Managerial Accounting Report: Activity-Based Budgeting Analysis

VerifiedAdded on 2022/11/13

|18

|4217

|241

Report

AI Summary

This report provides an overview of activity-based budgeting (ABB) for the CEO of an ASX-listed organization, focusing on Adelaide Brighton Cement. It begins with a description of the company's business operations, followed by an explanation of ABB and its key features. The report then contrasts ABB with traditional budgeting systems, highlighting differences in cost assignment and allocation methods. The analysis concludes by assessing the suitability of ABB for Adelaide Brighton Cement, considering its potential benefits in terms of cost savings, competitive advantage, and improved operational efficiency. The report emphasizes ABB's ability to eliminate unnecessary activities, enhance customer relationships, and provide better insights into resource allocation and performance measurement, making it a valuable tool for managerial decision-making in the context of the chosen company.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report intends to provide a brief overview of activity-based budgeting to the CEO

of an ASX listed organisation. Therefore, Adelaide Brighton Cement is chosen as the

organisation that operates within Australian manufacturing sector. With the help of activity-

based budgeting system, it becomes possible to remove all kinds of unessential activities,

which assists the business in saving its costs. The saved cost leads to the production of

products and services at lower cost compared to that of its rivals. It could be observed that

both ABB and traditional budgeting systems conduct costing of a cost object, which might be

a component, finished or semi-finished item, activity, customer, process including a group of

activities, supplier and others. However, the costing methodology in the two systems varies

from each other. Finally, it has been evaluated that activity-based budgeting system is

suitable for Adelaide Brighton Cement.

Executive Summary:

The current report intends to provide a brief overview of activity-based budgeting to the CEO

of an ASX listed organisation. Therefore, Adelaide Brighton Cement is chosen as the

organisation that operates within Australian manufacturing sector. With the help of activity-

based budgeting system, it becomes possible to remove all kinds of unessential activities,

which assists the business in saving its costs. The saved cost leads to the production of

products and services at lower cost compared to that of its rivals. It could be observed that

both ABB and traditional budgeting systems conduct costing of a cost object, which might be

a component, finished or semi-finished item, activity, customer, process including a group of

activities, supplier and others. However, the costing methodology in the two systems varies

from each other. Finally, it has been evaluated that activity-based budgeting system is

suitable for Adelaide Brighton Cement.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

a) Description of the business of Adelaide Brighton Cement:...................................................3

b) Description of activity-based budgeting (ABB) and its features:..........................................4

c) Difference between ABB and traditional budgeting systems:...............................................7

d) Discussion on whether ABB is suitable to Adelaide Brighton Cement:.............................11

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................3

a) Description of the business of Adelaide Brighton Cement:...................................................3

b) Description of activity-based budgeting (ABB) and its features:..........................................4

c) Difference between ABB and traditional budgeting systems:...............................................7

d) Discussion on whether ABB is suitable to Adelaide Brighton Cement:.............................11

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

For undertaking sound decisions along with coordinating the actions and decisions of

different departments, the business organisations have to develop a plan for profitability.

Generally, an organisation develops a budget annually, which, after approval, would become

the annual budget (Brewer, Garrison and Noreen 2015). The current report intends to provide

a brief overview of activity-based budgeting to the CEO of an ASX listed organisation.

Therefore, Adelaide Brighton Cement is chosen as the organisation that operates within

Australian manufacturing sector. The report is divided into four different sections. Firstly, a

brief overview of the business operations of Adelaide Brighton Cement has been provided in

this paper. The second part would include a description of activity-based budgeting and its

features. Thirdly, adequate discussion has been made regarding the dissimilarities between

ABB and traditional budgeting systems. Finally, the report would shed light on analysing the

suitability of ABB in Adelaide Brighton Cement.

a) Description of the business of Adelaide Brighton Cement:

Adelaide Brighton Cement is established in 1911 and it is a leading producer of

cement, lime as well as pre-packaged dry-blended products, which are engineered

particularly for fulfilling the needs of the customers. It mainly operates within the lime and

cement division of Adelaide Brighton Limited that has above 1,600 staffs throughout

Australia. Adelaide Brighton Limited has commenced its operations back in 1882 and at

present it is an S&P/ASX 100 organisation having primary activities including the production

of cement, clinker, premixed concrete, lime, concrete masonry and aggregate products

(Adelaidebrighton.com.au 2019).

