Report on Activity Based Budgeting for Keytone Dairy Corporation

VerifiedAdded on 2020/12/09

|13

|3931

|60

Report

AI Summary

This report provides a comprehensive analysis of Activity Based Budgeting (ABB) within the context of managerial accounting, using Keytone Dairy Corporation as a case study. The introduction defines managerial accounting and contrasts it with financial accounting, highlighting the significance of ABB as a budgeting technique. The main body begins with a detailed description of Keytone Dairy, including its market capitalization, vision, products, and expansion strategies. The report then defines ABB, outlining its features, advantages, and disadvantages, and illustrates its application with an example. It also discusses the differences between ABB and traditional budgeting methods, and assesses ABB's suitability for Keytone Dairy. The report concludes by summarizing the key findings and providing references for further study. The report emphasizes the importance of activity-based costing for determining costs, as well as the application of bottom-up approach for the preparation of budgets.

MANAGERIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(a) Description of Client Company........................................................................................1

(b) Definition and Features of Activity Based Budgeting (ABB)..........................................3

(c) Difference between Activity Based Budgeting and Traditional Budgeting Systems.......7

(d) Whether Activity based Budgeting is suitable for Keytone Dairy...................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(a) Description of Client Company........................................................................................1

(b) Definition and Features of Activity Based Budgeting (ABB)..........................................3

(c) Difference between Activity Based Budgeting and Traditional Budgeting Systems.......7

(d) Whether Activity based Budgeting is suitable for Keytone Dairy...................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Managerial Accounting can also be defined as cost accounting and it can be said as it is

any process to identify, analyse, measure, communicate and interpret information to managers

for achieving the organizational goals (Prowle, 2016). The difference between managerial

accounting and financial accounting is that financial accounting helps in providing information

to parties that are outsider whereas, managerial accounting helps in decision making for

managers. This report deals with Activity Based Budgeting which is a type of Budget. In also

includes features, advantages and disadvantages of ABB. The Client Company which has been

taken is leading manufacturer of dairy products having registered in Australia. The comparison

with traditional budgets of Activity Based Budgeting is also mentioned as required by client.

MAIN BODY

(a) Description of Client Company

Name- Keytone Dairy Corporation Limited

Market Capital- 92.25 million

No. of shares- 150 million

Listing Date in Australian Stock Exchange- 18/07/2018

Registered Office- Sydney Australia

Vision Statement- They aim to provide first class products to whole world.

Keytone dairy was established in 2011 for the supply and production of fresh and

nutritional dairy products for international and local markets, manufactured and located in the

heart of the South Island (Key Stone Dairy Corporation, 2018). Keytone dairy current production

of 1500 tonne per annum has enabled them to target small and medium sized consumers.

Keytone is in expansion phase by adding their production capacity through development of

manufacturing sites. The first expansion will include a new industry of 1886 square metres and

will produce with annual capacity of 3500 tonnes. They source ingredients that are made in New

Zealand’s clean and pure environment. These products are sold by leading supermarkets as well

as used by manufacturers and retailers around the globe. They are manufacturing first class

products with premium ingredients. They are operating in dairy products segments of FMCG

products. Keystone is focused on powdered dairy industry with nutritional ingredients which is

having market of about US $21.4 billion and continue to grow. These products are produced

1

Managerial Accounting can also be defined as cost accounting and it can be said as it is

any process to identify, analyse, measure, communicate and interpret information to managers

for achieving the organizational goals (Prowle, 2016). The difference between managerial

accounting and financial accounting is that financial accounting helps in providing information

to parties that are outsider whereas, managerial accounting helps in decision making for

managers. This report deals with Activity Based Budgeting which is a type of Budget. In also

includes features, advantages and disadvantages of ABB. The Client Company which has been

taken is leading manufacturer of dairy products having registered in Australia. The comparison

with traditional budgets of Activity Based Budgeting is also mentioned as required by client.

MAIN BODY

(a) Description of Client Company

Name- Keytone Dairy Corporation Limited

Market Capital- 92.25 million

No. of shares- 150 million

Listing Date in Australian Stock Exchange- 18/07/2018

Registered Office- Sydney Australia

Vision Statement- They aim to provide first class products to whole world.

Keytone dairy was established in 2011 for the supply and production of fresh and

nutritional dairy products for international and local markets, manufactured and located in the

heart of the South Island (Key Stone Dairy Corporation, 2018). Keytone dairy current production

of 1500 tonne per annum has enabled them to target small and medium sized consumers.

