MMBB08: Activity Based Costing Report for UAE Trekker LLC

VerifiedAdded on 2022/08/12

|11

|2809

|19

Report

AI Summary

This report analyzes the implementation of Activity Based Costing (ABC) at UAE Trekker LLC, a company producing travel backpacks. The report begins with an executive summary, followed by a detailed discussion of the calculation of cost per unit using both traditional and ABC methods. It explains the reasons for changes in cost when switching from traditional absorption costing to ABC, and the potential cost management implications. The report further explores the effects of ABC on pricing and product profitability, as well as steps to take and pitfalls to avoid when introducing ABC into a business. The study highlights the benefits of ABC in providing more accurate cost information, leading to improved decision-making regarding pricing, resource allocation, and overall profitability. The report also examines the risks and difficulties related to the ABC system and the steps towards eliminating such risks. The report concludes with a summary of findings and recommendations for UAE Trekker LLC, emphasizing the importance of ABC for effective cost management and strategic decision-making. The report includes a table of contents, references, and appendices.

Running head: IMPORTANCE OF ACTIVITY BASED COSTING

IMPORTANCE OF ACTIVITY BASED COSTING

Name of the Student

Name of the University

Author’s Note:

IMPORTANCE OF ACTIVITY BASED COSTING

Name of the Student

Name of the University

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1IMPORTANCE OF ACTIVITY BASED COSTING

Executive Summary

The report takes the example of UAE Trekker LLC that produces a broad range of products

where overheads play an important role. The Company, to improve its profitability and to make a

proper decision regarding the manufacturing process switches from a traditional approach to the

ABC approach. The report also studies about the reasons behind the changes in the cost per unit

of the goods under traditional costing method to ABC. In addition, implications of the potential

cost management, including the effects on pricing and profitability of switching from traditional

absorption costing to Activity-based costing has been discussed. Moreover, the reason behind

selecting the ABC system has been discussed in the report and how it helps the Company to

make their decision in an effective way to achieve the goals and better opportunities for their

production. Lastly, the study covers the risk and difficulty related to the ABC system into a

business and the steps towards eliminating such risks.

Executive Summary

The report takes the example of UAE Trekker LLC that produces a broad range of products

where overheads play an important role. The Company, to improve its profitability and to make a

proper decision regarding the manufacturing process switches from a traditional approach to the

ABC approach. The report also studies about the reasons behind the changes in the cost per unit

of the goods under traditional costing method to ABC. In addition, implications of the potential

cost management, including the effects on pricing and profitability of switching from traditional

absorption costing to Activity-based costing has been discussed. Moreover, the reason behind

selecting the ABC system has been discussed in the report and how it helps the Company to

make their decision in an effective way to achieve the goals and better opportunities for their

production. Lastly, the study covers the risk and difficulty related to the ABC system into a

business and the steps towards eliminating such risks.

2IMPORTANCE OF ACTIVITY BASED COSTING

“I ………… declare that I am the sole author of this assignment and the work is a result of my

own investigations, except where otherwise stated. All references have been duly cited”.

“I ………… declare that I am the sole author of this assignment and the work is a result of my

own investigations, except where otherwise stated. All references have been duly cited”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3IMPORTANCE OF ACTIVITY BASED COSTING

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

a) Calculation of cost per unit using traditional method...........................................................3

a) Calculation of cost per unit using ABC method...................................................................4

b) Reasons for the changes in cost per unit when the costing system are changed from

traditional absorption costing to ABC.........................................................................................4

c) Potential cost management implications of switching to an ABC system...........................5

d) Effects on pricing and product profitability from switching from traditional absorption

costing to an ABC system............................................................................................................6

e) Steps and possible pitfalls to avoid when introducing an ABC system into a business.......6

Conclusion.......................................................................................................................................7

References and bibliography...........................................................................................................8

Appendix..........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

a) Calculation of cost per unit using traditional method...........................................................3

a) Calculation of cost per unit using ABC method...................................................................4

b) Reasons for the changes in cost per unit when the costing system are changed from

traditional absorption costing to ABC.........................................................................................4

c) Potential cost management implications of switching to an ABC system...........................5

d) Effects on pricing and product profitability from switching from traditional absorption

costing to an ABC system............................................................................................................6

e) Steps and possible pitfalls to avoid when introducing an ABC system into a business.......6

Conclusion.......................................................................................................................................7

References and bibliography...........................................................................................................8

Appendix..........................................................................................................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4IMPORTANCE OF ACTIVITY BASED COSTING

Introduction

UAE Trekker LLC produces Travel Hiking Backpacks in three different colors, Black,

Grey and Orange, which are all manufactured from the same form of raw material. The

Company used to allocate overheads to its products using direct labor hours as per traditional full

costing. The Company is now preferring to use activity-based costing system to improve its

profitability. In this report, the calculation of cost per unit under traditional absorption costing

using direct labor costs and Activity Based costing has been shown. In this report, the reason

behind selecting the ABC system has been discussed and how it helps the business to make their

decision in an effective way.

