Managerial Accounting Report: ABC System and Integral Diagnostics

VerifiedAdded on 2021/05/31

|15

|3137

|27

Report

AI Summary

This report provides a comprehensive analysis of the activity-based costing (ABC) system, focusing on its characteristics, implementation, and benefits within the context of Integral Diagnostics Limited, an ASX-listed healthcare service provider. The report examines how the ABC system aligns with the company's goals and strategies, particularly in enhancing its management accounting approach. It highlights the advantages of ABC in identifying cost drivers and allocating costs more accurately than traditional methods, especially within the healthcare sector where direct costs are often categorized as overhead expenses. The report explores how Integral Diagnostics Limited can leverage the ABC system to optimize its cost structure, improve service pricing, and enhance brand awareness. Furthermore, the report recommends the implementation of budgetary control as an alternative management accounting technique to increase the overall cost efficiency of Integral Diagnostics Limited. The report also emphasizes the importance of top management support and a cross-functional team for successful ABC system implementation. The analysis includes a discussion of the company's mission, corporate strategies, and the specific activities where the ABC model can provide valuable insights for better financial management.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

In this report, evaluation is made regarding the various aspects related to activity-

based costing (ABC) system comprising of its characteristics, enforcement and others from

the company perspective. For satisfying the report criteria, ABC system is associated with

Integral Diagnostics Limited listed in ASX, since it is highly valuable for enhancing

management accounting approach of the higher management of the organisation. In case of

Integral Diagnostics Limited, ABC model could play a significant role by detecting those

particular business activities, which need special attention and evaluation. Depending on

this analysis, it would be helpful for the stated organisation to allocate costs to the activities

that are rendered mostly to the customers. Finally, budgetary control could be used in the

form of alternative management accounting technique so that the overall cost efficiency of

Integral Diagnostics Limited is increased.

Executive Summary:

In this report, evaluation is made regarding the various aspects related to activity-

based costing (ABC) system comprising of its characteristics, enforcement and others from

the company perspective. For satisfying the report criteria, ABC system is associated with

Integral Diagnostics Limited listed in ASX, since it is highly valuable for enhancing

management accounting approach of the higher management of the organisation. In case of

Integral Diagnostics Limited, ABC model could play a significant role by detecting those

particular business activities, which need special attention and evaluation. Depending on

this analysis, it would be helpful for the stated organisation to allocate costs to the activities

that are rendered mostly to the customers. Finally, budgetary control could be used in the

form of alternative management accounting technique so that the overall cost efficiency of

Integral Diagnostics Limited is increased.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

Answer to Part a:........................................................................................................................3

Answer to Part b:.......................................................................................................................5

Requirement i:........................................................................................................................5

Requirement ii:.......................................................................................................................6

Requirement iii:......................................................................................................................6

Answer to Part c:........................................................................................................................8

Answer to Part d:.......................................................................................................................9

Conclusion:...............................................................................................................................10

References:...............................................................................................................................12

Table of Contents

Introduction:..............................................................................................................................3

Answer to Part a:........................................................................................................................3

Answer to Part b:.......................................................................................................................5

Requirement i:........................................................................................................................5

Requirement ii:.......................................................................................................................6

Requirement iii:......................................................................................................................6

Answer to Part c:........................................................................................................................8

Answer to Part d:.......................................................................................................................9

Conclusion:...............................................................................................................................10

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

This report intends to evaluate the various aspects related to activity-based costing

(ABC) system comprising of its characteristics, enforcement and others from the company

perspective. For satisfying the report criteria, ABC system is associated with Integral

Diagnostics Limited listed in ASX, since it is highly valuable for enhancing management

accounting approach of the higher management of the organisation. It is a healthcare

service provider of diagnostic imaging services, medical specialists, general practitioners

along with allied health professionals and patients in Australia (Integraldiagnostics.com.au

2018). Effort has been made in aligning the ABC system with the goals and strategies if the

organisation for enhancing its management accounting system. Finally, effective

recommendations have been provided to enforce the system within the organisation along

with identifying another suitable management accounting tool based on the departmental

needs.