Keytone is in expansion phase by adding their production capacity through development of

manufacturing sites. The first expansion will include a new industry of 1886 square metres and

will produce with annual capacity of 3500 tonnes. They source ingredients that are made in New

Zealand’s clean and pure environment. These products are sold by leading supermarkets as well

as used by manufacturers and retailers around the globe. They are manufacturing first class

products with premium ingredients. They are operating in dairy products segments of FMCG

products. Keystone is focused on powdered dairy industry with nutritional ingredients which is

having market of about US $21.4 billion and continue to grow. These products are produced

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

under two brands i.e. “Key Dairy” and “Key Health” that includes premium milk and nutrition

powders as well as some of the beauty products (Key Stone Dairy Corporation, 2018). Keystone

is selling these products in multi form of packaging for meeting the needs of consumers in

today’s scenario. In addition to their brands, they are also manufacturing for other well-known

brands around the world. Their head office is based in the heart of city which in turn facilitates

transport connectivity rail road and port allows seamless logistics for the company. Keytone is

having a license of Certification and Accreditation Administration (CNCA). So, they can easily

export to China (Key Stone Dairy Corporation, 2018). They are holding a certification from

Federation of Islamic association which helps in selling there in products in Islamic countries.

Keytone has started selling their products in international markets in two brands which are:

1. Key Dairy- It includes all powdered milk nutritional products like skim milk powder,

colostrum milk powder, Kiwi fruit Milk Powder by using high quality products taken

from fine sources of New Zealand.

2. Key Health and Face Clear- In this brand, they provide the finest health supplement

capsules and the best natural beauty products.

Keytone is capable of manufacturing number of products in their personal brands, but

they also work in contract manufacturing business (Key Stone Dairy Corporation, 2018). Their

packaging is of different types which include sachets to bulk packing for industries. They are

experts in handling the requirements and logistics of their consumers globally. They are

supplying their bulk packaging throughout Australia and Asia. Some companies for which

Keytone does contract manufacturing are:

1. Woolworth (Countdown)

2. Alpine Milk Products

3. Metro

4. NZ Delight

5. Dairy Work

6. Natural Care

7. Kobe Beef Calf Milk Replacer etc.

The Latest Updates for Keystone are:

2

powders as well as some of the beauty products (Key Stone Dairy Corporation, 2018). Keystone

is selling these products in multi form of packaging for meeting the needs of consumers in

today’s scenario. In addition to their brands, they are also manufacturing for other well-known

brands around the world. Their head office is based in the heart of city which in turn facilitates

transport connectivity rail road and port allows seamless logistics for the company. Keytone is

having a license of Certification and Accreditation Administration (CNCA). So, they can easily

export to China (Key Stone Dairy Corporation, 2018). They are holding a certification from

Federation of Islamic association which helps in selling there in products in Islamic countries.

Keytone has started selling their products in international markets in two brands which are:

1. Key Dairy- It includes all powdered milk nutritional products like skim milk powder,

colostrum milk powder, Kiwi fruit Milk Powder by using high quality products taken

from fine sources of New Zealand.

2. Key Health and Face Clear- In this brand, they provide the finest health supplement

capsules and the best natural beauty products.

Keytone is capable of manufacturing number of products in their personal brands, but

they also work in contract manufacturing business (Key Stone Dairy Corporation, 2018). Their

packaging is of different types which include sachets to bulk packing for industries. They are

experts in handling the requirements and logistics of their consumers globally. They are

supplying their bulk packaging throughout Australia and Asia. Some companies for which

Keytone does contract manufacturing are:

1. Woolworth (Countdown)

2. Alpine Milk Products

3. Metro

4. NZ Delight

5. Dairy Work

6. Natural Care

7. Kobe Beef Calf Milk Replacer etc.

The Latest Updates for Keystone are:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. They have started their construction for second manufacturing plant to increase capacity

to 5000 tonnes per annum for Keytone Dairy products. The second manufacturing unit

may start during first half of 2019.

2. Listing of Products in Shanghai First Food Mall-: As they have license to sell their

products in China, they have started selling their products in Shanghai First food mall

which is having 12 Metropolitan Scale Stores.

3. Launching of Dairy Proprietary AMF product- They have launched their first Wet

Products in brand Key Dairy, Anhydrous Milk Fat in 18Kg tin for supplying in South

East Asia and china. This milk contains 99.9% milk Fat.

To achieve their vision, they are applying different strategies which are:

1. Expanding their production capacity to provide higher volume to consumers

2. Expansion of product range through in house and contract manufacturing

3. Increasing their distribution channels

4. Exporting of products to different countries

The customer base of Keytone Dairy is not only in Australia and New Zealand but

around the globe (Key Stone Dairy Corporation, 2018). There in house products are sold across

Asia, Europe and their base countries. Keytone is working with different retailers, wholesalers

and industrial consumers.

(b) Definition and Features of Activity Based Budgeting (ABB)

Activity Based Budgeting is any system where researching, recording and analyzing is

done according to the cost of activity. This method of budgeting provides more transparency in

the process of budget (Gurcanli, 2015). ABB can also be defined as it is a planning system in

which costs are associated according to their activities and afterwards, budgeted expenditures are

compiled on the basis of level of expectation. ABB focuses on volume and types of activities that

occur within any business. The outcome of using method is that in can reduce the level of

activities that are extra provided to manufacture any product (Activity Based Budgeting, 2018).

This method can also be helpful for checking how much cost is associated with each activity and

by this, they can decide where to allocate more funds (Noreen, Brewer & Garrison, 2014).

