Activity Based Costing (ABC) Analysis for A2 Milk Company Products

VerifiedAdded on 2021/02/21

|7

|1255

|55

Report

AI Summary

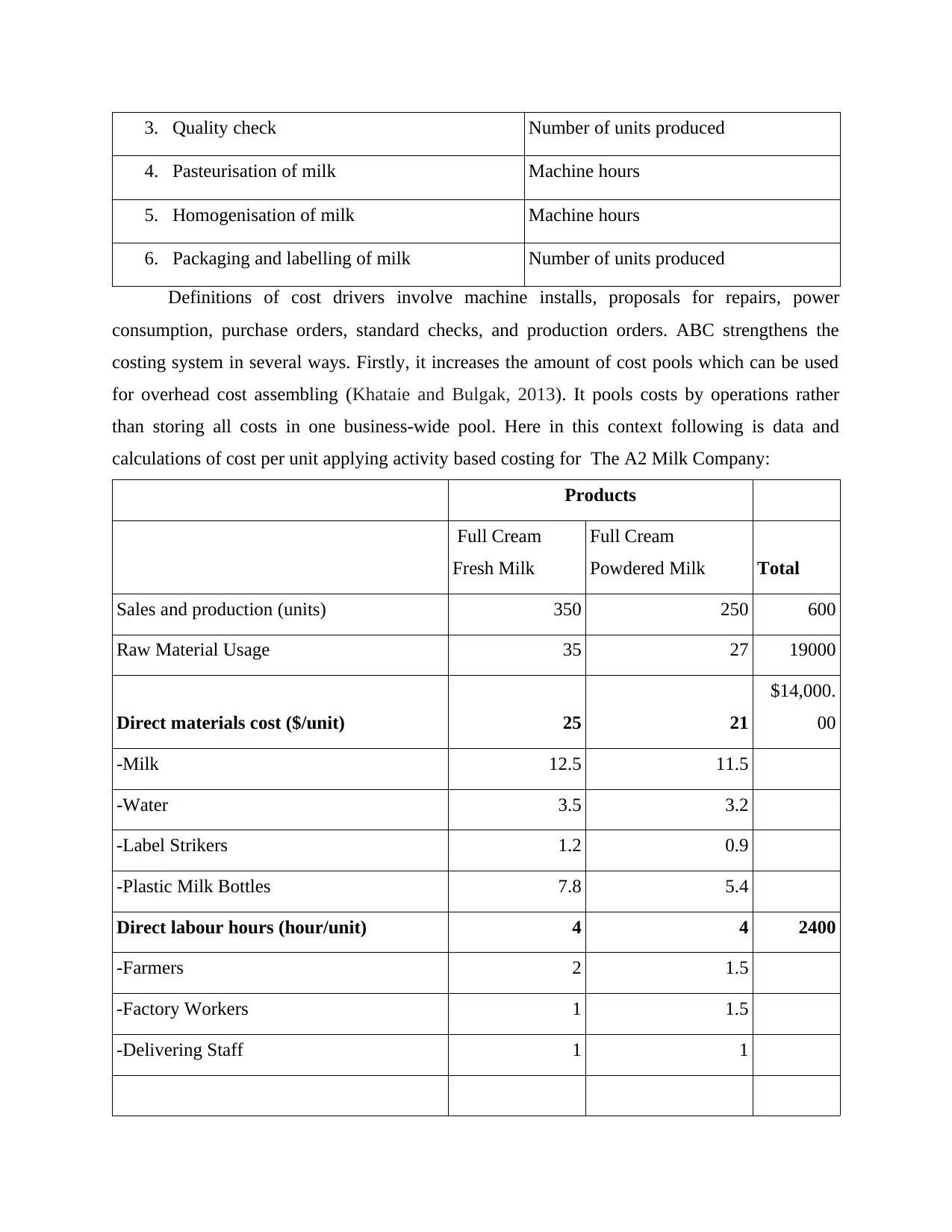

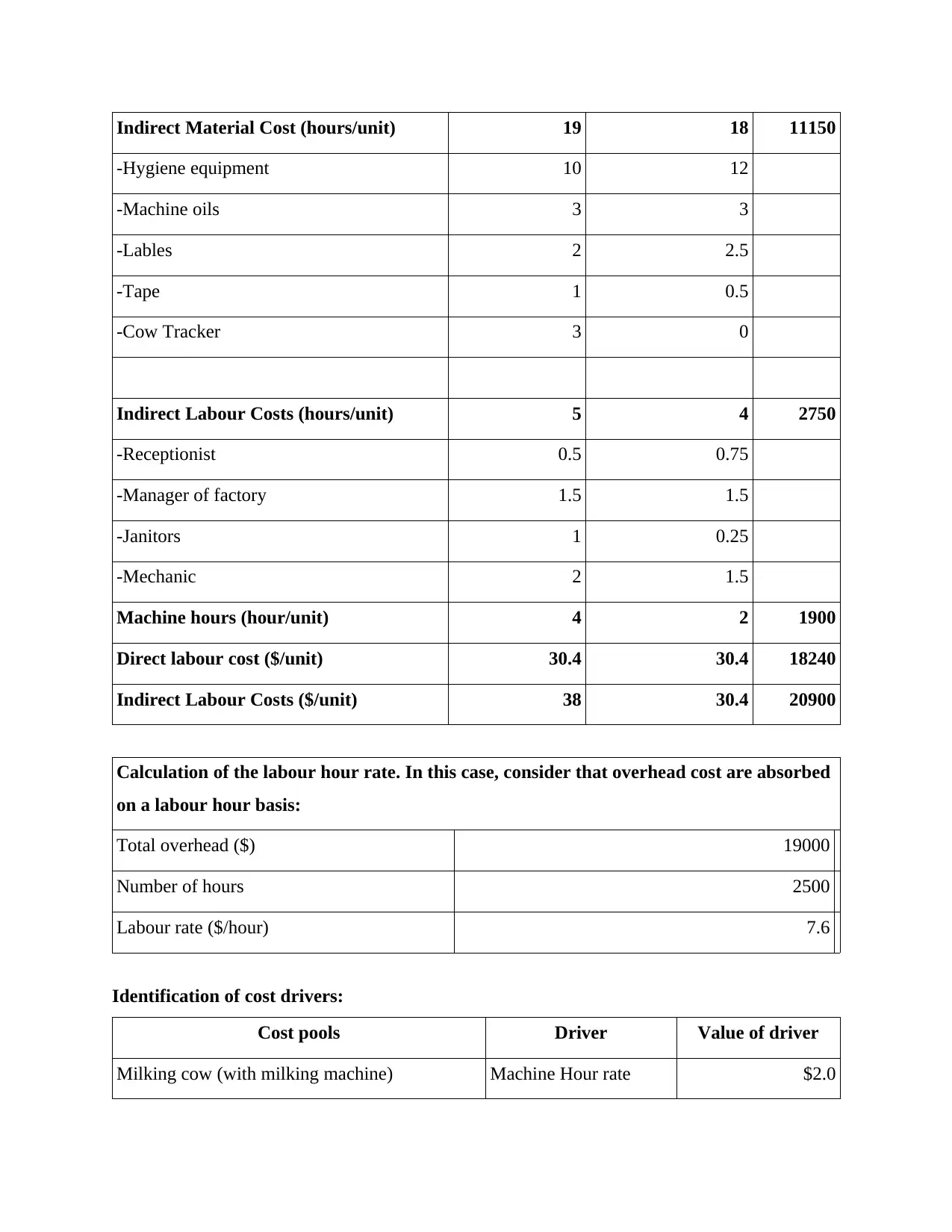

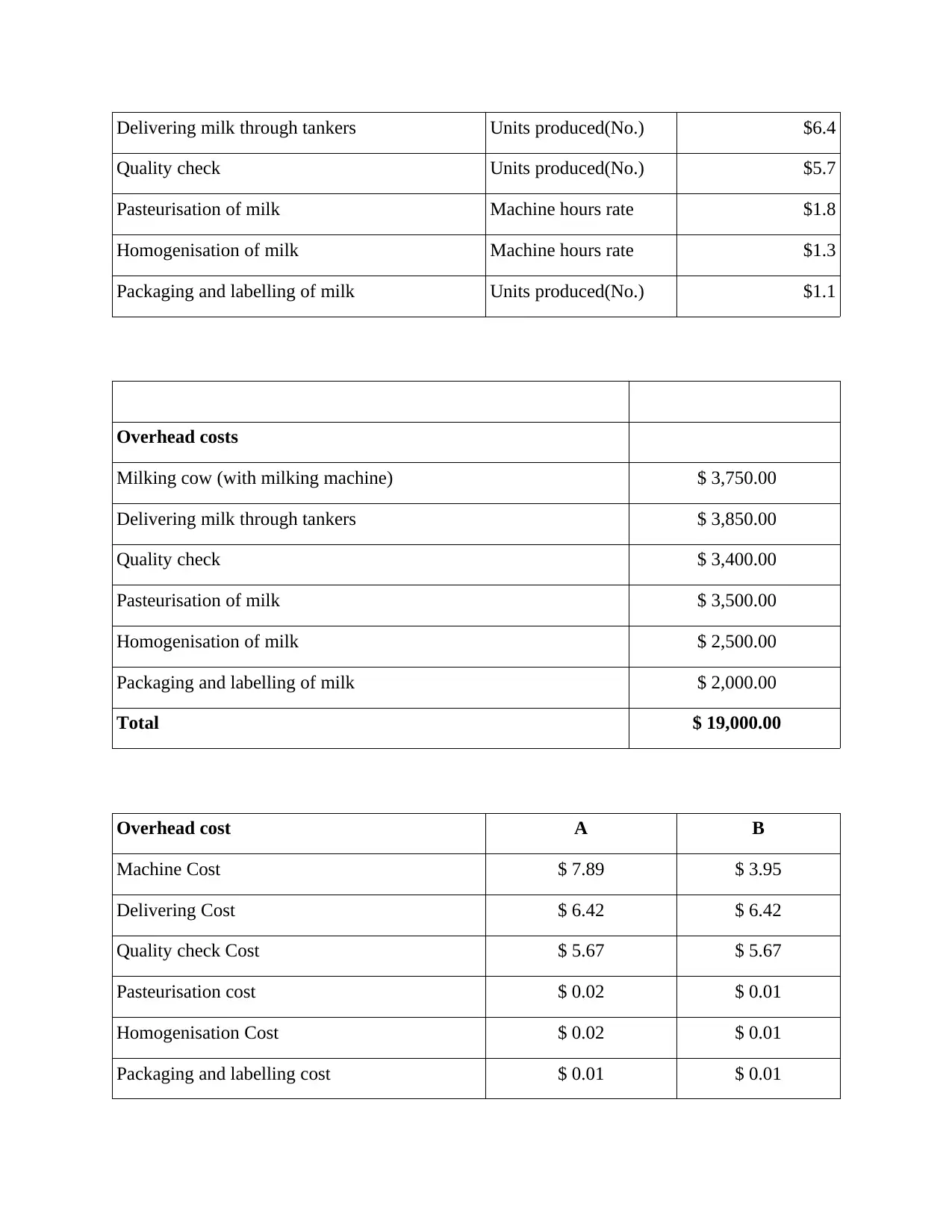

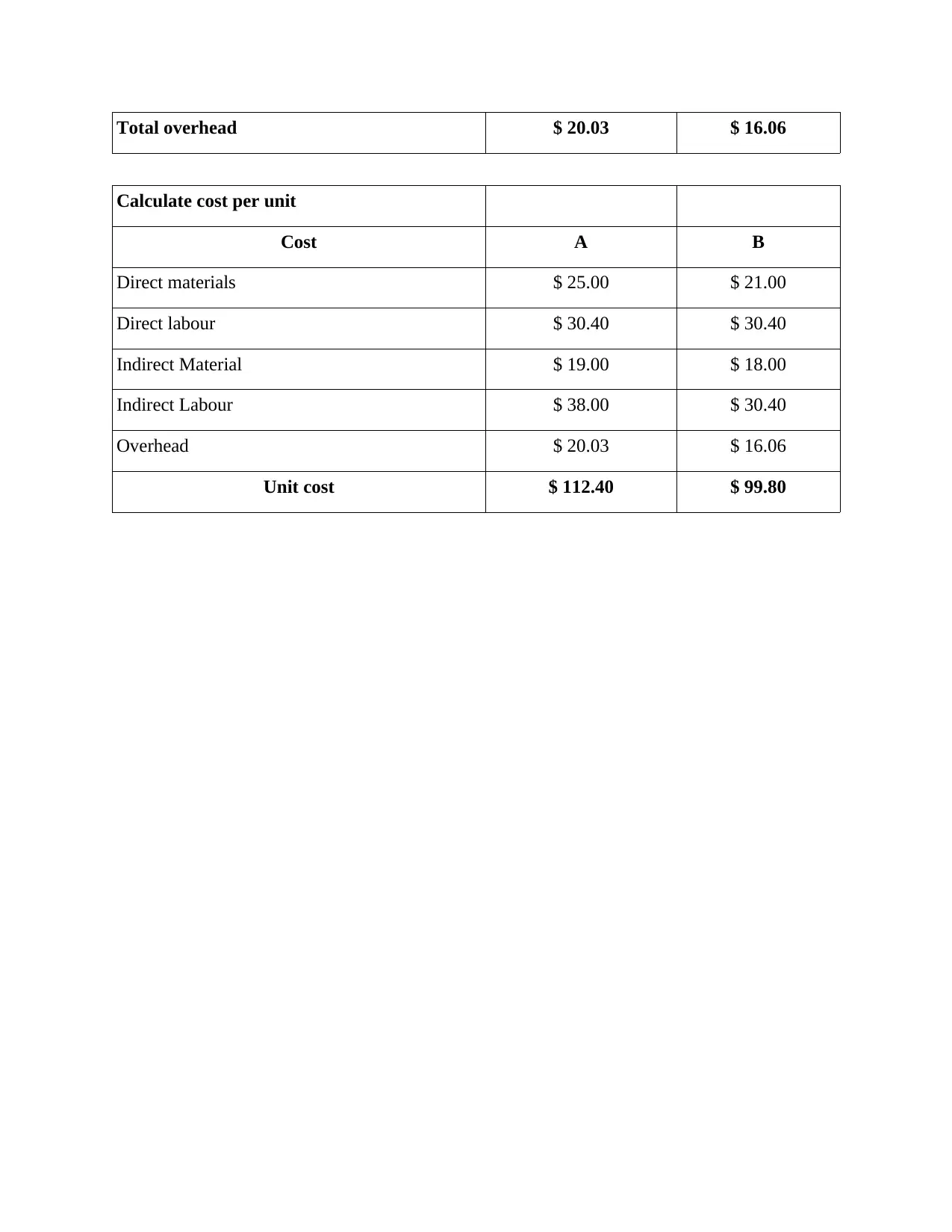

This report presents an Activity-Based Costing (ABC) analysis for A2 Milk Company, focusing on the calculation of product costs for "Full Cream Fresh Milk" and "Full Cream Powdered Milk." The analysis identifies key cost drivers, including machine hours and the number of units produced, to allocate overhead costs across various activities such as milking, delivering, quality checks, pasteurization, homogenization, and packaging. The report provides detailed data on direct materials, direct labor, and indirect costs, including calculations for labor hour rates and overhead allocation. The ABC method is applied to determine the cost per unit for each product, offering a comprehensive understanding of the company's cost structure and providing valuable insights for pricing and profitability analysis. The report includes references to relevant academic literature on ABC and its application in manufacturing environments. The report highlights how ABC improves cost report accuracy and provides a better understanding of expenditures, helping businesses to build a much more efficient pricing structure.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.