ABC Model: Costing Analysis for Corporate Travel Management

VerifiedAdded on 2021/06/17

|12

|3017

|32

Report

AI Summary

This report provides an analysis of the Activity Based Costing (ABC) model and its application to Corporate Travel Management (CTM), an Australian-based company. The report begins with an executive summary, followed by an introduction to the ABC model, defining its meaning and key features. The report then aligns the ABC model with CTM's mission, objectives, and corporate strategies, including growth, innovation, productivity, and leveraging scale. It identifies the benefits of applying the ABC model within CTM, particularly in improving cost allocation accuracy. Recommendations are provided for the implementation of the ABC model, along with an alternative management accounting tool, Total Quality Management (TQM). The report concludes by summarizing the findings and emphasizing the importance of ABC in enhancing CTM's financial management and strategic decision-making.

Corp Travel Company

ACTIVITY BASED COSTING

MODEL

Costing Methods

Name of the Author

ACTIVITY BASED COSTING

MODEL

Costing Methods

Name of the Author

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The current report focuses on the implications that the Activity Based Costing model

technique can have on the information provided to the top management under managerial

accounting. For the same, the example of a leading Australian company, Corporate Travel

Management is taken. By management team, it means CEO and the other senior managers.

The initial part of report emphasises on the meaning that the ABC model pertains to and the

features that adorn it. Strategies and current goals of the above-mentioned company are

identified along with its mission and objectives.

The current report focuses on the implications that the Activity Based Costing model

technique can have on the information provided to the top management under managerial

accounting. For the same, the example of a leading Australian company, Corporate Travel

Management is taken. By management team, it means CEO and the other senior managers.

The initial part of report emphasises on the meaning that the ABC model pertains to and the

features that adorn it. Strategies and current goals of the above-mentioned company are

identified along with its mission and objectives.

Table of Contents

INTRODUCTION.................................................................................................................................3

ACTIVITY BASED COSTING MODEL.............................................................................................3

MEANING........................................................................................................................................3

FEATURES OF ACTIVITY BASED COSTING.............................................................................3

ALIGNING ABC MODEL ACCORDING TO MISSION AND STRATEGIES OF CORPORATE

TRAVEL MANAGEMENT..................................................................................................................4

MISSION AND OBJECTIVES OF COMPANY..............................................................................4

STRATEGIES OF CORPORATE TRAVEL MANAGEMENT.......................................................4

CONTINUED GROWTH AND SERVICE EXCELLENCE........................................................5

CLIENT FACING INNOVATION...............................................................................................5

PRODUCTIVITY AND INTERNAL INNOVATION..................................................................5

LEVERAGING SCALE AND GEOGRAPHY.............................................................................5

THEIR PEOPLE............................................................................................................................5

BENEFITS IN APPLYING ABC MODEL IN CORPORATE TRAVEL MANAGEMENT...........6

RECOMMENDATION FOR IMPLEMENTATION OF ABC MODEL IN CTM...............................7

ALTERNATE MANAGEMENT ACCOUNTING TOOL RECOMMENDED....................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

INTRODUCTION.................................................................................................................................3

ACTIVITY BASED COSTING MODEL.............................................................................................3

MEANING........................................................................................................................................3

FEATURES OF ACTIVITY BASED COSTING.............................................................................3

ALIGNING ABC MODEL ACCORDING TO MISSION AND STRATEGIES OF CORPORATE

TRAVEL MANAGEMENT..................................................................................................................4

MISSION AND OBJECTIVES OF COMPANY..............................................................................4

STRATEGIES OF CORPORATE TRAVEL MANAGEMENT.......................................................4

CONTINUED GROWTH AND SERVICE EXCELLENCE........................................................5

CLIENT FACING INNOVATION...............................................................................................5

PRODUCTIVITY AND INTERNAL INNOVATION..................................................................5

LEVERAGING SCALE AND GEOGRAPHY.............................................................................5

THEIR PEOPLE............................................................................................................................5