Answer to Part a:

One of the significant costing methods is the ABC system and it involves identifying

the activities conducted during the business operations based on which the products are

assigned with indirect costs (Al-Sayed and Dugdale 2016). Moreover, emphasis is placed on

the association among costs, products and activities for apportioning the indirect costs to

products with less subjectivity as opposed to the conventional costing system. However, the

managers find it complicated in apportioning few particular costs through the ABC system

and these include indirect expenses like office staff salaries and this cost could not be

apportioned easily to the manufactured product. As a result of this, popularity of the ABC

Introduction:

This report intends to evaluate the various aspects related to activity-based costing

(ABC) system comprising of its characteristics, enforcement and others from the company

perspective. For satisfying the report criteria, ABC system is associated with Integral

Diagnostics Limited listed in ASX, since it is highly valuable for enhancing management

accounting approach of the higher management of the organisation. It is a healthcare

service provider of diagnostic imaging services, medical specialists, general practitioners

along with allied health professionals and patients in Australia (Integraldiagnostics.com.au

2018). Effort has been made in aligning the ABC system with the goals and strategies if the

organisation for enhancing its management accounting system. Finally, effective

recommendations have been provided to enforce the system within the organisation along

with identifying another suitable management accounting tool based on the departmental

needs.

Answer to Part a:

One of the significant costing methods is the ABC system and it involves identifying

the activities conducted during the business operations based on which the products are

assigned with indirect costs (Al-Sayed and Dugdale 2016). Moreover, emphasis is placed on

the association among costs, products and activities for apportioning the indirect costs to

products with less subjectivity as opposed to the conventional costing system. However, the

managers find it complicated in apportioning few particular costs through the ABC system

and these include indirect expenses like office staff salaries and this cost could not be

apportioned easily to the manufactured product. As a result of this, popularity of the ABC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

system has increased widely in different industries, especially, the manufacturing sector.

Moreover, it is possible to use ABC system in product costing, target costing, service pricing

and other aspects (Barros and Ferreira 2017).