By this method, any company can enhance their cost structure. This budgeting technique

must be applied only when Activity Based Costing method has been used to calculate cost as

identification of cost drivers would have already been done there. In this method budgets that are

3

to 5000 tonnes per annum for Keytone Dairy products. The second manufacturing unit

may start during first half of 2019.

2. Listing of Products in Shanghai First Food Mall-: As they have license to sell their

products in China, they have started selling their products in Shanghai First food mall

which is having 12 Metropolitan Scale Stores.

3. Launching of Dairy Proprietary AMF product- They have launched their first Wet

Products in brand Key Dairy, Anhydrous Milk Fat in 18Kg tin for supplying in South

East Asia and china. This milk contains 99.9% milk Fat.

To achieve their vision, they are applying different strategies which are:

1. Expanding their production capacity to provide higher volume to consumers

2. Expansion of product range through in house and contract manufacturing

3. Increasing their distribution channels

4. Exporting of products to different countries

The customer base of Keytone Dairy is not only in Australia and New Zealand but

around the globe (Key Stone Dairy Corporation, 2018). There in house products are sold across

Asia, Europe and their base countries. Keytone is working with different retailers, wholesalers

and industrial consumers.

(b) Definition and Features of Activity Based Budgeting (ABB)

Activity Based Budgeting is any system where researching, recording and analyzing is

done according to the cost of activity. This method of budgeting provides more transparency in

the process of budget (Gurcanli, 2015). ABB can also be defined as it is a planning system in

which costs are associated according to their activities and afterwards, budgeted expenditures are

compiled on the basis of level of expectation. ABB focuses on volume and types of activities that

occur within any business. The outcome of using method is that in can reduce the level of

activities that are extra provided to manufacture any product (Activity Based Budgeting, 2018).

This method can also be helpful for checking how much cost is associated with each activity and

by this, they can decide where to allocate more funds (Noreen, Brewer & Garrison, 2014).

By this method, any company can enhance their cost structure. This budgeting technique

must be applied only when Activity Based Costing method has been used to calculate cost as

identification of cost drivers would have already been done there. In this method budgets that are

3

prepared using ABC after consideration of overheads costs (Oseifuah, 2014). In, simple words

we can define it is a management tool that doesn't consider the past year budgets. The different

activities are analyzed and cost are allocated on that basis. It provides optimum utilization of

resources (Prowle, 2016). It starts with output than determines the activity that are necessary to

create that output and then determine resources that are available for it. ABB focuses on

activities that are performed rather than functions. Following are the features of Activity Based

Budgeting:

1. The total budget is divided in two types that are variable and fixed which are necessary

for providing quality information for designing a suitable budget system in any

manufacturing concern. Cost drivers are needed to be identified in a proper manner for

adding an overhead to that activity (Krumwiede & Charles, 2014). Cost drivers address

the pattern of activity for which budget has been made.

2. Different activities are identified and afterwords are ranked in order of priority

3. Resources which are available are directed towards priority to ensuring optimum results

4. Activities that are founded are evaluated as per systematic analysis of management

Example of Activity Based Budget

There are two setups for making a cell phone that are Machining and Assembling.

Managerial accountant first would be looking total amount of mobiles that are to be produced

and then he will define activities for producing cell phones. The activities can be:

1. Number of mobile phones in each batch

2. Setup time for machining

3. Setup time for Assembling

4. Hours required to do that work

So, after looking into all activities, managerial accountant can come up with effective

utilization of resources that would save money of company.

Budgets are made with two approaches

1. Top Down Approach-: In which top management decides and create budget that how

much and where to spend cost (Kazemi & Zadeh, 2015). The suggestion are taken from

managers before preparation of Budgets and are made according to objective of

organisation.

4

we can define it is a management tool that doesn't consider the past year budgets. The different

activities are analyzed and cost are allocated on that basis. It provides optimum utilization of

resources (Prowle, 2016). It starts with output than determines the activity that are necessary to

create that output and then determine resources that are available for it. ABB focuses on

activities that are performed rather than functions. Following are the features of Activity Based

Budgeting:

1. The total budget is divided in two types that are variable and fixed which are necessary

for providing quality information for designing a suitable budget system in any

manufacturing concern. Cost drivers are needed to be identified in a proper manner for

adding an overhead to that activity (Krumwiede & Charles, 2014). Cost drivers address

the pattern of activity for which budget has been made.

2. Different activities are identified and afterwords are ranked in order of priority

3. Resources which are available are directed towards priority to ensuring optimum results

4. Activities that are founded are evaluated as per systematic analysis of management

Example of Activity Based Budget

There are two setups for making a cell phone that are Machining and Assembling.

Managerial accountant first would be looking total amount of mobiles that are to be produced

and then he will define activities for producing cell phones. The activities can be:

1. Number of mobile phones in each batch

2. Setup time for machining

3. Setup time for Assembling

4. Hours required to do that work

So, after looking into all activities, managerial accountant can come up with effective

utilization of resources that would save money of company.

