Financial Analysis of Cost Reduction Techniques and Methods

VerifiedAdded on 2021/02/19

|7

|1407

|21

Report

AI Summary

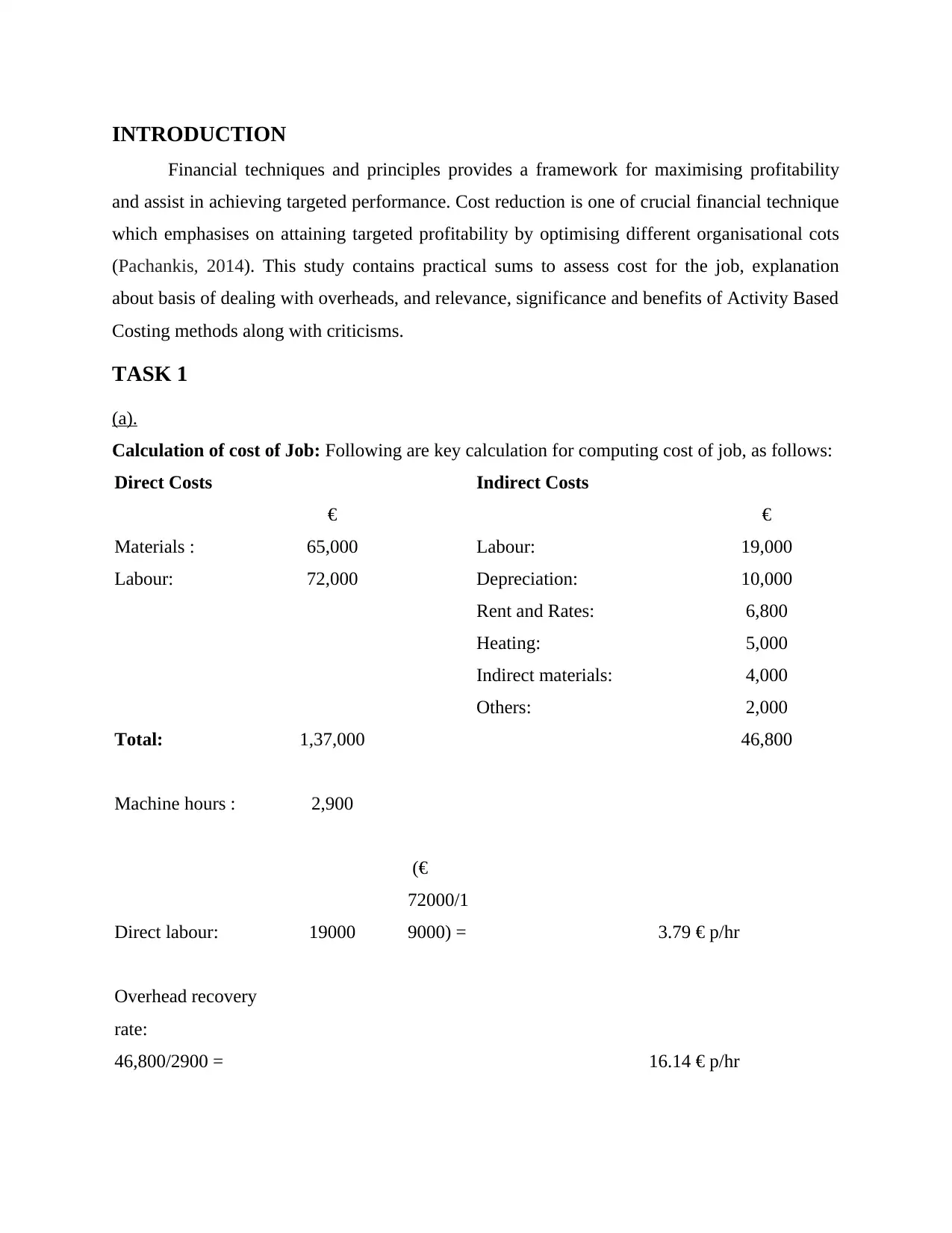

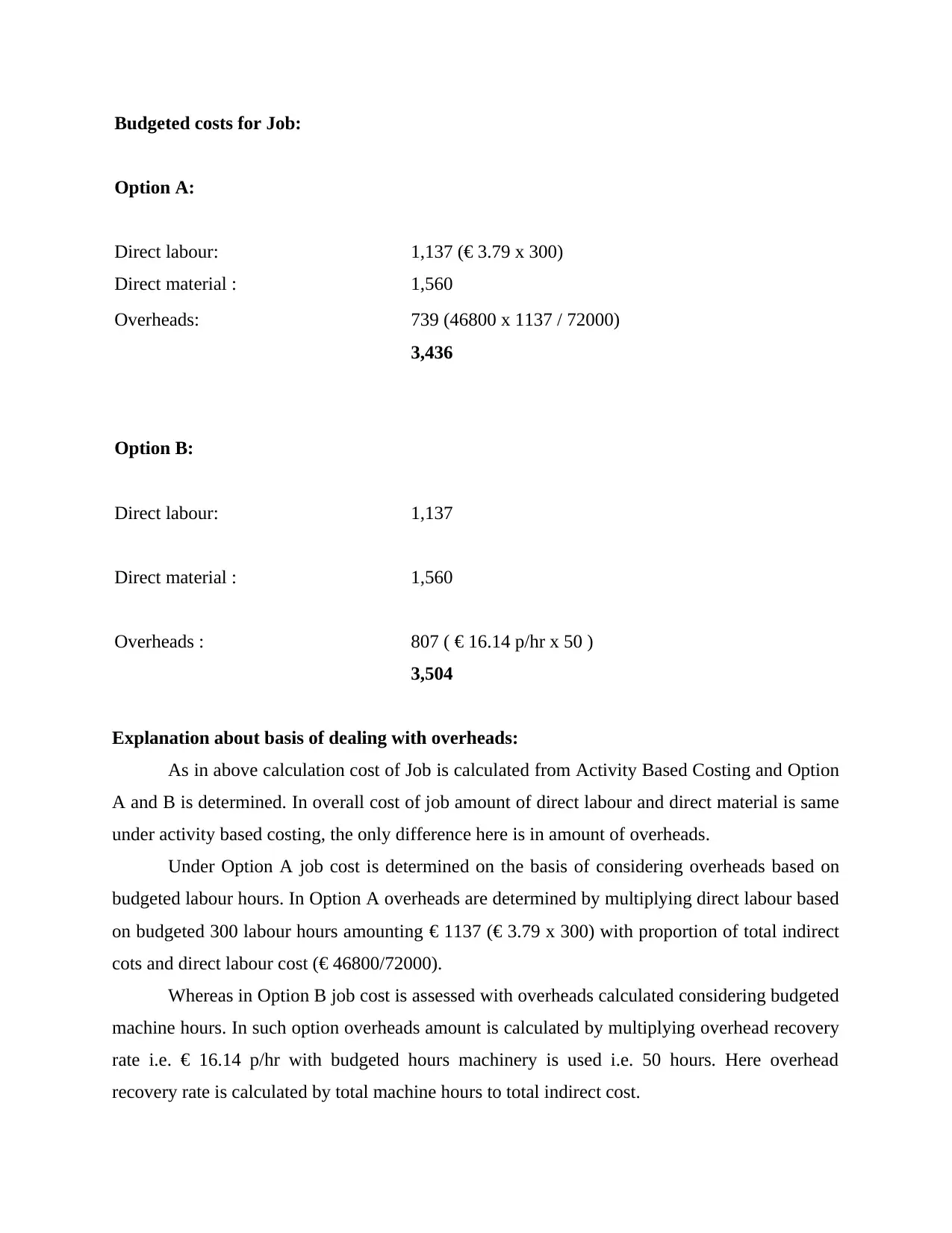

This report provides a comprehensive analysis of cost reduction techniques, focusing on financial principles and their application in maximizing profitability. It begins with an introduction to cost reduction as a crucial financial technique and then delves into practical calculations for job costing, including the determination of direct and indirect costs. The report explores the basis of dealing with overheads, comparing different methods like activity-based costing and traditional methods. The core of the report examines Activity Based Costing (ABC), highlighting its importance, advantages, and criticisms. It emphasizes how ABC improves accuracy and accountability in manufacturing activities by assigning overhead expenses more logically. The report also includes practical examples, such as calculating the cost of a job under different overhead allocation methods (Option A and Option B), and explains the importance of selecting the most appropriate method for cost reduction. It also discusses the benefits of ABC in terms of improving the understanding of overhead costs and cost drivers, and its role in making informed pricing decisions. The report concludes by summarizing the key findings and the benefits of applying financial techniques for achieving business objectives efficiently.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.