BENEFITS IN APPLYING ABC MODEL IN CORPORATE TRAVEL MANAGEMENT...........6

RECOMMENDATION FOR IMPLEMENTATION OF ABC MODEL IN CTM...............................7

ALTERNATE MANAGEMENT ACCOUNTING TOOL RECOMMENDED....................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Activity Based Costing is the most celebrated tool in managerial accounting, especially in the

manufacturing sector. As the name suggests, the cost allocation under this technique is based

on the relationship between the activities that the concern does and the respective products. It

is an improved method over the traditional approaches of cost allocations. In this approach,

the level of activity is the measure of the distribution of indirect costs, as the direct costs are

already attributable to the specific activities or product. In the report under study, the

company chosen for analysis is Corporate Travel Management, one of global giant corporate

that customises the travel needs of businesses. This report highlights the company’s missions

and objectives with its corporate strategies. The role of Activity Based Costing model in

improving the management accounting and the recommendations related to the same are

versed. The ABC model is incorporated to understand how it can help the corporate to

achieve its corporate strategies and recommendations for the same are given in the second

part of the report, based on the research findings. In the concluding section,

ACTIVITY BASED COSTING MODEL

MEANING

Any kind of activity or production or business incurs both direct and indirect costs in the

process. Indirect cost is not directly attributable to any output, are required to be divided on

some justified basis. Activity Based Costing has come as a saviour by judicially attributing

cost based on resources used by each activity and the total cost incurred. Various bases are

used as a base for distribution and are known as cost drivers, e.g. power consumed, machine

setups, maintenance request, production order etc. Here in this method, the machine hours or

direct labour hours are not used as a basis for allocation. It is the much-improved manner of

disbursement as it’s directly linked to the extent a department or section performs an activity

which generates a cost (Lee, & Kao, 2011). It is observed that if the proper ABC model

costing is used then it will increase the overall outcomes and efficiency of the business at

large.

Activity Based Costing is the most celebrated tool in managerial accounting, especially in the

manufacturing sector. As the name suggests, the cost allocation under this technique is based

on the relationship between the activities that the concern does and the respective products. It

is an improved method over the traditional approaches of cost allocations. In this approach,

the level of activity is the measure of the distribution of indirect costs, as the direct costs are

already attributable to the specific activities or product. In the report under study, the

company chosen for analysis is Corporate Travel Management, one of global giant corporate

that customises the travel needs of businesses. This report highlights the company’s missions

and objectives with its corporate strategies. The role of Activity Based Costing model in

improving the management accounting and the recommendations related to the same are

versed. The ABC model is incorporated to understand how it can help the corporate to

achieve its corporate strategies and recommendations for the same are given in the second

part of the report, based on the research findings. In the concluding section,

ACTIVITY BASED COSTING MODEL

MEANING

Any kind of activity or production or business incurs both direct and indirect costs in the

process. Indirect cost is not directly attributable to any output, are required to be divided on

some justified basis. Activity Based Costing has come as a saviour by judicially attributing

cost based on resources used by each activity and the total cost incurred. Various bases are

used as a base for distribution and are known as cost drivers, e.g. power consumed, machine

setups, maintenance request, production order etc. Here in this method, the machine hours or

direct labour hours are not used as a basis for allocation. It is the much-improved manner of

disbursement as it’s directly linked to the extent a department or section performs an activity

which generates a cost (Lee, & Kao, 2011). It is observed that if the proper ABC model

costing is used then it will increase the overall outcomes and efficiency of the business at

large.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FEATURES OF ACTIVITY BASED COSTING

Activity Based Costing model is concerned with dividing the indirect costs incurred in the

production or in providing any service. Any cost is either a fixed cost or a variable cost. A

similar situation is there in indirect cost. So firstly, the ABC model divides the cost incurred

into two parts- fixed part and a variable part. The fixed cost is bound to be incurred

irrespective of any work being done, whereas the variable cost varies with production or

activity pattern. Each kind of cost is properly analysed to distinguish the different patterns of

cost behaviour. Unlike the traditional methods based on machine/labour hours, the ABC

model distinct the cost behaviour patterns based on volume, diversity, events and time. Based

on cost behaviour pattern, the activity/cost drivers are selected which may be maintenance

requests, machine setups, the power consumed, quality inspections or purchase orders, and

ultimately each cost is allocated based on it (Manunen, 2010).