Introduction:

For undertaking sound decisions along with coordinating the actions and decisions of

different departments, the business organisations have to develop a plan for profitability.

Generally, an organisation develops a budget annually, which, after approval, would become

the annual budget (Brewer, Garrison and Noreen 2015). The current report intends to provide

a brief overview of activity-based budgeting to the CEO of an ASX listed organisation.

Therefore, Adelaide Brighton Cement is chosen as the organisation that operates within

Australian manufacturing sector. The report is divided into four different sections. Firstly, a

brief overview of the business operations of Adelaide Brighton Cement has been provided in

this paper. The second part would include a description of activity-based budgeting and its

features. Thirdly, adequate discussion has been made regarding the dissimilarities between

ABB and traditional budgeting systems. Finally, the report would shed light on analysing the

suitability of ABB in Adelaide Brighton Cement.

a) Description of the business of Adelaide Brighton Cement:

Adelaide Brighton Cement is established in 1911 and it is a leading producer of

cement, lime as well as pre-packaged dry-blended products, which are engineered

particularly for fulfilling the needs of the customers. It mainly operates within the lime and

cement division of Adelaide Brighton Limited that has above 1,600 staffs throughout

Australia. Adelaide Brighton Limited has commenced its operations back in 1882 and at

present it is an S&P/ASX 100 organisation having primary activities including the production

of cement, clinker, premixed concrete, lime, concrete masonry and aggregate products

(Adelaidebrighton.com.au 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Adelaide Brighton Cement has diversified operational base facilitating prompt supply

to the customers along with allowing for strategic balance of production capacity for

fulfilling demands throughout the nation. As a result, it assists the organisation in offering a

supply package, which is supported flexibly with storage, transportation and supply logistics

for places across Asia and Australia. The diversified operational efficiency of the

organisation assists it in providing turn-key solutions, which assures the basic objective of

going beyond the expectations of the customers (Adelaidebrighton.com.au 2019).

b) Description of activity-based budgeting (ABB) and its features:

Activity-based budgeting (ABB) could be defined as the method of budgeting where

budgets are formulated with the help of activity-based costing (ABC) system after taking into

account the overhead expenses. More precisely, ABB is a tool of management accounting

that does not take into account the budget of the previous year for arriving at the budget of

the existing year (Apostolou et al. 2019). Instead, the activities incurring the costs are

analysed thoroughly and accordingly, adequate research is conducted on the same.

Depending on the research outcome, there is allocation of resources to an activity. ABB is

conducted for bringing efficacy in the activities of an organisation. After the cost drivers are

justified, there is preparation of budgets. Hence, activity-based budgeting is not function-

oriented; instead, it is activity-oriented.

ABB is deemed to possess a number of features, which are summarised briefly as

follows:

Evaluation:

Adelaide Brighton Cement has diversified operational base facilitating prompt supply

to the customers along with allowing for strategic balance of production capacity for

fulfilling demands throughout the nation. As a result, it assists the organisation in offering a

supply package, which is supported flexibly with storage, transportation and supply logistics

for places across Asia and Australia. The diversified operational efficiency of the

organisation assists it in providing turn-key solutions, which assures the basic objective of

going beyond the expectations of the customers (Adelaidebrighton.com.au 2019).

b) Description of activity-based budgeting (ABB) and its features:

Activity-based budgeting (ABB) could be defined as the method of budgeting where

budgets are formulated with the help of activity-based costing (ABC) system after taking into

account the overhead expenses. More precisely, ABB is a tool of management accounting

that does not take into account the budget of the previous year for arriving at the budget of

the existing year (Apostolou et al. 2019). Instead, the activities incurring the costs are

analysed thoroughly and accordingly, adequate research is conducted on the same.