Discussion

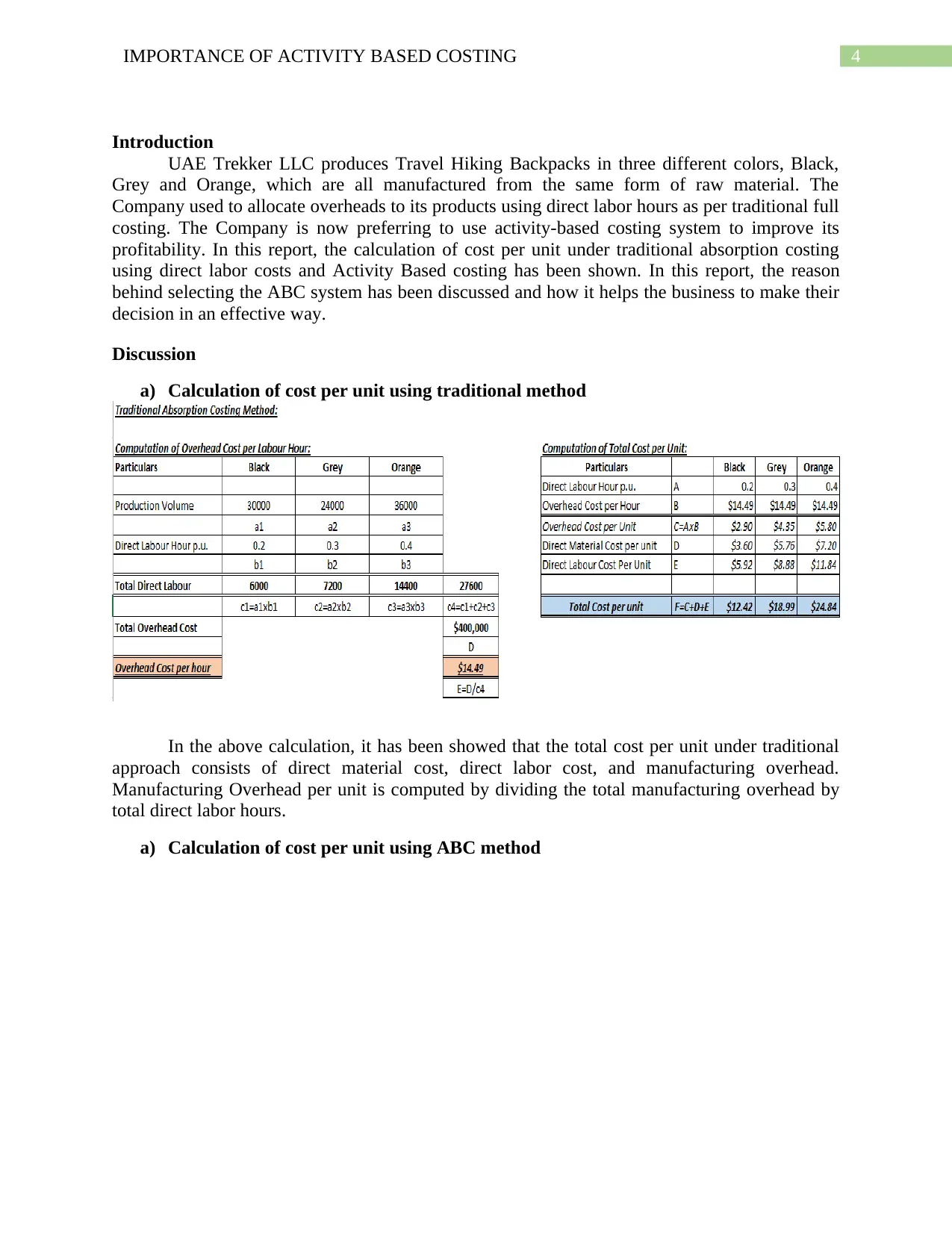

a) Calculation of cost per unit using traditional method

In the above calculation, it has been showed that the total cost per unit under traditional

approach consists of direct material cost, direct labor cost, and manufacturing overhead.

Manufacturing Overhead per unit is computed by dividing the total manufacturing overhead by

total direct labor hours.

a) Calculation of cost per unit using ABC method

Introduction

UAE Trekker LLC produces Travel Hiking Backpacks in three different colors, Black,

Grey and Orange, which are all manufactured from the same form of raw material. The

Company used to allocate overheads to its products using direct labor hours as per traditional full

costing. The Company is now preferring to use activity-based costing system to improve its

profitability. In this report, the calculation of cost per unit under traditional absorption costing

using direct labor costs and Activity Based costing has been shown. In this report, the reason

behind selecting the ABC system has been discussed and how it helps the business to make their

decision in an effective way.