Budgets are made with two approaches

1. Top Down Approach-: In which top management decides and create budget that how

much and where to spend cost (Kazemi & Zadeh, 2015). The suggestion are taken from

managers before preparation of Budgets and are made according to objective of

organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Bottom Up Approach-: In this approach, managers prepare budget according to their

departments and the past experience (Prowle, 2016). This approach begins with

identification of different operations and tasks that are performed by organization. Each

unit will disclose resources and utilization of funds. The approach used by Activity Based

Budgeting is Bottom up Approach.

Following are the pros and cons of Activity Based Budgeting:

Advantages

1. This budgeting process can provide useful information to total quality management

(TQM) relating to the cost of activity that is required to any level of service (Pazarceviren

& Celayir, 2014).

2. It recognizes all cost drivers so that management can control causes that are created and it

can better be managed and understood.

3. Creates attention for cost of overhead activities that are in large proportion of total costs.

Disadvantages

1. Identifying cost driver and then allocating to different activities may be difficult.

2. Time and heavy efforts are required to establish the key activity.

3. Short term overheads can't be controllable through this method of budgeting.

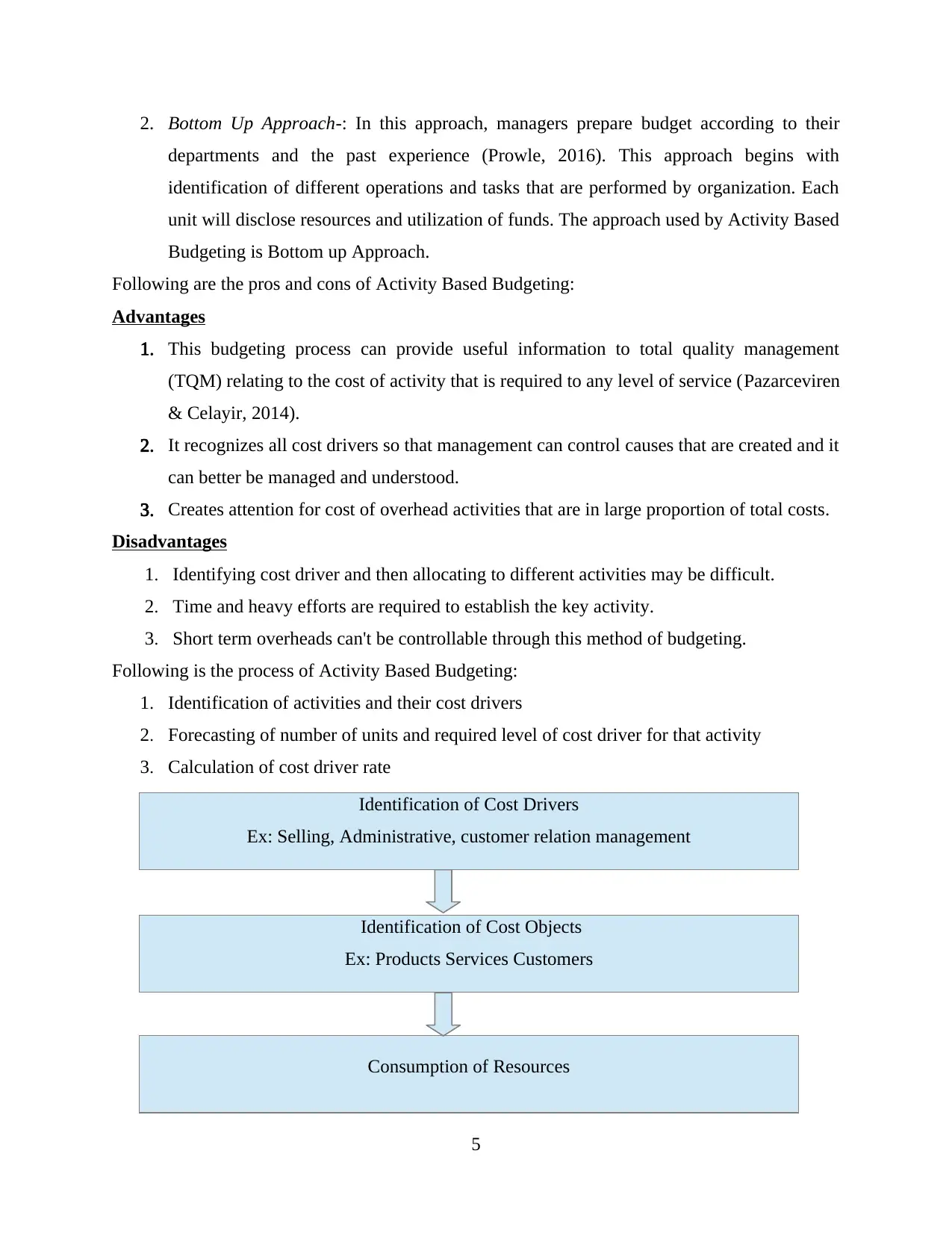

Following is the process of Activity Based Budgeting:

1. Identification of activities and their cost drivers

2. Forecasting of number of units and required level of cost driver for that activity

3. Calculation of cost driver rate

5

Identification of Cost Objects

Ex: Products Services Customers

Identification of Cost Drivers

Ex: Selling, Administrative, customer relation management

Consumption of Resources

departments and the past experience (Prowle, 2016). This approach begins with

identification of different operations and tasks that are performed by organization. Each

unit will disclose resources and utilization of funds. The approach used by Activity Based

Budgeting is Bottom up Approach.