Due to this, the departments which are less activity oriented do not bear a high burden of

costs and this ensures that both cost and time of the concern is saved in the allocation of true

costs to different departments. This shows that company will increase its outcomes if proper

ABC models are used.

ALIGNING ABC MODEL ACCORDING TO MISSION AND STRATEGIES OF

CORPORATE TRAVEL MANAGEMENT

MISSION AND OBJECTIVES OF COMPANY

The mission of CTM is to conduct business in a manner which is correct in the eyes of

environment, community and people and striving the business sustainably. It thrives to

provide the customers with fair value with utmost quality and invest in the skills of

employees. It even backs several charitable institutions. It wants to get fundamentally strong

by delivering maximum return on investment to clients and customise innovative practices

for them (Stouthuysen, et al. 2010).

Being an eleven-time AFTA award winner for being the best corporate travel management

company of Australia, the objective of the company is to further increase the client base and

continue to provide the high-quality services and be in the top of the corporate travel

management companies. It strives to excel at providing travel solutions to the clients and to

further reduce the cost of using the latest technology (Tsai, et al.(2013).

Activity Based Costing model is concerned with dividing the indirect costs incurred in the

production or in providing any service. Any cost is either a fixed cost or a variable cost. A

similar situation is there in indirect cost. So firstly, the ABC model divides the cost incurred

into two parts- fixed part and a variable part. The fixed cost is bound to be incurred

irrespective of any work being done, whereas the variable cost varies with production or

activity pattern. Each kind of cost is properly analysed to distinguish the different patterns of

cost behaviour. Unlike the traditional methods based on machine/labour hours, the ABC

model distinct the cost behaviour patterns based on volume, diversity, events and time. Based

on cost behaviour pattern, the activity/cost drivers are selected which may be maintenance

requests, machine setups, the power consumed, quality inspections or purchase orders, and

ultimately each cost is allocated based on it (Manunen, 2010).

Due to this, the departments which are less activity oriented do not bear a high burden of

costs and this ensures that both cost and time of the concern is saved in the allocation of true

costs to different departments. This shows that company will increase its outcomes if proper

ABC models are used.

ALIGNING ABC MODEL ACCORDING TO MISSION AND STRATEGIES OF

CORPORATE TRAVEL MANAGEMENT

MISSION AND OBJECTIVES OF COMPANY

The mission of CTM is to conduct business in a manner which is correct in the eyes of

environment, community and people and striving the business sustainably. It thrives to

provide the customers with fair value with utmost quality and invest in the skills of

employees. It even backs several charitable institutions. It wants to get fundamentally strong

by delivering maximum return on investment to clients and customise innovative practices

for them (Stouthuysen, et al. 2010).

Being an eleven-time AFTA award winner for being the best corporate travel management

company of Australia, the objective of the company is to further increase the client base and

continue to provide the high-quality services and be in the top of the corporate travel

management companies. It strives to excel at providing travel solutions to the clients and to

further reduce the cost of using the latest technology (Tsai, et al.(2013).

STRATEGIES OF CORPORATE TRAVEL MANAGEMENT

What makes CTM different from other travel management companies are its business

strategies that are core to its success. The strategies have made CTM functions flexible rather

than rigid. Various strategies are being followed by the corporate, but some of the major

strategies are discussed as below (Angelopoulos, & Pollalis, 2017)

Growth and service Excellency

The main motive of CTM as discussed earlier is to excel in the field of the service that they

provide, i.e. managing corporate travels mainly. There is no outsourced managing team, but a

localised team for better experience and ease of service utilization. They try to innovate the

services to be provided as per client needs and focuses on reducing the expenditure to be

made by the client. This ensures higher returns and value of expense. Travel safety is a pre-

requisite in every service extended. Various mergers and acquisitions opportunities are also

in the line of execution (Christopher, 2016).

Innovation for clients

It is observed that developing new tools with an understanding of client needs and

implementation of smart technology globally. CTM wants to address local or regional market

needs with the development of tools through localised technology centres (Corp Travel

Limited)

PRODUCTIVITY AND INTERNAL INNOVATION

The focus is to improvise and innovate the existing clients and non-client facing processes

through internal innovation tactics. To ensure higher efficiency from the employees, the trial

is to provide the staff with authority to take more decisions than past to make them more

engaged and involved. This eventually will result in the better provision of services to clients

(Dale, and Plunkett, 2017).