Discussion

a) Calculation of cost per unit using traditional method

In the above calculation, it has been showed that the total cost per unit under traditional

approach consists of direct material cost, direct labor cost, and manufacturing overhead.

Manufacturing Overhead per unit is computed by dividing the total manufacturing overhead by

total direct labor hours.

a) Calculation of cost per unit using ABC method

5IMPORTANCE OF ACTIVITY BASED COSTING

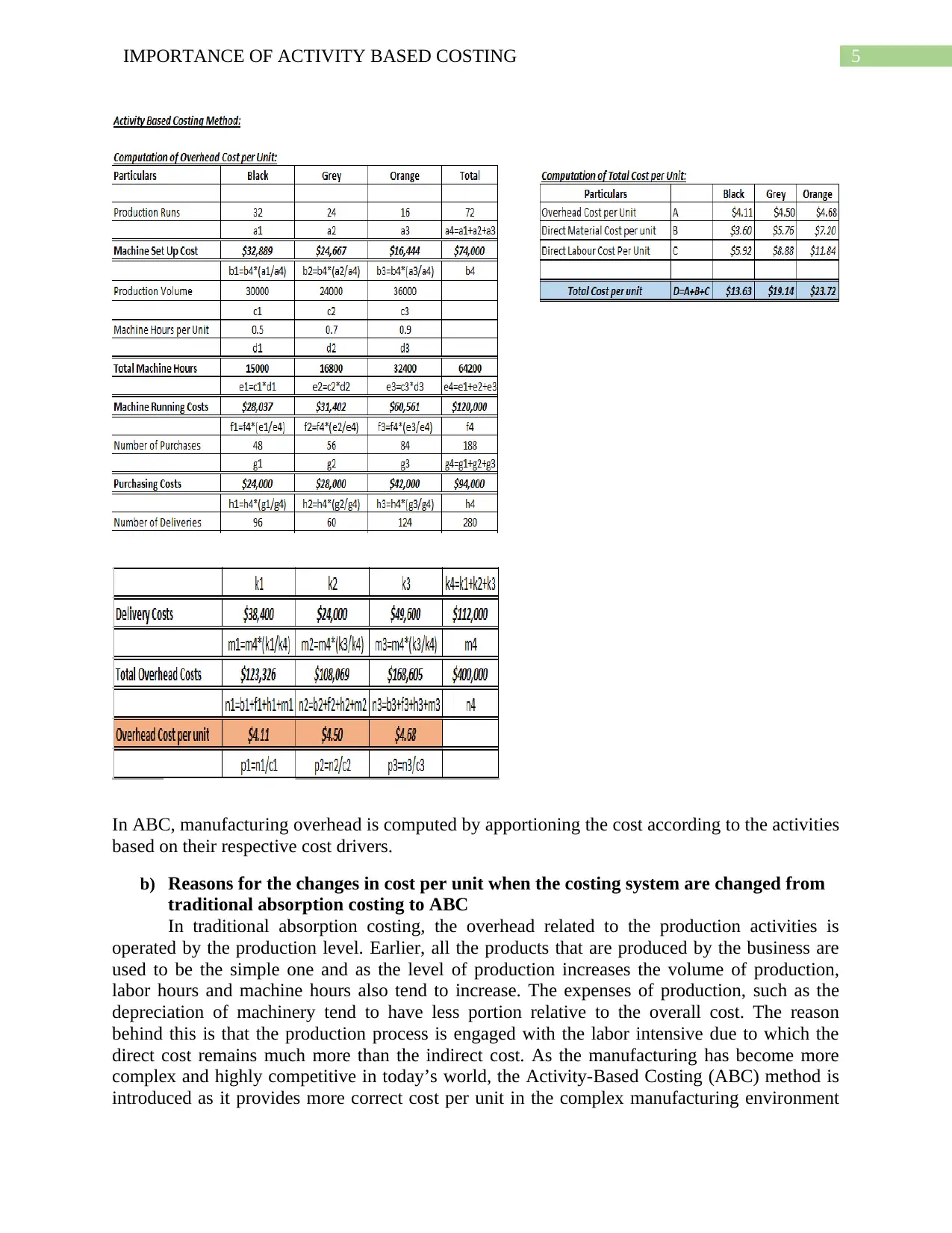

In ABC, manufacturing overhead is computed by apportioning the cost according to the activities

based on their respective cost drivers.

