Activity Based Costing Analysis and Recommendations for BOQ

VerifiedAdded on 2021/05/31

|15

|3175

|26

Report

AI Summary

This report examines the application of Activity-Based Costing (ABC) within the Bank of Queensland (BOQ). It begins with an overview of ABC, detailing its features and benefits in improving cost allocation and financial performance. The report then analyzes how BOQ can leverage ABC to align with its strategic objectives, including customer satisfaction and profitability. It explores BOQ's mission, objectives, and corporate strategies, demonstrating how ABC supports these goals through accurate cost management and improved decision-making. The analysis includes a visual representation of cost allocation and provides recommendations for the effective implementation of ABC within BOQ, emphasizing the importance of management support, employee training, and continuous process improvement. The report also suggests financial planning as an alternative or complementary management tool. Overall, the report provides a comprehensive analysis of ABC's potential to enhance BOQ's financial strategies and operational efficiency.

Activity based costing 1

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

ACTIVITY BASED COSTING

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 2

Table of Contents

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................4

Explanation of Activity based costing and its features................................................................................5

How Activity based costing system with the new strategies and goals of the Bank of Queensland............6

The mission and objectives of the Bank of Queensland..........................................................................6

Corporate strategy of the Bank of Queensland.......................................................................................7

Description on how activity based costing helps the BOQ in achieving its strategies..............................8

Recommendations for implementation of ABC (Activity based costing) model for MOQ.........................10

The alternative management tool appropriate for Bank of Queensland...................................................10

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Table of Contents

Executive summary.....................................................................................................................................3

Introduction.................................................................................................................................................4

Explanation of Activity based costing and its features................................................................................5

How Activity based costing system with the new strategies and goals of the Bank of Queensland............6

The mission and objectives of the Bank of Queensland..........................................................................6

Corporate strategy of the Bank of Queensland.......................................................................................7

Description on how activity based costing helps the BOQ in achieving its strategies..............................8

Recommendations for implementation of ABC (Activity based costing) model for MOQ.........................10

The alternative management tool appropriate for Bank of Queensland...................................................10

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Activity based costing 3

Executive summary

This paper discusses the application of the ABC system in Bank of Queensland. It does so

by describing how the Bank uses Activity-based costing to improve both the full costing systems

and partial costs. The paper starts with a brief explanation of the model. It then looks at the

features of the ABC system. Some of the benefits of this approach are that it addresses the

problems associated with the product mix, it helps the organization to save costs, and it also

improves the cost structure as well as the services and products that the firms provide to its

customers. The model can also help in reducing the complications of processes within the

organization (Siebold and Berger 2018). The implementation of this model into the organization

requires the management to fully support all the staff by the provision of the necessary

resources. Training of all the employees is also essential since it enables the entire team to gain

the required skills and knowledge on the use of the Activity-based costing system (Ning, Zhang

Bing and Baležentis 2018).

Executive summary

This paper discusses the application of the ABC system in Bank of Queensland. It does so

by describing how the Bank uses Activity-based costing to improve both the full costing systems

and partial costs. The paper starts with a brief explanation of the model. It then looks at the

features of the ABC system. Some of the benefits of this approach are that it addresses the

problems associated with the product mix, it helps the organization to save costs, and it also

improves the cost structure as well as the services and products that the firms provide to its

customers. The model can also help in reducing the complications of processes within the

organization (Siebold and Berger 2018). The implementation of this model into the organization

requires the management to fully support all the staff by the provision of the necessary

resources. Training of all the employees is also essential since it enables the entire team to gain

the required skills and knowledge on the use of the Activity-based costing system (Ning, Zhang

Bing and Baležentis 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 4

Introduction

Bank of Queensland is challenged with progressively more complex, dynamic and

diverse market environment. The demand for the bank services and products has led the Bank

of Queensland to establish new, non-traditional services and products and test new and

innovative methods with the intention of attracting funds from their customers. Besides, Bank

of Queensland has to change quickly and invent new technologies to enable it to be at the same

level with the increased moving, electronic economy (Du, Worthington and Zelenyuk 2018).