Depending on the research outcome, there is allocation of resources to an activity. ABB is

conducted for bringing efficacy in the activities of an organisation. After the cost drivers are

justified, there is preparation of budgets. Hence, activity-based budgeting is not function-

oriented; instead, it is activity-oriented.

ABB is deemed to possess a number of features, which are summarised briefly as

follows:

Evaluation:

5MANAGERIAL ACCOUNTING

This method of budgeting analyses all cost drivers. It takes into account all the steps

associated with an activity. There is elimination of irrelevant activities and only the essential

activities form portion of the business.

Competitive edge:

With the help of activity-based budgeting system, it becomes possible to remove all

kinds of unessential activities, which assists the business in saving its costs (Apostolou et al.

2015). The saved cost leads to the production of products and services at lower cost

compared to that of its rivals. It aids the organisation in gaining competitive advantage in the

market.

Business as a unit:

With the help of activity-based budgeting technique, the business could be viewed in

the form of a single unit and not as departments. The top management or the managers

formulate the budget for the overall business unit by not bearing in mind any single

department as made in the other budgeting methods (Cardoş 2014).

Removal of bottlenecks:

The budgets formulated under activity-based budgeting system are made after

conduction of adequate research and analysis. The use of such research assists in the

elimination of all unessential business activities of an organisation (Collier 2015). By

conducting the same, it becomes possible for the business organisation to eradicate all kinds

of bottlenecks related to an activity and there would be smooth conduction of the business

functions.

Improvement in relationship:

This method of budgeting analyses all cost drivers. It takes into account all the steps

associated with an activity. There is elimination of irrelevant activities and only the essential

activities form portion of the business.

Competitive edge:

With the help of activity-based budgeting system, it becomes possible to remove all

kinds of unessential activities, which assists the business in saving its costs (Apostolou et al.

2015). The saved cost leads to the production of products and services at lower cost

compared to that of its rivals. It aids the organisation in gaining competitive advantage in the

market.

Business as a unit:

With the help of activity-based budgeting technique, the business could be viewed in

the form of a single unit and not as departments. The top management or the managers

formulate the budget for the overall business unit by not bearing in mind any single

department as made in the other budgeting methods (Cardoş 2014).

Removal of bottlenecks:

The budgets formulated under activity-based budgeting system are made after

conduction of adequate research and analysis. The use of such research assists in the

elimination of all unessential business activities of an organisation (Collier 2015). By

conducting the same, it becomes possible for the business organisation to eradicate all kinds

of bottlenecks related to an activity and there would be smooth conduction of the business

functions.

Improvement in relationship:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

By using activity-based budgeting system, it becomes possible for an organisation to

enhance the relationship with its customers. The primary goal of the budgeting system is to

eradicate all unessential activities so that best quality products could be served to the

customers at the best prices (Elmassri, Harris and Carter 2016). This has indirect enforcement

on the staffs of the organisation for serving the customers in the most suitable manner along

with assuring customer satisfaction. This, in turn, would help in enhancing the relationship

between the organisation and its customers.

Discussion on operational terms:

Since activity-based budgeting system provides a clear overview of the relationship

between resources and activities, it could help the staffs and managers in understanding and

communicating budget information in tangible non-financial terms. As a result, they could

have a better understanding of the requirements for further improvements and accordingly,

they could perform better in their jobs (Gitman, Juchau and Flanagan 2015). With the

improvement in the flow of resources and activities, it becomes easier to analyse performance

by specifying the respective personnel responsible for certain activities that could have

overlapped in several departments. Thus, the managers could be highly agile when it comes

to contingency planning, performance measurement, decision-making and evaluation by

utilising this budgeting system.