b) Reasons for the changes in cost per unit when the costing system are changed from

traditional absorption costing to ABC

In traditional absorption costing, the overhead related to the production activities is

operated by the production level. Earlier, all the products that are produced by the business are

used to be the simple one and as the level of production increases the volume of production,

labor hours and machine hours also tend to increase. The expenses of production, such as the

depreciation of machinery tend to have less portion relative to the overall cost. The reason

behind this is that the production process is engaged with the labor intensive due to which the

direct cost remains much more than the indirect cost. As the manufacturing has become more

complex and highly competitive in today’s world, the Activity-Based Costing (ABC) method is

introduced as it provides more correct cost per unit in the complex manufacturing environment

In ABC, manufacturing overhead is computed by apportioning the cost according to the activities

based on their respective cost drivers.

b) Reasons for the changes in cost per unit when the costing system are changed from

traditional absorption costing to ABC

In traditional absorption costing, the overhead related to the production activities is

operated by the production level. Earlier, all the products that are produced by the business are

used to be the simple one and as the level of production increases the volume of production,

labor hours and machine hours also tend to increase. The expenses of production, such as the

depreciation of machinery tend to have less portion relative to the overall cost. The reason

behind this is that the production process is engaged with the labor intensive due to which the

direct cost remains much more than the indirect cost. As the manufacturing has become more

complex and highly competitive in today’s world, the Activity-Based Costing (ABC) method is

introduced as it provides more correct cost per unit in the complex manufacturing environment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6IMPORTANCE OF ACTIVITY BASED COSTING

and multiplex business (Gerwin, Norinsky and Tolwani 2018). In ABC, the running cost are not

related to the volume of production and sales and are operated by executing cost drivers. In

Activity-based costing, cost driver is important and hence impacts the cost level. For each of the

Activity, the cost driver is identified and are used for allocating the cost (actual) as per the

activities that are involved. The reason behind this cost of Activity to be incurred would be the

cost drivers. The absorption rate of overhead is calculated similar to the Traditional absorption

costing, but there is a separate calculation of absorption rate of overhead for each of the Activity,

considering the cost of Activity and dividing it as per the information of the cost drivers. This

method is not only limited to the production activities but are also applicable to all cost of

overhead. Cost per unit is calculated by absorbing the cost of Activity again in each of the

products. Therefore, the Activity costing method brought into the picture to cope up with the

recognized weakness of costing under the traditional absorption approach (Jassem 2019).

c) Potential cost management implications of switching to an ABC system.

Activity-based costing analyzes the activities in a business and appoints each cost activity to

the manufacturing overhead of each good and service (Chouhan, Soral and Chandra 2017). In the

ABC approach, the indirect costs (overhead) are more allocated to direct costs. By doing so, a

business can calculate the cost of each of the manufactured goods and services correctly to

identify and dismiss those costs which are not giving a profit. In addition, it focuses on reducing

the prices if those whose prices are more than the original cost.

In business, the ABC approach allocates the cost of its reserves through activities to the

products and services provided to its buyers. It is generally used as a mean for understanding the

cost and profitability of the product and consumer (Zheng and Abu 2019). However, ABC has

broadly been used to support vital decisions such as pricing, deployment, identifying and

measuring the process:

It helps to identify the cost used at a basic level or on a departmental level.

The products, activities and departments aim to get identified.

It finds out the cost which is not necessary to eliminate them.

It focuses on assigning more resources on products, activities and departments that are

profitable.

There is a need to focus on the activities that enable such costs in order to manage costs by

the manager. Correspondingly, to facilitate cost management, it is the responsibility of the

managers in a business to implement ABC method.

The non- value-added activities are recognized with the help of the ABC approach by a

business which utilizes resources without adding value to the services of the consumers. These

activities are identified and reduced with the help of Activity-based costing. In addition, a

business needs to expand certain measures which are non-financial. It aims to keep track of

consumer’s time that they intend for their goods and other services and focus on the manager’s

attention to know the problem and get an effective solution to those critical issues. However,

reducing waste may not eliminate the costs of the product in every way but can lead to enhance

the quality of services provided.

and multiplex business (Gerwin, Norinsky and Tolwani 2018). In ABC, the running cost are not

related to the volume of production and sales and are operated by executing cost drivers. In

Activity-based costing, cost driver is important and hence impacts the cost level. For each of the

Activity, the cost driver is identified and are used for allocating the cost (actual) as per the

activities that are involved. The reason behind this cost of Activity to be incurred would be the

cost drivers. The absorption rate of overhead is calculated similar to the Traditional absorption

costing, but there is a separate calculation of absorption rate of overhead for each of the Activity,

considering the cost of Activity and dividing it as per the information of the cost drivers. This

method is not only limited to the production activities but are also applicable to all cost of

overhead. Cost per unit is calculated by absorbing the cost of Activity again in each of the

products. Therefore, the Activity costing method brought into the picture to cope up with the

recognized weakness of costing under the traditional absorption approach (Jassem 2019).

c) Potential cost management implications of switching to an ABC system.