When any business changes the traditional ways of operation and starts running into another

new, diverse environment, then the company has to change the simple tools it initially uses to

manage its activities and measure its daily performance to do away with any errors associated

with the traditional ways of handling their operations. The bank also has to understand and

identify its profit areas, which is more crucial to any business to grow and be ahead of its

competitors. This will enable the bank to know the sources of their profits and services with the

high demand (Meng, Cavoli and Deng 2018). The bank will then use all these information to

make decisions which will increase the performance of the institution in the marketplace. One

of the significant problems that the Bank of Queensland is facing is coming up with a cost-

effective and accurate method of managing and measuring its portfolio of customers and

products (Almarzoqi, Mansour and Krichene 2018). The bank also needs accurately apportion

its costs to the services and products it sells as well as to the numerous customers that buy

their products in the market. The most appropriate resources for solving these challenges at

Bank of Queensland are the use of Activity-based costing (ABC) system. The paper starts by

describing the model and its features. It also discusses how the Bank of Queensland can use the

Introduction

Bank of Queensland is challenged with progressively more complex, dynamic and

diverse market environment. The demand for the bank services and products has led the Bank

of Queensland to establish new, non-traditional services and products and test new and

innovative methods with the intention of attracting funds from their customers. Besides, Bank

of Queensland has to change quickly and invent new technologies to enable it to be at the same

level with the increased moving, electronic economy (Du, Worthington and Zelenyuk 2018).

When any business changes the traditional ways of operation and starts running into another

new, diverse environment, then the company has to change the simple tools it initially uses to

manage its activities and measure its daily performance to do away with any errors associated

with the traditional ways of handling their operations. The bank also has to understand and

identify its profit areas, which is more crucial to any business to grow and be ahead of its

competitors. This will enable the bank to know the sources of their profits and services with the

high demand (Meng, Cavoli and Deng 2018). The bank will then use all these information to

make decisions which will increase the performance of the institution in the marketplace. One

of the significant problems that the Bank of Queensland is facing is coming up with a cost-

effective and accurate method of managing and measuring its portfolio of customers and

products (Almarzoqi, Mansour and Krichene 2018). The bank also needs accurately apportion

its costs to the services and products it sells as well as to the numerous customers that buy

their products in the market. The most appropriate resources for solving these challenges at

Bank of Queensland are the use of Activity-based costing (ABC) system. The paper starts by

describing the model and its features. It also discusses how the Bank of Queensland can use the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 5

ABC system to improve its operations. The next part presents the recommendation that should

be put in place to ensure smooth implementation of the model. Finally, the paper states the

best alternative accounting tool that can be used instead of or together with the ABC system.

Explanation of Activity based costing and its features

ABC system is a two-step costing method that starts with an allocation of costs with the

intention of identifying activities of any business and then after the identification of the

activities, and they are apportioned to services or products. An activity is a work element that

has to be performed to ensure completion of a project; this operation or process requires

resources and associated time (Popoola, Rayaan, Samsudin and Ahmad 2016). ABC system is a

TOM tool for performance and cost measurements of resources, activities, as well as cost

project. Activity-based costing is also called cross-functional or horizontal cost view. The model

can offer into detail the actual spending as well as the profitability of services, products,

distribution line, and customers (Bataev, Rodionov and Kosonogova 2018). The costing of

services or products depends on the activities performed by the organization to render specific

services or products. Example is where the bank makes product A, without the use of activity Y,

the actual cost associated with activity Y will not be apportioned to product A. The ABC system

is the most suitable technique of costing services or products since it assist most of the

organization in the identification of most of their activities, it then designates most of the costs

especially the direct costs to products (Nuaimi, Mohamed and Alekam 2017). The features of

the activity based costing include the following:

ABC system to improve its operations. The next part presents the recommendation that should

be put in place to ensure smooth implementation of the model. Finally, the paper states the

best alternative accounting tool that can be used instead of or together with the ABC system.

