore they need to consolidate those investments in the

balance sheet.

Conclusion

The above discussion shows the various investment and loans that are provided to

different businesses during this period. The assessment shows the application of the provisions of

AASB 10 in order to determine whether the finance director should incorporate the transactions

in the consolidated financial statements of the businesses. The assessment effectively deals with

the reporting requirements of investment made in other businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference & Bibliography:

Aasb.gov.au. 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 11 Oct. 2018].

Brown, R., 2014. A history of accounting and accountants. Routledge.

Carlin, T.M., 2014. Debating the impact of accrual accounting and reporting in the public sector.

Financial Accountability & Management, 21(3), pp.309-336.

Carlon, S., McAlpine-Mladenovic, R., Palm, C., Mitrione, L., Kirk, N. and Wong, L.,

2015. Financial accounting: Reporting, analysis and decision making. John Wiley and Sons

Australia.

Elliott, B., 2017. Financial Accounting and Reporting 18th Edition. Pearson Higher Ed

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Howieson, B., 2013. Defining the Reporting Entity in the Not‐for‐Profit Public Sector:

Implementation Issues Associated with the Control Test. Australian Accounting Review, 23(1),

pp.29-42.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Aasb.gov.au. 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 11 Oct. 2018].

Brown, R., 2014. A history of accounting and accountants. Routledge.

Carlin, T.M., 2014. Debating the impact of accrual accounting and reporting in the public sector.

Financial Accountability & Management, 21(3), pp.309-336.

Carlon, S., McAlpine-Mladenovic, R., Palm, C., Mitrione, L., Kirk, N. and Wong, L.,

2015. Financial accounting: Reporting, analysis and decision making. John Wiley and Sons

Australia.

Elliott, B., 2017. Financial Accounting and Reporting 18th Edition. Pearson Higher Ed

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Howieson, B., 2013. Defining the Reporting Entity in the Not‐for‐Profit Public Sector:

Implementation Issues Associated with the Control Test. Australian Accounting Review, 23(1),

pp.29-42.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

TAN, P.H.N., Lim, C.Y. and Kuah, E.W., 2017. Advanced financial accounting: An IFRS

standards approach.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Schipper, K., Francis, J. and Weil, R., 2017. Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

TAN, P.H.N., Lim, C.Y. and Kuah, E.W., 2017. Advanced financial accounting: An IFRS

standards approach.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.