Following are the pros and cons of Activity Based Budgeting:

Advantages

1. This budgeting process can provide useful information to total quality management

(TQM) relating to the cost of activity that is required to any level of service (Pazarceviren

& Celayir, 2014).

2. It recognizes all cost drivers so that management can control causes that are created and it

can better be managed and understood.

3. Creates attention for cost of overhead activities that are in large proportion of total costs.

Disadvantages

1. Identifying cost driver and then allocating to different activities may be difficult.

2. Time and heavy efforts are required to establish the key activity.

3. Short term overheads can't be controllable through this method of budgeting.

Following is the process of Activity Based Budgeting:

1. Identification of activities and their cost drivers

2. Forecasting of number of units and required level of cost driver for that activity

3. Calculation of cost driver rate

5

Identification of Cost Objects

Ex: Products Services Customers

Identification of Cost Drivers

Ex: Selling, Administrative, customer relation management

Consumption of Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Budgeting as a Management Tools

1. Helps in assessing actual progress for the evaluation of cost

2. Identify any critical events of projects and helps in setting up milestones for cost

3. Clarify the range and level of expenses that are incurred to stakeholders

4. Managing three key factors that are time, money and purpose of cost

5. Helps in assessing any risk that is associated with costs

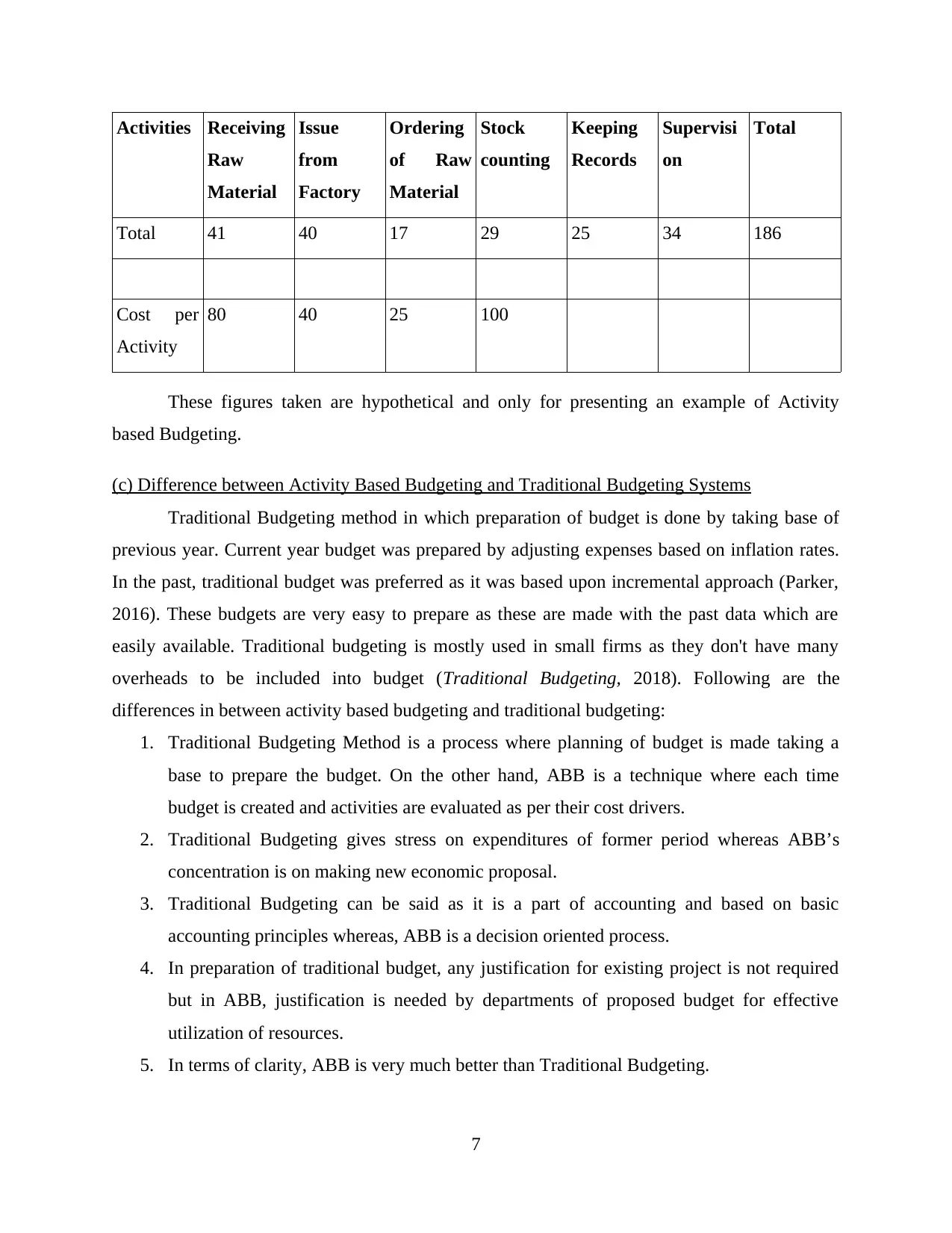

Example of Activity Based Budgeting:

Activities Receiving

Raw

Material

Issue

from

Factory

Ordering

of Raw

Material

Stock

counting

Keeping

Records

Supervisi

on

Total

Cost

Driver

No. of

Deliveries

Store

Requisitio

ns

Number of

Orders

Number of

counts

Managem

ent Salary

0 0 0 2 6 30 38

Basic

Wages

25 30 10 5 12 0 82

Overtime

Payments

10 0 0 15 0 0 25

Stationery 1 3 5 6 2 2 19

Others 5 7 2 1 5 2 22

6

Calculation of Cost per Activity

1. Helps in assessing actual progress for the evaluation of cost

2. Identify any critical events of projects and helps in setting up milestones for cost

3. Clarify the range and level of expenses that are incurred to stakeholders

4. Managing three key factors that are time, money and purpose of cost

5. Helps in assessing any risk that is associated with costs

Example of Activity Based Budgeting:

Activities Receiving

Raw

Material

Issue

from

Factory

Ordering

of Raw

Material

Stock

counting

Keeping

Records

Supervisi

on

Total

Cost

Driver

No. of

Deliveries

Store

Requisitio

ns

Number of

Orders

Number of

counts

Managem

ent Salary

0 0 0 2 6 30 38

Basic

Wages

25 30 10 5 12 0 82

Overtime

Payments

10 0 0 15 0 0 25

Stationery 1 3 5 6 2 2 19

Others 5 7 2 1 5 2 22

6

Calculation of Cost per Activity

Activities Receiving

Raw

Material

Issue

from

Factory

Ordering

of Raw

Material

Stock

counting

Keeping

Records

Supervisi

on

Total

Total 41 40 17 29 25 34 186

Cost per

Activity

80 40 25 100

These figures taken are hypothetical and only for presenting an example of Activity

based Budgeting.

(c) Difference between Activity Based Budgeting and Traditional Budgeting Systems

Traditional Budgeting method in which preparation of budget is done by taking base of

previous year. Current year budget was prepared by adjusting expenses based on inflation rates.

In the past, traditional budget was preferred as it was based upon incremental approach (Parker,

2016). These budgets are very easy to prepare as these are made with the past data which are

easily available. Traditional budgeting is mostly used in small firms as they don't have many

overheads to be included into budget (Traditional Budgeting, 2018). Following are the

differences in between activity based budgeting and traditional budgeting:

1. Traditional Budgeting Method is a process where planning of budget is made taking a

base to prepare the budget. On the other hand, ABB is a technique where each time

budget is created and activities are evaluated as per their cost drivers.

2. Traditional Budgeting gives stress on expenditures of former period whereas ABB’s

concentration is on making new economic proposal.

3. Traditional Budgeting can be said as it is a part of accounting and based on basic

accounting principles whereas, ABB is a decision oriented process.

4. In preparation of traditional budget, any justification for existing project is not required

but in ABB, justification is needed by departments of proposed budget for effective

utilization of resources.

5. In terms of clarity, ABB is very much better than Traditional Budgeting.

7

Raw

Material

Issue

from

Factory

Ordering

of Raw

Material

Stock

counting

Keeping

Records

Supervisi

on

Total

Total 41 40 17 29 25 34 186

Cost per

Activity

80 40 25 100

These figures taken are hypothetical and only for presenting an example of Activity

based Budgeting.

(c) Difference between Activity Based Budgeting and Traditional Budgeting Systems

Traditional Budgeting method in which preparation of budget is done by taking base of

previous year. Current year budget was prepared by adjusting expenses based on inflation rates.

In the past, traditional budget was preferred as it was based upon incremental approach (Parker,

2016). These budgets are very easy to prepare as these are made with the past data which are

easily available. Traditional budgeting is mostly used in small firms as they don't have many

overheads to be included into budget (Traditional Budgeting, 2018). Following are the

differences in between activity based budgeting and traditional budgeting:

1. Traditional Budgeting Method is a process where planning of budget is made taking a

base to prepare the budget. On the other hand, ABB is a technique where each time

budget is created and activities are evaluated as per their cost drivers.

2. Traditional Budgeting gives stress on expenditures of former period whereas ABB’s

concentration is on making new economic proposal.

3. Traditional Budgeting can be said as it is a part of accounting and based on basic

accounting principles whereas, ABB is a decision oriented process.

4. In preparation of traditional budget, any justification for existing project is not required

but in ABB, justification is needed by departments of proposed budget for effective

utilization of resources.