Explanation of Activity based costing and its features

ABC system is a two-step costing method that starts with an allocation of costs with the

intention of identifying activities of any business and then after the identification of the

activities, and they are apportioned to services or products. An activity is a work element that

has to be performed to ensure completion of a project; this operation or process requires

resources and associated time (Popoola, Rayaan, Samsudin and Ahmad 2016). ABC system is a

TOM tool for performance and cost measurements of resources, activities, as well as cost

project. Activity-based costing is also called cross-functional or horizontal cost view. The model

can offer into detail the actual spending as well as the profitability of services, products,

distribution line, and customers (Bataev, Rodionov and Kosonogova 2018). The costing of

services or products depends on the activities performed by the organization to render specific

services or products. Example is where the bank makes product A, without the use of activity Y,

the actual cost associated with activity Y will not be apportioned to product A. The ABC system

is the most suitable technique of costing services or products since it assist most of the

organization in the identification of most of their activities, it then designates most of the costs

especially the direct costs to products (Nuaimi, Mohamed and Alekam 2017). The features of

the activity based costing include the following:

Activity based costing 6

It enables the raw material of the Companies to cost less as compared to their finished

products, ABC system has the cost drivers that help in the determination of the behavior of

cost, the patterns of cost behavior are mostly linked to diversity, volume, time and events and

lastly, Activity-based costing is composed of 2 types that are variable cost and fixed cost that

are crucial in the provision of quality information which is being used in designing appropriate

system of cost (Becker et al. 2016).

How Activity based costing system with the new strategies and goals of the Bank of

Queensland

The mission and objectives of the Bank of Queensland

The mission of the Bank of Queensland is to become one of the loved banks in Australia.

It can be made possible by attending to activities that will satisfy the need of its customers in

the market. The company will do that by getting close contact and establishing long-lasting

relationships with its customers. The company will also focus on the use of proper

communication techniques to help foster the relationship between the customers and the Bank

of Queensland. The objectives of the BOQ are to create long-term relationships with its

customers that depend on the mutual understanding and respect, and the bank also strives to

deliver quality products to its customers, the bank also aims at creating products that are

simple and easy to understand to help in supporting the financial needs of their customers.

Other objectives of the bank include providing a variety of services to its business customers

and individuals, as well as collecting payments including interest, and charges on the services

and products offered to customers with the aim of making profits for stakeholders (Bawab and

It enables the raw material of the Companies to cost less as compared to their finished

products, ABC system has the cost drivers that help in the determination of the behavior of

cost, the patterns of cost behavior are mostly linked to diversity, volume, time and events and

lastly, Activity-based costing is composed of 2 types that are variable cost and fixed cost that

are crucial in the provision of quality information which is being used in designing appropriate

system of cost (Becker et al. 2016).

How Activity based costing system with the new strategies and goals of the Bank of

Queensland

The mission and objectives of the Bank of Queensland

The mission of the Bank of Queensland is to become one of the loved banks in Australia.

It can be made possible by attending to activities that will satisfy the need of its customers in

the market. The company will do that by getting close contact and establishing long-lasting

relationships with its customers. The company will also focus on the use of proper

communication techniques to help foster the relationship between the customers and the Bank

of Queensland. The objectives of the BOQ are to create long-term relationships with its

customers that depend on the mutual understanding and respect, and the bank also strives to

deliver quality products to its customers, the bank also aims at creating products that are

simple and easy to understand to help in supporting the financial needs of their customers.

Other objectives of the bank include providing a variety of services to its business customers

and individuals, as well as collecting payments including interest, and charges on the services

and products offered to customers with the aim of making profits for stakeholders (Bawab and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 7

Rawashdeh 2016). The bank also aims at changing the living standard of most of the people by

alleviating poverty in the country.