Activity-based costing analyzes the activities in a business and appoints each cost activity to

the manufacturing overhead of each good and service (Chouhan, Soral and Chandra 2017). In the

ABC approach, the indirect costs (overhead) are more allocated to direct costs. By doing so, a

business can calculate the cost of each of the manufactured goods and services correctly to

identify and dismiss those costs which are not giving a profit. In addition, it focuses on reducing

the prices if those whose prices are more than the original cost.

In business, the ABC approach allocates the cost of its reserves through activities to the

products and services provided to its buyers. It is generally used as a mean for understanding the

cost and profitability of the product and consumer (Zheng and Abu 2019). However, ABC has

broadly been used to support vital decisions such as pricing, deployment, identifying and

measuring the process:

It helps to identify the cost used at a basic level or on a departmental level.

The products, activities and departments aim to get identified.

It finds out the cost which is not necessary to eliminate them.

It focuses on assigning more resources on products, activities and departments that are

profitable.

There is a need to focus on the activities that enable such costs in order to manage costs by

the manager. Correspondingly, to facilitate cost management, it is the responsibility of the

managers in a business to implement ABC method.

The non- value-added activities are recognized with the help of the ABC approach by a

business which utilizes resources without adding value to the services of the consumers. These

activities are identified and reduced with the help of Activity-based costing. In addition, a

business needs to expand certain measures which are non-financial. It aims to keep track of

consumer’s time that they intend for their goods and other services and focus on the manager’s

attention to know the problem and get an effective solution to those critical issues. However,

reducing waste may not eliminate the costs of the product in every way but can lead to enhance

the quality of services provided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7IMPORTANCE OF ACTIVITY BASED COSTING

d) Effects on pricing and product profitability from switching from traditional

absorption costing to an ABC system

The cost of the product plays an important role in the pricing decision process, which are

more complex. There is a different cost of a product which are used by a business in the decision

of pricing. The total cost is considered to be the most popular choice, but as some of them are not

traceable it appears to be misstated. This lead to making the allocation of cost inaccurate and

such inaccurate result affect the pricing decision in a negative way (Haladu 2016). The

inaccuracy of cost allocation is bad for pricing. Hence, it is important to have accurate costing as

such misstatement costing of the product make the pricing unrealistic. In this support, ABC

system proved to be an adequate solution to this issue as it provides accurate information related

to the cost. There is a basic reason why ABC is preferred by the managers in the implementation

of decision regarding a product is that the system of ABC gives more exact costing and used to

recognize the associated costs that can be reduced along with the resources that are underutilized

(Lueg and Storgaard 2017). The ABC approach also authorizes the differentiation of price

among products, consumers, and place of a market which enhance the value effect on the

decisions of prices and profitability. The Company can price its product according to the cost of

activities carried out in manufacturing the goods and services and thus can get the more precise

cost of the product. By doing this, there will be no overpricing or underpricing of the product.

By saving the time, money, and resources of a company, the activity-based costing

method increases the profitability (ȘUTEU et al. 2016). The ABC system makes this possible by

recognizing the exact costs of overhead and cost drivers. When all cost such as the direct and

indirect costs are assigned to good or service, the head department develops an idea regarding

which processes of business are executing well including which are not performing efficiently.

These processes can be organized well by reducing application that is costly along with

allocating resources to the profitable activities. The product pricing is an accurate term to help to

increase the profitability of the Company, which can allow them in maximizing their returns by

offering competitive pricing (Lu et al. 2017). Hence, UAE Trekker LLC can manage the

manufacturing performance in a better way and can also improve the quality of their products

and services by adopting this ABC approach.

e) Steps and possible pitfalls to avoid when introducing an ABC system into a business

As it is a known fact how ABC system helps in improving the profitability of a business,

there are certain pitfalls to avoid while introducing this system into a business. Use of activity-

based costing approach is not suitable for all. It becomes important for the managers to

understand the conditions of the work environment in which ABC works best and give accurate

results.

The ABC system aims to provide information of high quality; however there is a huge

cost pools which depicts that the existence of more cost pools will make more cost of

system management. In order to, reduce cost, a company needs to analyze the cost to

keep up each cost pool as compared with benefit of derived information. It will bring

down amount of cost pools according to feasible proportions.