5. In terms of clarity, ABB is very much better than Traditional Budgeting.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. Activity Based Budgeting follows straightforward method whereas, traditional budgeting

follows a routine approach.

7. In traditional budgeting, the references are taken from previous spending levels and

afterwards, they consider if any inflation in prices but in ABB, the costs are based on

priority and are according to their relevance.

8. In preparation of traditional Budget figures for assumption are taken from previous years

whereas in ABB it is estimated as per different department and current market trends.

9. Traditional budgeting is not cost effective whereas, ABB’s main purpose is cost

effectiveness.

10. Traditional budgets are based on historical information that has been provided whereas,

ABB is based on estimated information.

11. Traditional budget is simpler when it comes for the preparation of budget as compared

with ABB.

12. The base of Traditional Budgets are that they are involved around accounting process of

organization whereas ABB orientation is depended upon projects.

(d) Whether Activity based Budgeting is suitable for Keytone Dairy

Activity based Budgeting is any method which provides transparency to budget process.

It is the most basic form of budgeting wherein expenses which are generated and are allocated

directly to its activity. Activity Based Budgeting is a system wherein costs that are associated

with activities are allocated according to their level of expectation. It provides a high degree of

refinement in planning of cost (Gurcanli, Bilir & Sevim, 2015). The outcome for this budgeting

is that it helps in reducing activity levels which are required to complete any process which in

turns provide profits to any company. ABB provides detailed knowledge of cost structure and

they can manage it accordingly. ABB is a long exercise to find out cost of each and every

organization as well as assess addition in value for the same (Noreen, Brewer & Garrison, 2014).

The cost drivers are responsible for defining any activity related to cost. So, cost drivers are any

factor which influence and contribute to different business operations (Activity Based Budgeting,

2018).

Determining cost drivers is essential because it allows determination of cost that is

needed to perform activity at different levels. Activity Based Budgeting is mostly found in the

cost accounting (Oseifuah, 2014). Managers of any company prepare budgets and proposition to

8

follows a routine approach.

7. In traditional budgeting, the references are taken from previous spending levels and

afterwards, they consider if any inflation in prices but in ABB, the costs are based on

priority and are according to their relevance.

8. In preparation of traditional Budget figures for assumption are taken from previous years

whereas in ABB it is estimated as per different department and current market trends.

9. Traditional budgeting is not cost effective whereas, ABB’s main purpose is cost

effectiveness.

10. Traditional budgets are based on historical information that has been provided whereas,

ABB is based on estimated information.

11. Traditional budget is simpler when it comes for the preparation of budget as compared

with ABB.

12. The base of Traditional Budgets are that they are involved around accounting process of

organization whereas ABB orientation is depended upon projects.

(d) Whether Activity based Budgeting is suitable for Keytone Dairy

Activity based Budgeting is any method which provides transparency to budget process.

It is the most basic form of budgeting wherein expenses which are generated and are allocated

directly to its activity. Activity Based Budgeting is a system wherein costs that are associated

with activities are allocated according to their level of expectation. It provides a high degree of

refinement in planning of cost (Gurcanli, Bilir & Sevim, 2015). The outcome for this budgeting

is that it helps in reducing activity levels which are required to complete any process which in

turns provide profits to any company. ABB provides detailed knowledge of cost structure and

they can manage it accordingly. ABB is a long exercise to find out cost of each and every

organization as well as assess addition in value for the same (Noreen, Brewer & Garrison, 2014).

The cost drivers are responsible for defining any activity related to cost. So, cost drivers are any

factor which influence and contribute to different business operations (Activity Based Budgeting,

2018).

Determining cost drivers is essential because it allows determination of cost that is

needed to perform activity at different levels. Activity Based Budgeting is mostly found in the

cost accounting (Oseifuah, 2014). Managers of any company prepare budgets and proposition to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

spend according to their past activities. ABB not only saves money of company but also helps in

examination of each and every activity. It allows management of any company to have increased

control in budgeting process which will help in achieving the organizational goals.

The process to prepare an activity based budget can be:

1. Determination of no. of units that are related to that activity

2. Calculate cost per unit of activity and multiply it with no. of units.

Activity Based Budgeting is totally based on Activity Based Costing as this method can

estimate different cost elements to calculate the cost of product (Kazemi & Zadeh, 2015). The

Activity Based Costing can help in:

1. Identifying and eliminating products that are not profitable and are overpriced.

2. Elimination and identification of production process that is ineffective. ABC costing

involves in identification of cost drivers to different activities and which helps in creating

activity based budgeting. So, main problem of determination of cost driver has already

been done with the help of ABC costing. Keystone Dairy Corporation must use Activity

Based Budgeting as a tool to create budgets because there are multiple activities that are

involved in production of dairy products. So, allocation of cost is necessary to every

activity that is used in the manufacturing process (Krumwiede & Charles, 2014). This

will help in knowing the actual cost of production of any product and actual cost in

different activities that are involved with it. Following can be the activities that are

involved in manufacturing process of dairy products by Key Stone Dairy-:

1. Collection of Milk-: Milk collection will be the first activity for any Keytone to start

there manufacturing process. So, different costs that are involved in it can be:

1. Salary for staff to collect the milk

2. Contract with Milk Man for providing milk

3. Keeping Records, etc.

2. Receiving of Milk-: There should be a section where milk is kept and stored. Costs

associated it with are:

1. Cold Storage for keeping milk

2. Salary and wages for operation of Cold Storage

3. Supervision, etc.

9

examination of each and every activity. It allows management of any company to have increased

control in budgeting process which will help in achieving the organizational goals.