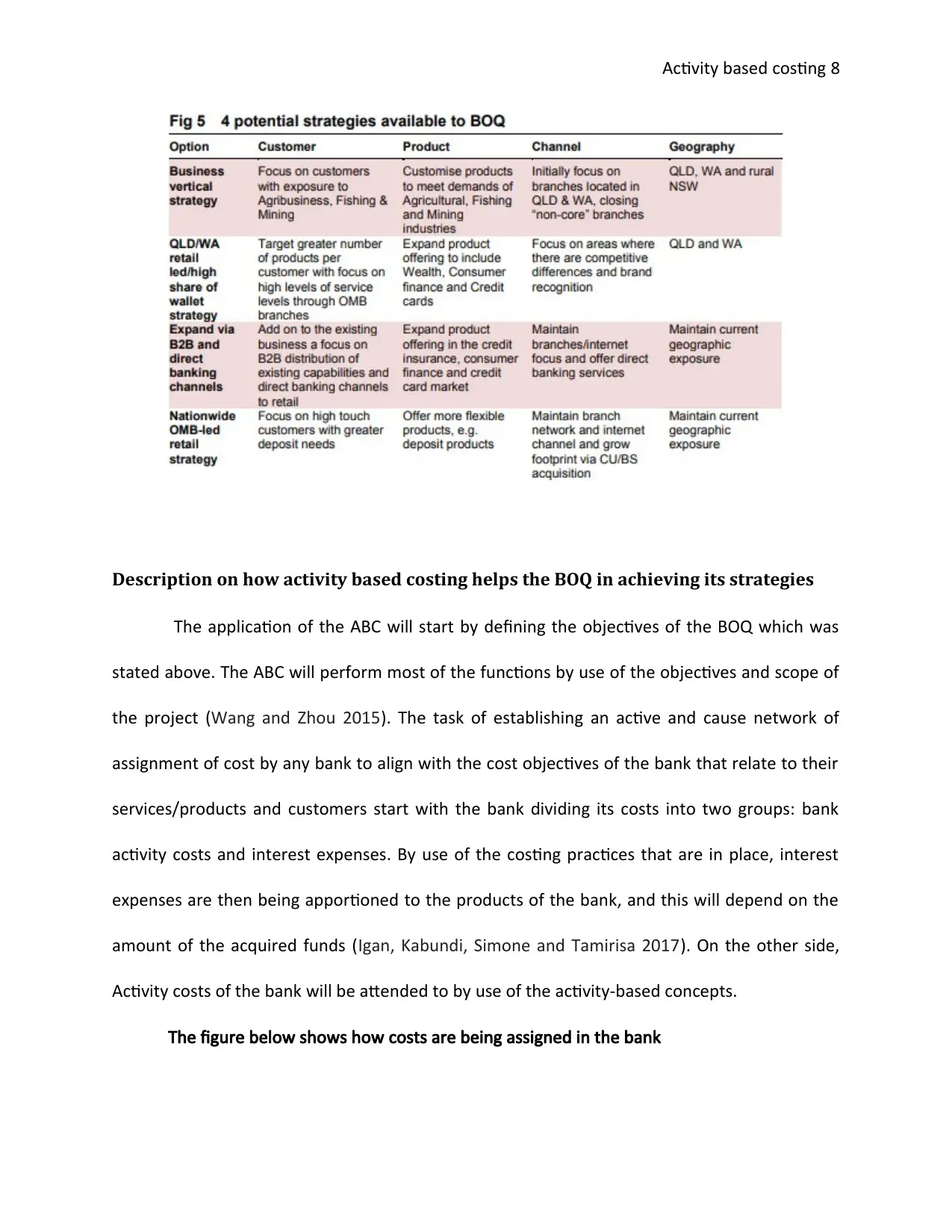

Corporate strategy of the Bank of Queensland

The Bank of Queensland made use of marketing strategy. The marketing team creates

good relationships between the bank and its customers in the marketplace. Through this

strategy, the bank will promote most of its services and many people will start to buy and use

their services hence leading to increased sales. The team will use the clash board to help in

tracking of all the performance of the campaign.