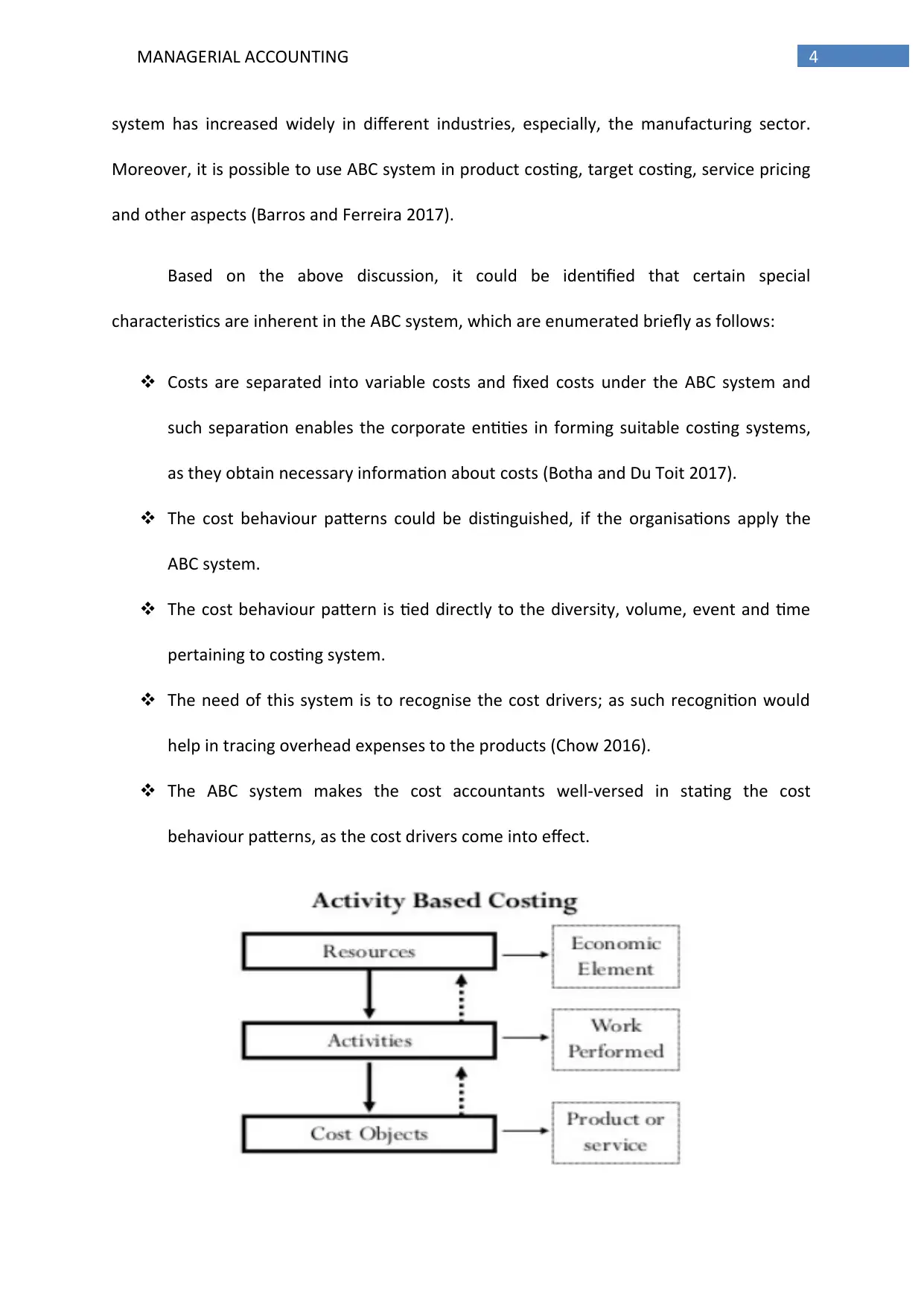

Based on the above discussion, it could be identified that certain special

characteristics are inherent in the ABC system, which are enumerated briefly as follows:

Costs are separated into variable costs and fixed costs under the ABC system and

such separation enables the corporate entities in forming suitable costing systems,

as they obtain necessary information about costs (Botha and Du Toit 2017).

The cost behaviour patterns could be distinguished, if the organisations apply the

ABC system.

The cost behaviour pattern is tied directly to the diversity, volume, event and time

pertaining to costing system.

The need of this system is to recognise the cost drivers; as such recognition would

help in tracing overhead expenses to the products (Chow 2016).

The ABC system makes the cost accountants well-versed in stating the cost

behaviour patterns, as the cost drivers come into effect.

system has increased widely in different industries, especially, the manufacturing sector.

Moreover, it is possible to use ABC system in product costing, target costing, service pricing

and other aspects (Barros and Ferreira 2017).

Based on the above discussion, it could be identified that certain special

characteristics are inherent in the ABC system, which are enumerated briefly as follows:

Costs are separated into variable costs and fixed costs under the ABC system and

such separation enables the corporate entities in forming suitable costing systems,

as they obtain necessary information about costs (Botha and Du Toit 2017).

The cost behaviour patterns could be distinguished, if the organisations apply the

ABC system.

The cost behaviour pattern is tied directly to the diversity, volume, event and time

pertaining to costing system.

The need of this system is to recognise the cost drivers; as such recognition would

help in tracing overhead expenses to the products (Chow 2016).

The ABC system makes the cost accountants well-versed in stating the cost

behaviour patterns, as the cost drivers come into effect.