Increased traceability and transparency:

By using sophisticated operating model, a richer group of tools could be enabled for

balance of capacity. It becomes simple to alter demands or changes in the allocated resource

amounts and it would be easier in adjusting the activity or rate of consumption resources

owing to the resource capacity analysis made in this kind of budgeting system (Hoque 2018).

Such increased traceability and transparency related to consumption of resources could result

By using activity-based budgeting system, it becomes possible for an organisation to

enhance the relationship with its customers. The primary goal of the budgeting system is to

eradicate all unessential activities so that best quality products could be served to the

customers at the best prices (Elmassri, Harris and Carter 2016). This has indirect enforcement

on the staffs of the organisation for serving the customers in the most suitable manner along

with assuring customer satisfaction. This, in turn, would help in enhancing the relationship

between the organisation and its customers.

Discussion on operational terms:

Since activity-based budgeting system provides a clear overview of the relationship

between resources and activities, it could help the staffs and managers in understanding and

communicating budget information in tangible non-financial terms. As a result, they could

have a better understanding of the requirements for further improvements and accordingly,

they could perform better in their jobs (Gitman, Juchau and Flanagan 2015). With the

improvement in the flow of resources and activities, it becomes easier to analyse performance

by specifying the respective personnel responsible for certain activities that could have

overlapped in several departments. Thus, the managers could be highly agile when it comes

to contingency planning, performance measurement, decision-making and evaluation by

utilising this budgeting system.

Increased traceability and transparency:

By using sophisticated operating model, a richer group of tools could be enabled for

balance of capacity. It becomes simple to alter demands or changes in the allocated resource

amounts and it would be easier in adjusting the activity or rate of consumption resources

owing to the resource capacity analysis made in this kind of budgeting system (Hoque 2018).

Such increased traceability and transparency related to consumption of resources could result

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

allow the business organisations in detecting the capacity issues through which it is possible

to make timely adjustments.

c) Difference between ABB and traditional budgeting systems:

Certain differences are deemed to be observed between activity-based budgeting

system and traditional budgeting system and they are summarised briefly as follows:

Assignment of cost:

It could be observed that both ABB and traditional budgeting systems conduct costing

of a cost object, which might be a component, finished or semi-finished item, activity,

customer, process including a group of activities, supplier and others (Kaplan and Atkinson

2015). However, the costing methodology in the two systems varies from each other. For

example, it is assumed that a particular component consumes specific amount of material and

labour, which could be measured effectively. The material and labour costing treatment is

same under both the methods, as it is obtained by multiplying total material consumed by the

component by the unit price of the material and by multiplying the overall labour hours that

the component has utilised by labour rate per hour. However, in ABB, the proportion of

overheads would be added, which is consumed by the component. In the conventional

budgeting system, it is conducted by loading a portion of the overall overhead cost of the

organisation to the component (Kotas 2014).

Generally, the proportion is either percentage of labour cost or the proportion of

material cost of the component or machine hours or labour in contrast to the total labour cost

or material cost or overall labour hours or machine hours of the organisation. Hence, there is

absence of any rationale to the same, as the component might not have attracted actually the

overheads in this procedure of percentages. However, in ABB, the actual overhead activities

allow the business organisations in detecting the capacity issues through which it is possible

to make timely adjustments.

c) Difference between ABB and traditional budgeting systems:

Certain differences are deemed to be observed between activity-based budgeting

system and traditional budgeting system and they are summarised briefly as follows:

Assignment of cost:

It could be observed that both ABB and traditional budgeting systems conduct costing

of a cost object, which might be a component, finished or semi-finished item, activity,

customer, process including a group of activities, supplier and others (Kaplan and Atkinson

2015). However, the costing methodology in the two systems varies from each other. For

example, it is assumed that a particular component consumes specific amount of material and

labour, which could be measured effectively. The material and labour costing treatment is

same under both the methods, as it is obtained by multiplying total material consumed by the

component by the unit price of the material and by multiplying the overall labour hours that

the component has utilised by labour rate per hour. However, in ABB, the proportion of

overheads would be added, which is consumed by the component. In the conventional

budgeting system, it is conducted by loading a portion of the overall overhead cost of the

organisation to the component (Kotas 2014).