BOQ also merger with different banks such as the Metro bank, IGObaking and

Commerce Bank with the aim of getting a clear path of how to improve their returns by putting

their focus on geography/customers industry specialization. The three banks will divide the

market into segments, and each will target different areas with Commercial bank focusing on

Healthcare, Agribusiness, distribution and marketing, Metro Bank will put their target mainly on

the retail business, and lastly, IGObaking will target the ethnic client. There are four potential

strategies of the BOQ that is the Business vertical strategy, High share of wallet, national

strategy and Direct banking channel and B2B

Rawashdeh 2016). The bank also aims at changing the living standard of most of the people by

alleviating poverty in the country.

Corporate strategy of the Bank of Queensland

The Bank of Queensland made use of marketing strategy. The marketing team creates

good relationships between the bank and its customers in the marketplace. Through this

strategy, the bank will promote most of its services and many people will start to buy and use

their services hence leading to increased sales. The team will use the clash board to help in

tracking of all the performance of the campaign.

BOQ also merger with different banks such as the Metro bank, IGObaking and

Commerce Bank with the aim of getting a clear path of how to improve their returns by putting

their focus on geography/customers industry specialization. The three banks will divide the

market into segments, and each will target different areas with Commercial bank focusing on

Healthcare, Agribusiness, distribution and marketing, Metro Bank will put their target mainly on

the retail business, and lastly, IGObaking will target the ethnic client. There are four potential

strategies of the BOQ that is the Business vertical strategy, High share of wallet, national

strategy and Direct banking channel and B2B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 8

Description on how activity based costing helps the BOQ in achieving its strategies

The application of the ABC will start by defining the objectives of the BOQ which was

stated above. The ABC will perform most of the functions by use of the objectives and scope of

the project (Wang and Zhou 2015). The task of establishing an active and cause network of

assignment of cost by any bank to align with the cost objectives of the bank that relate to their

services/products and customers start with the bank dividing its costs into two groups: bank

activity costs and interest expenses. By use of the costing practices that are in place, interest

expenses are then being apportioned to the products of the bank, and this will depend on the

amount of the acquired funds (Igan, Kabundi, Simone and Tamirisa 2017). On the other side,

Activity costs of the bank will be attended to by use of the activity-based concepts.