5MANAGERIAL ACCOUNTING

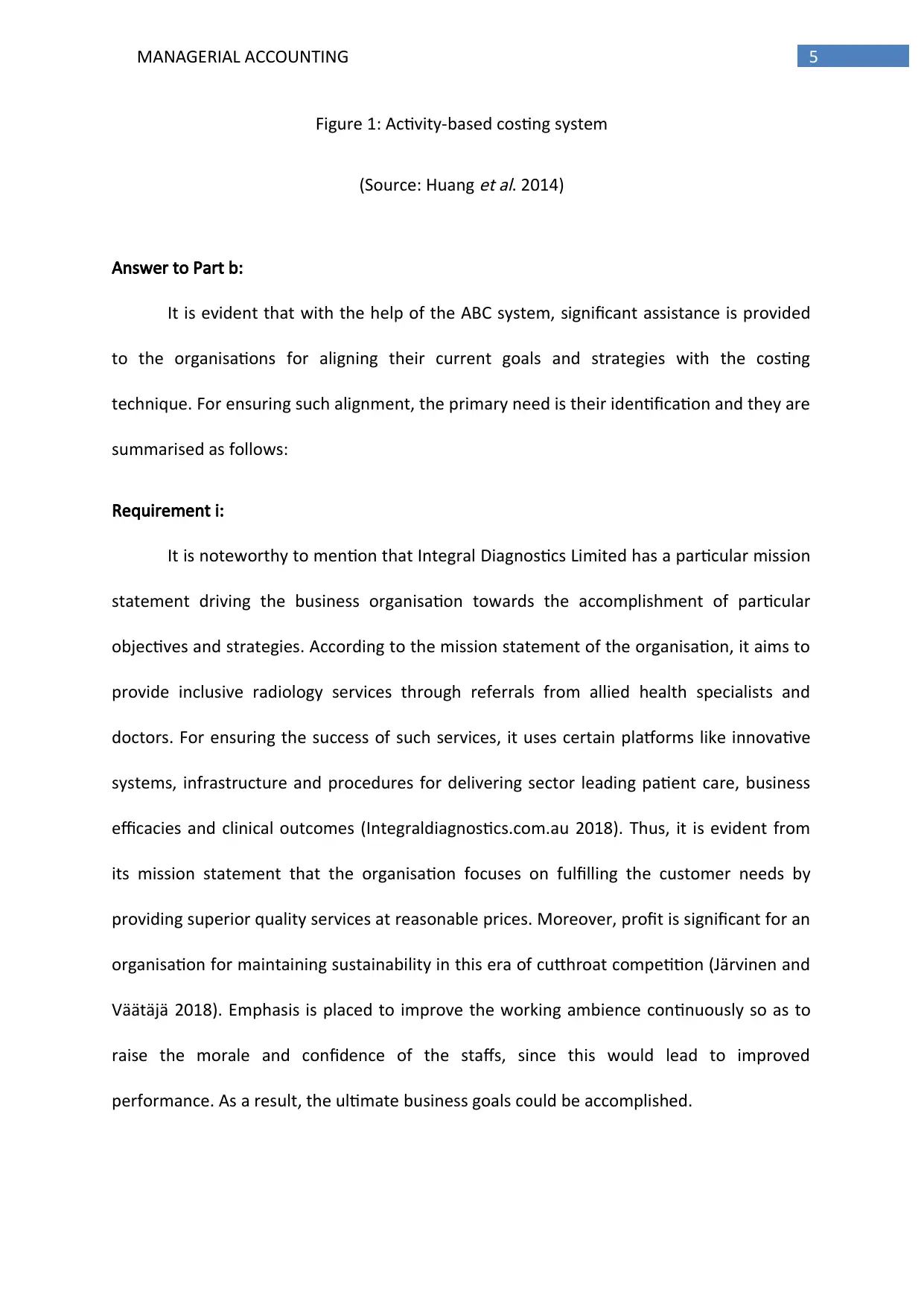

Figure 1: Activity-based costing system

(Source: Huang

et al. 2014)

Answer to Part b:

It is evident that with the help of the ABC system, significant assistance is provided

to the organisations for aligning their current goals and strategies with the costing

technique. For ensuring such alignment, the primary need is their identification and they are

summarised as follows:

Requirement i:

It is noteworthy to mention that Integral Diagnostics Limited has a particular mission

statement driving the business organisation towards the accomplishment of particular

objectives and strategies. According to the mission statement of the organisation, it aims to

provide inclusive radiology services through referrals from allied health specialists and

doctors. For ensuring the success of such services, it uses certain platforms like innovative

systems, infrastructure and procedures for delivering sector leading patient care, business

efficacies and clinical outcomes (Integraldiagnostics.com.au 2018). Thus, it is evident from

its mission statement that the organisation focuses on fulfilling the customer needs by

providing superior quality services at reasonable prices. Moreover, profit is significant for an

organisation for maintaining sustainability in this era of cutthroat competition (Järvinen and

Väätäjä 2018). Emphasis is placed to improve the working ambience continuously so as to

raise the morale and confidence of the staffs, since this would lead to improved

performance. As a result, the ultimate business goals could be accomplished.

Figure 1: Activity-based costing system

(Source: Huang

et al. 2014)

Answer to Part b:

It is evident that with the help of the ABC system, significant assistance is provided

to the organisations for aligning their current goals and strategies with the costing

technique. For ensuring such alignment, the primary need is their identification and they are

summarised as follows:

Requirement i:

It is noteworthy to mention that Integral Diagnostics Limited has a particular mission

statement driving the business organisation towards the accomplishment of particular

objectives and strategies. According to the mission statement of the organisation, it aims to

provide inclusive radiology services through referrals from allied health specialists and

doctors. For ensuring the success of such services, it uses certain platforms like innovative

systems, infrastructure and procedures for delivering sector leading patient care, business

efficacies and clinical outcomes (Integraldiagnostics.com.au 2018). Thus, it is evident from

its mission statement that the organisation focuses on fulfilling the customer needs by

providing superior quality services at reasonable prices. Moreover, profit is significant for an

organisation for maintaining sustainability in this era of cutthroat competition (Järvinen and

Väätäjä 2018). Emphasis is placed to improve the working ambience continuously so as to

raise the morale and confidence of the staffs, since this would lead to improved

performance. As a result, the ultimate business goals could be accomplished.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

Requirement ii:

Integral Diagnostics Limited has developed its corporate strategies in such a manner

that its business objectives are achieved and these strategies are summarised briefly as

follows:

The primary corporate strategy of the organisation is to offer quality services to all

the rural patients in Australia as well as the other urban individuals so that profit

level could be increased while devising out suitable ways to reduce the business

cost.

The next strategy is to expand further in the rural areas for providing support to the

rural communities that would help in developing positive brand image of the

organisation.

Thirdly, Integral Diagnostics Limited aims to initiate new centres all over the nation

by adopting cost-efficient techniques so as to increase its profit margin.

Fourthly, it takes necessary steps for assuring that the newly opened centres

encounter positive future growth that would assist in increasing its earnings.

Finally, it focuses on valuing evidence-based medicines for the best possible

outcomes of the patients.

Requirement iii:

ABC model is widely utilised in the manufacturing industry; however, it has certain

characteristics that could not be overlooked in the healthcare sector as well. It is identified

that the healthcare service providers do not bear any direct cost; instead, the costs incurred

are categorised as overhead expenses. By adopting the ABC system, it is possible for Integral

Requirement ii:

Integral Diagnostics Limited has developed its corporate strategies in such a manner

that its business objectives are achieved and these strategies are summarised briefly as

follows:

The primary corporate strategy of the organisation is to offer quality services to all

the rural patients in Australia as well as the other urban individuals so that profit

level could be increased while devising out suitable ways to reduce the business

cost.

The next strategy is to expand further in the rural areas for providing support to the

rural communities that would help in developing positive brand image of the

organisation.