There is a collection of data input from multiple departments in Activity-based costing

approach, and each of those departments may have some other concern than ABC

system. Therefore, as there will be larger involvement in the system of the number of

departments, there will be more risk of failure of data inputs over time. One of the ways

d) Effects on pricing and product profitability from switching from traditional

absorption costing to an ABC system

The cost of the product plays an important role in the pricing decision process, which are

more complex. There is a different cost of a product which are used by a business in the decision

of pricing. The total cost is considered to be the most popular choice, but as some of them are not

traceable it appears to be misstated. This lead to making the allocation of cost inaccurate and

such inaccurate result affect the pricing decision in a negative way (Haladu 2016). The

inaccuracy of cost allocation is bad for pricing. Hence, it is important to have accurate costing as

such misstatement costing of the product make the pricing unrealistic. In this support, ABC

system proved to be an adequate solution to this issue as it provides accurate information related

to the cost. There is a basic reason why ABC is preferred by the managers in the implementation

of decision regarding a product is that the system of ABC gives more exact costing and used to

recognize the associated costs that can be reduced along with the resources that are underutilized

(Lueg and Storgaard 2017). The ABC approach also authorizes the differentiation of price

among products, consumers, and place of a market which enhance the value effect on the

decisions of prices and profitability. The Company can price its product according to the cost of

activities carried out in manufacturing the goods and services and thus can get the more precise

cost of the product. By doing this, there will be no overpricing or underpricing of the product.

By saving the time, money, and resources of a company, the activity-based costing

method increases the profitability (ȘUTEU et al. 2016). The ABC system makes this possible by

recognizing the exact costs of overhead and cost drivers. When all cost such as the direct and

indirect costs are assigned to good or service, the head department develops an idea regarding

which processes of business are executing well including which are not performing efficiently.

These processes can be organized well by reducing application that is costly along with

allocating resources to the profitable activities. The product pricing is an accurate term to help to

increase the profitability of the Company, which can allow them in maximizing their returns by

offering competitive pricing (Lu et al. 2017). Hence, UAE Trekker LLC can manage the

manufacturing performance in a better way and can also improve the quality of their products

and services by adopting this ABC approach.

e) Steps and possible pitfalls to avoid when introducing an ABC system into a business

As it is a known fact how ABC system helps in improving the profitability of a business,

there are certain pitfalls to avoid while introducing this system into a business. Use of activity-

based costing approach is not suitable for all. It becomes important for the managers to

understand the conditions of the work environment in which ABC works best and give accurate

results.

The ABC system aims to provide information of high quality; however there is a huge

cost pools which depicts that the existence of more cost pools will make more cost of

system management. In order to, reduce cost, a company needs to analyze the cost to

keep up each cost pool as compared with benefit of derived information. It will bring

down amount of cost pools according to feasible proportions.

There is a collection of data input from multiple departments in Activity-based costing

approach, and each of those departments may have some other concern than ABC

system. Therefore, as there will be larger involvement in the system of the number of

departments, there will be more risk of failure of data inputs over time. One of the ways

8IMPORTANCE OF ACTIVITY BASED COSTING

to avoid it is to design the system only to get information from the most encouraging

managers.

The relevant information is collected once from the project of ABC which is developed to

be competent in company’s current operational scenario. Over a time the operational

structure gets changed declining its usefulness. However, the organization can inhibit

financing for more Activity-based costing projects in future. Hence, to eliminate this

issue, it is advisable to construct more form of ABC data collection into prevailing

accounting system as much as required. This is to be done to bring down cost of these

ABC projects providing the authorization of supplementary ABC projects in future.

The wide range of issues mentioned above defines that Activity-based costing system tends

to follow an irregular path in many businesses and the usefulness decreases over time

(Gooneratne and Wijerathne 2019). There is a need to construct a highly positioned Activity-

based costing system that gives required information on logical cost.

Conclusion

Thus, from the above discussion, it has been concluded that UAE Trekker LLC produces

a broad range of products where overheads play an important role. The traditional approach to

allocating overheads to its products using direct labor hours are not validated in the extreme

worldwide competition.

to avoid it is to design the system only to get information from the most encouraging

managers.

The relevant information is collected once from the project of ABC which is developed to

be competent in company’s current operational scenario. Over a time the operational

structure gets changed declining its usefulness. However, the organization can inhibit

financing for more Activity-based costing projects in future. Hence, to eliminate this

issue, it is advisable to construct more form of ABC data collection into prevailing

accounting system as much as required. This is to be done to bring down cost of these

ABC projects providing the authorization of supplementary ABC projects in future.

The wide range of issues mentioned above defines that Activity-based costing system tends

to follow an irregular path in many businesses and the usefulness decreases over time

(Gooneratne and Wijerathne 2019). There is a need to construct a highly positioned Activity-

based costing system that gives required information on logical cost.

Conclusion

Thus, from the above discussion, it has been concluded that UAE Trekker LLC produces

a broad range of products where overheads play an important role. The traditional approach to

allocating overheads to its products using direct labor hours are not validated in the extreme

worldwide competition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9IMPORTANCE OF ACTIVITY BASED COSTING

References and bibliography

Bloechl, S.J., Michalicki, M. and Schneider, M., 2017. Simulation game for lean leadership–

shopfloor management combined with accounting for lean. Procedia manufacturing, 9, pp.97-

105.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters, 7(3), pp.135-144.