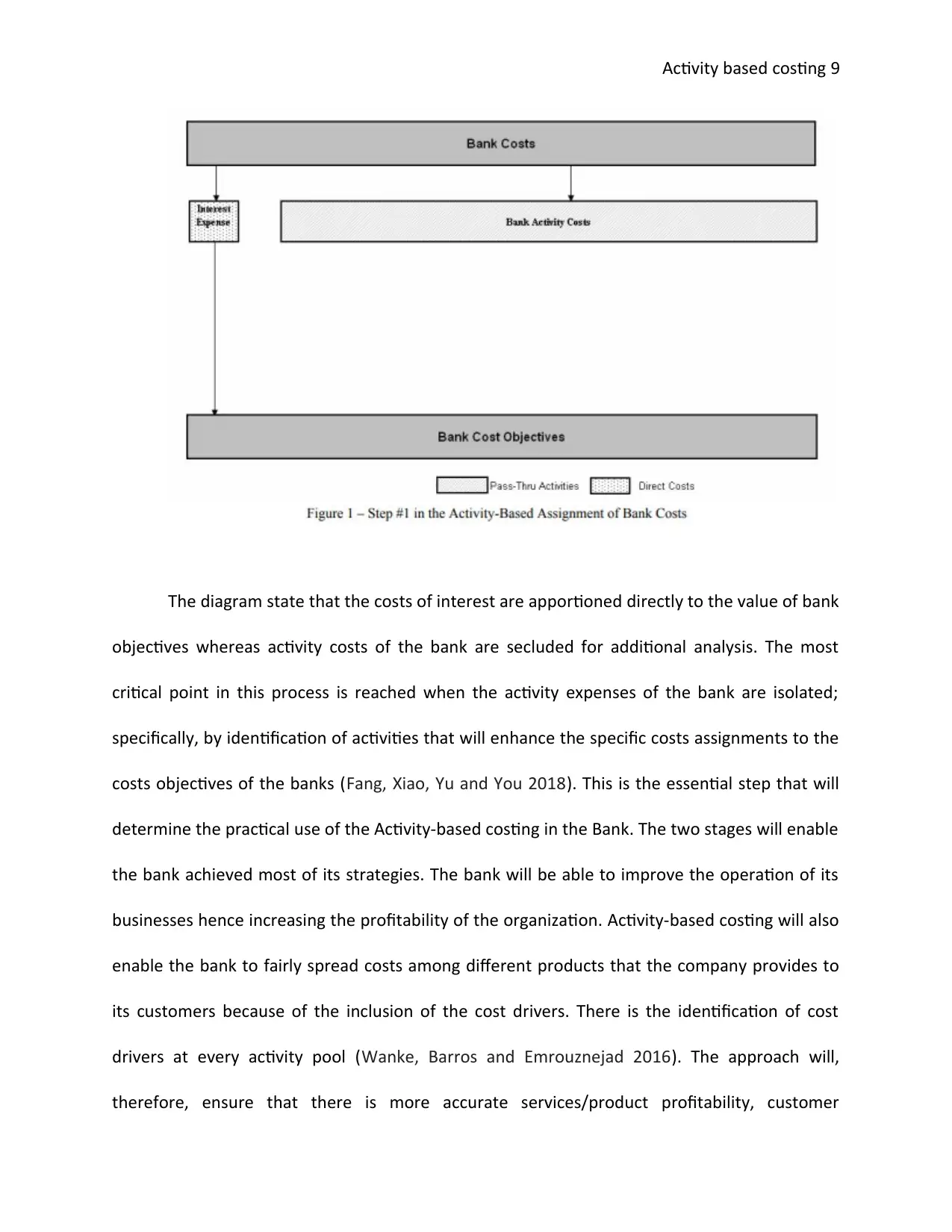

The figure below shows how costs are being assigned in the bank

Description on how activity based costing helps the BOQ in achieving its strategies

The application of the ABC will start by defining the objectives of the BOQ which was

stated above. The ABC will perform most of the functions by use of the objectives and scope of

the project (Wang and Zhou 2015). The task of establishing an active and cause network of

assignment of cost by any bank to align with the cost objectives of the bank that relate to their

services/products and customers start with the bank dividing its costs into two groups: bank

activity costs and interest expenses. By use of the costing practices that are in place, interest

expenses are then being apportioned to the products of the bank, and this will depend on the

amount of the acquired funds (Igan, Kabundi, Simone and Tamirisa 2017). On the other side,

Activity costs of the bank will be attended to by use of the activity-based concepts.

The figure below shows how costs are being assigned in the bank

Activity based costing 9

The diagram state that the costs of interest are apportioned directly to the value of bank

objectives whereas activity costs of the bank are secluded for additional analysis. The most

critical point in this process is reached when the activity expenses of the bank are isolated;

specifically, by identification of activities that will enhance the specific costs assignments to the

costs objectives of the banks (Fang, Xiao, Yu and You 2018). This is the essential step that will

determine the practical use of the Activity-based costing in the Bank. The two stages will enable

the bank achieved most of its strategies. The bank will be able to improve the operation of its

businesses hence increasing the profitability of the organization. Activity-based costing will also

enable the bank to fairly spread costs among different products that the company provides to

its customers because of the inclusion of the cost drivers. There is the identification of cost

drivers at every activity pool (Wanke, Barros and Emrouznejad 2016). The approach will,

therefore, ensure that there is more accurate services/product profitability, customer