Thirdly, Integral Diagnostics Limited aims to initiate new centres all over the nation

by adopting cost-efficient techniques so as to increase its profit margin.

Fourthly, it takes necessary steps for assuring that the newly opened centres

encounter positive future growth that would assist in increasing its earnings.

Finally, it focuses on valuing evidence-based medicines for the best possible

outcomes of the patients.

Requirement iii:

ABC model is widely utilised in the manufacturing industry; however, it has certain

characteristics that could not be overlooked in the healthcare sector as well. It is identified

that the healthcare service providers do not bear any direct cost; instead, the costs incurred

are categorised as overhead expenses. By adopting the ABC system, it is possible for Integral

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Diagnostics Limited to enjoy certain benefits that would fulfil its business strategies and

objectives (Lu, Sridharan and Michael 2016).

ABC system has activity, resources and cost objective sections. For Integral

Diagnostics Limited, the resource section includes the costs of its various departments.

Certain segments are there in these departments, which include the following:

Corporate office

Call centres

Selling channels such as direct selling agents and online portals

Shared service departments such as information technology and human resources

For calculating cost, it is important to explain the shared services (Mumford

et al.

2015). The departmental service volumes are taken into consideration so that costs could be

passed over to the other departments. Besides, there are different branches of the

organisation, in which grouping could be conducted depending on costs. Therefore, it could

be stated that the ABC system increases the cost assignment scope for all branches and as a

result, advertising costs could be anticipated appropriately (Orwig

et al. 2015).

The cost objectives are those, which could be explained depending on the business

transactions and operations that Integral Diagnostics Limited carry out for selling various

types of services. Hence, from the perspective of the organisation, these activities might be

the purchase of wholesale equipment, order receipt, services rendered to the customers,

after service support and others (Parker 2016). After explaining these transactions,

separation is to be made into activities in the ABC system. After this, the activities would be

named and timed and they would be put against each of them. In this case, batch size is

Diagnostics Limited to enjoy certain benefits that would fulfil its business strategies and

objectives (Lu, Sridharan and Michael 2016).

ABC system has activity, resources and cost objective sections. For Integral

Diagnostics Limited, the resource section includes the costs of its various departments.

Certain segments are there in these departments, which include the following:

Corporate office

Call centres

Selling channels such as direct selling agents and online portals

Shared service departments such as information technology and human resources

For calculating cost, it is important to explain the shared services (Mumford

et al.

2015). The departmental service volumes are taken into consideration so that costs could be

passed over to the other departments. Besides, there are different branches of the

organisation, in which grouping could be conducted depending on costs. Therefore, it could

be stated that the ABC system increases the cost assignment scope for all branches and as a

result, advertising costs could be anticipated appropriately (Orwig

et al. 2015).

The cost objectives are those, which could be explained depending on the business

transactions and operations that Integral Diagnostics Limited carry out for selling various

types of services. Hence, from the perspective of the organisation, these activities might be

the purchase of wholesale equipment, order receipt, services rendered to the customers,

after service support and others (Parker 2016). After explaining these transactions,

separation is to be made into activities in the ABC system. After this, the activities would be

named and timed and they would be put against each of them. In this case, batch size is

8MANAGERIAL ACCOUNTING

significant for performing activities in batch mode. Thus, the departmental needs are taken

into account to group activities in the ABC system. It would help Integral Diagnostics Limited

in minimising the additional cost pressure from the patients and the new technology could

be implemented as well (Patrick, Blessing and Gloria 2015).

It is possible to distinguish cost objective into two sections. The first section includes

calculating the additional cost to be borne by the patients for different services and the

channels of distribution would be different as well. This could be the sale of radiology

services and diagnostic imaging services. It is evaluated that the patients would have to bear

the same additional cost for both services (Phan, Baird and Blair 2014). However, the costs

should not be calculated in combination, as radiology services are provided more as

opposed to diagnostic imaging services. If it adopts the ABC system, it could identify the

service that is rendered more between the two services. Thus, brand awareness could be

developed for the organisation that would ensure both business sustainability and

competitive advantage.