LEVERAGING SCALE AND GEOGRAPHY

To smooth out the whole client experience, CTM is trying to optimise supplier performance

by demonstrating the higher value of self in the whole supply chain (Fagnant, and

Kockelman, 2014).

What makes CTM different from other travel management companies are its business

strategies that are core to its success. The strategies have made CTM functions flexible rather

than rigid. Various strategies are being followed by the corporate, but some of the major

strategies are discussed as below (Angelopoulos, & Pollalis, 2017)

Growth and service Excellency

The main motive of CTM as discussed earlier is to excel in the field of the service that they

provide, i.e. managing corporate travels mainly. There is no outsourced managing team, but a

localised team for better experience and ease of service utilization. They try to innovate the

services to be provided as per client needs and focuses on reducing the expenditure to be

made by the client. This ensures higher returns and value of expense. Travel safety is a pre-

requisite in every service extended. Various mergers and acquisitions opportunities are also

in the line of execution (Christopher, 2016).

Innovation for clients

It is observed that developing new tools with an understanding of client needs and

implementation of smart technology globally. CTM wants to address local or regional market

needs with the development of tools through localised technology centres (Corp Travel

Limited)

PRODUCTIVITY AND INTERNAL INNOVATION

The focus is to improvise and innovate the existing clients and non-client facing processes

through internal innovation tactics. To ensure higher efficiency from the employees, the trial

is to provide the staff with authority to take more decisions than past to make them more

engaged and involved. This eventually will result in the better provision of services to clients

(Dale, and Plunkett, 2017).

LEVERAGING SCALE AND GEOGRAPHY

To smooth out the whole client experience, CTM is trying to optimise supplier performance

by demonstrating the higher value of self in the whole supply chain (Fagnant, and

Kockelman, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THEIR PEOPLE

More emphasis is to be powered by the staff and employee team in terms of education and

training to develop and retain them. To maintain harmony, various cultures and diversities are

to be comprised in the entity’s environment. This will work favourably in the service that will

be served to the clients (Ganorkar, Lakhe, & Agrawal, 2018).