The diagram state that the costs of interest are apportioned directly to the value of bank

objectives whereas activity costs of the bank are secluded for additional analysis. The most

critical point in this process is reached when the activity expenses of the bank are isolated;

specifically, by identification of activities that will enhance the specific costs assignments to the

costs objectives of the banks (Fang, Xiao, Yu and You 2018). This is the essential step that will

determine the practical use of the Activity-based costing in the Bank. The two stages will enable

the bank achieved most of its strategies. The bank will be able to improve the operation of its

businesses hence increasing the profitability of the organization. Activity-based costing will also

enable the bank to fairly spread costs among different products that the company provides to

its customers because of the inclusion of the cost drivers. There is the identification of cost

drivers at every activity pool (Wanke, Barros and Emrouznejad 2016). The approach will,

therefore, ensure that there is more accurate services/product profitability, customer

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing 10

profitability, the profitability of distribution of channel, Buy versus makes a decision,

outsourcing decision and the determination of transfer pricing.

Recommendations for implementation of ABC (Activity based costing) model for

MOQ

The management should implement the program known as the COPQ from the

perspective of the ABC system as this will enable continuous improvement of business

processes in the organization. Most of the traditional approach avoids the use of COPQ because

of it being expensive, but accurate use of the program can enable the ABC model to perform

according to the requirement of the firm (Etges, Souza, Kliemann and Felix 2018).

The management should provide enough training and support the employees with

required resources needed for the implementation of the Activity-based costing. There should

also be the training of managers to ensure that there are productivity, satisfaction and safety in

the workplace. Among the essential skills that the organization should use include employee

motivation, manager communication, and the recognition of the employees (Carauta et al.

2018).

The alternative management tool appropriate for Bank of Queensland

Being that this is the bank sector; the most suitable model that the organization should

use instead of the ABC system is the financial planning. This management tool will enable the

Bank to keep in check their current finances against their long-term goals. It will allow MOQ to

approximate the amount of money that they need to spend on a particular project. Financial

profitability, the profitability of distribution of channel, Buy versus makes a decision,

outsourcing decision and the determination of transfer pricing.

Recommendations for implementation of ABC (Activity based costing) model for

MOQ

The management should implement the program known as the COPQ from the

perspective of the ABC system as this will enable continuous improvement of business

processes in the organization. Most of the traditional approach avoids the use of COPQ because

of it being expensive, but accurate use of the program can enable the ABC model to perform

according to the requirement of the firm (Etges, Souza, Kliemann and Felix 2018).

The management should provide enough training and support the employees with

required resources needed for the implementation of the Activity-based costing. There should

also be the training of managers to ensure that there are productivity, satisfaction and safety in

the workplace. Among the essential skills that the organization should use include employee

motivation, manager communication, and the recognition of the employees (Carauta et al.

2018).

The alternative management tool appropriate for Bank of Queensland

Being that this is the bank sector; the most suitable model that the organization should

use instead of the ABC system is the financial planning. This management tool will enable the

Bank to keep in check their current finances against their long-term goals. It will allow MOQ to

approximate the amount of money that they need to spend on a particular project. Financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing 11

planning will also help the Bank to negotiate any incoming financial barriers that may arise at

any stage of the organization’s life (Mendonça and Silva 2018).

Conclusion

The paper discusses the application of the Activity-based costing in the banking sector, from

where we found how the model can be used to improve the performance of the Bank of

Queensland model. The model is not only more appropriate for service organizations for

example financial institution; it is also more suitable for a manufacturing environment.