Answer to Part c:

The top level management of Integral Diagnostics Limited should extend support, if

ABC system is to be implemented within the organisation. Once the approval is sought, it is

the duty of the cross-functional team to develop as well as implement the model rather

than the accounting department. In this case, a special team needs to be developed by

unifying members from each department to use data derived from the ABC system.

Moreover, external specialists could be appointed, as their advice would ensure successful

enforcement of the ABC system (Quinn, Elafi and Mulgrew 2017).

significant for performing activities in batch mode. Thus, the departmental needs are taken

into account to group activities in the ABC system. It would help Integral Diagnostics Limited

in minimising the additional cost pressure from the patients and the new technology could

be implemented as well (Patrick, Blessing and Gloria 2015).

It is possible to distinguish cost objective into two sections. The first section includes

calculating the additional cost to be borne by the patients for different services and the

channels of distribution would be different as well. This could be the sale of radiology

services and diagnostic imaging services. It is evaluated that the patients would have to bear

the same additional cost for both services (Phan, Baird and Blair 2014). However, the costs

should not be calculated in combination, as radiology services are provided more as

opposed to diagnostic imaging services. If it adopts the ABC system, it could identify the

service that is rendered more between the two services. Thus, brand awareness could be

developed for the organisation that would ensure both business sustainability and

competitive advantage.

Answer to Part c:

The top level management of Integral Diagnostics Limited should extend support, if

ABC system is to be implemented within the organisation. Once the approval is sought, it is

the duty of the cross-functional team to develop as well as implement the model rather

than the accounting department. In this case, a special team needs to be developed by

unifying members from each department to use data derived from the ABC system.

Moreover, external specialists could be appointed, as their advice would ensure successful

enforcement of the ABC system (Quinn, Elafi and Mulgrew 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Certain reasons are evident to steer the top management of Integral Diagnostics

Limited in supporting the system. Primarily, the managers and the subordinates might not

show adequate interest to accept the change, if the top management does not show

adequate interest regarding the implementation of the ABC model. Secondly, the

importance of this system would not be much in the eyes of the employees, if there is lack

of support from the management of the organisation. For ensuring successful adoption of

this system, the management of Integral Diagnostics Limited should develop an in-depth

knowledge about the current costing technique inherent within the organisation. In order to

allocate costs suitably, the role of the cross-functional team is worth mentioning, as much of

the success of implementation relies on the team (Rodríguez-Olalla and Avilés-Palacios

2017).

Answer to Part d:

As already evaluated, ABC model would fetch immense benefits to Integral

Diagnostics Limited, if it is implemented successfully within the organisation. However,

certain other management accounting tools are available, which could meet the interests of

the organisation. Out of such tools, budgetary control could be taken into account for the

organisation. This is because budgets are highly advantageous to conduct planning and

controlling the business processes. Along with this, the managers of Integral Diagnostics

Limited would have the option of utilising the budgets for planning, controlling as well as

monitoring various kinds of activities that take place in the normal business cycle (Rooney

and Dumay 2016). Benefits are deemed to be obtained when budgetary control would be

introduced in Integral Diagnostics Limited and these benefits are undernoted:

Certain reasons are evident to steer the top management of Integral Diagnostics

Limited in supporting the system. Primarily, the managers and the subordinates might not

show adequate interest to accept the change, if the top management does not show

adequate interest regarding the implementation of the ABC model. Secondly, the

importance of this system would not be much in the eyes of the employees, if there is lack

of support from the management of the organisation. For ensuring successful adoption of

this system, the management of Integral Diagnostics Limited should develop an in-depth

knowledge about the current costing technique inherent within the organisation. In order to

allocate costs suitably, the role of the cross-functional team is worth mentioning, as much of

the success of implementation relies on the team (Rodríguez-Olalla and Avilés-Palacios

2017).