The process to prepare an activity based budget can be:

1. Determination of no. of units that are related to that activity

2. Calculate cost per unit of activity and multiply it with no. of units.

Activity Based Budgeting is totally based on Activity Based Costing as this method can

estimate different cost elements to calculate the cost of product (Kazemi & Zadeh, 2015). The

Activity Based Costing can help in:

1. Identifying and eliminating products that are not profitable and are overpriced.

2. Elimination and identification of production process that is ineffective. ABC costing

involves in identification of cost drivers to different activities and which helps in creating

activity based budgeting. So, main problem of determination of cost driver has already

been done with the help of ABC costing. Keystone Dairy Corporation must use Activity

Based Budgeting as a tool to create budgets because there are multiple activities that are

involved in production of dairy products. So, allocation of cost is necessary to every

activity that is used in the manufacturing process (Krumwiede & Charles, 2014). This

will help in knowing the actual cost of production of any product and actual cost in

different activities that are involved with it. Following can be the activities that are

involved in manufacturing process of dairy products by Key Stone Dairy-:

1. Collection of Milk-: Milk collection will be the first activity for any Keytone to start

there manufacturing process. So, different costs that are involved in it can be:

1. Salary for staff to collect the milk

2. Contract with Milk Man for providing milk

3. Keeping Records, etc.

2. Receiving of Milk-: There should be a section where milk is kept and stored. Costs

associated it with are:

1. Cold Storage for keeping milk

2. Salary and wages for operation of Cold Storage

3. Supervision, etc.

9

3. Transformation of Liquid Products- Milk that had been purchased from market are to

be transformed or processed for making consumer milk, chocolate milk etc. The costs

that are involved here are:

1. Salary and wages for operation of plant

2. Machinery related expenses

3. Counting of Stock

4. Keeping Records Supervision, etc.

4. Processing of Milk into different products that are milk powder, Ghee, Butter etc. So,

here costs that are involved in each product will be activities for that product like for

making ghee, the cost drivers will be all the expenses which are related to manufacture

that product.

1. Record Keeping

2. Stock Counting

3. Repairs and maintenance of plant and machinery that

4. Wages and salary for staff.

5. Cost of Supervision etc.

So, with the help of Activity Based Budgeting, different cost drivers are determined for

different activities. It will help Keystone in determining the cost of each activity through which

they can use resources at optimum level and eliminate the costs that are ineffective.

CONCLUSION

From the above report it can be concluded that activity based budget is better form of

budgeting as it helps in finding different activities by which cost can be allocated. It can be seen

in the report that the cost drivers are key for activity based budgeting. This project report

concludes regarding use of Activity Based Budgeting in Keytone Dairy Corporation. Besides

this, it can be inferred that activity based budgeting will help in effective utilization of resources

in client company. Moreover, it provides high level of assistance in avoiding redundant business

activities and thereby facilitates cost reduction and profit maximization. Hence, it can be stated

that ABB is highly prominent which in turn helps in making optimal use of financial resources.

10

be transformed or processed for making consumer milk, chocolate milk etc. The costs

that are involved here are:

1. Salary and wages for operation of plant

2. Machinery related expenses

3. Counting of Stock

4. Keeping Records Supervision, etc.

4. Processing of Milk into different products that are milk powder, Ghee, Butter etc. So,

here costs that are involved in each product will be activities for that product like for

making ghee, the cost drivers will be all the expenses which are related to manufacture

that product.

1. Record Keeping

2. Stock Counting

3. Repairs and maintenance of plant and machinery that

4. Wages and salary for staff.

5. Cost of Supervision etc.

So, with the help of Activity Based Budgeting, different cost drivers are determined for

different activities. It will help Keystone in determining the cost of each activity through which

they can use resources at optimum level and eliminate the costs that are ineffective.

CONCLUSION

From the above report it can be concluded that activity based budget is better form of

budgeting as it helps in finding different activities by which cost can be allocated. It can be seen

in the report that the cost drivers are key for activity based budgeting. This project report

concludes regarding use of Activity Based Budgeting in Keytone Dairy Corporation. Besides

this, it can be inferred that activity based budgeting will help in effective utilization of resources

in client company. Moreover, it provides high level of assistance in avoiding redundant business

activities and thereby facilitates cost reduction and profit maximization. Hence, it can be stated

that ABB is highly prominent which in turn helps in making optimal use of financial resources.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.