Therefore, Bank of Queensland should apply the use of Activity-based costing concept to help in

improving most of its performance through the accurate allocation of costs to services and

products (Ishaq, Karim, Zaheer and Ahmed 2016). Through ABC model, Bank of Queensland can

apply unit costing, which is mostly being used to determine the value of services offered in the

bank by finding out the price as well as consumption of every unit of the firm’s output needed

for the delivery of the services. The paper also states that the practical implementation process

of the ABC model requires the management to provide enough support to the staff. The

administration should also provide enough training to all the employees about the use of the

Activity-based costing. Lastly, the most alternative control too which should use together with

the ABC system is the Financial planning (Elias and Mehrotra 2018).

planning will also help the Bank to negotiate any incoming financial barriers that may arise at

any stage of the organization’s life (Mendonça and Silva 2018).

Conclusion

The paper discusses the application of the Activity-based costing in the banking sector, from

where we found how the model can be used to improve the performance of the Bank of

Queensland model. The model is not only more appropriate for service organizations for

example financial institution; it is also more suitable for a manufacturing environment.

Therefore, Bank of Queensland should apply the use of Activity-based costing concept to help in

improving most of its performance through the accurate allocation of costs to services and

products (Ishaq, Karim, Zaheer and Ahmed 2016). Through ABC model, Bank of Queensland can

apply unit costing, which is mostly being used to determine the value of services offered in the

bank by finding out the price as well as consumption of every unit of the firm’s output needed

for the delivery of the services. The paper also states that the practical implementation process

of the ABC model requires the management to provide enough support to the staff. The

administration should also provide enough training to all the employees about the use of the

Activity-based costing. Lastly, the most alternative control too which should use together with

the ABC system is the Financial planning (Elias and Mehrotra 2018).

Activity based costing 12

References

Al-Bawab, A.A. and Al-Rawashdeh, H., 2016. The Impact of the Activity Based Costing System

(ABC) in the Pricing of Services Banks in the Jordanian commercial Banks: A Field

Study.

International Business Research,

9(4), p.1.

Almarzoqi, R.M., Mansour, W. and Krichene, N., 2018.

Islamic Macroeconomics: A Model for

Efficient Government, Stability and Full Employment. Routledge.

Al-Nuaimi, S.I.M., Mohamed, R. and Alekam, J.M.E., 2017. The Link between Information

Technology, Activity-based Costing Implementation and Organizational

Performance.

International Review of Management and Marketing,

7(1).

Bataev, A.V., Rodionov, D.G. and Kosonogova, E.S., 2018, January. Evaluation of efficiency of

using bank smart-card in Russian financial institutions. In

Information Networking (ICOIN), 2018

International Conference on (pp. 589-593). IEEE.

Becker, J., Delfmann, P., Dietrich, H.A., Steinhorst, M. and Eggert, M., 2016. Business process

compliance checking–applying and evaluating a generic pattern matching approach for

conceptual models in the financial sector.

Information Systems Frontiers,

18(2), pp.359-405.

References

Al-Bawab, A.A. and Al-Rawashdeh, H., 2016. The Impact of the Activity Based Costing System

(ABC) in the Pricing of Services Banks in the Jordanian commercial Banks: A Field

Study.

International Business Research,

9(4), p.1.

Almarzoqi, R.M., Mansour, W. and Krichene, N., 2018.

Islamic Macroeconomics: A Model for

Efficient Government, Stability and Full Employment. Routledge.

Al-Nuaimi, S.I.M., Mohamed, R. and Alekam, J.M.E., 2017. The Link between Information

Technology, Activity-based Costing Implementation and Organizational

Performance.

International Review of Management and Marketing,

7(1).

Bataev, A.V., Rodionov, D.G. and Kosonogova, E.S., 2018, January. Evaluation of efficiency of

using bank smart-card in Russian financial institutions. In

Information Networking (ICOIN), 2018

International Conference on (pp. 589-593). IEEE.

Becker, J., Delfmann, P., Dietrich, H.A., Steinhorst, M. and Eggert, M., 2016. Business process

compliance checking–applying and evaluating a generic pattern matching approach for

conceptual models in the financial sector.

Information Systems Frontiers,

18(2), pp.359-405.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.