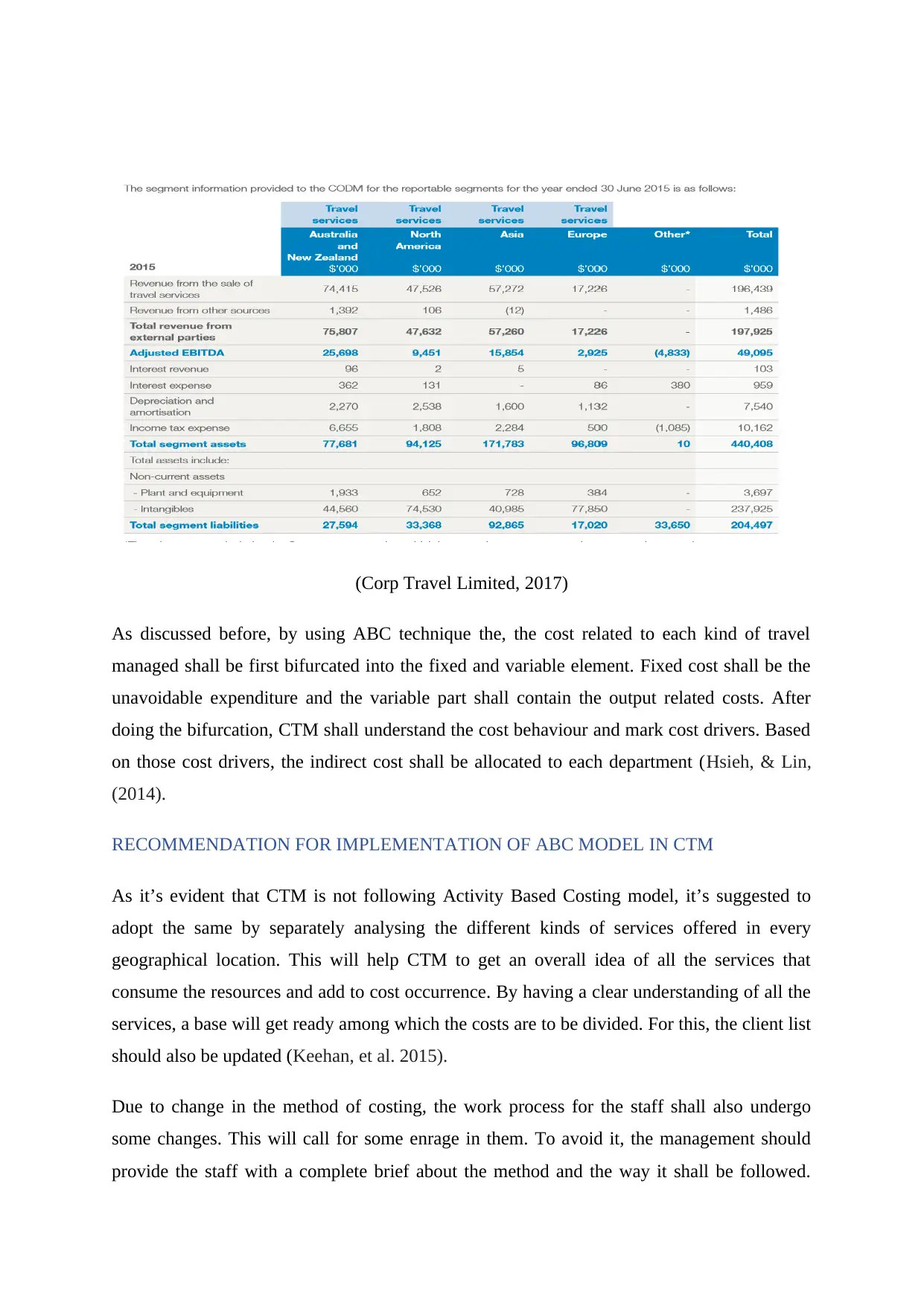

BENEFITS IN APPLYING ABC MODEL IN CORPORATE TRAVEL MANAGEMENT

The question is whether ABC model will assist in achieving the strategies of the concern or

not. As per the extract of the reportable segment taken from the Annual Report of 2015 of

CTM, it is evident that the company has divided the segments on geographical basis (New

Zealand and Australia; North America; Asia; Europe; Other) and not on the kind of service

extended, as the company also provide travel solutions for leisure, sports, events etc. other

than business ones. The kind of reporting that company has followed does not state the

different types of travel solutions provided in each geographical area. The total distribution of

costs is based on the resources used by each geographical location based on the straight line.

Although ABC model is much preferred for the manufacturing sector, in the case of service

industry like CTM, this model can help to provide a better understanding of the actual

performance at each kind travel type in each geographical area (Gerwin, Norinsky, &

Tolwani, 2018).

In the kind of disbursement done by CTM, the cost allocation is not proper and misguiding as

there are no references to cost with the level of service provided (Lee, & Kao, 2011). The

allocation is based on the total amount of installation and not the basis of the actual run. This

will even help in attaining the strategy of cost reduction (Hofmann, & Bosshard, 2017).

More emphasis is to be powered by the staff and employee team in terms of education and

training to develop and retain them. To maintain harmony, various cultures and diversities are

to be comprised in the entity’s environment. This will work favourably in the service that will

be served to the clients (Ganorkar, Lakhe, & Agrawal, 2018).

BENEFITS IN APPLYING ABC MODEL IN CORPORATE TRAVEL MANAGEMENT

The question is whether ABC model will assist in achieving the strategies of the concern or

not. As per the extract of the reportable segment taken from the Annual Report of 2015 of

CTM, it is evident that the company has divided the segments on geographical basis (New

Zealand and Australia; North America; Asia; Europe; Other) and not on the kind of service

extended, as the company also provide travel solutions for leisure, sports, events etc. other

than business ones. The kind of reporting that company has followed does not state the

different types of travel solutions provided in each geographical area. The total distribution of

costs is based on the resources used by each geographical location based on the straight line.