Generally, the proportion is either percentage of labour cost or the proportion of

material cost of the component or machine hours or labour in contrast to the total labour cost

or material cost or overall labour hours or machine hours of the organisation. Hence, there is

absence of any rationale to the same, as the component might not have attracted actually the

overheads in this procedure of percentages. However, in ABB, the actual overhead activities

8MANAGERIAL ACCOUNTING

need to be identified, which are carried out on the component. All overhead activities are

gauged in terms of cost drivers or in other words, the number of units of the cost driver that

the component has used actually (Kravet 2014). On each overhead activity, the overall cost of

that overhead activity is gathered at the organisational level. This is denoted by overhead cost

pool related to the activity. In addition, the cost per unit of each activity driver is calculated

by dividing the overhead cost pool of that activity by the overall units of the cost driver,

which are utilised at the organisational level.

This would provide the actual cost per unit of the cost driver related to that activity.

By multiplying the cost driver units that the component has used by using the cost driver rate,

it is possible to obtain the actual cost of overhead activity conducted on the component

(Mahieu, Vroman and Calluy 2015). In this way, there is allocation of overhead cost to the

component for all the overhead activities used by the component.

Therefore, ABB has separate overhead cost pools for each activity at the

organisational level. More precisely, each overhead activity has cost driver having

measurement unit and all cost drivers have unit costs or the cost driver costs. As a result,

there is improvement in product costing procedure under activity-based budgeting in contrast

to traditional budgeting, since it realises that the fixed overhead expenses vary in percentage

to changes besides the units of production (Miller-Nobles, Mattison and Matsumura 2016).

Two-stage allocation:

It has been identified that both traditional budgeting system and activity-based

budgeting system are involved in following two-stage allocation system. In the initial phase,

under traditional budgeting system, there is allocation of overhead costs to the production

departments (Narayanaswamy 2017). However, in the initial stage, under activity-based

budgeting system, there is allocation of overhead costs to each significant activity and not the

need to be identified, which are carried out on the component. All overhead activities are

gauged in terms of cost drivers or in other words, the number of units of the cost driver that

the component has used actually (Kravet 2014). On each overhead activity, the overall cost of

that overhead activity is gathered at the organisational level. This is denoted by overhead cost

pool related to the activity. In addition, the cost per unit of each activity driver is calculated

by dividing the overhead cost pool of that activity by the overall units of the cost driver,

which are utilised at the organisational level.

This would provide the actual cost per unit of the cost driver related to that activity.

By multiplying the cost driver units that the component has used by using the cost driver rate,

it is possible to obtain the actual cost of overhead activity conducted on the component

(Mahieu, Vroman and Calluy 2015). In this way, there is allocation of overhead cost to the

component for all the overhead activities used by the component.

Therefore, ABB has separate overhead cost pools for each activity at the

organisational level. More precisely, each overhead activity has cost driver having

measurement unit and all cost drivers have unit costs or the cost driver costs. As a result,

there is improvement in product costing procedure under activity-based budgeting in contrast

to traditional budgeting, since it realises that the fixed overhead expenses vary in percentage

to changes besides the units of production (Miller-Nobles, Mattison and Matsumura 2016).

Two-stage allocation:

It has been identified that both traditional budgeting system and activity-based

budgeting system are involved in following two-stage allocation system. In the initial phase,

under traditional budgeting system, there is allocation of overhead costs to the production

departments (Narayanaswamy 2017). However, in the initial stage, under activity-based

budgeting system, there is allocation of overhead costs to each significant activity and not the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

departments. Under the traditional budgeting system, there is pooling or collection of

department-wise overhead. However, under activity-based budgeting system, there is creation

of various cost centres or activity-based cost pools.