Gerwin, P.M., Norinsky, R.M. and Tolwani, R.J., 2018. Using a Time-Driven Activity-Based

Costing Model To Determine the Actual Cost of Services Provided by a Transgenic

Core. Journal of the American Association for Laboratory Animal Science, 57(2), pp.157-160.

Gooneratne, T. and Wijerathne, C., 2019. APPEARANCE, DISAPPEARANCE AND

REAPPEARANCE OF ACTIVITY BASED COSTING: A CASE STUDY FROM A SRI

LANKAN MANUFACTURING FIRM. Asia-Pacific Management Accounting Journal, 14(3),

pp.49-80.

Haladu, A., 2016. The practicability of activity-based costing in service firms. International

Journal of Management Research and Reviews, 6(7), p.876.

Jassem, S., 2019. Benefits of Switching from Activity-Based Costing to Resource Consumption

Accounting: Evidence from a Power Generator Manufacturing Plant. Management and

Accounting Review (MAR), 18(3), pp.169-190.

Laing, G.K. and Perrin, R.W., 2018. Management Accounting in the Australian Printing

Industry: A Survey. The Journal of New Business Ideas & Trends, 16(3), pp.13-19.

Lu, T.Y., Wang, S.L., Wu, M.F. and Cheng, F.T., 2017. Competitive Price Strategy with

Activity-Based Costing–Case Study of Bicycle Part Company. Procedia CIRP, 63, pp.14-20.

Lueg, R. and Storgaard, N., 2017. The adoption and implementation of Activity-based Costing:

A systematic literature review. International Journal of Strategic Management, 17(2), pp.7-24.

Malik, G.H., Al Jasimee, K.H. and Alhasan, G.A.K., 2019. Investigating the Effect of Using

Activity Based Costing (ABC) on Captive Product Pricing System in Internet Supply Chain

Services. Int. J Sup. Chain. Mgt Vol, 8(1), p.400.

Namazi, M., 2016. Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), pp.457-482.

ȘUTEU, M.D., MEȘTER, L.E., Bugnar, N.G., Andreescu, N. and Petrica, D.M., 2016. The

impact of costing methods on profitability of enterprises operating in the embroidery

industry. Tekstil ve Konfeksiyon, 26(3), pp.239-243.

Wegmann, G., 2018. A Typology of Cost Accounting Practices Based on Activity-Based

Costing–A Strategic Cost Management Approach and a Case Study. Available at SSRN 3236159.

Zheng, C.W. and Abu, M.Y., 2019. Application of Activity based costing for palm oil

plantation. Journal of Modern Manufacturing Systems and Technology, 2, pp.1-14.

References and bibliography

Bloechl, S.J., Michalicki, M. and Schneider, M., 2017. Simulation game for lean leadership–

shopfloor management combined with accounting for lean. Procedia manufacturing, 9, pp.97-

105.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters, 7(3), pp.135-144.

Gerwin, P.M., Norinsky, R.M. and Tolwani, R.J., 2018. Using a Time-Driven Activity-Based

Costing Model To Determine the Actual Cost of Services Provided by a Transgenic

Core. Journal of the American Association for Laboratory Animal Science, 57(2), pp.157-160.

Gooneratne, T. and Wijerathne, C., 2019. APPEARANCE, DISAPPEARANCE AND

REAPPEARANCE OF ACTIVITY BASED COSTING: A CASE STUDY FROM A SRI

LANKAN MANUFACTURING FIRM. Asia-Pacific Management Accounting Journal, 14(3),

pp.49-80.

Haladu, A., 2016. The practicability of activity-based costing in service firms. International

Journal of Management Research and Reviews, 6(7), p.876.

Jassem, S., 2019. Benefits of Switching from Activity-Based Costing to Resource Consumption

Accounting: Evidence from a Power Generator Manufacturing Plant. Management and

Accounting Review (MAR), 18(3), pp.169-190.

Laing, G.K. and Perrin, R.W., 2018. Management Accounting in the Australian Printing

Industry: A Survey. The Journal of New Business Ideas & Trends, 16(3), pp.13-19.

Lu, T.Y., Wang, S.L., Wu, M.F. and Cheng, F.T., 2017. Competitive Price Strategy with

Activity-Based Costing–Case Study of Bicycle Part Company. Procedia CIRP, 63, pp.14-20.

Lueg, R. and Storgaard, N., 2017. The adoption and implementation of Activity-based Costing:

A systematic literature review. International Journal of Strategic Management, 17(2), pp.7-24.

Malik, G.H., Al Jasimee, K.H. and Alhasan, G.A.K., 2019. Investigating the Effect of Using

Activity Based Costing (ABC) on Captive Product Pricing System in Internet Supply Chain

Services. Int. J Sup. Chain. Mgt Vol, 8(1), p.400.