Although ABC model is much preferred for the manufacturing sector, in the case of service

industry like CTM, this model can help to provide a better understanding of the actual

performance at each kind travel type in each geographical area (Gerwin, Norinsky, &

Tolwani, 2018).

In the kind of disbursement done by CTM, the cost allocation is not proper and misguiding as

there are no references to cost with the level of service provided (Lee, & Kao, 2011). The

allocation is based on the total amount of installation and not the basis of the actual run. This

will even help in attaining the strategy of cost reduction (Hofmann, & Bosshard, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Corp Travel Limited, 2017)

As discussed before, by using ABC technique the, the cost related to each kind of travel

managed shall be first bifurcated into the fixed and variable element. Fixed cost shall be the

unavoidable expenditure and the variable part shall contain the output related costs. After

doing the bifurcation, CTM shall understand the cost behaviour and mark cost drivers. Based

on those cost drivers, the indirect cost shall be allocated to each department (Hsieh, & Lin,

(2014).

RECOMMENDATION FOR IMPLEMENTATION OF ABC MODEL IN CTM

As it’s evident that CTM is not following Activity Based Costing model, it’s suggested to

adopt the same by separately analysing the different kinds of services offered in every

geographical location. This will help CTM to get an overall idea of all the services that

consume the resources and add to cost occurrence. By having a clear understanding of all the

services, a base will get ready among which the costs are to be divided. For this, the client list

should also be updated (Keehan, et al. 2015).

Due to change in the method of costing, the work process for the staff shall also undergo

some changes. This will call for some enrage in them. To avoid it, the management should

provide the staff with a complete brief about the method and the way it shall be followed.

As discussed before, by using ABC technique the, the cost related to each kind of travel

managed shall be first bifurcated into the fixed and variable element. Fixed cost shall be the

unavoidable expenditure and the variable part shall contain the output related costs. After

doing the bifurcation, CTM shall understand the cost behaviour and mark cost drivers. Based

on those cost drivers, the indirect cost shall be allocated to each department (Hsieh, & Lin,

(2014).

RECOMMENDATION FOR IMPLEMENTATION OF ABC MODEL IN CTM

As it’s evident that CTM is not following Activity Based Costing model, it’s suggested to

adopt the same by separately analysing the different kinds of services offered in every

geographical location. This will help CTM to get an overall idea of all the services that

consume the resources and add to cost occurrence. By having a clear understanding of all the

services, a base will get ready among which the costs are to be divided. For this, the client list

should also be updated (Keehan, et al. 2015).

Due to change in the method of costing, the work process for the staff shall also undergo

some changes. This will call for some enrage in them. To avoid it, the management should

provide the staff with a complete brief about the method and the way it shall be followed.

Presentations should be made and communicated clearly to the employees. Accountants

should be trained according to the new procedure and the queries should be invited.

The ABC model should surely be implemented and followed, but with proper understanding

and clarity. Feedbacks should be promoted from staff for understanding the scope of

improvements or the areas of errors (Mouseli, et al. 2017).

Recommendation for the Alternative accounting model

According to the analysis of the strategies and mission of CTM, TOTAL QUALITY

MANAGEMENT is the most appropriate management accounting tool that can be followed.

In this technique, both employees and management join hands to create an organisation

whose main motive is to make continued efforts to maintain the customer base and increase it

by maintaining customer loyalty and ensuring maximum customer satisfaction. The goal of

profit maximisation comes after customer satisfaction in this kind of technique. This

technique is also known with the name PDCA cycle. PDCA refers to Plan, Do, Check and

Act (Zhuang, & Chang, 2017).

In the planning phase, the employees and management identify the customer needs and the

problems faced by them and try to develop a sustainable but flexible plan to overcome the

issues and provide high-quality services. After the planning is done, the actual

implementation of the plan is done in doing phase. The resources are utilised, and output is

given. In the checking step, monitoring is done to find the deficit in the output provision from

the desired level. In the final phase, the employees note down their actions and results,

perform for the deficiencies and boost themselves for the future course of actions (Mouseli, et

al. 2017).