Under traditional budgeting system, there is allocation or reapportionment of service

department costs to the production departments and therefore, in this system, there is

existence of only fewer cost pools in the final stage. However, there is creation of separate

cost pools under activity-based budgeting system for the service activities and there is direct

allocation of overhead costs of these service activities to particular products by the

application of the cost driver rates (Oseifuah 2014). Therefore, the ABB system eliminates

the need of allocating or reapportioning service department overheads.

Usage of historical costs:

Another difference between traditional budgeting system and activity-based budgeting

system is related to historical orientation. It is usual for any organisation to use the actual

historical cost as the base in order to develop manufacturing cost standards. Such historical

costs often constitute of rework, waste, duplication, redundancy and inefficiency

(Pazarceviren and Celayir 2014).

The acceptance of historical costs as provided and representing such costs in

standards does not provide support to the continual improvement. In a competitive condition,

in which the competitors are proactive to remove waste along with enhancing activities, there

is chance for an organisation to go out of business at the time of fulfilling its standards

(Ponisciakova, Gogolova and Ivankova 2015). Despite the fact that activity-based budgeting

is computed with the help of historical resource costs, difference in orientation could be

found. The proponents of the ABB system are worried regarding future competitive positions

departments. Under the traditional budgeting system, there is pooling or collection of

department-wise overhead. However, under activity-based budgeting system, there is creation

of various cost centres or activity-based cost pools.

Under traditional budgeting system, there is allocation or reapportionment of service

department costs to the production departments and therefore, in this system, there is

existence of only fewer cost pools in the final stage. However, there is creation of separate

cost pools under activity-based budgeting system for the service activities and there is direct

allocation of overhead costs of these service activities to particular products by the

application of the cost driver rates (Oseifuah 2014). Therefore, the ABB system eliminates

the need of allocating or reapportioning service department overheads.

Usage of historical costs:

Another difference between traditional budgeting system and activity-based budgeting

system is related to historical orientation. It is usual for any organisation to use the actual

historical cost as the base in order to develop manufacturing cost standards. Such historical

costs often constitute of rework, waste, duplication, redundancy and inefficiency

(Pazarceviren and Celayir 2014).

The acceptance of historical costs as provided and representing such costs in

standards does not provide support to the continual improvement. In a competitive condition,

in which the competitors are proactive to remove waste along with enhancing activities, there

is chance for an organisation to go out of business at the time of fulfilling its standards

(Ponisciakova, Gogolova and Ivankova 2015). Despite the fact that activity-based budgeting

is computed with the help of historical resource costs, difference in orientation could be

found. The proponents of the ABB system are worried regarding future competitive positions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

and they only consider the historical cost only in the form of a baseline in relation to

improvement.