Namazi, M., 2016. Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), pp.457-482.

ȘUTEU, M.D., MEȘTER, L.E., Bugnar, N.G., Andreescu, N. and Petrica, D.M., 2016. The

impact of costing methods on profitability of enterprises operating in the embroidery

industry. Tekstil ve Konfeksiyon, 26(3), pp.239-243.

Wegmann, G., 2018. A Typology of Cost Accounting Practices Based on Activity-Based

Costing–A Strategic Cost Management Approach and a Case Study. Available at SSRN 3236159.

Zheng, C.W. and Abu, M.Y., 2019. Application of Activity based costing for palm oil

plantation. Journal of Modern Manufacturing Systems and Technology, 2, pp.1-14.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10IMPORTANCE OF ACTIVITY BASED COSTING

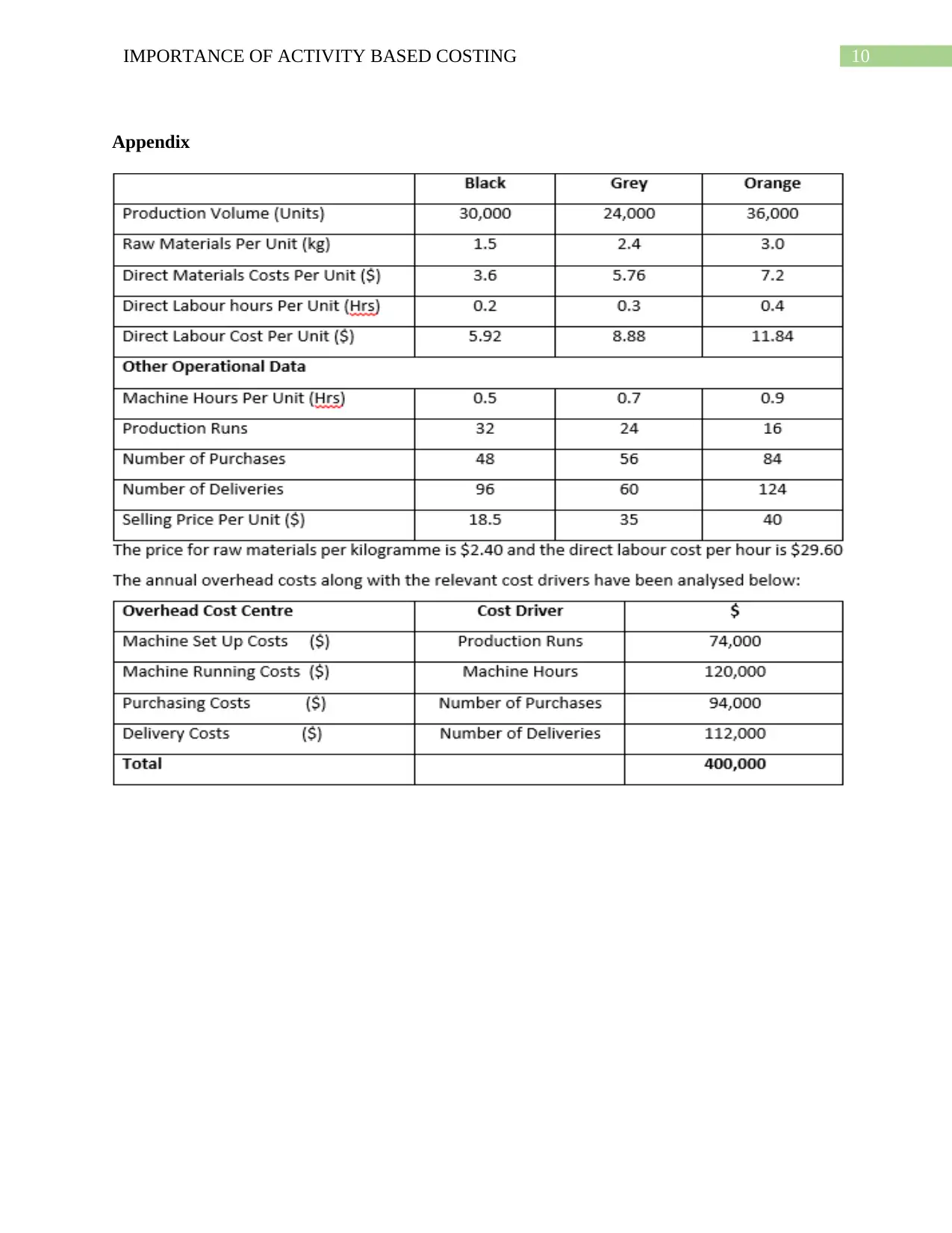

Appendix

Appendix

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.