Conclusion

After analysing all the details of the ABC model and alternative methods which could

be used, it could be inferred that the role of Activity Based Costing model is to improve the

management accounting of the costing of the business. However, there are several other

options which could be undertaken by Corp Travel Company to increase the recording and

accounting of its cost and expenses. The Corp travel company could also use TOTAL

QUALITY MANAGEMENT technique as cost accounting method as it i is the most

appropriate management accounting tool that can be followed.

should be trained according to the new procedure and the queries should be invited.

The ABC model should surely be implemented and followed, but with proper understanding

and clarity. Feedbacks should be promoted from staff for understanding the scope of

improvements or the areas of errors (Mouseli, et al. 2017).

Recommendation for the Alternative accounting model

According to the analysis of the strategies and mission of CTM, TOTAL QUALITY

MANAGEMENT is the most appropriate management accounting tool that can be followed.

In this technique, both employees and management join hands to create an organisation

whose main motive is to make continued efforts to maintain the customer base and increase it

by maintaining customer loyalty and ensuring maximum customer satisfaction. The goal of

profit maximisation comes after customer satisfaction in this kind of technique. This

technique is also known with the name PDCA cycle. PDCA refers to Plan, Do, Check and

Act (Zhuang, & Chang, 2017).

In the planning phase, the employees and management identify the customer needs and the

problems faced by them and try to develop a sustainable but flexible plan to overcome the

issues and provide high-quality services. After the planning is done, the actual

implementation of the plan is done in doing phase. The resources are utilised, and output is

given. In the checking step, monitoring is done to find the deficit in the output provision from

the desired level. In the final phase, the employees note down their actions and results,

perform for the deficiencies and boost themselves for the future course of actions (Mouseli, et

al. 2017).

Conclusion

After analysing all the details of the ABC model and alternative methods which could

be used, it could be inferred that the role of Activity Based Costing model is to improve the

management accounting of the costing of the business. However, there are several other

options which could be undertaken by Corp Travel Company to increase the recording and

accounting of its cost and expenses. The Corp travel company could also use TOTAL

QUALITY MANAGEMENT technique as cost accounting method as it i is the most

appropriate management accounting tool that can be followed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Angelopoulos, M., & Pollalis, Y. (2017). Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Christopher, M., (2016). Logistics & supply chain management. Pearson UK.

Corp Travel Limited, Annual report, retrieved from

http://www.travelctm.com/resources/investor-relations/reports/

Dale, B.G. & Plunkett, J.J., (2017). Quality costing. Routledge.

Fagnant, D.J. & Kockelman, K.M., (2014). The travel and environmental implications of

shared autonomous vehicles, using agent-based model scenarios. Transportation

Research Part C: Emerging Technologies, 40, pp.1-13.

Ganorkar, A. B., Lakhe, R. R., & Agrawal, K. N. (2018). Time Driven Activity Based

Costing (TDABC) Model for Cost Estimation of Assembly for a SSI. International

Journal of Productivity Management and Assessment Technologies (IJPMAT), 6(2),

56-69.

Gerwin, P. M., Norinsky, R. M., & Tolwani, R. J. (2018). Using a Time-Driven Activity-

Based Costing Model To Determine the Actual Cost of Services Provided by a

Transgenic Core. Journal of the American Association for Laboratory Animal

Science, 57(2), 157-160.

Hofmann, E., & Bosshard, J. (2017). Supply chain management and activity-based costing:

Current status and directions for the future. International Journal of Physical

Distribution & Logistics Management, 47(8), 712-735.

Hsieh, F. S., & Lin, J. B. (2014). Context-aware workflow management for virtual enterprises

based on coordination of agents. Journal of Intelligent Manufacturing, 25(3), 393-

412.

Keehan, S.P., Cuckler, G.A., Sisko, A.M., Madison, A.J., Smith, S.D., Stone, D.A., Poisal,

J.A., Wolfe, C.J. & Lizonitz, J.M., (2015). National health expenditure projections,

Angelopoulos, M., & Pollalis, Y. (2017). Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Christopher, M., (2016). Logistics & supply chain management. Pearson UK.

Corp Travel Limited, Annual report, retrieved from

http://www.travelctm.com/resources/investor-relations/reports/

Dale, B.G. & Plunkett, J.J., (2017). Quality costing. Routledge.