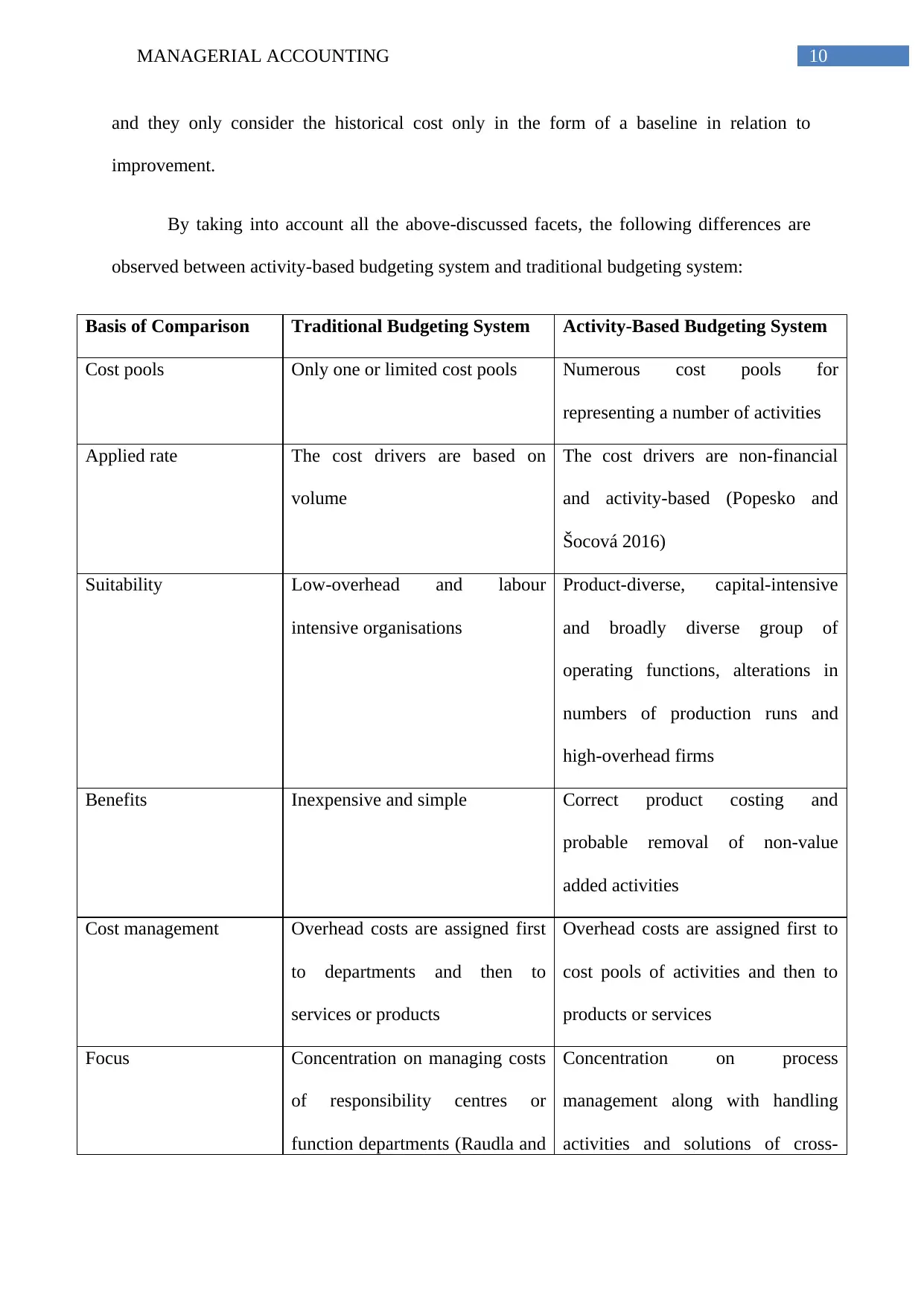

By taking into account all the above-discussed facets, the following differences are

observed between activity-based budgeting system and traditional budgeting system:

Basis of Comparison Traditional Budgeting System Activity-Based Budgeting System

Cost pools Only one or limited cost pools Numerous cost pools for

representing a number of activities

Applied rate The cost drivers are based on

volume

The cost drivers are non-financial

and activity-based (Popesko and

Šocová 2016)

Suitability Low-overhead and labour

intensive organisations

Product-diverse, capital-intensive

and broadly diverse group of

operating functions, alterations in

numbers of production runs and

high-overhead firms

Benefits Inexpensive and simple Correct product costing and

probable removal of non-value

added activities

Cost management Overhead costs are assigned first

to departments and then to

services or products

Overhead costs are assigned first to

cost pools of activities and then to

products or services

Focus Concentration on managing costs

of responsibility centres or

function departments (Raudla and

Concentration on process

management along with handling

activities and solutions of cross-

and they only consider the historical cost only in the form of a baseline in relation to

improvement.