Answer to Part d:

As already evaluated, ABC model would fetch immense benefits to Integral

Diagnostics Limited, if it is implemented successfully within the organisation. However,

certain other management accounting tools are available, which could meet the interests of

the organisation. Out of such tools, budgetary control could be taken into account for the

organisation. This is because budgets are highly advantageous to conduct planning and

controlling the business processes. Along with this, the managers of Integral Diagnostics

Limited would have the option of utilising the budgets for planning, controlling as well as

monitoring various kinds of activities that take place in the normal business cycle (Rooney

and Dumay 2016). Benefits are deemed to be obtained when budgetary control would be

introduced in Integral Diagnostics Limited and these benefits are undernoted:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

When budgetary control is enforced, it makes easy for the management of Integral

Diagnostics Limited in integrating the actions of the staffs towards the fulfilment of a

sole and common objective. Moreover, budgetary control ensures synchronisation

that would help in meeting the set standards and targets at the start of the financial

year.

The budgetary control techniques enable to undertake corrective actions, if the

amount estimated for a particular department at the start of the period is more than

the one incurred at the end of the period.

With the help of budgetary control, it would become relatively easy for the

management of Integral Diagnostics Limited to know about the previous events, in

which errors were made. The information accumulated should be evaluated

accordingly and steps could be taken for assuring that such errors do not happen in

future or at least their chances would be reduced. Hence, budgetary control sets out

the platform where suitable strategies could be framed to deal with the unexpected

contingencies as well as rectifying past errors.

Conclusion:

It is evident from the above discussion and evaluation that base for separating costs

into fixed costs and variable costs could be developed with the help of the ABC system. Such

separation would allow the business entities to formulate as well as enforced the needed

costing services. In case of Integral Diagnostics Limited, ABC model could play a significant

role by detecting those particular business activities, which need special attention and

evaluation. Depending on this analysis, it would be helpful for the stated organisation to

allocate costs to the activities that are rendered mostly to the customers. Finally, budgetary

When budgetary control is enforced, it makes easy for the management of Integral

Diagnostics Limited in integrating the actions of the staffs towards the fulfilment of a

sole and common objective. Moreover, budgetary control ensures synchronisation

that would help in meeting the set standards and targets at the start of the financial

year.

The budgetary control techniques enable to undertake corrective actions, if the

amount estimated for a particular department at the start of the period is more than

the one incurred at the end of the period.

With the help of budgetary control, it would become relatively easy for the

management of Integral Diagnostics Limited to know about the previous events, in

which errors were made. The information accumulated should be evaluated

accordingly and steps could be taken for assuring that such errors do not happen in

future or at least their chances would be reduced. Hence, budgetary control sets out

the platform where suitable strategies could be framed to deal with the unexpected

contingencies as well as rectifying past errors.

Conclusion:

It is evident from the above discussion and evaluation that base for separating costs

into fixed costs and variable costs could be developed with the help of the ABC system. Such

separation would allow the business entities to formulate as well as enforced the needed

costing services. In case of Integral Diagnostics Limited, ABC model could play a significant

role by detecting those particular business activities, which need special attention and

evaluation. Depending on this analysis, it would be helpful for the stated organisation to

allocate costs to the activities that are rendered mostly to the customers. Finally, budgetary

11MANAGERIAL ACCOUNTING

control could be used in the form of alternative management accounting technique so that

the overall cost efficiency of Integral Diagnostics Limited is increased. This is because such

cost efficiency would minimise the burden of additional cost from the patients and the

organisation could provide services to the patients at prices, which are reasonable and

within the reach of the patients.

control could be used in the form of alternative management accounting technique so that

the overall cost efficiency of Integral Diagnostics Limited is increased. This is because such

cost efficiency would minimise the burden of additional cost from the patients and the

organisation could provide services to the patients at prices, which are reasonable and

within the reach of the patients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.