Fagnant, D.J. & Kockelman, K.M., (2014). The travel and environmental implications of

shared autonomous vehicles, using agent-based model scenarios. Transportation

Research Part C: Emerging Technologies, 40, pp.1-13.

Ganorkar, A. B., Lakhe, R. R., & Agrawal, K. N. (2018). Time Driven Activity Based

Costing (TDABC) Model for Cost Estimation of Assembly for a SSI. International

Journal of Productivity Management and Assessment Technologies (IJPMAT), 6(2),

56-69.

Gerwin, P. M., Norinsky, R. M., & Tolwani, R. J. (2018). Using a Time-Driven Activity-

Based Costing Model To Determine the Actual Cost of Services Provided by a

Transgenic Core. Journal of the American Association for Laboratory Animal

Science, 57(2), 157-160.

Hofmann, E., & Bosshard, J. (2017). Supply chain management and activity-based costing:

Current status and directions for the future. International Journal of Physical

Distribution & Logistics Management, 47(8), 712-735.

Hsieh, F. S., & Lin, J. B. (2014). Context-aware workflow management for virtual enterprises

based on coordination of agents. Journal of Intelligent Manufacturing, 25(3), 393-

412.

Keehan, S.P., Cuckler, G.A., Sisko, A.M., Madison, A.J., Smith, S.D., Stone, D.A., Poisal,

J.A., Wolfe, C.J. & Lizonitz, J.M., (2015). National health expenditure projections,

2014–24: spending growth faster than recent trends. Health Affairs, 34(8), pp.1407-

1417.

Mouseli, A., Barouni, M., Amiresmaili, M., Samiee, S. M., & Vali, L. (2017). Cost-price

estimation of clinical laboratory services based on activity-based costing: A case

study from a developing country. Electronic physician, 9(4), 4077.

Zhuang, Z. Y., & Chang, S. C. (2017). Deciding product mix based on time-driven activity-

based costing by mixed integer programming. Journal of Intelligent

Manufacturing, 28(4)

Manunen, O. (2010). An activity-based costing model for logistics operations of

manufacturers and wholesalers. International Journal of Logistics, 3(1), 53-65.

Stouthuysen, K., Swiggers, M., Reheul, A.M. & Roodhooft, F., (2010). Time-driven activity-

based costing for a library acquisition process: A case study in a Belgian

University. Library Collections, Acquisitions, and Technical Services, 34(2-3), pp.83-

91.

Tsai, W.H., Chen, H.C., Leu, J.D., Chang, Y.C. & Lin, T.W., (2013). A product-mix decision

model using green manufacturing technologies under activity-based costing. Journal

of cleaner production, 57, pp.178-187.

Lee, T.R. & Kao, J.S., (2011). Application of simulation technique to activity-based costing

of agricultural systems: a case study. Agricultural systems, 67(2), pp.71-82.

1417.

Mouseli, A., Barouni, M., Amiresmaili, M., Samiee, S. M., & Vali, L. (2017). Cost-price

estimation of clinical laboratory services based on activity-based costing: A case

study from a developing country. Electronic physician, 9(4), 4077.

Zhuang, Z. Y., & Chang, S. C. (2017). Deciding product mix based on time-driven activity-

based costing by mixed integer programming. Journal of Intelligent

Manufacturing, 28(4)

Manunen, O. (2010). An activity-based costing model for logistics operations of

manufacturers and wholesalers. International Journal of Logistics, 3(1), 53-65.

Stouthuysen, K., Swiggers, M., Reheul, A.M. & Roodhooft, F., (2010). Time-driven activity-

based costing for a library acquisition process: A case study in a Belgian

University. Library Collections, Acquisitions, and Technical Services, 34(2-3), pp.83-

91.

Tsai, W.H., Chen, H.C., Leu, J.D., Chang, Y.C. & Lin, T.W., (2013). A product-mix decision

model using green manufacturing technologies under activity-based costing. Journal

of cleaner production, 57, pp.178-187.

Lee, T.R. & Kao, J.S., (2011). Application of simulation technique to activity-based costing

of agricultural systems: a case study. Agricultural systems, 67(2), pp.71-82.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.