By taking into account all the above-discussed facets, the following differences are

observed between activity-based budgeting system and traditional budgeting system:

Basis of Comparison Traditional Budgeting System Activity-Based Budgeting System

Cost pools Only one or limited cost pools Numerous cost pools for

representing a number of activities

Applied rate The cost drivers are based on

volume

The cost drivers are non-financial

and activity-based (Popesko and

Šocová 2016)

Suitability Low-overhead and labour

intensive organisations

Product-diverse, capital-intensive

and broadly diverse group of

operating functions, alterations in

numbers of production runs and

high-overhead firms

Benefits Inexpensive and simple Correct product costing and

probable removal of non-value

added activities

Cost management Overhead costs are assigned first

to departments and then to

services or products

Overhead costs are assigned first to

cost pools of activities and then to

products or services

Focus Concentration on managing costs

of responsibility centres or

function departments (Raudla and

Concentration on process

management along with handling

activities and solutions of cross-

11MANAGERIAL ACCOUNTING

Savi 2015) functional issues

d) Discussion on whether ABB is suitable to Adelaide Brighton Cement:

Activity Based Budgeting management accounting technique is considered to be

suitable for Adelaide Brighton Cement as it facilitates in recognising the activities of the

company along with allotting the cost of all the activity source to every cement products as

per their actual utilisation (Weygandt et al. 2018). Through implementing the ABB the

company will be able to correctly anticipate the costs related with its products so that the

organisation can eliminate the ones that are not advantageous along with decreasing the

prices for the ones that are costly. The ABB technique implemented by Adelaide Brighton

Cement Company can also be beneficial for it in allocating its resource costs through

activities to products that are offered to the consumers. The important purpose of this

technique used by the company is to effectively understand the product as well as consumer

cost and the profitability (Smith 2017). ABB is also deemed to be suitable to implement by

Adelaide Brighton Cement for attaining support in its strategic decisions like outsourcing,

pricing, identification and management of the process development approaches in the

company. It is deemed that if the cement company considers implementing ABB in their

management accounting process it can facilitate the company in attaining reliability and

accuracy in its product cost determination through focussing in the cause and effect

relationship within the cost incurrence (Shields 2015).

Implementation of ABB can also facilitate Adelaide Brighton Cement Company in

recognising that the activities are the root causes of increasing costs and not the products and

it is the products that devour activities. In the advanced cement manufacturing environment

of Adelaide Brighton Cement Company along with the technology that supports functions

Savi 2015) functional issues

d) Discussion on whether ABB is suitable to Adelaide Brighton Cement:

Activity Based Budgeting management accounting technique is considered to be

suitable for Adelaide Brighton Cement as it facilitates in recognising the activities of the

company along with allotting the cost of all the activity source to every cement products as

per their actual utilisation (Weygandt et al. 2018). Through implementing the ABB the

company will be able to correctly anticipate the costs related with its products so that the

organisation can eliminate the ones that are not advantageous along with decreasing the

prices for the ones that are costly. The ABB technique implemented by Adelaide Brighton

Cement Company can also be beneficial for it in allocating its resource costs through

activities to products that are offered to the consumers. The important purpose of this

technique used by the company is to effectively understand the product as well as consumer

cost and the profitability (Smith 2017). ABB is also deemed to be suitable to implement by

Adelaide Brighton Cement for attaining support in its strategic decisions like outsourcing,

pricing, identification and management of the process development approaches in the

company. It is deemed that if the cement company considers implementing ABB in their

management accounting process it can facilitate the company in attaining reliability and

accuracy in its product cost determination through focussing in the cause and effect

relationship within the cost incurrence (Shields 2015).

Implementation of ABB can also facilitate Adelaide Brighton Cement Company in

recognising that the activities are the root causes of increasing costs and not the products and

it is the products that devour activities. In the advanced cement manufacturing environment

of Adelaide Brighton Cement Company along with the technology that supports functions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.